Ross Stores: A Trade-Down Beneficiary, But At A Price

Summary

- Ross Stores has massively outperformed XRT with a 50% increase in its stock despite a single-digit gain for the sector.

- This has been helped by strong Q2 results with an 8% increase in revenue, prompting the company to raise annual EPS guidance by ~9% while maintaining a cautious outlook.

- However, while Ross Stores has been somewhat of an all-weather stock and been a standout performer during recessionary environments, it's hard to justify chasing the stock above $117.00.

Wolterk

Just over a year ago, I wrote on Ross Stores (NASDAQ:ROST), noting that while the macro environment looked to be worsening, any pullbacks below $70.00 would provide buying opportunities given that much of this was priced into the stock. Since then, the stock is up over 50% despite a single-digit gain for the Retail Sector (XRT). This outperformance can be attributed to Ross Stores' positioning as a trade-down beneficiary, opportunistic buybacks to boost its per share metrics, and strong execution in Q2 with Ross Stores taking annual EPS guidance higher by ~9% at the mid-point. In this update, we'll dig into the recent results, the H2-23 outlook, and where the stock's updated low-risk buy zone lies after a year of outperformance.

Recent Results & Updated FY2023 Outlook

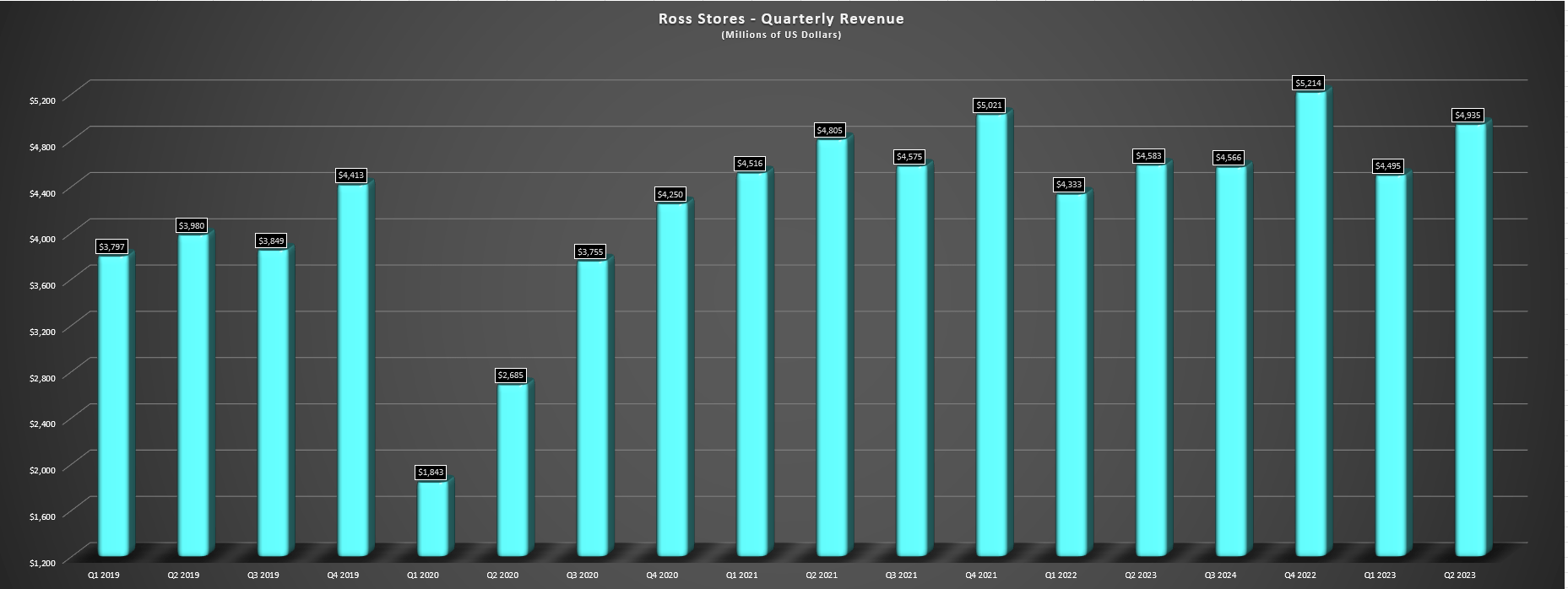

Ross Stores released its Q2 results in mid August, reporting quarterly revenue of ~$4.93 billion, an 8% increase year-over-year. This was driven by comp sales growth of 5% (3% year-to-date) on the back of higher traffic, with the company noting that sales and earnings were "well above expectations". This translated to an improvement from Q1 results when Ross Stores noted that results were in line, and the company also noted that DD's Discounts (its more sensitive concept) improved in Q2, with this brand having a lower average household income of ~$45,000 vs. ~$65,000 at Dress For Less stores at the high-end. Meanwhile, quarterly earnings per share improved to $1.32 vs. $1.11 in the year-ago period (+19% year-over-year), benefiting from significant share repurchases over the past year (including ~2.2 million at ~$104.50 in the most recent quarter).

Ross Stores - Quarterly Revenue - Company Filings, Author's Chart

Digging into the results a little closer, Ross Stores noted that customers responded well to its value offerings in the period, and that cosmetics and accessories were stand-out categories yet again in Q2, similar to its Q1 2023 results. In addition, the company noted that Home performed above the chain average which was consistent with TJX Companies (TJX) results, with TJX noting that Home was improving and had returned to positive comps. Overall, Ross Stores attributed to the better performance despite the difficult macro environment to a better merchandise assortment but did share that it expects a very promotional holiday season. That said, despite continuing to take a cautious approach which is how it entered the year, the company surprised investors with a significant raise in its annual EPS outlook, now targeting $5.19 per share (+19%) at the mid-point, up from a previous outlook of $4.65 - $4.95.

Positioning In Macro Environment

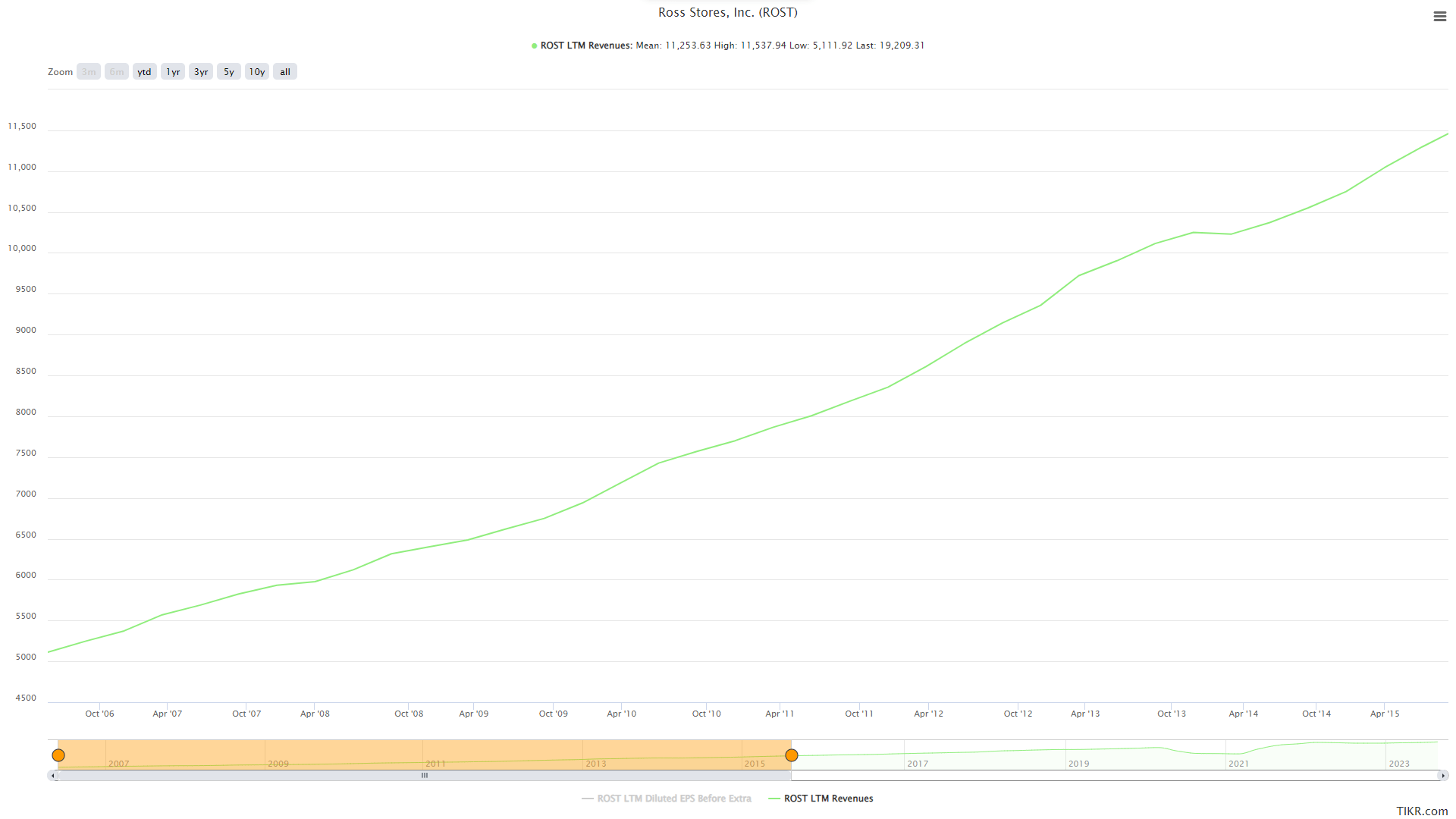

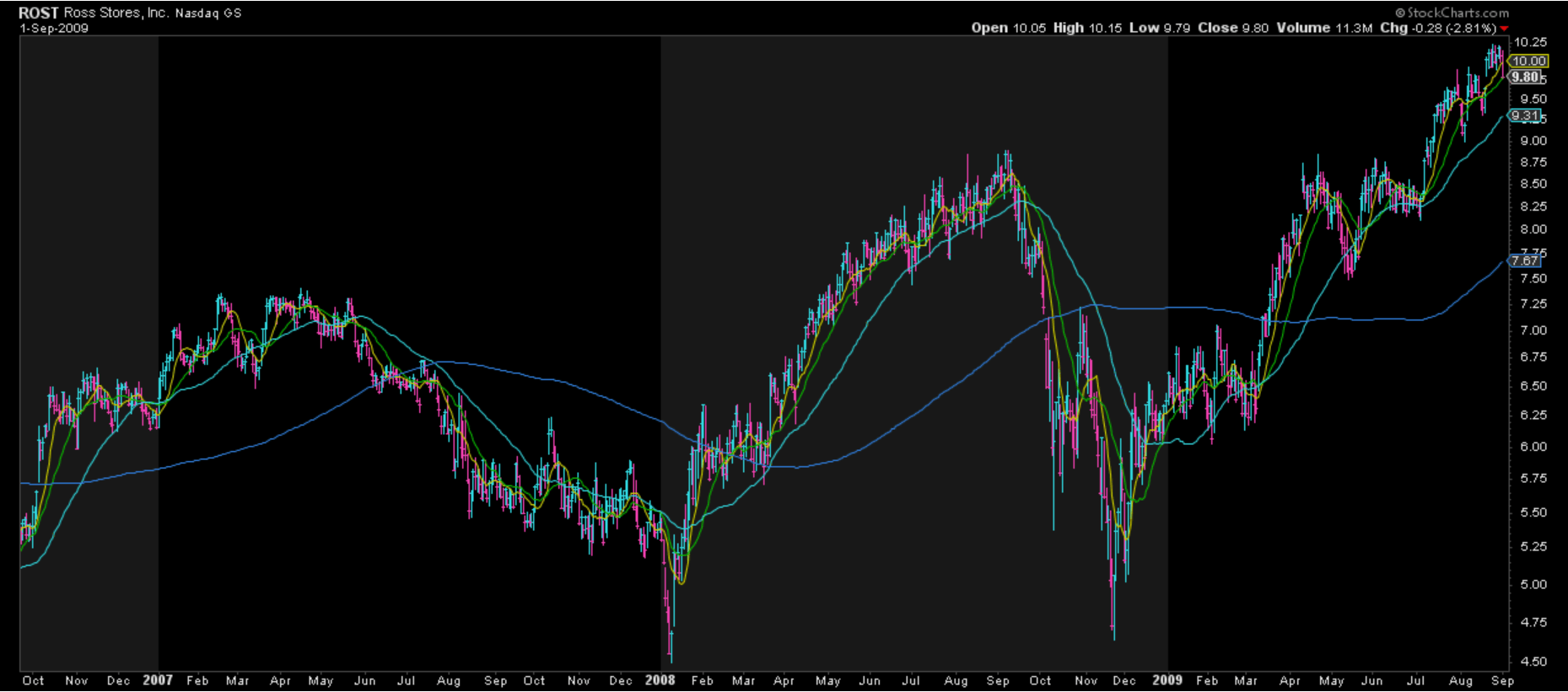

Overall, this strong performance is not overly surprising, with Ross Stores being one of the few standout names during the Great Financial Crisis in 2008 to grow sales and earnings, with the latter helped by its opportunistic share repurchases. In fact, the company reported 2% comp sales growth and 9% sales growth in FY2008 and repurchased ~$300 million worth of shares at ~$8.00 per share, and also grew its units by an impressive 7% while others were reporting closures. And it's this resiliency to a more difficult macro environment (trade-down beneficiary) and hunger to buy more than its fair share of its common stock when its share price is down that has made helped it to perform so well over the past 20 years (~18% annualized).

Ross Stores - TTM Revenue (2006-2015) - TIKR.com

ROST Stock Chart (2007-2010) - StockCharts.com

As for industry-wide trends, there's certainly been carnage in the Retail Sector (XRT) from a share price standpoint, and while retail sales were up 0.70% in September and beat estimates, the macro environment remains challenging. Record credit card debt and personal savings rates that continue to trend lower are evidence of this, and it certainly doesn't help that gas prices are not pinching wallets further, putting further strain on less affluent customers. Fortunately, this isn't Ross Stores' first rodeo, and the company certainly has the balance sheet to support unit growth (targeting 100 stores this year or ~5% growth) and continued share repurchases with ~$2.1 billion in debt and growing interest income because of the high-rate environment. So, the company is certainly better positioned than its peers and can be thought of as a defensive way to play the sector.

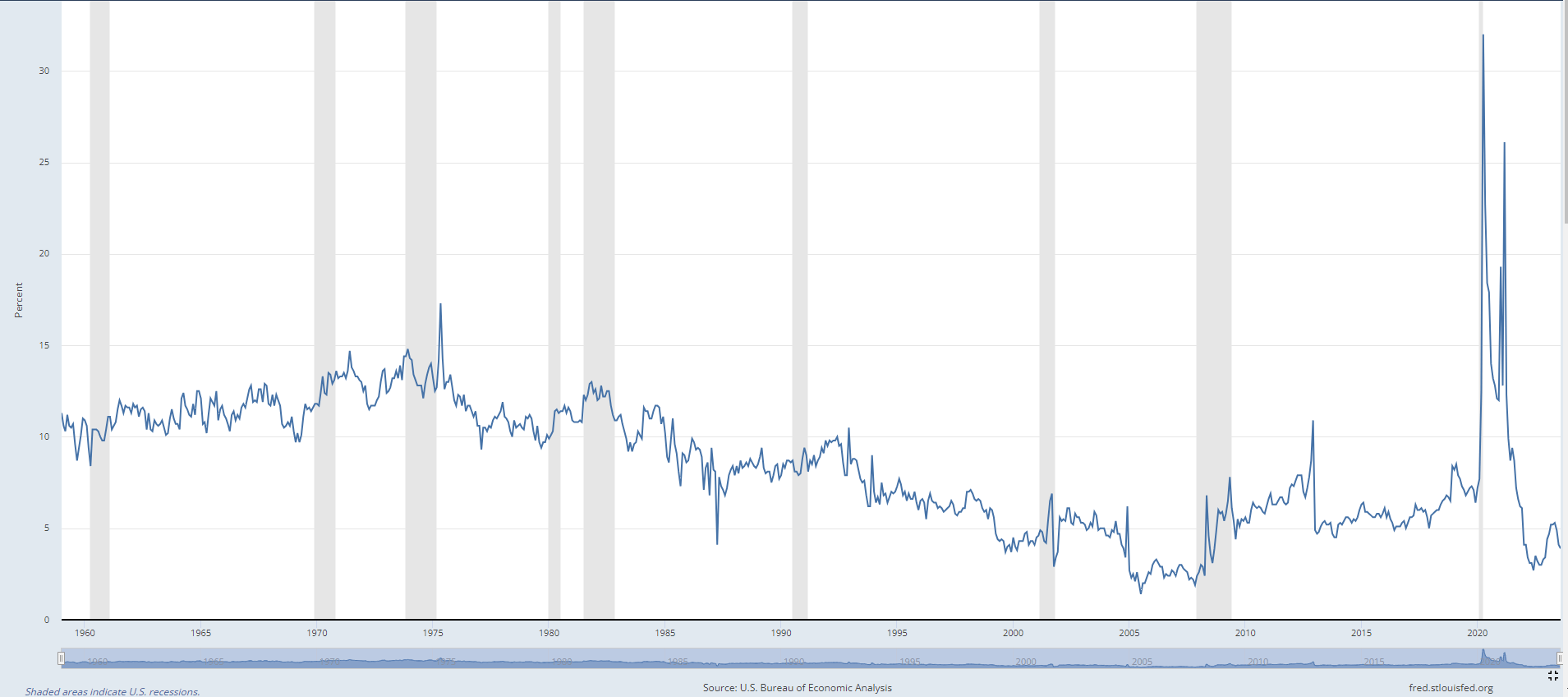

Personal Savings Rate - BLS, FRED

There's no question that Ross Stores has been an all-weather name for a portfolio and although DD's is more sensitive with exposure to a less affluent customer, it's nice to see an improvement in the most recent results. That said, while there's nothing wrong with owning a recession-resistant retailer and defensive names have certainly enjoyed a strong bid since the cyclical bear market in the S&P 500 (SPY) began in Q1 2022, these gains can evaporate quickly if one chases trends, just like we've seen from many staples names like Hershey (HSY), Coke (KO), and Hormel (HRL) to name a few. And while Ross Stores was undoubtedly on the sale rack in Q3 2022 in what was a tougher year, it's hard to argue that this is the case here, even if the stock remains reasonably valued given its strong track record. Let's take a closer look at its valuation:

Valuation

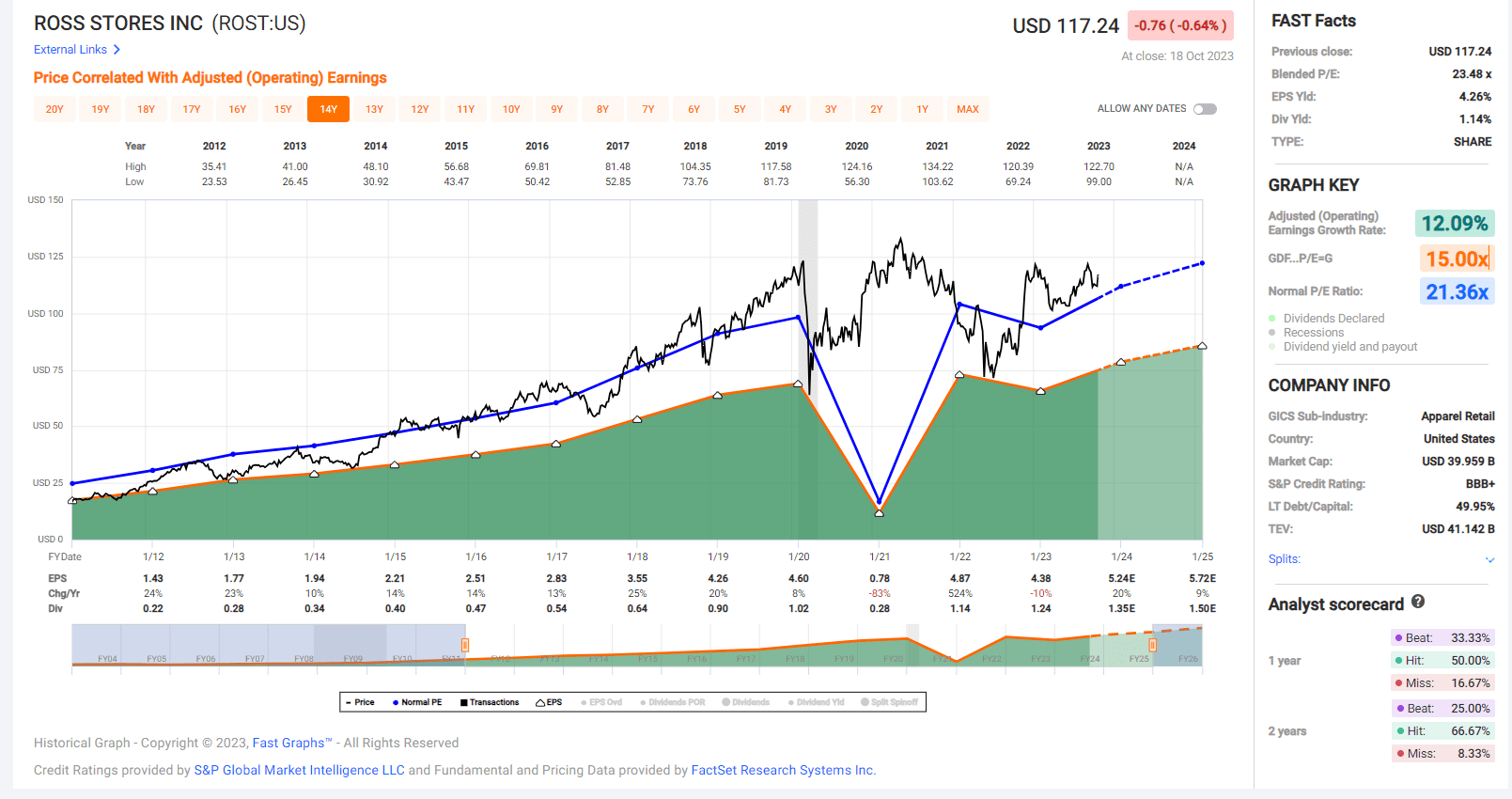

Based on ~339 million shares and a share price of $117.00, Ross Stores trades at a market cap of ~$37.7 billion and an enterprise value of ~$40.8 billion. This makes it one of the highest capitalization names in the sector, just behind the off-price leader by market cap, TJX Companies. And from a valuation standpoint, ROST trades at a discount to TJX from a free cash flow multiple and earnings standpoint, trading at ~24x CY-24 EV/FCF vs. TJX at ~29.0x, and ~20.3x CY24 annual EPS estimates vs. TJX at ~22.0x, respectively. Finally, if we look at how ROST stacks up vs. its historical multiples, we can see that the stock is hovering below its long-term average (15-year) of ~21.4x annual EPS based on FY2024 annual EPS estimates of $5.70.

Ross Stores Historical Earnings Multiple - FASTGraphs.com

Using what I believe to be a fair multiple of 22.0x earnings for Ross Stores and FY2024 annual EPS estimates of $5.75, I see a fair value for the stock of $126.50. This points to an 8% upside from current levels and a 9% upside from a total return basis. However, while Ross Stores benefits from being defensively positioned as an off-price name and trade-down beneficiary vs. full-priced peers in the space, I am looking for a minimum 20% discount to fair value when buying large-cap names, and ideally closer to 25%. And even if we use the lower end of this discount range, the stock's ideal buy zone comes in at $101.20 or lower. So, although the stock was a steal last year when I highlighted it as a Buy under $70.00, it's hard to argue for chasing the stock today with it over 65% off its lows and trading at only a slight discount to fair value.

Ross Stores - October 2022 Update - Seeking Alpha PRO

Summary

Ross Stores has massively outperformed the S&P 500 (SPY) over the past year with TJX Companies with an average return for the two of ~48% vs. a ~22% gain for SPY. And while Ross Stores still remains reasonably valued given its solid execution and it being one of the few retail names to raise its FY2023 guidance (and by a whopping 9% at the mid-point), I prefer to buy at the right price or pass entirely, especially in a volatile market with macro and geopolitical risks. Hence, while I think it is certainly one of the better-run names in the space, I don't see any reason to pay up for the stock above $117.00. So, if I was looking to put new capital to work in Consumer Discretionary, I see Aritzia (ATZ:CA) as the better bet, trading at barely ~13x CY2024 earnings estimates.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.