Fisker: Avoid This Heavily Shorted EV Stock

Summary

- Fisker's stock has plummeted 27% YTD, underperforming Tesla and Invesco QQQ Trust.

- Fisker's asset-light business model sets it apart from competitors, but it faces challenges in production and delivery.

- The company may need to raise more capital, potentially diluting shareholders, and its short interest is high.

Mario Tama

Fisker (NYSE:FSR) is yet another EV company with plans to gain market share in the growing electric vehicle landscape.

Like many of the 2021 EV SPACs, FSR stock soared shortly after its NASDAQ debut and then crashed along with the entire EV sector.

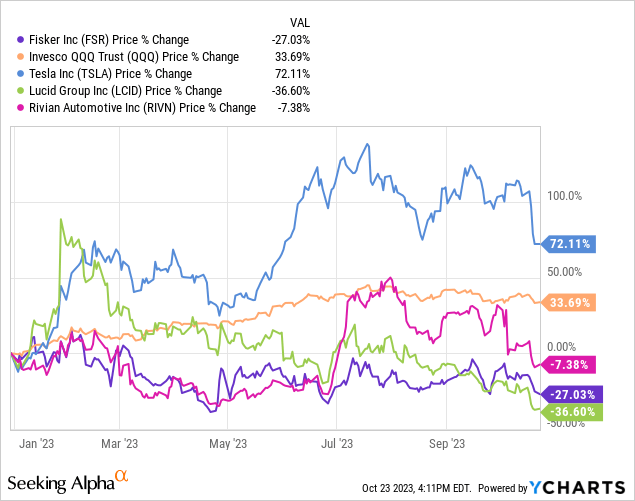

FSR shares are down 27% YTD and you would have done better buying Tesla (TSLA) or the Invesco QQQ Trust (QQQ) instead of holding Fisker stock.

Data by YCharts

Data by YCharts

The company has faced major headwinds including a struggle to deliver its flagship Fisker Ocean SUV on time and an extremely negative short seller report by Fuzzy Panda Research that accused the company of allegedly lying about its financial stability.

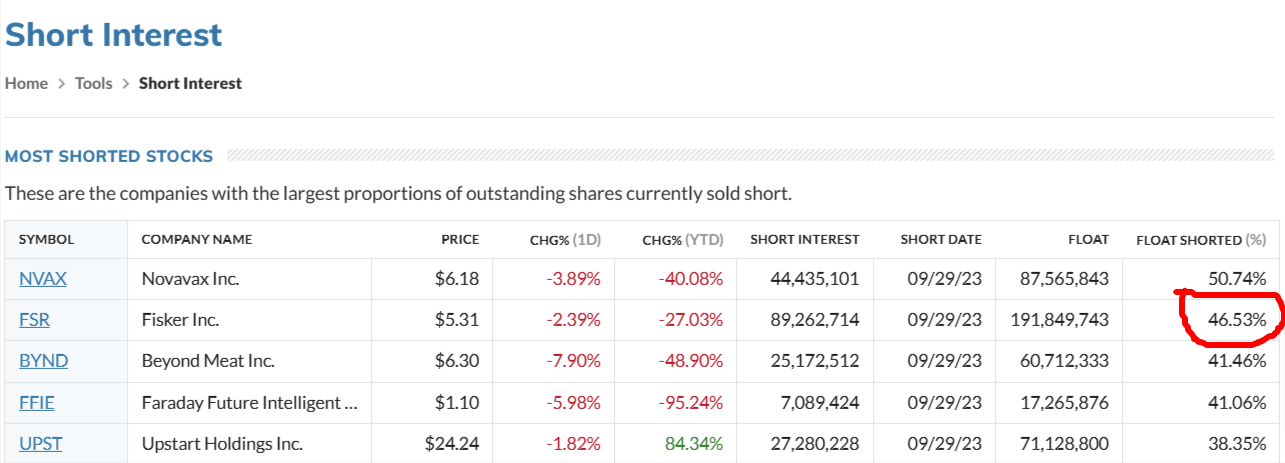

With so much negativity surrounding Fisker, FSR stock is the 2nd most shorted NASDAQ listing with a short interest of over 46%.

FSR Short Interest (marketwatch.com)

Many of you are probably wondering if Fisker could benefit from a short squeeze that would send its stock soaring back to new highs.

It's possible but I'm very skeptical of Fisker's ability to stay in business without raising more capital through dilutive share offerings or taking on debt.

Fisker Overview

Fisker has changed drastically since I previously wrote about the company here so I'll provide a refresher on the company's EV models and deliveries targets.

Fisker's most popular EV is the Fisker Ocean SUV with a range of 360 miles (km). The base model price is $69,000 with over 67,000 reservations as of Q2 2023.

What makes Fisker stand out from the competition is the company's asset-light business model approach to EV production.

Fisker outsources 100% of its EV production to Magna International's (MGA) Magna Steyr in Graz, Austria while the company focuses on design, engineering, and customer service.

This is a stark contrast from the asset-heavy approach of its competitors such as Tesla (TSLA), Rivian (RIVN), and Lucid (LCID). All 3 of these companies own and operate their own EV production facilities to control the entire manufacturing process.

In order to reduce costs, Fisker CEO Henrik Fisker did the opposite and contracted out the Fisker Ocean production to speed up the company's production and delivery process.

However, Henrik Fisker mentioned in an interview with The Verge that the company may build a production facility in the future once it's more mature.

The company has also planned the production of 2 new EVs in the future: The Fisker PEAR and the Fisker Ronin.

The Fisker PEAR is a simplified EV with fewer moving parts to offer a cheap, affordable electric vehicle to the masses. It's priced at $29,900 intentionally to hopefully attract budget-conscious consumers who want an EV but cannot afford a more luxurious model.

The Fisker Ronin is Henrik Fisker's dream sports car that helps diversify the company's product line in the future.

Q2 Business Update

In Q2 2023, Fisker began its first deliveries of the Fisker Ocean and hit 11 deliveries during the quarter. The company generated just $825,000 in revenue but plans to continue scaling through the rest of 2023.

Fisker is projected to produce 20,000 to 23,000 EVs in 2023 with an estimated 18.5% gross margin per vehicle.

Fisker lost $85.5 million (-$0.25 per share) and raised $170 through a 0% senior unsecured convertible note due in 2025 offering to bolster the company's balance sheet.

The company ended Q2 2023 with $521.8 million in cash on its balance sheet, which covers just under 1 year's worth of expenses.

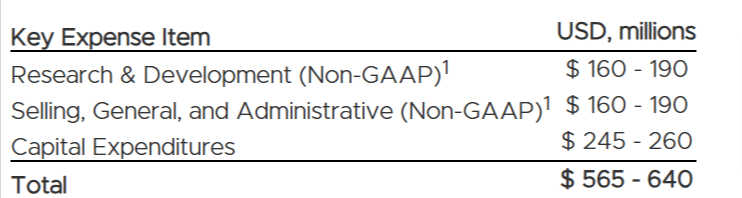

Fisker 2023 Annual Expenses (fiskerinc.com)

More Dilution May Be Coming Soon

What's troubling is that Fisker could tap an additional $550 million in 0% senior unsecured convertible notes to help fund production.

Fisker currently has a $1.8 billion market cap and another convertible note offering would possibly dilute FSR stock by almost 33%.

With only 335.9 million shares outstanding as of Q2 2023, it's highly likely that Fisker will convert those notes into shares and dilute shareholders in the process.

Take a look at the total shares outstanding counts of similar EV companies to understand my reasoning.

Total Shares Outstanding by EV Company

| Company | Shares Outstanding |

| Fisker | 335 million |

| Tesla | 3.15 billion |

| Lucid Group | 1.9 billion |

| Rivian | 990 million |

As long as EV companies are forced to cut prices in an ongoing war, I don't see the reason to own FSR stock when dilution seems nearly 100% certain.

Fisker's Short Interest Could Increase

FSR's 46%+ short interest may increase even more once we get more details on the company's Q3 2023 earnings and delivery numbers. The entire EV sector is selling off and even Fisker's cheaper EVs may be affected negatively by cost-conscious consumers.

While Fisker's monthly lease costs start at only $379, you must pay an upfront $2,999 activation fee and a $299 lease termination fee.

With so many people struggling with inflation and debt, I think the $2,999 activation fee will scare many buyers away initially.

If Elon Musk was right about the overall economy then Fisker could miss on its Q3 2023 numbers and cause even more short sellers to beat against FSR shares.

Normally, I would bet against the shorts and hope for a short squeeze but I'm staying away from FSR until I see those Q3 2023 numbers.

Risk Factors

- Lower Delivery Estimates: Fisker has lowered its delivery estimates multiple times in 2023 and could do the same in 2024. It's promising to see the company project 300 EVs delivered per day but history shows that Fiser hasn't backed up its claims. If delivery estimates fail again then FSR stock could sell off and dip much lower.

- Declining Margins: Elon Musk warned investors about the issues facing the EV industry during Tesla's Q3 2023 earnings call and I believe Fisker will be affected by the same problems of high interest rates. Fisker will probably cut prices to stir up demand, which could hurt operating and profit margins.

- Lack of Production Control: Fisker's decision to outsource all of its production to a 3rd party could backfire if Magna fails to meet Fisker's production demands or makes too many production errors. It's difficult to make an EV and I wonder if outsourcing everything is a bad decision long term. Apple earned a fortune by outsourcing the iPhone production but it's a lot more difficult to produce an electric vehicle versus a smartphone in my opinion.

I'm Avoiding FSR Stock For Now

I'm rooting for Henrik Fisker because founder-led companies tend to outperform the market over time. However, I don't see how Fisker can scale production without raising more capital in the future.

FSR stock trades just under $6 and I wouldn't be surprised if FSR shares dipped below $4 by Q1 2024.

FSR's high short interest and high P/S ratio is a massive warning signal for me to stay away from Fisker until I see a much more affordable price-to-sales ratio in comparison to its competitors.

Fisker's market cap is $1.8 billion even though the company generated $825,000 in revenue during Q2 2023.

Even if Fisker delivers all of its 5,000 EVs produced, Fisker's revenue would be just $187 million. That's assuming that Fisker doesn't have reservation cancellations or issues.

I'm not buying the company's 300 EV deliveries per day and take their bold claim with a grain of salt.

I'm placing a SELL rating on Fisker until I see proof of the company's aggressive growth claims because the final numbers don't add up to me.

Recent price cuts show that the demand for the Fisker Ocean is decreasing so be careful when buying FSR shares right now.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.