Restaurant Brands: Further Weakness Should Present A Buying Opportunity

Summary

- Restaurant Brands put together phenomenal results in Q2 at Tim Hortons and BK International, and it has initiatives in place to grow AUVs and profitability in its other brands/markets.

- Unfortunately, the company is coming up against tough industry-wide traffic trends that have leaked into quick-service traffic as well, setting up a tougher Q3 on deck.

- In this update, we'll look at recent progress, industry-wide trends, its valuation relative to peers, and whether the stock is worthy of owning ahead of its upcoming Q3 results.

sarayuth3390

It's been a challenging year for the restaurant industry group which was up ~23% as of summer measured by the AdvisorShares Restaurant ETF (EATZ), but has since given up nearly all of its gains. This unfortunate trend change can be attributed to what continues to be a difficult macro environment for consumer discretionary, and what's become a more competitive environment for restaurants (elevated promotions) due to an overall decline in traffic. That said, while many names continue to make new lows like Portillo's (PTLO) and Denny's (DENN) after coming into the year with little margin of safety, Restaurant Brands (NYSE:QSR) has been an exception, making new all-time highs in July before pulling back recently.

In this update, we'll look at its recent results across its four brands (Burger King, Popeyes Chicken, Firehouse Subs, Tim Hortons) industry-wide trends, and whether it's worth buying ahead of the upcoming Q3 results.

Popeyes Chicken - Company Presentation

Introduction

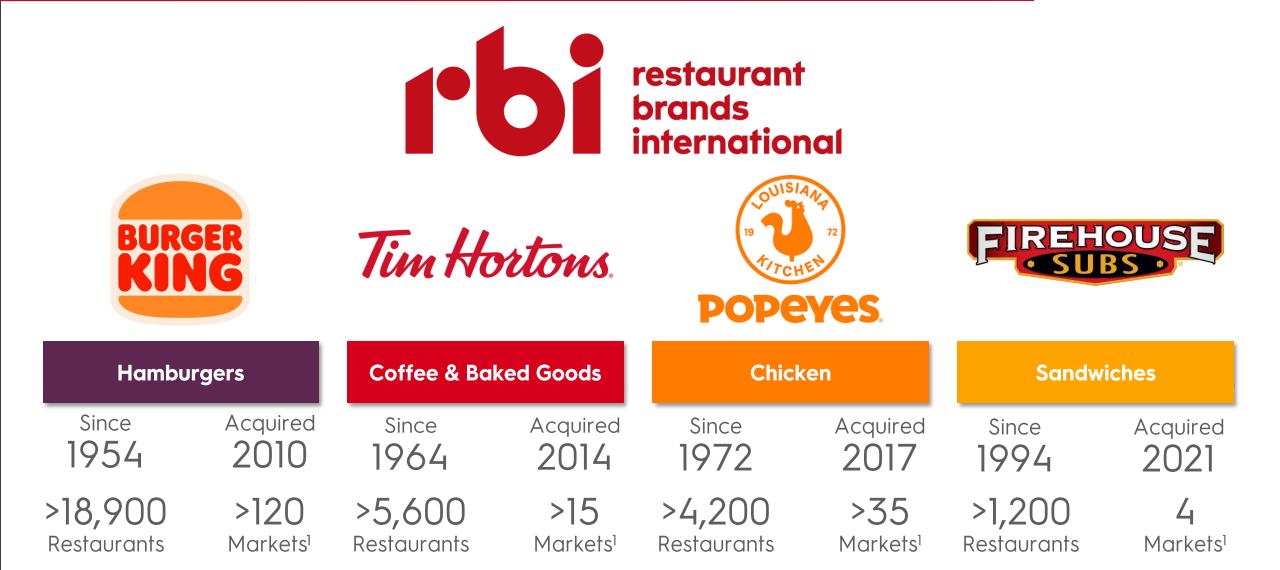

Restaurant Brands International is a franchisor in the restaurant industry group that began trading in late 2014 at the time of its Tim Hortons acquisition that gave it two concepts from one previously (solely Burger King). The company has continued to grow organically and through acquisition since then, acquiring sandwich store Firehouse Subs and Popeyes Chicken, and growing its store base from ~19,000 to 30,000+ as of the most recent quarter. Meanwhile, the company has consistently maintained one of the highest percentages of stores franchised under its system, increasing to 99% to 100% as of year-end 2022. This gives it an asset-light model relative to operators like Darden (DRI) and while it is relatively saturated in North American among its two largest brands (Burger King, Tim Hortons), the domestic and international opportunity is significant for Popeyes/Firehouse Subs, and all brands, respectively.

Restaurant Brands Concepts - Investor Presentation

Recent Results & Q3 Outlook

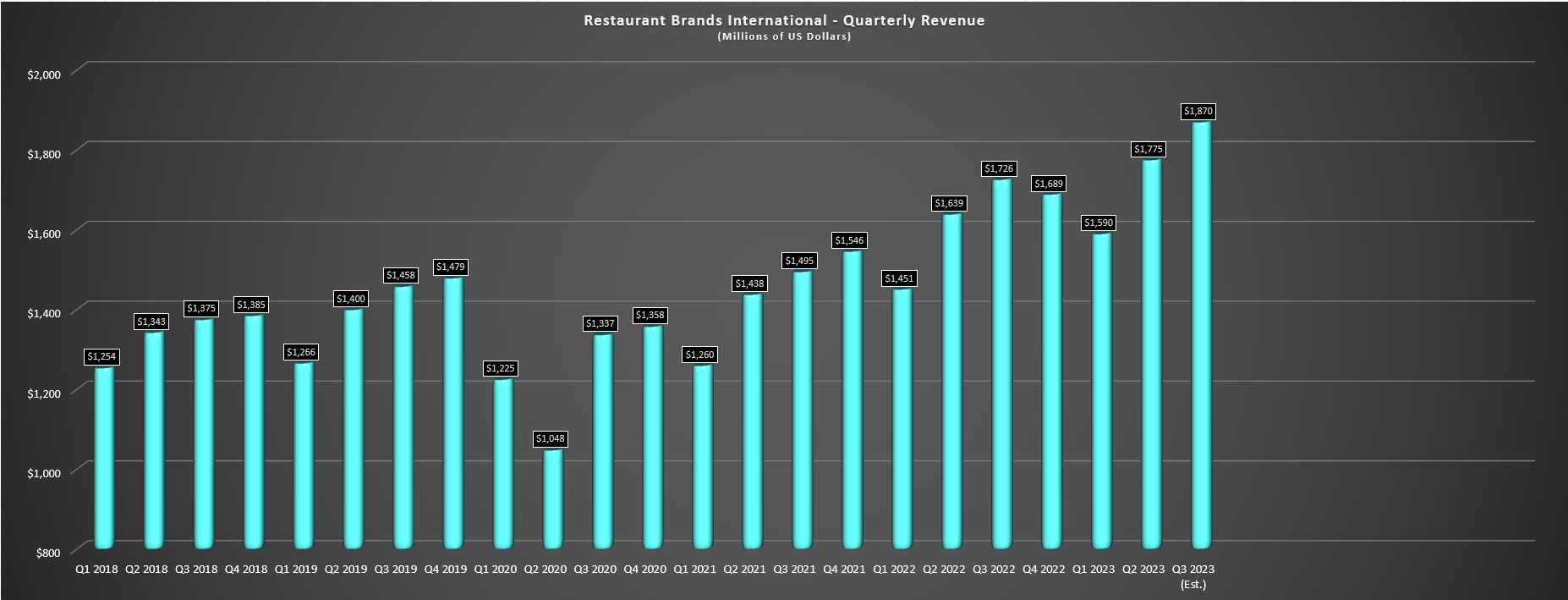

Restaurant Brands had a blowout quarter in Q2 relative to many of its peers, reporting global comparable sales growth of 10%, system-wide sales of 14%, and net restaurant growth of 4% (169 net new restaurants). This translated to record revenue of ~$1.78 billion, adjusted earnings per share of $0.85 (+7% year-over-year), and free cash flow of ~$380 million excluding Reclaim the Flame investments. Digging into the results a little closer, Tim Hortons and Burger King International were the star performers, with 15% and 18% system-wide sales, respectively against a backdrop of declining industry-wide traffic. Looking at Tim Hortons a little closer, the company reported a 23.6% 2-year stack for comparable sales, enjoyed improved speed of service, and has continued to grow rapidly and take market share in PM food (+14.2% year-over-year) and cold beverages (+16.6% year-over-year), while retaining its impressive market share in coffee and breakfast of ~70% and ~60%, respectively.

Restaurant Brands Quarterly Revenue & Q3-23 Estimates - Company Filings, FactSet, Author's Chart

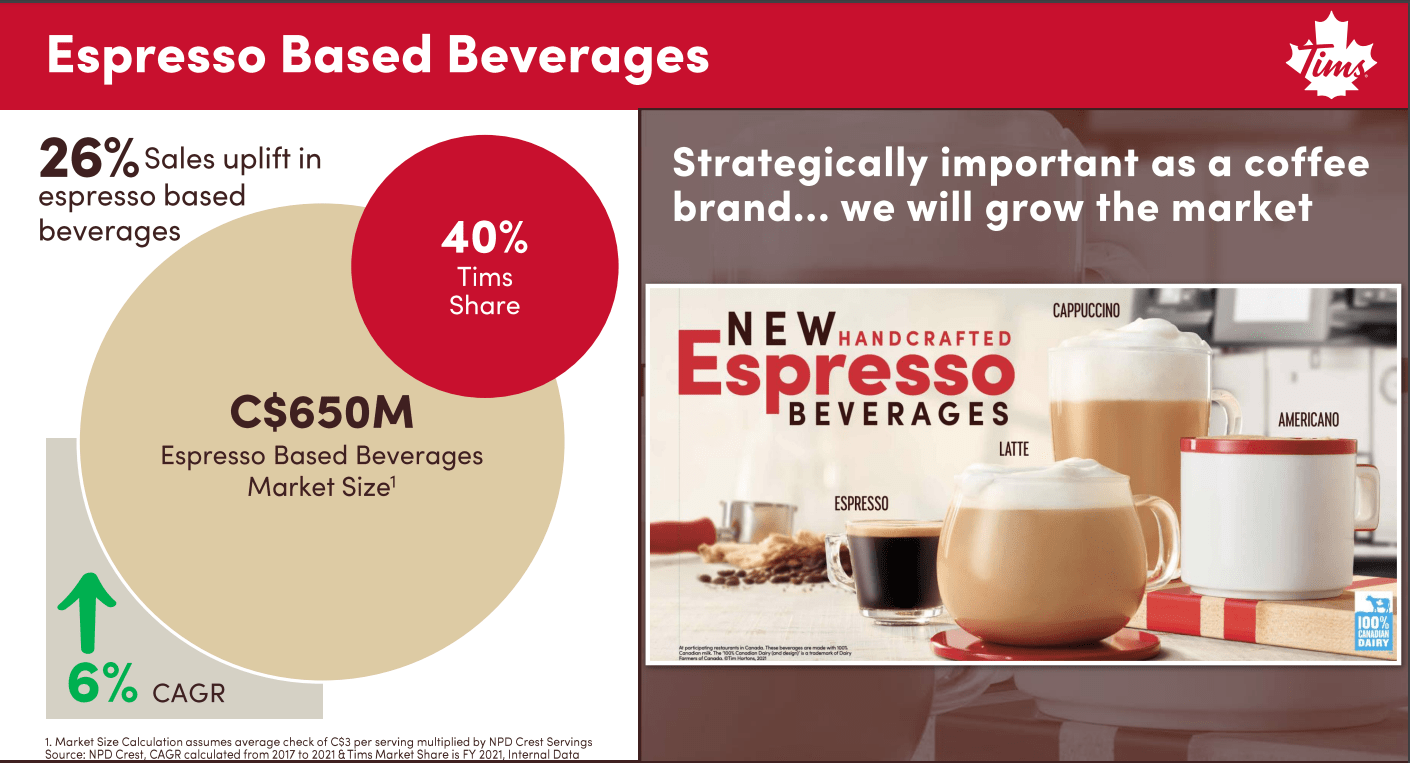

Notably, these results were achieved despite lapping more difficult comps from the Justin Bieber collaboration last year, and the company continues to see the opportunity for growth for this concept being taking additional market share in PM daypart which its wraps/bowls have resonated, and expanding internationally. Importantly, the company noted that its PM menu items have led to improve preference measures for younger guests and appear to have added frequency for existing guests that typically visited the restaurant mainly for breakfast and snacks only. Finally, from a digital standpoint, the company is knocking it out of the park, with ~5.0 million daily average users (+23% since Q4 2022), representing ~13% of Canada's population on its Tim Rewards App.

Tim Hortons Espresso Opportunity - Company Presentation

Moving over to Burger King, international had another incredible quarter which makes up ~60% of Burger King's system-wide sales, with 11.6% comp sales growth, positive traffic and a higher average check. And while this was partially offset by Burger King US, its domestic market had a decent quarter with 8.3% comp sales, benefiting from the SpiderVerse Whopper which helped bring in younger guests while not impacting its core whopper volumes. However, although US lagged, we appear to be nearing an inflection point, with remodels set to begin later this year as well as investments in technology and back-of-house equipment as part of its $400 million Reclaim the Flame program. As it stands, the company has been investing modestly while focusing on food first with training on Whopper quality, but AUVs should start accelerating with investments in equipment, technology, and modernized stores with its remodels over the next 6-18 months.

The company's Executive Chairman Patrick Doyle also noted that it is looking at kiosks at Burger King where it's seen better guest reception than in the past which could help to offset some labor costs and allow its team members to focus on delivering excellent service with more time freed up. And assuming these initiatives are successful (which the company appears very confident), a return to growth for Burger King US would allow the company to see its net restaurant accelerate back towards the ~6% range from ~4%, with higher franchisee profitability helping to improve development for this lagging area of the system. Hence, I remain very confident in Burger King's turnaround domestically and it's important to note they aren't re-inventing the wheel here, just bringing learnings back home from international where the company is executing near flawlessly.

"And then if you look at what I think is pretty extraordinary story within all of this. You know, if you look at the net restaurant growth in the rest of the world for the other concepts, you've still got rest of the world growth north of 5% for BK in the rest of the world, but you're at 24% on Tim Hortons, 27% on Popeyes, 48% on Firehouse. Those are big businesses and as they continue to scale, plus hopefully getting some incremental growth from Firehouse in the U.S. and from Tim Hortons in the U.S., I mean it just - the picture says that 5% starts looking very, very doable."

- Restaurant Brands International, Executive Chairman, Patrick Doyle

Finally, on the company's two smallest brands, two-year stacked same-store sales lagged, with Popeyes seeing 7.7% two-year stacked same-store sales (15% system-wide sales on back of strong unit growth), and Firehouse Subs saw 0.3% two-year stacked same-store sales growth. However, it's worth noting that Firehouse Subs did see a 1% impact from extended downtime with its technology provider, NCR, impacting results in the period. And while Popeyes performance has lagged, the company is confident that it can re-accelerate growth with its Easy To Love strategy (aimed at growing four-wall profitability to $300,000 by year-end 2025). And in addition to menu innovation, the company will be looking to remodel Popeyes kitchens to allow for faster and more accurate service. Not only should this improve guest satisfaction and allow for higher AUVs, but it should also help with team member retention as duties are less complex, and it's a better overall work experience.

Finally, as for Firehouse Subs, the brand did lag my expectations, but I continue to be very bullish on the long-term opportunity here, and it's nice to see an entrance into fast-casual with a brand that has strong community support (portion of purchases go to Firehouse Subs Public Safety Foundation - $65+ million since 2005), a solid digital presence given its size (3.5+ million loyalty members), and considerable whitespace with its first restaurant opened internationally in Switzerland, and still a relatively small presence domestically (1,260 restaurants). Notably, the company recently landed an agreement for 100 Firehouse locations over the next decade across UAE and Oman by partnering with Apparel Group, and added a new CMO in Dena vonWerssowetz, an extremely bullish development with Dena bringing 14 years of experience from PepsiCo (PEP), leading the portfolio transformation and innovation for its International Beverages division.

To summarize, the Q2 results were exceptional, and the company appears more confident than ever that it can push growth further, with its previous 2029 goal (stated in 2019) being to have 40,000+ restaurants across its system. Given the addition of another concept in Firehouse Subs, this looks more than doable, and this growth combined with improved sentiment around its Burger King US should help the stock to trade at a premium multiple later this decade and play catch-up with some of its best-in class quick-service peers on valuation.

Industry-Wide Trends

That said, while the company has executed successfully in regards to what it can control and is taking market share in PM foods and cold beverages in Canada at Tim Hortons, the macro environment remains challenging and traffic has been an issue, with industry-wide traffic decelerating since July. In addition, while commodity inflation has cooled year-over-year, costs for beef, tea, and coffee have remained elevated relative to the commodity basket, which will could profitability short-term at Burger King and Tim Hortons, its two largest brands. This is a slight offset vs. deceleration in pork and chicken prices that will benefit its smaller brands.

However, I don't see this as material at all to the long-term thesis because the real opportunity here is improving speed of service and ease of operation and growing market share in areas that can be considered low-hanging fruit (PM food is fastest growing daypart where Tim Hortons is winning) which should ultimately boost AUVs and franchisee profitability. Hence, these are the metrics worth watching for the company's long-term success, and it's nice to see Restaurant Brands has switched from cost-cutting leadership (3G Capital) to a seasoned turnaround specialist with Patrick Doyle that understands where/when it's necessary to invest to turn around underperforming brands/markets and accelerate growth in its best performing concepts. Also of huge value is new appointment Tom Curtis (President of Burger King US/Canada), who will be pivotal to turning around the brand after 35 years at Domino's Pizza (DPZ), both as Operations and as a franchisee.

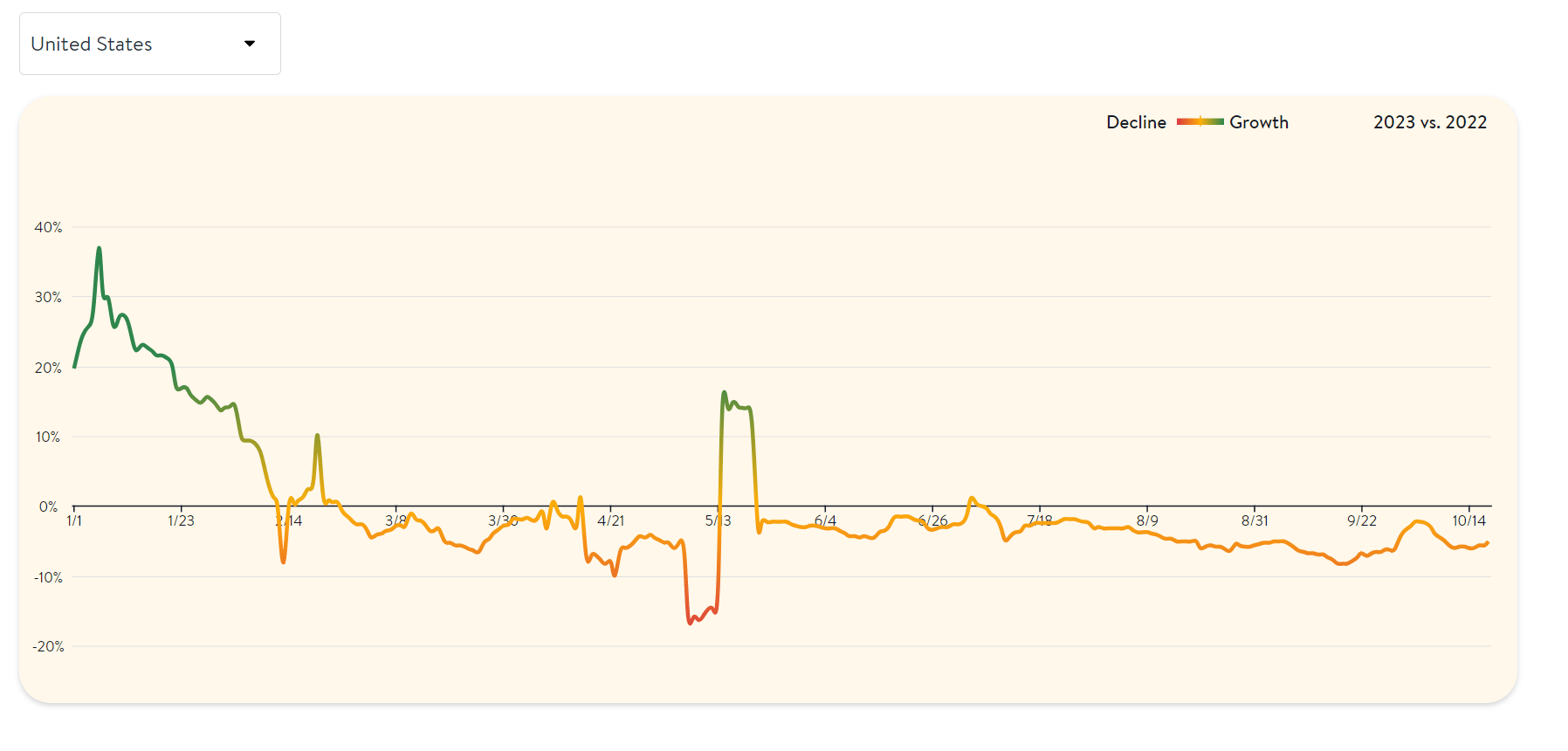

Open Table Seated Diners - Open Table

Looking at industry-wide traffic above, August and September traffic were down sharply industry-wide, and October traffic is off to a slow start as well, at least according to Seated Diners from OpenTable. Worse, quick-service traffic also fell sharply in September logging its worst month year-to-date, suggesting that even trade-down beneficiaries like quick-service and fast-casual are seeing negative traffic. This is not ideal because it was previously a sanctuary among a period of slowing casual dining sales. And given this trend, it is possible that we could see noisier results in Q3/Q4 for Restaurant Brands, which may have a tougher time materially beating estimates in Q3 of ~$1.87 billion (implying 8% growth year-over-year) in Q2-2023 and $0.85 in EPS. So, with a more difficult setup, I think it's better to wait for pullbacks to buy vs. rushing in ahead of earnings after its recent rally.

Valuation & Technical Picture

Based on ~455 million shares and a share price of $66.00, Restaurant Brands trades at a market cap of ~$30.0 billion and an enterprise value of ~$43.0 billion. This gives it one of the higher capitalizations in the sector, ahead of Darden (DRI), Domino's, and Texas Roadhouse (TXRH), and just behind Pizza Hut, KFC, and Taco Bell owner, Yum Brands (YUM). And for those that have owned the stock since its IPO debut, the performance has certainly been disappointing, with a ~50% return compared to a ~180% return from burger competitors like McDonald's (MCD) and ~110% return from Wendy's (WEN) in the same period. However, there's no reason that the past nine years have to look like the next nine, and this underperformance in the stock despite multiple acquisitions (Tim Hortons, Popeyes, Firehouse Subs) has not only allowed it to build a massive base in its chart as it's gone sideways, but has also left it at a very reasonable valuation.

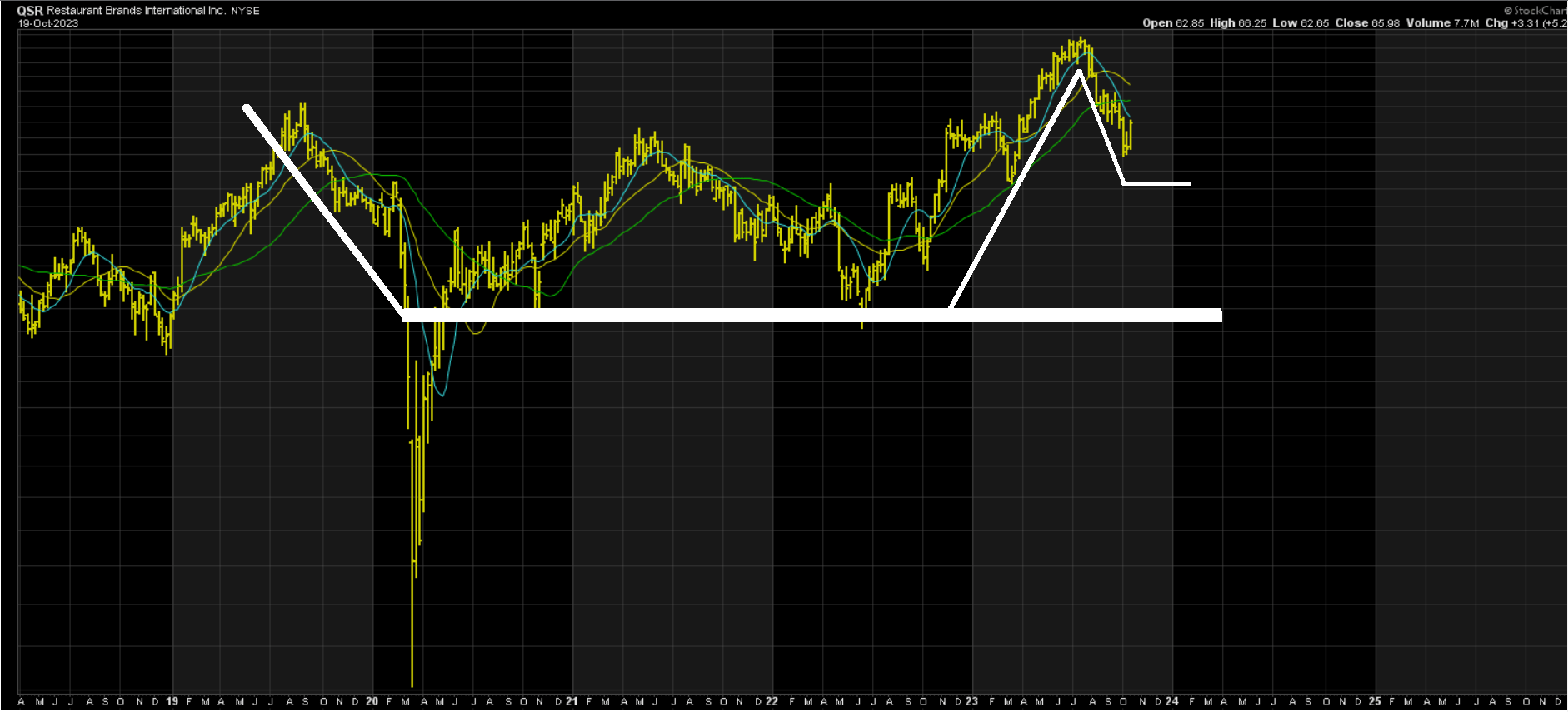

QSR Weekly Chart - StockCharts.com

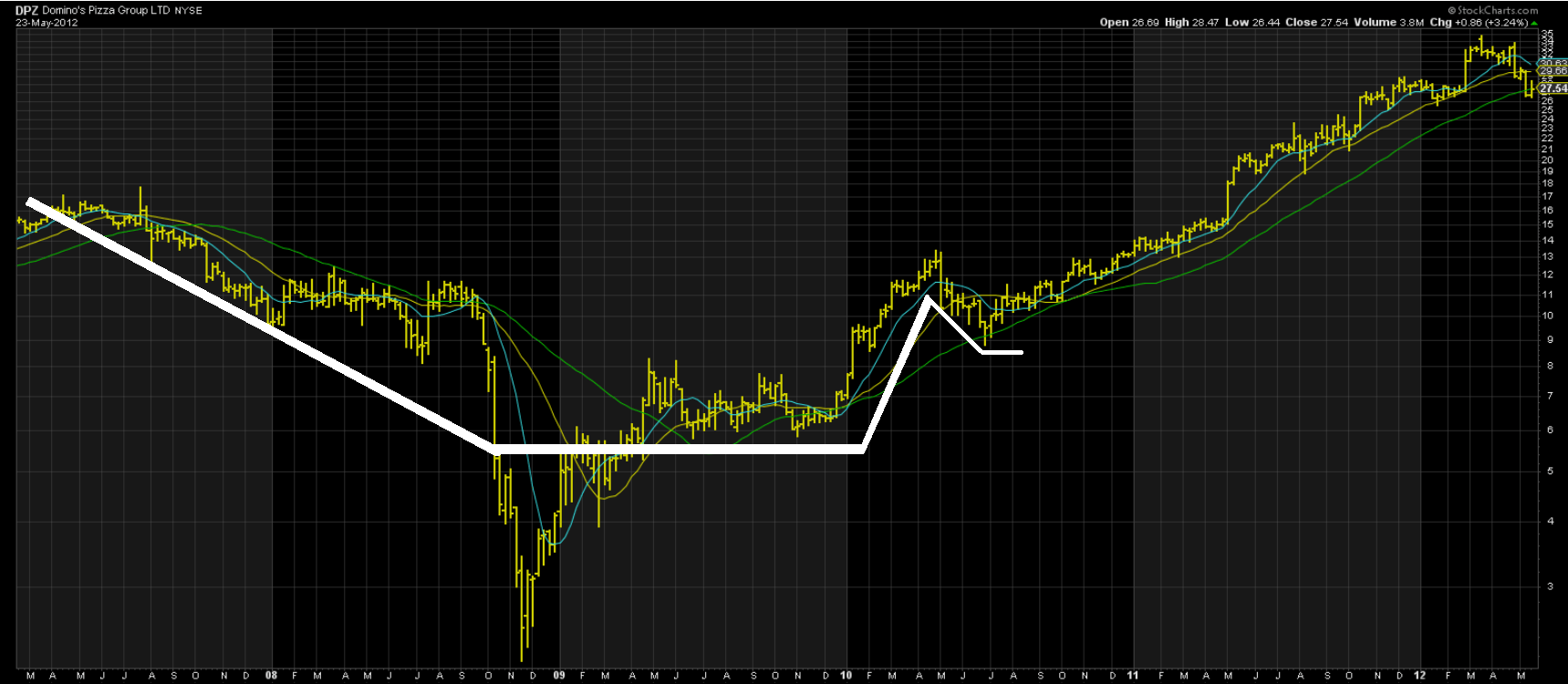

DPZ Weekly Chart (2007-2015) - StockCharts.com

Starting with the technical picture, and if we ignore the Q1 2020 correction that distorted the charts of nearly all restaurant stocks, we can see that QSR is building a multi-year cup & handle base, and looks to be in the handle portion of this base currently. This is typically a bullish continuation pattern, with the ideal time to buy being in the double bottom portion of the base for long-term investors, and near where one believes the bottom of the handle to be (only knowable in hindsight) if one wants to top up one's position. As the chart above illustrates, it looks like the floor for QSR from now on could be ~$59 based on what I would consider a normal handle depth, suggesting further weakness in the stock would provide a buying opportunity.

This setup isn't that dissimilar to the warped 3+year semi-saucer & handle base with a 65%+ correction on its left side that Domino's built between February 2007 and August 2010 (shown above), with the same leader at the helm: Patrick Doyle. The stock would go on to be the sector's best performers, up over 2000% over the next seven years from its handle, and while I do not expect a repeat for QSR, the technical setup remains quite attractive.

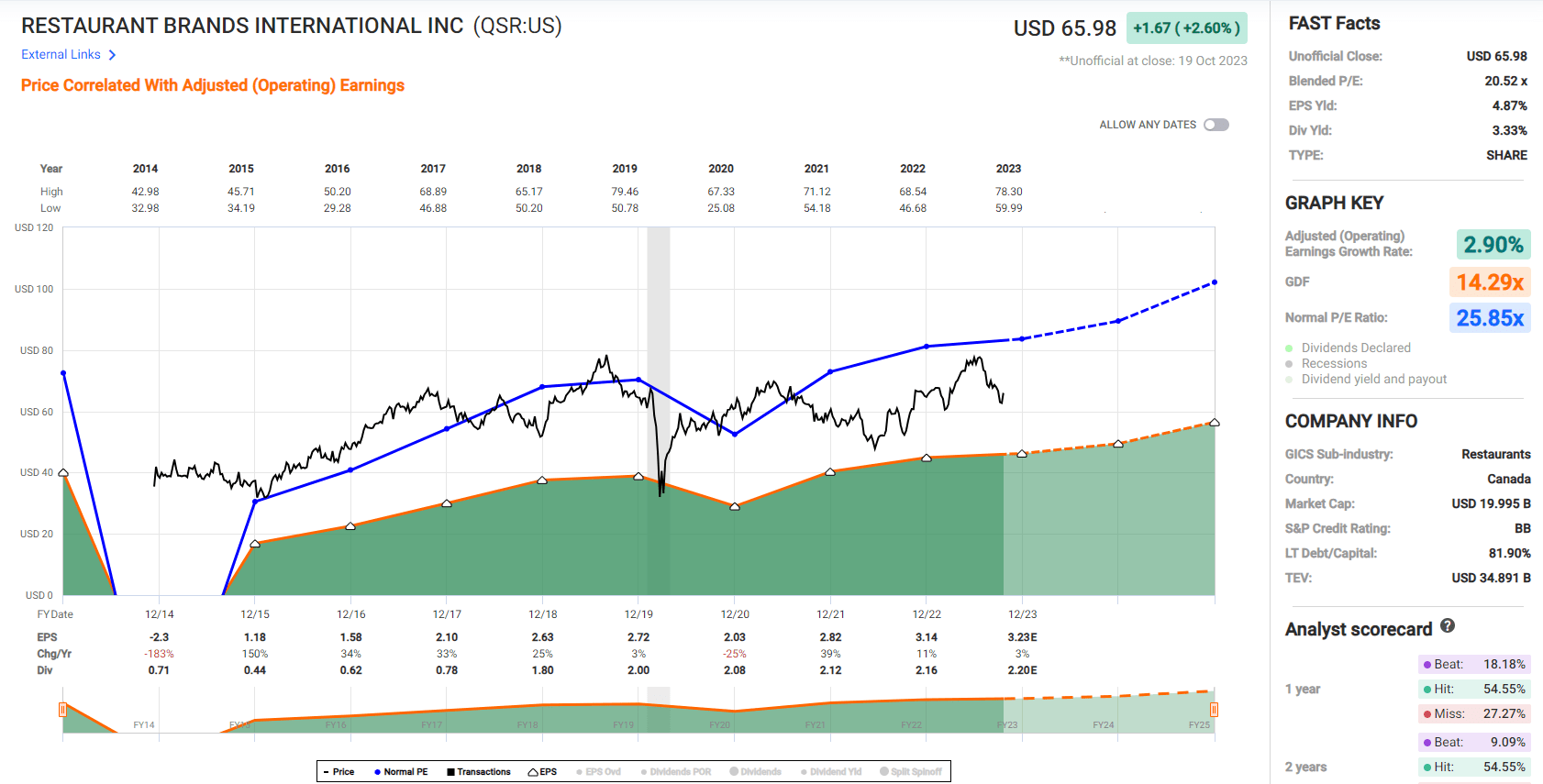

Restaurant Brands - Historical Earnings Multiple - FASTGraphs.com

Meanwhile, from a valuation standpoint, QSR remains attractively valued, and would become even more reasonably valued if it were to make new correction lows and form a deeper handle in the $59 - $60 region. This is because the stock would trade at just ~17.0 FY2024 earnings estimates ($3.55), a steep discount to other quick-service franchisors like McDonald's at ~21.0x, and Yum! Brands at ~20.5x FY2024 earnings. And given the upgrade to leadership, the impressive unit growth and the significant room for growth internationally, I think the stock should trade in line with its peers with 10-year average earnings multiples of ~25.0x. That said, even if we use a more conservative 22.5x earnings to derive fair value, QSR's fair value would come in at $79.90 per share.

Although this points to a ~24% total return, I am looking for a minimum 25% discount to fair value for large-cap stocks even if they are more recession resilient and trade-down beneficiaries. And if we apply this discount to QSR, its ideal buy zone comes in at $60.00 or lower, lining up with where I would expect the stock to find support if it were to form a double-bottom handle as part of its current 4-year base. So, while I am long the stock with a cost basis of ~$54.00, and initially bought below $51.00 in May 2022, I don't see a low-risk opportunity to add to the position just yet, even if I see it as one of the better-positioned names in the market (a trade-down beneficiary that could be setup up for a decade of outperformance after a decade of underperformance at a very reasonable valuation).

Summary

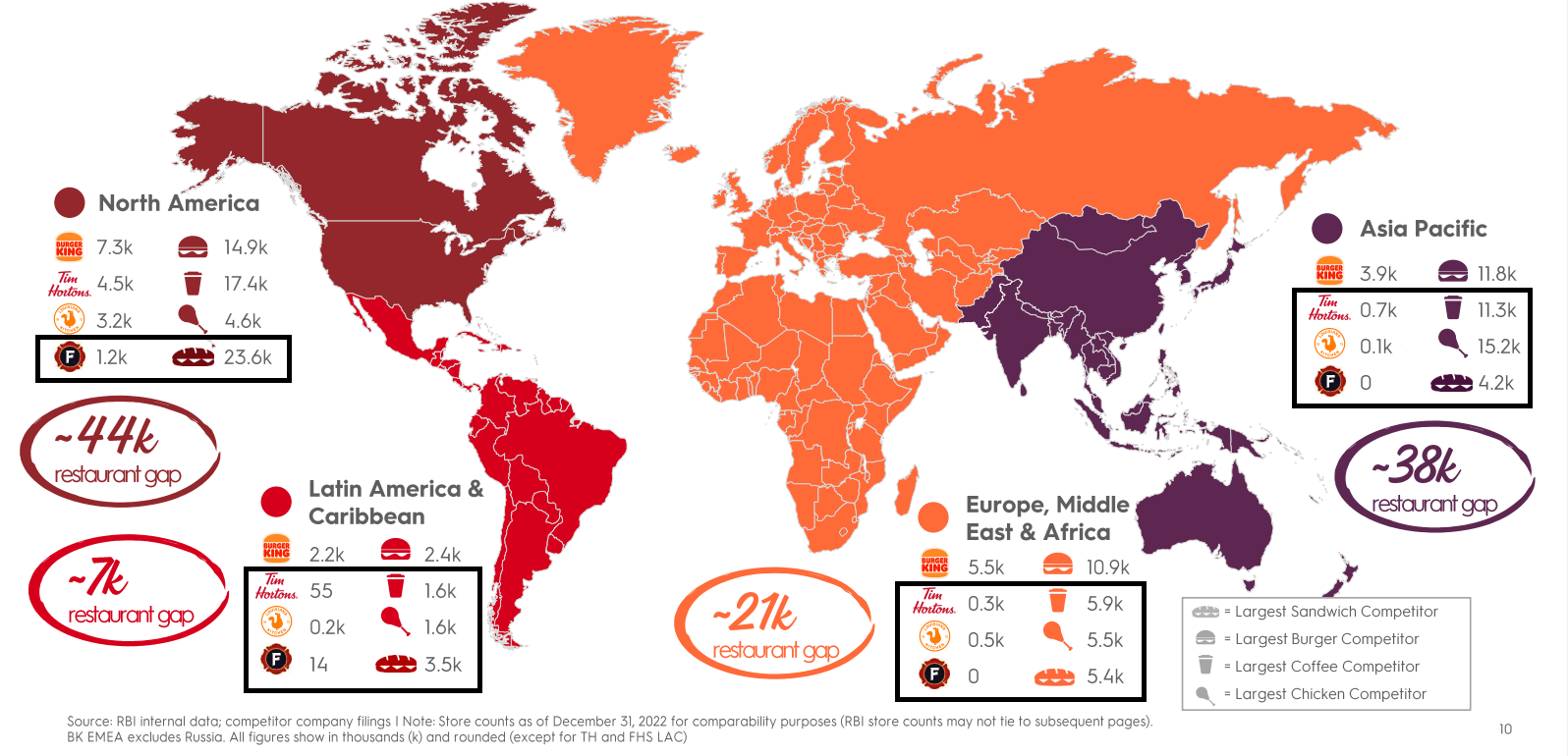

Restaurant Brands had a blowout quarter in Q2 2023 and it is one of the better setups going into its November 3rd earnings in the sector given that its sales performance was strong despite being up against tough comps and industry-wide traffic declines. Meanwhile, the long-term opportunity for the stock is also compelling, with the company proving it can successfully grow internationally yet having a massive restaurant gap in other markets, especially for its smaller brands Firehouse and Popeyes which have 800 restaurants outside of North America vs. ~35,000 the category leader in sandwiches and chicken. Hence, the long-term goal of 40,000 restaurants may actually prove conservative, especially with an additional brand in Firehouse Subs (most recent acquisition).

International Opportunity Restaurant Brands International - Investor Presentation

That said, I prefer to buy at a deep discount to fair value even when adding to existing positions, and while QSR is better positioned than most peers for a beat, I still don't see a low-risk buying opportunity just yet. However, given the stock's mix of growth and value with one of the better-looking term charts in the restaurant space with a ~20% correction after a multi-year breakout to new all-time highs, I would view any pullbacks below $60 as buying opportunities.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.