Analog Devices: Correction Just Started, Still Neutral

Summary

- We’re hold-rated on Analog Devices stock.

- 4Q23 results and outlook confirm ADI will continue to experience top-line deceleration and gross margin contraction due to the industrial and auto correction through 1H24.

- We see no near-term catalyst offsetting the softer end-demand in all ADI’s end markets.

- Additionally, we don’t believe the weakness has been fully priced into the stock yet.

- We recommend investors remain on the sidelines as we see ADI being an in-line performer into 2024.

Ghulam Hussain/iStock via Getty Images

We’re maintaining our hold rating on Analog Devices (NASDAQ:ADI). We don’t think the bottom is here yet; we continue to expect the auto and industrial correction to cause top-line deceleration and gross margin contraction in 1HFY24 as the correction has just begun.

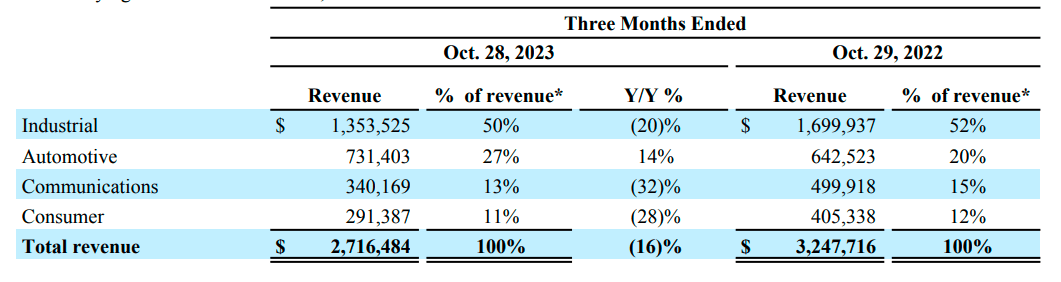

ADI reported revenue of $2.7B this quarter, up 16.4% Y /Y and 16% QoQ based on demand weakness in all end markets. Industrial sales, accounting for 50% of revenue, compared to 53% of revenue last quarter, dropped 20% Y/Y and 19% QoQ, and automotive, which accounts for 27% of total sales, increased in the slower double-digit range, up 14% Y/Y and down 1% QoQ. Our negative thesis regarding the analog market’s exposure to the last leg of the correction in auto and industrial markets is playing out.

The following chart outlines ADI’s end-market performance this quarter.

TSP

Additionally, we expect gross margin pressure to continue into next quarter due to lower fab utilization. ADI’s gross margins have been contracting each quarter since 3Q22 due to a variety of less favorable sales mix and fab underutilization. We think management will have to continue discipline in lower fab utilization to move along the industry correction for autos and industrials. Management noted that inventory levels and channel inventory levels are declining, and there’s a shift in focus on sell thru being higher than sell-in. We’re constructive on management moving along the correction cycle, but we don’t think this means anything material for the stock in the near-term as consistent with management’s expectations, we expect 1-2 more quarters of inventory correction. Management now expects all markets to be down QoQ next quarter, with the following severity: industrial, consumer, comms, and auto. We think management is too optimistic about auto faring relatively well into 2024; we believe the auto-correction has just begun, and we’re seeing the impact play out on other analog and power management names, referencing ON Semiconductor (ON).

Morgan Stanley recently upgraded ADI referencing resilience driven by higher ASP; we’re less optimistic about the higher ASP as we think prices may normalize in 1H24, negatively impacting the top-line. Foundries raised prices in 4Q22 and early 2023 for the first time, pushing analog to raise prices. Our neutral sentiment on ADI is primarily based on our belief in the following: 1. The company will continue to see weakness in all end markets, specifically as the auto and industrial corrections have just started. We expect this to impact unit sales; we’ve already seen this play out in FY23. 2. The company is at higher risk of seeing prices normalize, which will also weigh on the top-line through 1H24.

Management guided lower than consensus in 2Q23 and 3Q23; last quarter, management guided a revenue decline of 12% QoQ and 17% Y/Y decline to $2.7B. Now, management expects revenue to decline 8% QoQ to $2.5B in 1Q24. We think the weakness is getting priced into the outlook, but we still don’t think it’s been fully priced into the stock itself. ADI has been performing in-line with the S&P 500 over the past three months; we believe the stock will be an in-line performer to the S&P 500 and an underperformer to the SOX. We believe the stock still hasn’t priced in the weakness. Additionally, we don’t see any unique catalyst offsetting the macro weakness for ADI. We recommend investors stay on the sidelines for the near-term.

Valuation

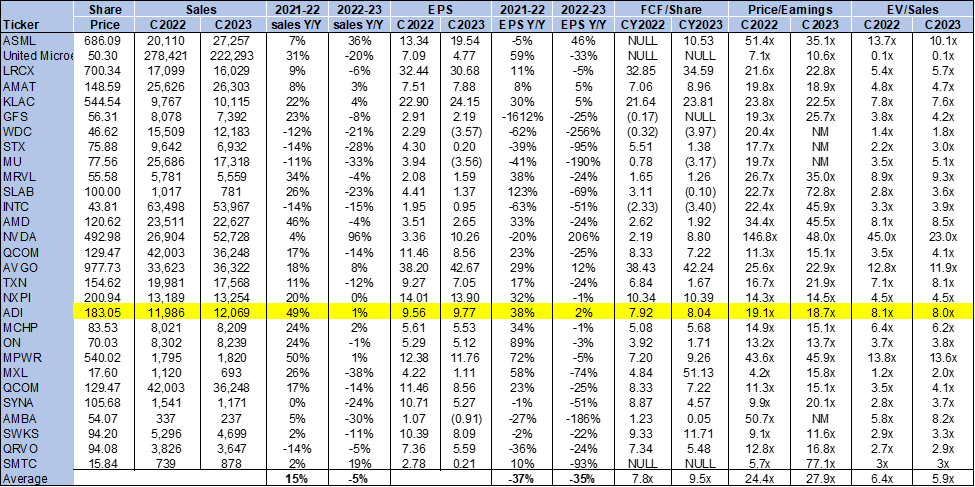

The stock is trading below the peer group. We don’t see attractive entry points at current levels, given the auto and industrial correction. On a P/E basis, the stock is trading at 18.7x EPS $9.77 C2023 compared to the peer group average of 27.9x. The stock is trading at 8.0x EV/C2024 Sales versus the peer group average of 5.9x. We think investors are better positioned on the sidelines for the near-term.

The following chart outlines ADI’s valuation against the peer group.

TSP

Word on Wall Street

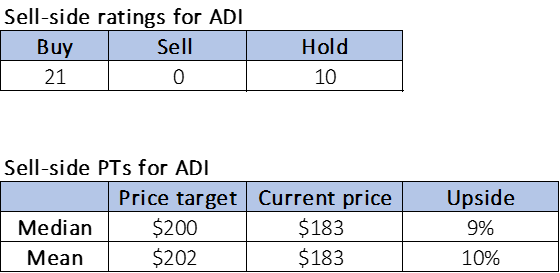

Wall Street remains more bullish on the stock. Of the 31 analysts covering the stock, 21 are buy-rated, and the remaining are hold-rated. We think Wall Street is bullish on the longer-term outlook of ADI, which we share. Still, our neutral sentiment in the near-term is based on our belief that the analog semiconductor market will underperform the semiconductor market in the near-term.

The stock is trading at $183 per share. The median sell-side price target is $200, while the mean is $202, with a potential 9-10% upside. The following charts outline Wall Street’s sentiment on the stock.

TSP

What to do with the stock

We’re hold-rated on ADI. We still don’t think macro headwinds have been priced into the stock yet as it has yet to underperform the market. We also see more pressure on auto and industrial sales through 1H24 due to the last leg of the correction. Until the correction is complete, we remain less optimistic about the analog space as we see no near-term catalyst offsetting the weaker end-market demand in the near term. We recommend investors remain on the sidelines as we see ADI being an in-line performer through 1H24.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.