Elastic: Improved Sentiment May Not Be Justified

Summary

- Elastic's stock has performed well recently, on the back of improved sentiment from Elastic's exposure to generative AI and vector databases.

- While ESTC is well positioned to benefit from the use of generative AI in enterprise search, its competitive positioning in the relatively large observability and security markets remains weak.

- Elastic is no longer an obvious buy based on valuation alone, and further share price gains will likely require a significant improvement in growth/profitability.

gremlin

Elastic's (NYSE:ESTC) stock has performed well relative to the market in recent months on the back of stabilizing fundamentals and potential AI tailwinds. While Elastic retains a strong position within enterprise search, and vector databases provide a growth opportunity, Elastic's competitive positioning across its end markets is generally poor. As a result, investors should be cautious about overpaying for the stock.

Market

Elastic's platform gives it exposure to the security, observability and enterprise search markets. While security has been an area of strength in recent years, demand has been softening in 2023. Similarly, observability has been facing consumption headwinds from customer optimization efforts. It could be argued that Elastic stands to benefit from customer cost consciousness in security and observability though, as its platform provides a low-cost alternative to best-of-breed solutions. Elastic's search business is probably benefitting from generative AI hype at the moment as customers try to leverage the capabilities of LLMs.

Elastic stated on the Q1 FY2024 earnings call that the macro environment has been stable. While customers are ramping consumption of new workloads, customer acquisitions remain muted. This situation has led to Elastic's growth stabilizing at a relatively low level. Given Elastic's recent depressed valuation, stabilization appears to have been enough to improve sentiment toward the stock.

Elastic

Elastic has stated that generative AI has spurred a resurgence of interest in enterprise search, and as a result, the company has been focused on embedding LLMs in its products. This is still early though, as customers are grappling with how to best use the technology and how to implement it in a safe manner.

For LLMs to be safe and effective in enterprise search, a number of conditions must be met:

- IP must be protected and privacy policies followed

- The output of LLMs must be accurate, traceable and deterministic

- Customers should be able to use their own models or third-party models to generate embeddings from their data

Elastic is utilizing a similar architecture to resolve some of these issues as companies like C3.ai (AI). Elastic's Elasticsearch Relevance Engine (ESRE) is a search solution that is used to power generative AI solutions for private data sets with a vector database and machine learning models for semantic search. Vector embeddings are used to retrieve context using semantic search and help to enhance transformer model output at speed and scale. Elastic also provides both role-based and attribute-based access control to protect data and enables all data to be kept within a customer's network. Customers are reportedly already using ESRE to build generative AI applications using Elastic's vector search and hybrid search capabilities.

Elastic's background in search means that it is not just leveraging third-party LLMs in a search product. Elastic enables hybrid search using a combination of vector, semantic, and keyword search techniques to ensure the most relevant results possible. Elastic also continues to drive improvements in the speed and performance of the Elasticsearch platform, which is a differentiator at scale.

Elastic recently announced an AI Assistant for Observability, which leverages generative AI to reduce the learning curve for site reliability engineers and eliminate the need for manual data wrangling. The importance of this product offering is unknown at this stage though as many SaaS companies have launched AI assistants, meaning the solution is unlikely to be differentiated. It is also unclear how much utility these assistants will provide to customers and hence how much demand there will be.

Customers continue to consolidate multiple use cases on Elastic's platform and make large multi-year commitments in an effort to reduce total spend. A lot of these consolidations are reportedly around observability and security. For example, thousands of customers are now using Elastic for APM. Elastic typically leads with Log Analytics, Security Analytics and Search though. The extent to which customers standardize on Elastic's platform is an important value driver for Elastic, as it should lead to:

- Improved expansion rates

- Improved LTV/CAC

- Improved retention rates

Financial Analysis

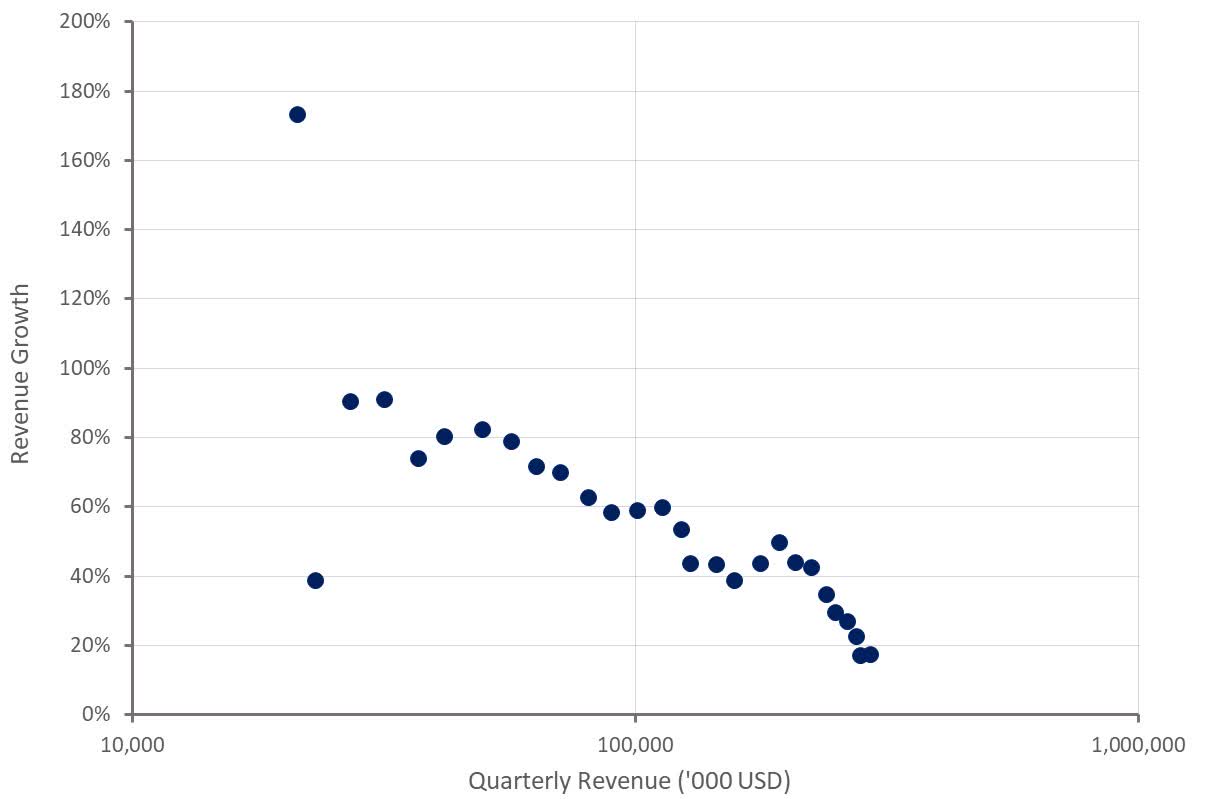

Elastic's revenue increased by 17% YoY in the first quarter of FY2024, with Elastic Cloud growing 24% YoY. Elastic Cloud contributed 41% of total revenue in the first quarter. Professional services revenue was 24 million USD, increasing 29% YoY. From a geographic perspective, EMEA was an area of strength during the first quarter, with APJ performing relatively poorly. Revenue in the second quarter of FY2024 is expected to increase 15% YoY. For the full fiscal year, Elastic expects revenue to increase 17% YoY.

Figure 1: Elastic Revenue Growth (source: Created by author using data from Elastic)

While Elastic continues to land new customers, and gross retention rates reportedly remain strong, customer acquisition continues to be difficult. Elastic's net expansion rate in the first quarter was 113%, indicating the extent to which Elastic is currently reliant on existing customers to drive growth.

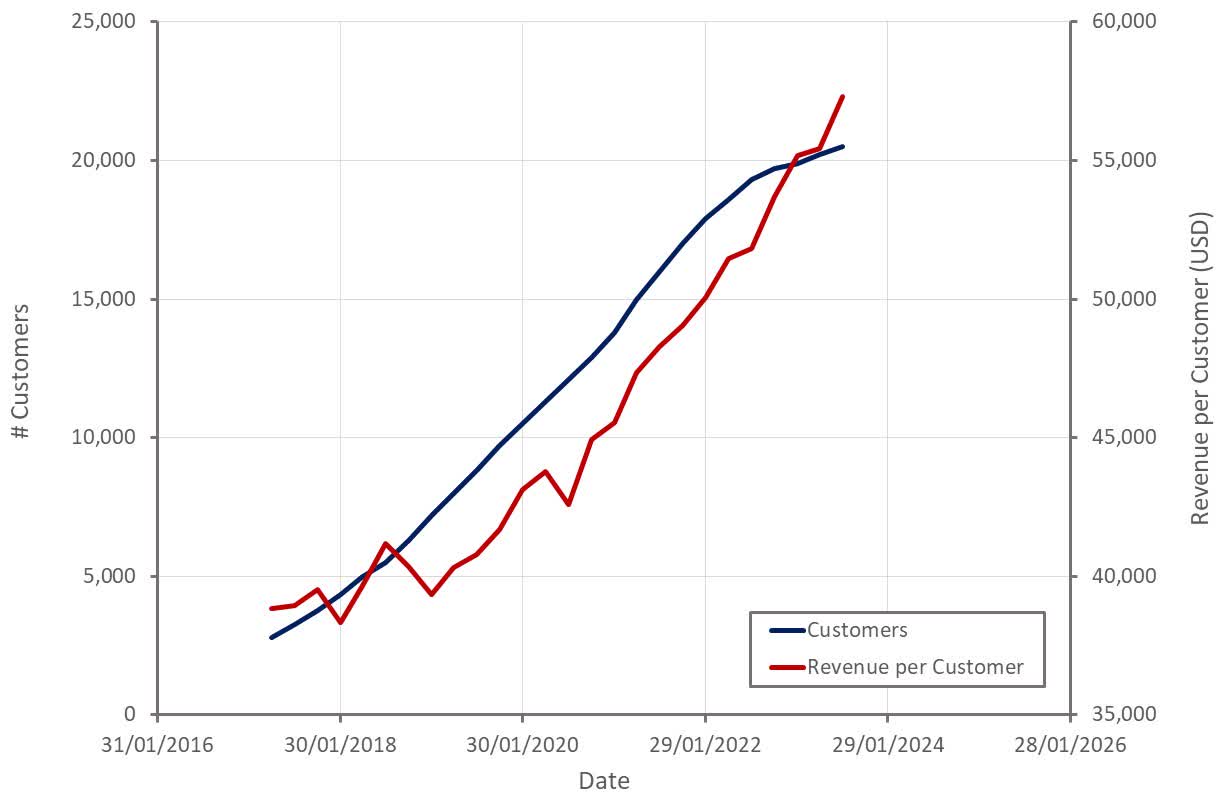

Figure 2: Elastic Customers (source: Created by author using data from Elastic)

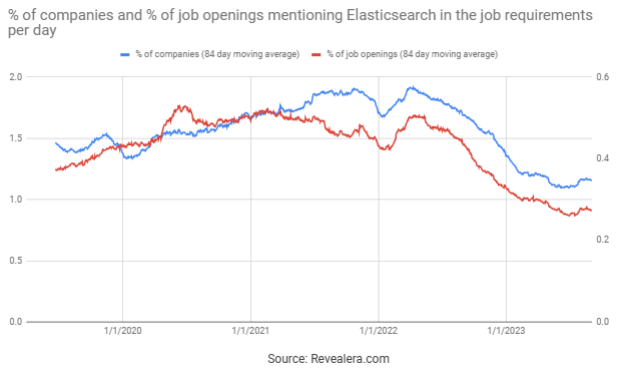

The number of job openings mentioning Elastic in the job requirements has not increased in recent months, which is unsurprising given Elastic's struggle to attract new customers. This somewhat undermines the generative AI-led growth narrative though. To support the recent move in share price, investors should look for Elastic to begin adding more customers in the coming quarters.

Figure 3: Job Openings Mentioning Elasticsearch in the Job Requirements (source: Revealera.com)

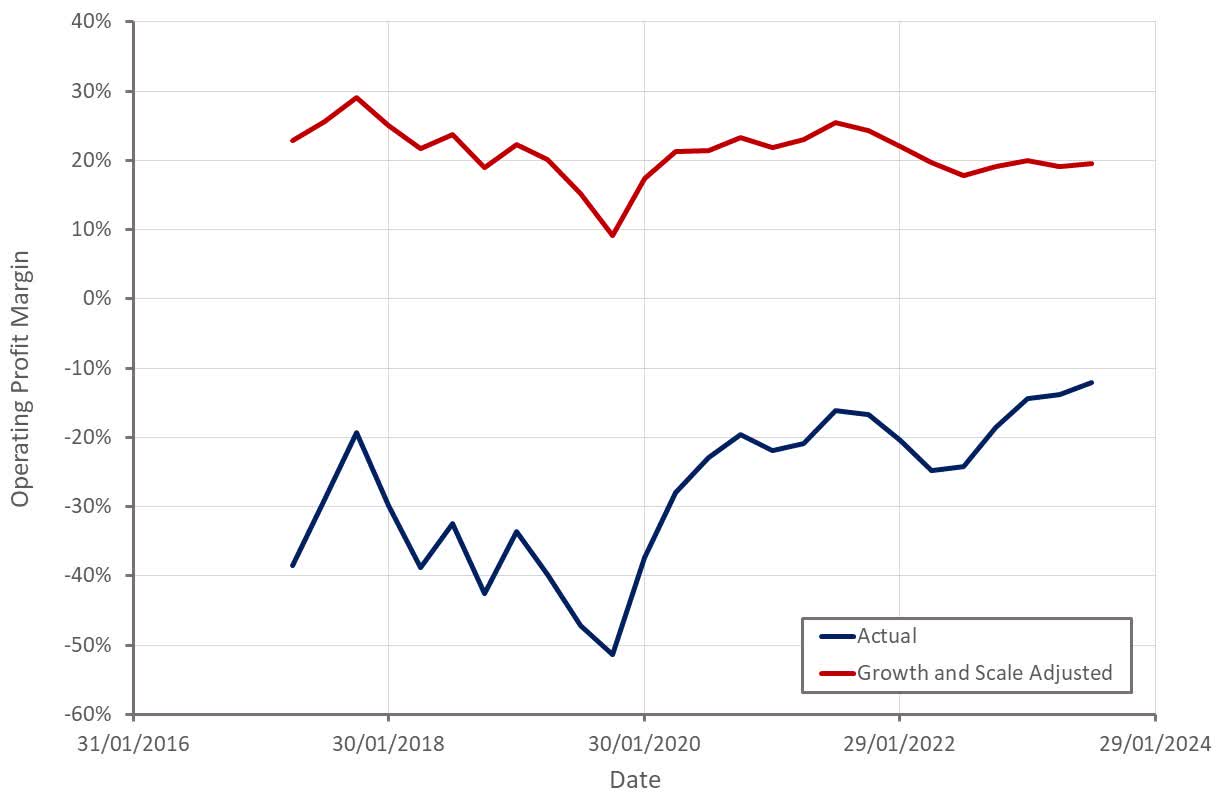

Elastic's operating profit margins continue to improve, which should be supportive of the stock price. Rather than an outright improvement in efficiency, this is more a reflection of Elastic's business continuing to scale and growth moderating. Elastic remains a reasonably efficient company that should eventually be profitable, although it is far less efficient than best-in-class SaaS peers.

Figure 4: Elastic Operating Profit Margins (source: Created by author using data from Elastic)

Valuation

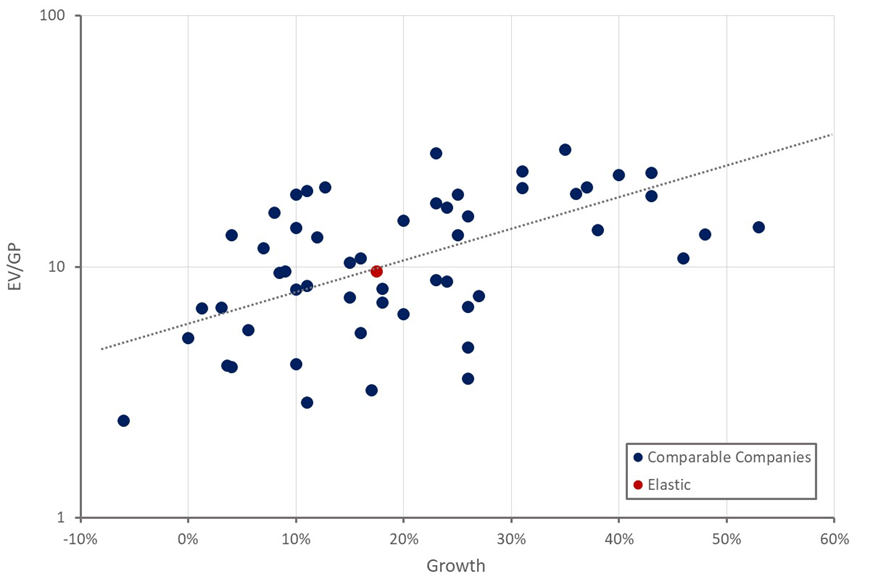

Elastic's stock is up roughly 70% from the lows in early 2023, and while the stock is still not overly expensive, it is also no longer an obvious buy on valuation alone. Based on its current growth and profitability profile, Elastic is priced broadly in line with comparable companies. While generative AI and its applications in enterprise search have improved investor sentiment towards Elastic, the company's competitive position in observability and security is weak and MongoDB (MDB) continues to expand the functionality of its transactional database into areas that compete with Elastic.

Figure 5: Elastic Relative Valuation (source: Created by author using data from Seeking Alpha)

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.