How to Use the Dividend Capture Strategy to Generate Passive Income

Table of Contents:

- What is the Dividend Capture Strategy?

- Understanding the Dividend Timeline

- Key Dates and Stock Price Movements

- Steps to Implement the Dividend Capture Strategy

- Real World Example

- Tax Implications

- Dividend Tax Rates Comparison

- Potential Risks and Downsides

- Dividend Capture Strategy Scorecard

- FAQs

Introduction

In a world of complex investing strategies, the dividend capture strategy stands out for its simplicity. The core concept involves buying and holding a stock just long enough to receive the dividend payout, then selling it afterwards. While easy to understand in principle, successfully implementing dividend capture on a consistent basis involves understanding key dates, anticipating stock price movements, and minimizing risks.

This comprehensive guide takes an in-depth look at how dividend capture works, who can benefit from using it, and tips to improve your odds of success. Whether you’re an experienced day trader or new investor looking to generate more passive income, dividend capture deserves a closer look.

What is the Dividend Capture Strategy?

The dividend capture strategy, sometimes called dividend stripping, is a short-term investment strategy focused on earning dividend income. It involves buying and selling stocks around key dividend dates rather than investing for the long-term growth potential of companies.

Specifically, a trader using this strategy will purchase shares of a company just before the ex-dividend date, hold them long enough to receive the declared dividend, then sell the stock afterwards — either breaking even or at a slight profit or loss depending on price movement. This allows them to collect dividend payments from stocks they may hold for only a few days or weeks.

Unlike buy-and-hold dividend investing, dividend capture is an active and fast-paced trading strategy better suited for investors with sufficient capital to buy larger company positions, the availability to monitor prices on a daily basis, and a higher tolerance for risk. However, it also provides more flexibility to switch between stocks and the possibility of amplifying returns through compounding.

Now let’s look at the key timeline and dates involved.

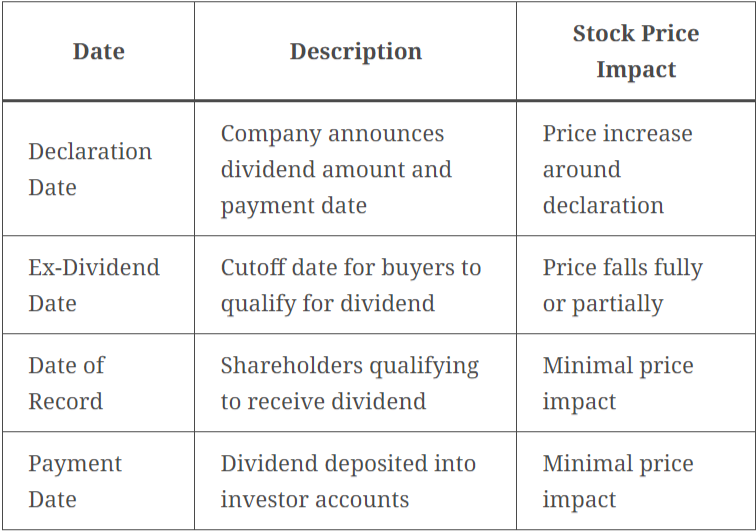

Understanding the Dividend Timeline

Capturing a stock’s dividend comes down to understanding and taking advantage of key dates in the dividend distribution timeline:

- Declaration Date: The first critical date is the declaration date when a company’s Board of Directors announces the next dividend amount and payment date. This usually happens several weeks or months before the actual payment.

- Ex-Dividend Date: This is the single most important date for dividend capture investors to know. The ex-dividend date (typically shortened to ex-date) is the cutoff for stock buyers to be eligible for the recently declared upcoming dividend.

- Date of Record: Shareholders who are on the company’s books as owners on the date of record become the “holders of record” that qualify to receive the declared dividend. This usually happens a couple days after the ex-date.

- Payment Date: Lastly, the actual dividend payment gets deposited into the accounts of qualifying shareholders a few weeks or months after the whole process begins on the declaration date.

>>Related 7 Cheap Stocks to Buy Now for $100 Investing

Key Dates and Stock Price Movements

Below is a summary table outlining the key dates to understand and typical stock price movements:

Additional Statistics

According to historical data analyzed by Yale professor William Brainard, on average stocks fall 70% of the actual dividend amount on the ex-date — allowing for profitable dividend captures in many cases.

Now let’s walk through how to actually implement these dates into an actionable dividend capture strategy.

Steps to Implement the Dividend Capture Strategy

While the core concept is simple — buy before the ex-date, collect the dividend, and sell afterwards — being successful with dividend capture long-term requires an organized system and risk management rules. Here are the key steps:

- Find upcoming dividend declaration dates: Use Nasdaq’s dividend calendar or your brokerage firm’s dividend information center to find companies that will soon declare their next dividends. Focus on stocks paying higher yields even if the share prices are higher.

- Review historical stock price movement: Gather data on how much the stocks typically fall in price on the ex-dates. Is there a predictable pattern to exploit? Some stocks might fully adjust while others only fall a fraction of the dividend amount.

- Buy shares prior to the ex-date: Purchase an appropriate position size just before the ex-date to qualify for the dividend. Consider buying options contracts simultaneously to profit from expected downward price movement afterwards.

- Hold through the date of record: Ensure your name is listed as a qualifying shareholder on the company’s date of record a couple days after ex-date.

- Collect dividends: The dividend will deposit into your account a few weeks later on the payment date so long as you continue holding through the date of record.

- Consider selling on ex-date: Sell positions in stocks that reliably fall close to the full dividend amount for easy profit capturing. For those declining less, hold out for the stock to recover.

- Wash, rinse, repeat: Roll proceeds over into new soon-to-declare dividend stocks and continually compound returns. Reinvested dividends can dramatically turbocharge total gains over time from this strategy.

>>Related Don’t Let the Bears Scare You — Why Apple and Amazon Are Top Stocks to Buy Now

Now let’s walk through a real example to see these steps in action:

Real World Example

With these dates and timeline in mind, let’s look at how dividend capture would work using real stocks and dividend declaration dates.

Microsoft (MSFT) shares trade around $250 in early September when the company sets its next dividend declaration date for September 21st, 2022. An investor checks historical price movement patterns and finds MSFT typically falls around 60% of the dividend amount on ex-date.

On September 21st, MSFT declares a dividend of $0.68 per share payable to shareholders of record on November 18th, 2022. The ex-date is set for November 17th.

On November 16th, the investor uses the dividend capture strategy to purchase 100 shares of MSFT for approximately $247 per share, for $24,700 total. Based on historical declines of 60% the dividend, they expect a ~$0.41 drop in MSFT.

As predicted, on November 17th (the ex-date), MSFT shares fall $0.42 to $246.58. The investor chooses to sell half the shares at a slight profit and keeps the other half, having secured the $68 dividend payment regardless of additional price movement.

After November 18th’s date of record, the investor receives their $68 dividend payment on the December 9th payment date. In total they captured $34 in profit from selling half the shares plus $68 in dividends for $102 total or 0.4% return in less than a month — equivalent to a 5% annualized return from just this single MSFT position.

Rinse and repeat the process with other soon-to-declare dividend stocks, and the compounding can significantly boost annual portfolio returns. But dividend capture does come with some notable downsides and risks…

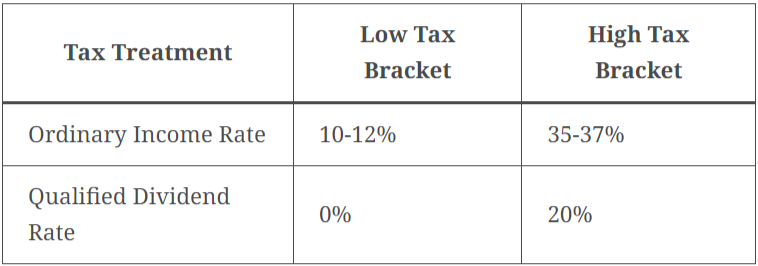

Tax Implications

The table below shows how missing out on qualified dividend tax rates severely impacts income investors using dividend capturing strategies:

With dividend captures taxed as ordinary income, rates can be 2–3x higher for investors already in higher brackets. Sizable dividends could also trigger additional Medicare or AMT tax liabilities. Consultation with a tax advisor is highly recommended when strategizing dividend capturing.

>>Related Is It Good to Buy in a Bull Market?

Now let’s examine the key potential risks and downsides.

Potential Risks and Downsides of Dividend Capturing

While dividend capture strategies can seem attractive for their simplicity and regular payout potential, investors should carefully weigh some of the key downsides first:

- Missed stock price appreciation — Frequent buying and selling makes it impossible to capture longer term share price appreciation from quality companies. Dividend capture focuses strictly on dividends alone.

- Increased tax liability — Captured dividends get taxed at higher ordinary income rates instead of the preferential qualified dividend rates for long-term holds. Significant dividends can push investors into higher brackets.

- Higher commission costs — Active trading leads to accumulated commission fees and impacts compounding if a portion of dividends go towards covering fees. Index funds minimize fees.

- Company and sector research is still required — Blindly chasing dividends without researching company fundamentals, debt levels, cash flows and so on can lead to capturing unsustainable yields right before cuts.

- Interest rates impacts — Rising interest rates tend to make fixed income products more appealing vs. speculating in stocks for dividend income. Captured dividend returns look less attractive by comparison during periods of rising rates.

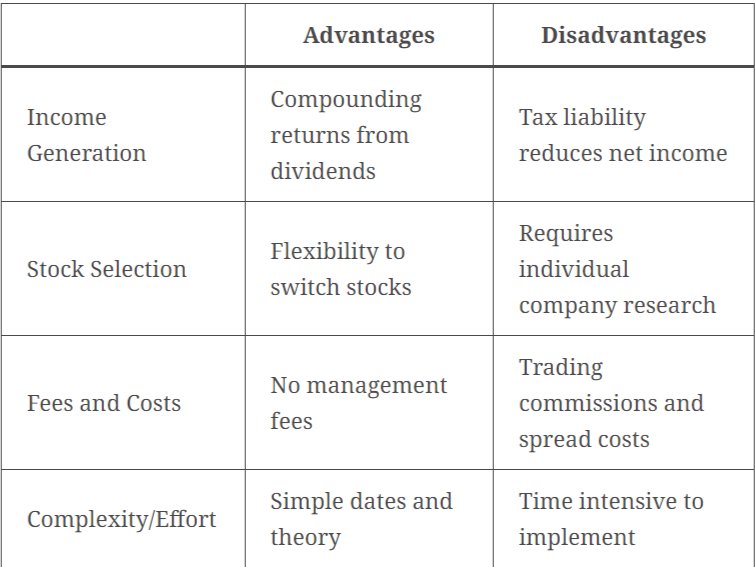

Dividend Capture Strategy Scorecard

Below is a basic scorecard summarizing some of the key pros and cons:

And finally, some frequently asked questions about dividend capture strategies:

FAQs

Q: What dividend yield is best for dividend capture?

A: Look for dividend stocks paying yields of at least 2–4%. This provides enough dividend income relative to the share price to make the active trading worthwhile. Extremely high dividend yields above 8% or so tend to be less sustainable long-term.

Q: What happens if I buy on or after the ex-date?

A: Buying shares on or after the ex-date means you will not qualify for the recently declared upcoming dividend payment. It’s crucial to buy before the ex-date.

Q: Are captured dividends qualified or ordinary income?

A: Unfortunately, dividends earned through active dividend capturing strategies do not meet the 60+ day stock holding period required to qualify for preferential tax treatment as qualified dividends. They get taxed as ordinary income.

Q: Is dividend capture legal?

A: Yes dividend capture approaches are entirely legal strategies that simply take advantage of publicly available information on dividend calendars. Companies intend for shareholders able to purchase before key dates to earn dividends accordingly through normal price adjustment mechanisms.

The Bottom Line

While easy to understand conceptually, dividend capture strategies come with enhanced risks and costs compared to traditional buy-and-hold investing. But they also offer patient, dedicated investors a compelling way to generate passive income with the right dividend stocks and system. Just be sure to have a disciplined, organized process in place and manage risks along the way.

How to Use the Dividend Capture Strategy to Generate Passive Income was originally published in InsiderFinance Wire on Medium, where people are continuing the conversation by highlighting and responding to this story.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

After reading about your article, now I can understand Tax Implications , Dividend Tax Rates Comparison as well as Dividend Capture Strategy Scorecard, thanks for your sharing!