Idi

Idio

I just started reading Advanced Portfolio Management by Giuseppe Paleologo.

About the author

- He’s on garden leave after running risk at Hudson River Trading. He has also held senior positions at Millennium, Citadel, Axioma, and IBM Research. He was formerly a mathematical researcher at Stanford and an instructor in the master’s program in Financial Engineering at Cornell University.

I started reading this book because I was interested in how fundamental investors think about risk and performance attribution. I heard the book was standard issue at Citadel for pod PMs. I haven’t verified that but I did notice that Brett Caughran strongly recommended it in his terrific 5 THINGS I WISH I KNEW AS A FIRST TIME HEDGE FUND PORTFOLIO MANAGER thread.

The first 2 chapters are brief background info. Chapter 3 starts the journey. My notes (which are intended to be references for me as opposed to “study notes”):

Chapter 3: A tour of risk and performance

- Alpha is the expected value of the idiosyncratic return and epsilon is the noise masking it.

- There’s general agreement that accurately forecasting market returns is very difficult or at least not the mandate of a fundamental analyst. A macro investor may have an edge in forecasting the market, but the fundamental one does not have a differentiated view.

- The job of the fundamental investor is to estimate alpha accurately

- The risk manager’s job is to estimate beta and identify the correct benchmark

- The error around an alpha estimate is larger than that alpha estimate itself. This is not true for beta. You cannot observe alpha directly and you cannot estimate it from a time series of returns. The fundamental analyst predicts forward-looking alphas based on deep research. The ability to combine these alpha forecasts from a variety of sources and process a large number of unstructured data is a competitive advantage of the fundamental investor.

- The chapter decomposes alpha(idio) and beta contribution and risks

Kris: found this helpful for understanding portfolio alpha even though I’ve covered this all before in https://moontowermeta.com/from-capm-to-hedging/ from my own experience.

This is my take:

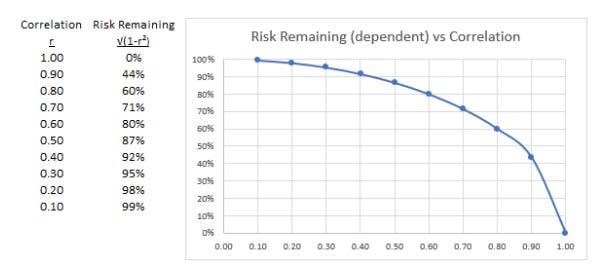

What the industry calls “idio”, I refer to as “risk remaining”. Same exact concept.

If X = market and Y = stock then this identity decomposes the risk:

Stock variance = Market variance + Idio variance

Var (Y) = R² * (VarY/VarX) + (1-R²) * (VarY/VarX)

Note that market variance is Beta² so:

Beta = R * (σᵧ /σₓ )

Risk remaining or idio is a non-linear function of correlation. As correlation drops, idio explodes. Once R is .86 or lower the idio risk exceeds the market risk!

Fyi, It’s a short book, 168 pages plus appendices.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.