Impala Platinum Holdings: It's Hard To Think It Could Drop Much Further

Summary

- Impala Platinum Holdings Limited reported a net loss of $483.76 million in H1 2023, with a negative EBITDA of $325.16 million.

- The company's stock performance has underperformed Sibanye Stillwater Limited, and it has dropped 59% on a one-year basis.

- I recommend buying Impala Platinum Holdings shares between $4 and $3.40, with a lower support at $3.25.

RHJ

Introduction

On August 31, 2023, the Johannesburg-based Impala Platinum Holdings Limited (IMPUY) announced its H1 2023 for the year ended June 30, 2023. It next reports results on November 2nd.

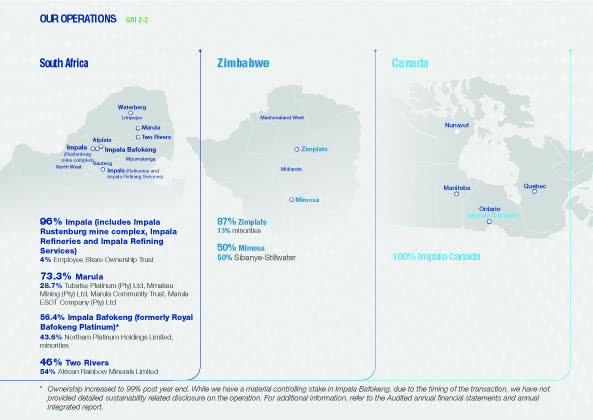

Impala Platinum Holdings is a leading producer of platinum group metals (PGMs) structured around seven mining operations and a refining business called Impala Refining Services.

The South African company's mining operations span the Bushveld Complex in South Africa, the Great Dyke in Zimbabwe, and the Canadian Shield.

IMPUY Map Presentation (IMPUY Presentation)

1: H1 2023 Results Snapshot (last 6 months)

Impala Platinum posted a net loss of $483.76 million, or $0.57 per share, in H1 2023. The company posted a negative EBITDA of $325.16 million with a free cash flow of $66.74 million.

Impala Platinum also indicated FY23 with revenue of $5,948 million, down 20.3% compared to $7,465 million in FY22.

IMPUY Yearly Revenue History (Fun Trading)

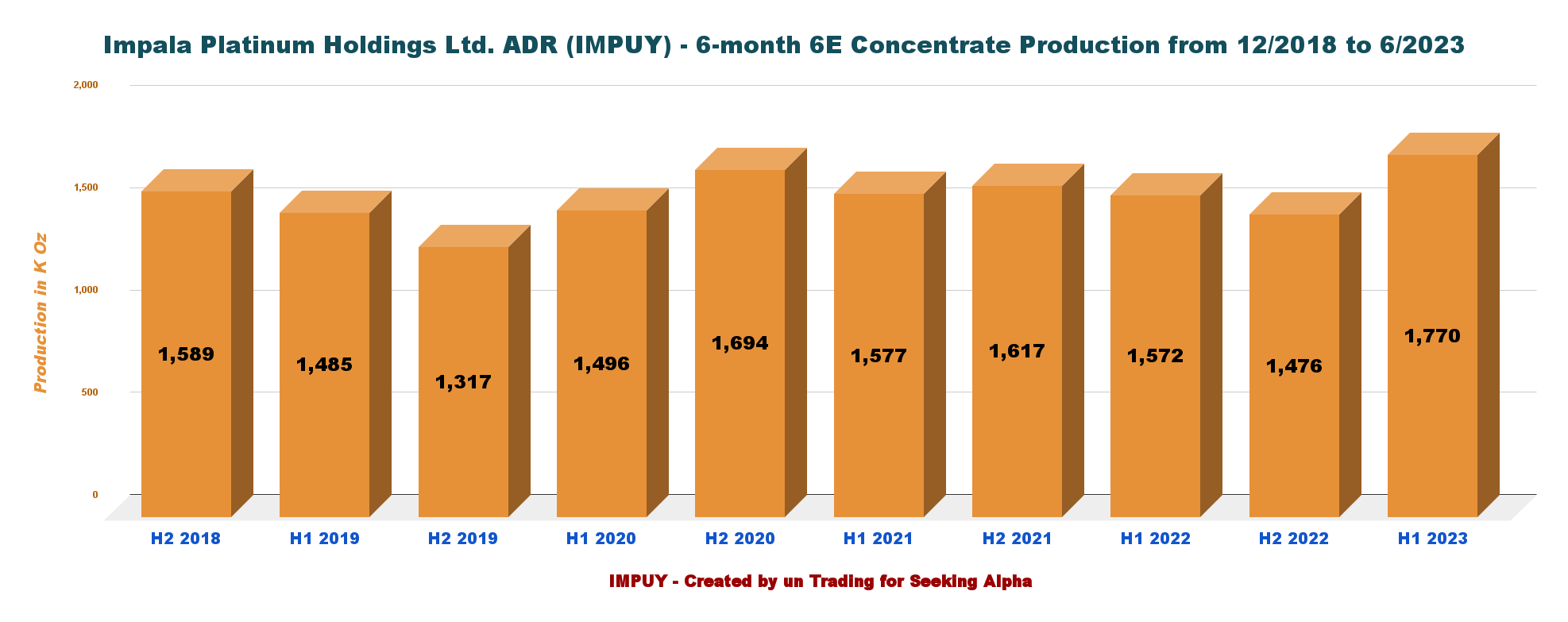

Impala Platinum 6E Concentrate production was stable on a one-year basis.

IMPUY 1-Year 6E Production history (Fun Trading)

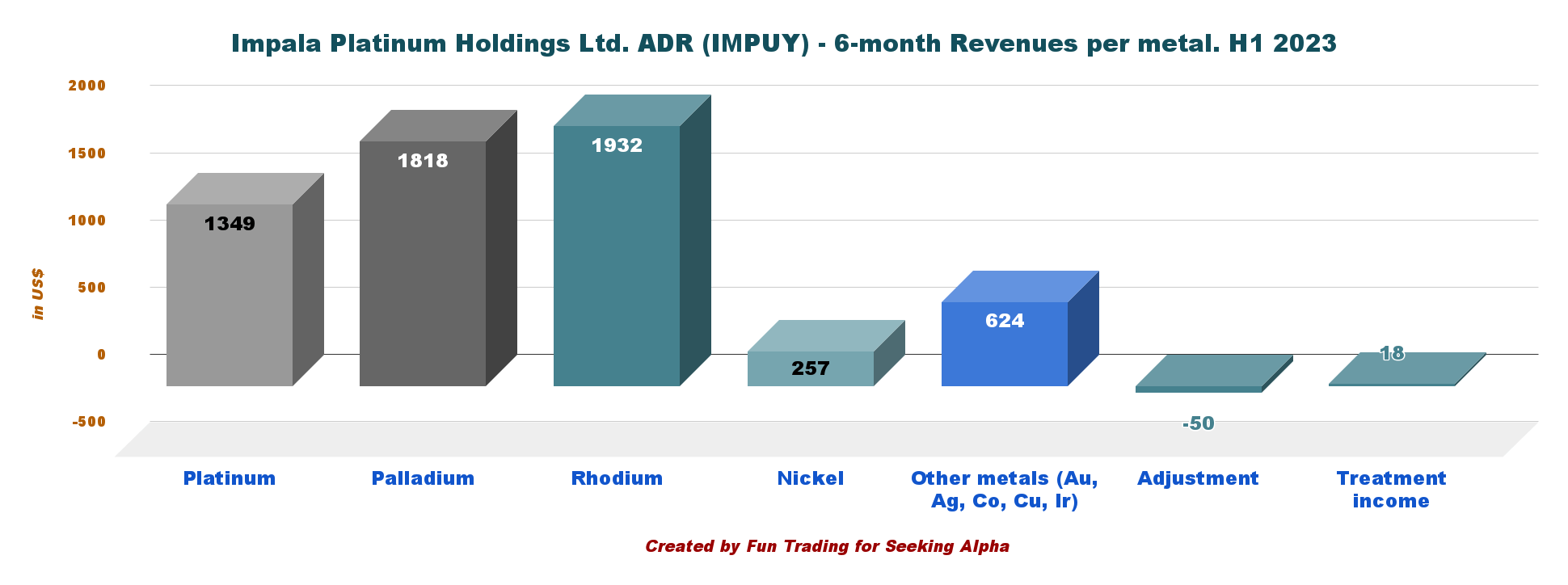

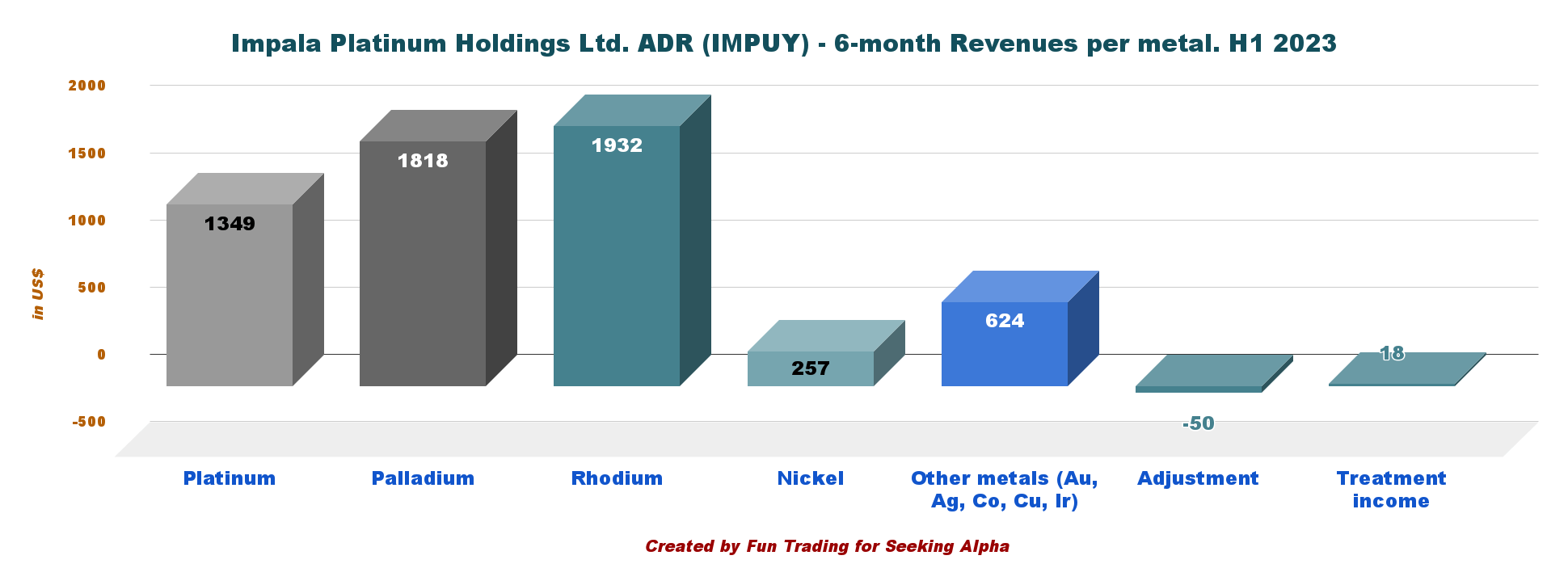

Note: 6E production is based on the primarily six metals mined by the company (Platinum, Palladium, Rhodium, Nickel, etc.). Below is the revenue repartition per metal for the last H1 2023 (6 months):

IMPUY 6-month Revenue per Metal in H1 2023 (Fun Trading)

Note: When it comes to South African companies such as SBSW, IMPUY, and others, the results are somewhat intricate. The results are presented on a 6-month and a full-year basis, and they are very complex. Additionally, the majority of the results are shown in South African Rand, a currency that fluctuates frequently. To make things easier for readers to understand, I will combine the 6-month and full-year results in this article. Although it isn't ideal, it's the only solution I could think of.

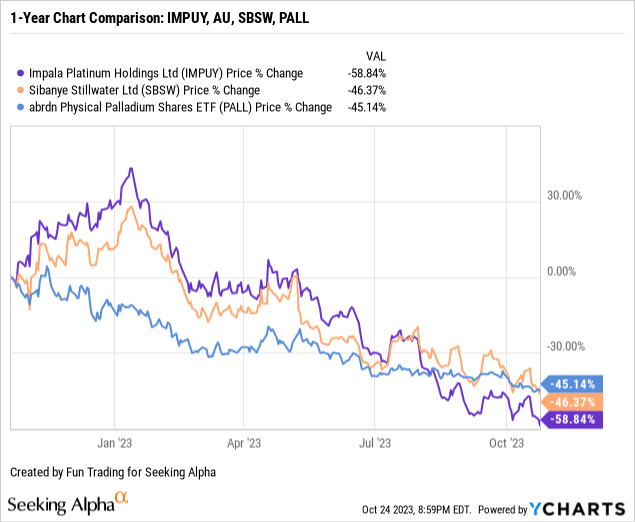

2: Stock Performance

Impala Platinum Holding has significantly underperformed Sibanye Stillwater Limited (SBSW). One exchange-traded fund, or ETF, that could be great to follow in this platinum/palladium segment is the Aberdeen Standard Physical Palladium Shares ETF (NYSEARCA: PALL).

IMPUY has dropped significantly since the beginning of 2023 due to a painful slide in palladium prices. IMPUY is down 59% on a one-year basis, underperforming SBSW and PALL.

Data by YCharts

Data by YCharts

The Investment Thesis

IMPUY is a solid PGM producer despite this massive slide that started in early 2023 and may continue until next year. The company is a pure PGM and, therefore, looks more volatile and subject to long periods of depression, which is what we have experienced in 2023.

On the other hand, I think this bearish cycle is about to end, and IMPUY appeals to me. Of course, patience is the key.

The industry is going through some tough times. For instance, Sibanye Stillwater recently announced it planned restructuring its PGM mining and close four loss-making platinum group metal shafts in South Africa, which could result in the loss of 4,095 jobs.

Also, the Chief Executive, Nico Muller, said:

A rapid decline in palladium and rhodium prices that has squeezed profits, lowered dividend payouts, and shifted the focus to cutting costs caught platinum miners off guard.

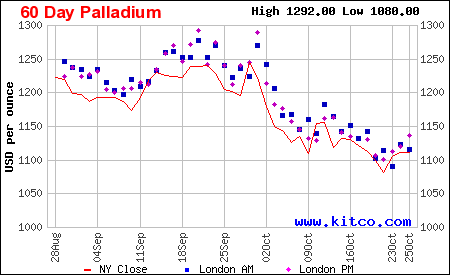

6-month Chart Palladium Chart (Kitco.com)

In addition, mining in South Africa is difficult and fraught with problems (a faulty electricity grid, unstable labor, etc.), which complicates the problem.

Consequently, I advise trading LIFO for roughly 50% of your long-term stake, even though IMPUY is an attractive stock with strong growth options.

By doing this, you can build on weaknesses and significantly reduce risks.

Assets and Production Presentation

The 6E production (concentrate) originates from three different groups:

- Managed mining operations: Impala, Zimplats, Marula, and, more recently, Impala Canada. The company said that "6E production at managed operations increased by 6% to 2.42 million ounces (FY2022: 2.29 million ounces), and a maiden contribution of 43 000 6E ounces in concentrate from RBPlat was recorded for the 30 days to June 30, 2023."

- Joint venture operations: Mimosa and Two Rivers’ Merensky Mine (46%), UG2 plant expansion, and tailings projects The company said "6E concentrate production of 541 000 ounces from JV operations declined by 1% (FY 2022: 548 000 ounces). Safety stoppages and intermittent localized community disruptions at Two Rivers exacerbated the ongoing impact of split-reef and development tonnage on milled grade."

- Third-party Purchased.

Also, the attributable Mineral Resource estimate decreased by 2% to 262.7 million ounces (6E) due to production depletion and a model update to the Zimplats Hartley Mineral Resources.

As I mentioned in my previous post, acquiring ownership of Royal Bafokeng Platinum Limited was the year's high point.

The combined asset base of Impala Rustenburg and RBPlat – which will be renamed Impala Bafokeng on delisting – will result in a more secure and sustainable Rustenburg operating complex in years to come, with a premier mine-tomarket production base, well-capitalised infrastructure and long-term competitive positioning, enhanced by industry-leading integrated processing capability

Impala Platinum Holdings Ltd.: Balance Sheet And Production History For H1 2023: The Raw Numbers

Note: As for most South African gold and PGM miners, full results end in December. The recent results are the interim results for H1 2023.

Note: The data indicated has been translated into US dollars using the $US/ZAR ratio of 17.68. The ratio between Implats ordinary South African (ZAR-denominated) shares and the ADR is 1:1.

Implats shares trade on OTCQX, the premier tier of the Over-the-Counter (OTC) market in the USA, as ADRs.

| IMPUY | H2 2021 | H1 2022 | H2 2022 | H1 2023 |

| Total Revenues in Millions (6 months) | 3499.96 | 3965.50 | 3344.73 | 2603.23 |

| Net Income in Millions (6 months) | 870.77 | 1151.55 | 808.62 | -483.76 |

| EBITDA: $ Million (6 months) | 1462.91 | 1768.39 | 1386.05 | -325.16 |

| EPS diluted in $/share (6 months) | 1.06 | 1.36 | 0.95 | -0.57 |

| Cash from operating activities in a million dollars (6 months) | 1107.06 | 1096.85 | 838.31 | 484.56 |

| Capital Expenditure in Millions (6 months) | 215.85 | 348.16 | 279.98 | 417.82 |

| Free Cash Flow in the Million (6 months) | 889.21 | 748.68 | 558.33 | 66.74 |

| Total Cash: $ Million | 1231.28 | 1742.78 | 1626.85 | 1432.02 |

| LT Debt (incl. current) in Million | 0.00 | 0.00 | 0.00 | 78.58 |

| Share outstanding diluted in million | 819.99 | 849.29 | 850.09 | 857.45 |

| Dividend $/ share | 0.2637 | 0.4254 | 0.1637 | 0.0580 |

| $US/ZAR ratio | 15.94 | 17.50 | 16.27 | 18.85 |

| PGM Production | 2020 | 2021 | 2022 | 2023 |

| Gross Refined Production: 6E Koz | 2,813 | 3,271 | 3,189 | 3,246 |

Source: the company booklets FY23 and Fun Trading.

Warning: A haircut of 25.6% is applied to the dividend payment to cover costs and withhold foreign tax.

Impala Platinum Holdings: Balance Sheet Details

1: Revenues And Trends using 6-months Revenue History

IMPUY 6-month Revenue History (Fun Trading)

Note: Revenue for FY23 is calculated by adding H1 2023 to H2 2022.

The company said in the FY23 press release:

The Group’s financial performance was negatively impacted by the retracement in rand PGM pricing, lower refined production and sales volumes, continued higher levels of inflation, and the accounting impact of end-of-period inventory valuations and impairments related to Impala Canada and RBPlat, the latter as required by its consolidation.

Impala Platinum revenues for H1 2023 were $2,603.23 million, down significantly from the preceding 6-month period. The net loss was $483.76 million, down from $808.62 million in H2 2022. Kindly review the above table.

The combination of lower revenue and a higher cost of sales reduced gross profit by 46% YoY. As we can see below, Rhodium represents the lion's share of the revenues (H1 2023).

IMPUY H1 2023 Production per Metal (Fun Trading)

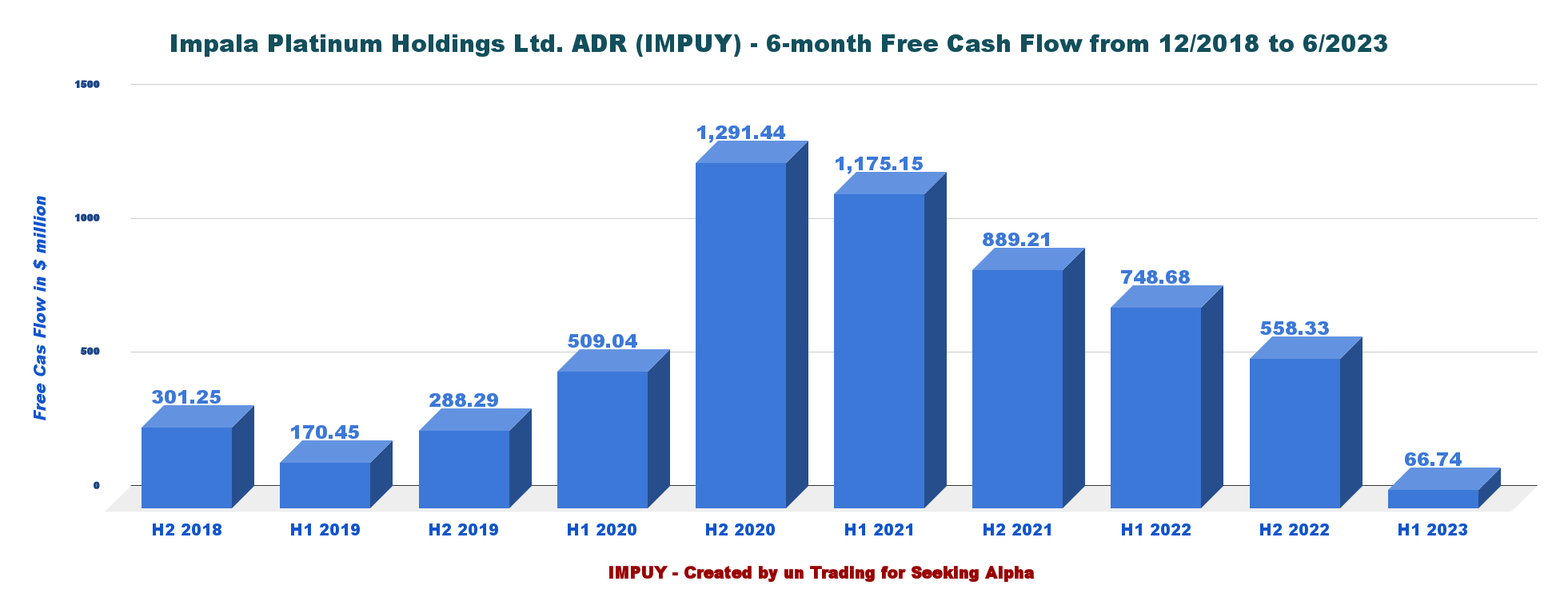

2: Free Cash Flow Was $66.74 Million In H1 2023

IMPUY 6-month Free Cash Flow History (Fun Trading)

Note: Cash from operations less capex is known as generic free cash flow. The business may occasionally disclose an alternative computation (non-GAAP) that takes into account additional factors like acquisitions.

Free cash flow for H1 2023 was down to $66.74 million, or a trailing 12-month free cash flow of $625.07 million.

The company paid a dividend of $0.2217 per share in 2023.

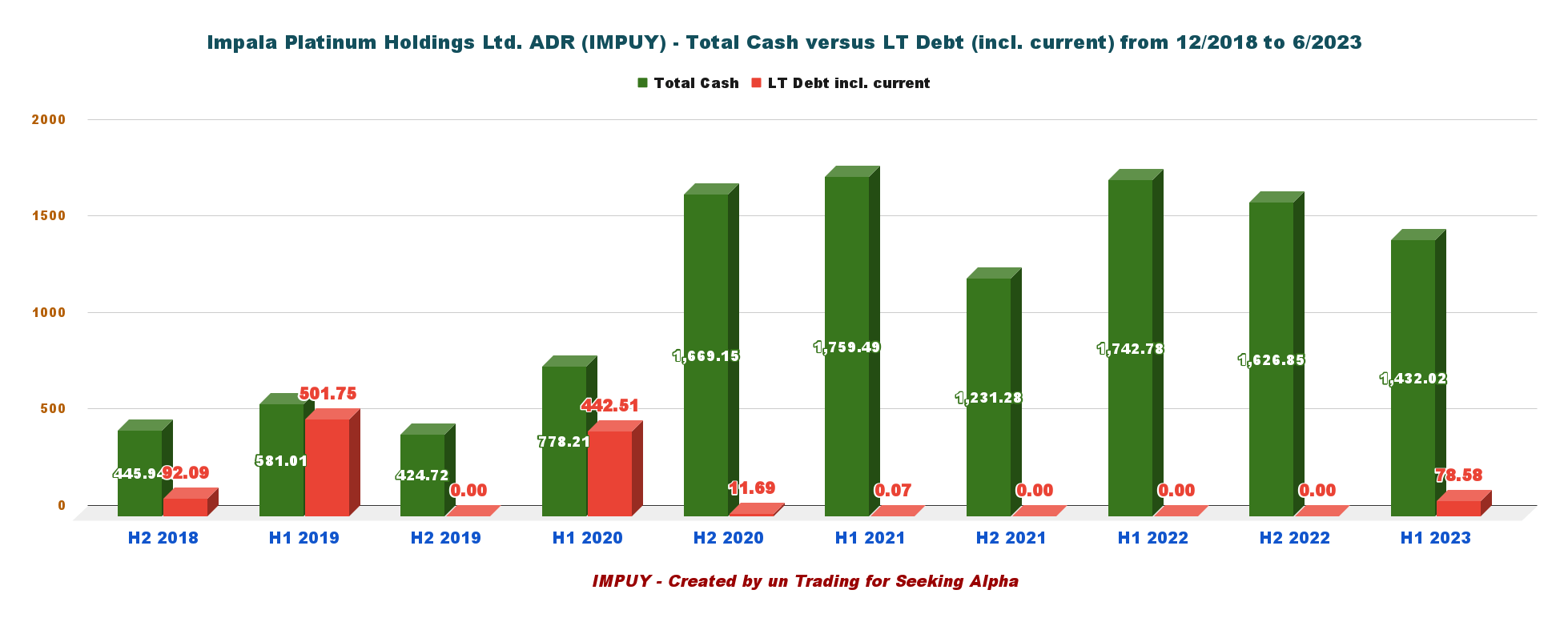

3: H1 2022 Impala Platinum Holdings' Debt Situation Is still Excellent

IMPUY 6-month Cash versus Debt History (Fun Trading)

The company is nearly debt-free, with $1,432.02 million in cash, and the LT debt is now $78.58 million.

4: H1 2022 6E Concentrate Production Analysis

IMPUY 6-month 6E Production Concentrate History (Fun Trading)

Group refined 6E production was 1,770K ounces in H1 2023, an increase from 1,478K ounces in the prior 6-month period. FY 2023 production was 3,246K oz.

The company said in the booklet:

- 6% increase in managed 6E production to 2.42Moz

- 1% lower JV 6E production of 541koz

- 18% decrease in third-party 6E receipts to 287koz

- Refined 6E production declined 4% to 2.96Moz

- 6E sales volumes declined 6% to 2.97Moz

- Group 6E unit costs rose 14% to 1,122/oz (stock-adjusted)

- Consolidated Group capital expenditure of $698 million.

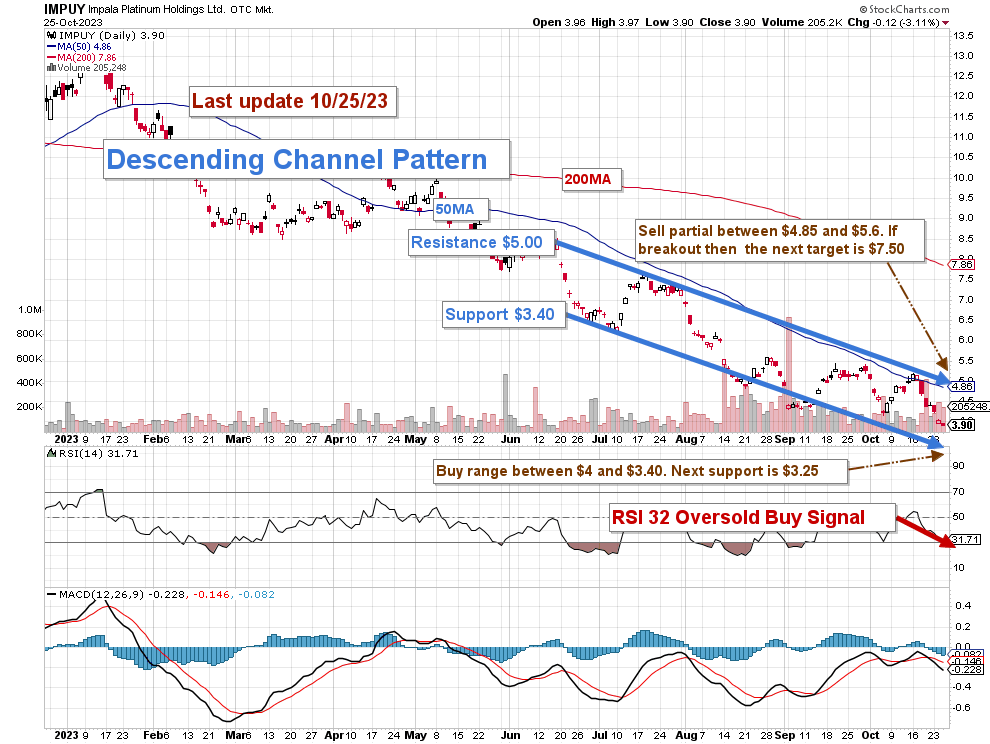

Technical Analysis And Commentary

IMPUY TA Chart (Fun Trading StockCharts.)

Note: The chart is adjusted for the dividend.

IMPUY forms a descending channel pattern with resistance at $5.00 and support at $3.40. The RSI is now 32 which is oversold flashing a buy signal.

Descending channel patterns are short-term bearish in that a stock moves lower within a descending channel, but they often form within longer-term uptrends as continuation patterns. Higher prices usually follow The descending channel pattern but only after an upside penetration of the upper trend line.

The main feature of IMPUY is that it is strongly correlated with the price of PGM, particularly palladium, rhodium, and platinum. The outlook for the fourth quarter is not positive. According to Kitco on October 17. 2023:

They added that with PGMs posting the worst year-to-date returns in five years, platinum and palladium “are likely to finish 2023 in the red, even when factoring in a possible late-Q4 rally in line with seasonal expectations” as “downward price trends tend to persist in the last quarter during PGM bear markets.”

Thus, I believe it is an important time to accumulate slowly on weakness expecting some rebound in 2024. I recommend trading short-term LIFO about 50% of your position, by selling between $4.85 and $5.60 with higher resistance at $7.50 and buying slowly between $4 and $3.40 with a lower support at $3.25.

Warning: The TA chart must be updated frequently to be relevant. It is what I am doing in my stock tracker. The chart above has a possible validity of about a week. Remember, the TA chart is a tool only to help you adopt the right strategy. It is not a way to foresee the future. No one and nothing can.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.