Depression Alert: Why The Shrinking Money Supply Spells Trouble For SPY

Summary

- The U.S. money supply is shrinking for the first time since 1949, with M2 declining by around $700 billion since the hiking cycle began.

- We look at the factors driving the shrinking money supply.

- We also look at the implications of this macro trend for SPDR® S&P 500 ETF Trust.

Adam Gault

The U.S. economy is currently experiencing a rare event that hasn't been witnessed since 1949: a shrinking money supply. M2 has declined by a whopping ~$700 billion since the hiking cycle began. This phenomenon is sparking discussions and debates about its causes, implications, and effects on various financial instruments, including the SPDR® S&P 500 ETF Trust (NYSEARCA:SPY).

In this article, we will explore why the U.S. money supply is shrinking and delve into its potentially negative implications for SPY and the broader financial landscape.

Why The Money Supply Is Shrinking

The recent contraction in the U.S. money supply is not solely due to a single, isolated cause. Rather, it is a result of a complex interplay of factors that have evolved over time, including changes in Federal Reserve policy, rising interest rates, financial innovations, and shifts in market dynamics.

Federal Reserve, Goldman Sachs Research

We will discuss the three most prominent of these factors below:

Fed Quantitative Policy: One significant contributor to the shrinking money supply is the change in Federal Reserve policy away from quantitative easing and towards quantitative tightening. The Fed has been reducing its massive $8 trillion balance sheet (so far to the tune of $800 billion), which in turn has had a direct impact on savings deposits because as the Fed rolls off assets like Treasuries and mortgage-backed securities as they reach maturity, it reduces the money supply since these assets instead need to be financed by bank deposits or other forms of money.

Rising Interest Rates: Additionally, rising interest rates - which have pushed yields higher in numerous financial products such as money markets - have discouraged individuals and institutions from keeping their funds in low-yield savings and checking accounts, leading to a decline in deposits:

Federal Reserve, Goldman Sachs Research

Financial Innovation: Moreover, the continued growth in credit and debit card adoption by consumers has reduced the reliance on physical cash for everyday transactions, while the years of ultra-low interest rates, the growing digitization of financial markets, and the rise of user-friendly commission-free trading apps like Robinhood (HOOD) have made it easier and more attractive for households to allocate their savings to investments rather than traditional bank deposits. Yes, interest rates have risen recently, but many individuals have already been activated as investors and have formed the habit of allocating excess savings to stocks rather than to a bank savings account.

These three major factors have led to a staggering ~$2.4 trillion decline in savings deposits since the Federal Reserve began hiking interest rates in early 2022.

The Implications for SPY

So what does the shrinking U.S. money supply mean for SPY? The reality is quite nuanced.

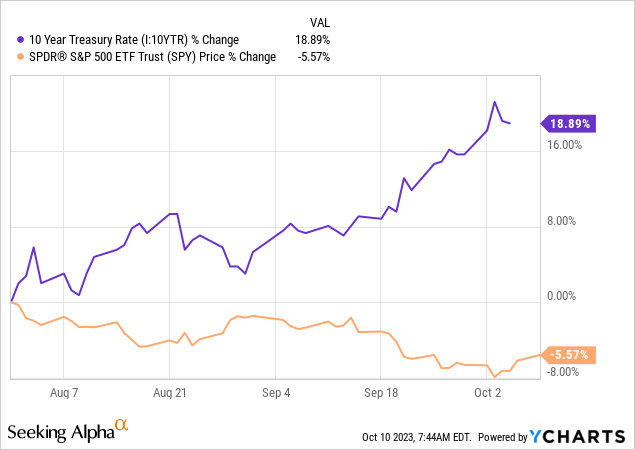

One of the most accurate ways of measuring the relationship between the money supply and SPY performance is its impact on interest rates, though the relationship between interest rates and stock market performance is complex. Rising interest rates can make bonds and other fixed-income assets more attractive relative to stocks. As investors seek higher yields in bonds, there might be a shift away from equities like those in SPY, thereby hurting its performance. We have seen this dynamic at play recently as surging bond yields have weighed on SPY's performance:

Data by YCharts

Data by YCharts

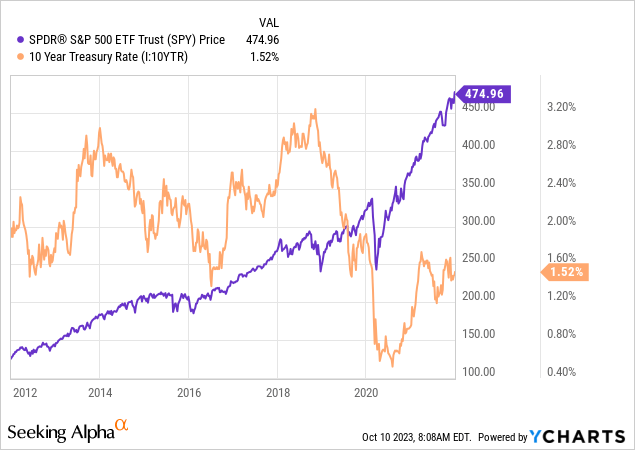

Conversely, when interest rates are very low, investors seeking returns are inclined to invest in riskier assets like stocks, driving their prices higher due to increased demand. This was one of the main reasons why SPY boomed over the decade between 2012 and 2021, especially in the aftermath of the COVID-19 outbreak:

Data by YCharts

Data by YCharts

Another reason why interest rates have an impact on SPY is that - when market interest rates rise - it becomes more expensive for companies to borrow money for profitable projects, leading to higher interest payments and lower profits. In some cases, projects may become unfeasible. Lower profits translate to lower stock prices because stock prices are a reflection of a company's future earnings. Conversely, when interest rates fall, companies can borrow more easily, boosting profits and economic growth. A classic recent example of this was seen at NextEra Energy Partners (NEP), where management just slashed its target growth rate in half due to a soaring cost of capital.

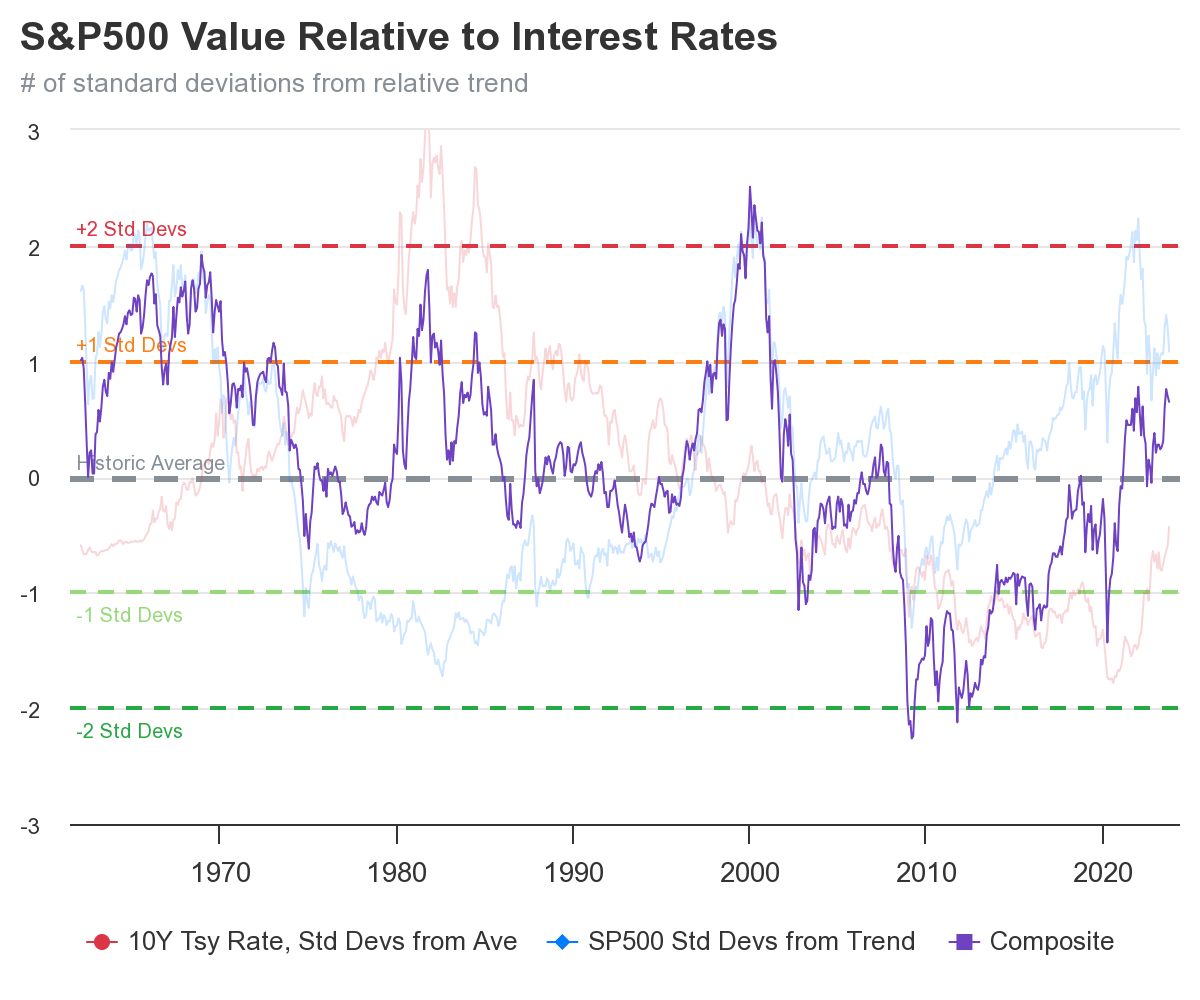

Moreover, Goldman Sachs research suggests that interest rates are one of the more reliable indicators for estimating the impact of tighter monetary policy and financial conditions on the economy, which in turn can assist us with predicting SPY performance. In fact, one of the more prominent S&P 500 valuation models in use today is known as the Interest Rate Model:

Interest Rate Model (currentmarketvaluation.com)

That said, while interest rates certainly do play a prominent role in the behavior of stock markets, they are also influenced by a myriad of other factors, including investor sentiment, economic conditions, corporate earnings, and geopolitical events. While changes in the money supply can play a role in shaping economic conditions, they are just one piece of the broader puzzle. As a result, historical data reveals that relying solely on monetary aggregates for predicting market performance can be unreliable.

Fortunately for SPY, its top holdings are in cash-rich technology mega-cap stocks like Apple (AAPL), Microsoft (MSFT), Amazon (AMZN), Nvidia (NVDA), Alphabet (GOOG, GOOGL), Tesla (TSLA), and Meta (META) as well as one of the strongest conglomerates in the world in Berkshire Hathaway (BRK.A, BRK.B):

Seeking Alpha

This should make it more resistant to higher for longer interest rates than some other financial instruments out there. That said, there are still reasons to be concerned. First of all, SPY is quite overvalued based on several leading valuation models such as the Buffett Indicator, the Price/Earnings Model, the S&P 500 Mean Reversion Model, and the Yield Curve Model.

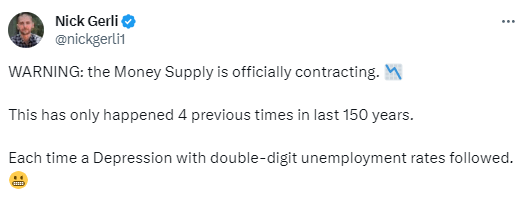

Moreover, as a recent tweet pointed out:

X.com

When a contraction in the money supply is coupled with inflation, such as we are seeing now, there is an elevated threat of the market and broader economy experiencing a deflationary crash. This would undoubtedly have a terrible impact on SPY. Similar circumstances occurred in the post-World War I era and the Spanish Flu pandemic, resulting in 11% deflation and high unemployment. A mere -2% contraction in the money supply in 1921 triggered this deflationary depression, and currently, in 2023, we are already at a -2% contraction. This suggests that the economy's resilience and the current inflation may not be as robust as believed.

re:venture consulting

While the money supply in 2023 is substantially higher than pre-pandemic levels, history indicates that depressions and deflation do not require a linear decrease in the money supply but can result from even a slight contraction of 2-4% year-on-year. Many expect the current inflation to persist indefinitely, akin to the 1970s, but the key difference is that the Federal Reserve is engaged in Quantitative Tightening right now, causing the money supply to contract. As a result, economic history seems to indicate that a deflationary depression in the near future is a possibility unless the Federal Reserve changes course away from QT.

Investor Takeaway

The currently shrinking U.S. money supply is a historically rare and complex phenomenon driven by multiple factors, including changes in Federal Reserve policy, rising interest rates, and financial innovation. While there are reasons to believe that it could bode poorly for SPY - particularly given that rising interest rates often follow and are mechanically bad for equity valuations, SPY appears to be overvalued based on numerous models, and a shrinking money supply dramatically increases the chances of depression - it is also important to keep in mind that the relationship between the money supply and stock market performance is not straightforward.

As a result, while this analysis does lead us to be bearish on SPY and rate it a Sell, we do not think that long-term investors should overreact, sell everything, and "head for the hills" in a panic. However, it does emphasize the importance of proper diversification and having a financial plan that does not depend on liquidating SPY shares for several years to come.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.