Osisko Gold Royalties: Buy The Dips

Summary

- Osisko Gold Royalties has appointed a new President & CEO, Jason Attew, appointed a new Chair, and seen previous Chair Sean Roosen resign, removing previous uncertainty.

- Meanwhile, the company has closed new streams and royalties this year which has added to its already deep portfolio, offsetting the temporary suspension of operations at Renard and impairment.

- In this update, we'll look at the Q3 results, recent developments, and whether OR stock is worthy of investing following what's been a busy and volatile year.

Claude Laprise

Osisko Gold Royalties (NYSE:OR) was one of the best performers in 2023 for good reason until a key piece of the investment thesis was lost (former CEO, Sandeep Singh) which saw the stock suffer a 35% drawdown from its highs. Fortunately, the recent news has provided some needed certainty. For starters, a new President & CEO will join Osisko in February, Jason Attew, whose recent roles include the CFO of Goldcorp (responsible for corporate development & strategy) at the time of its acquisition. He was also CEO of Gold Standard Ventures ahead of its acquisition by Orla (ORLA), and most recently the CEO of Liberty Gold (OTCQX:LGDTF) where despite a difficult environment for juniors he's done an excellent job keeping share dilution to a minimum and de-risking the company's Black Pine Project in Idaho with modest cash outlays, including:

- securing process water rights and completing additional metallurgical work

- significantly increasing the overall resource to ~3.1 million

- drilling on a modest that points to further resource growth with ~4.0 million ounces looking likely, highlighted by near-surface mineralization at the Back Range, CD-Tallman and Range Front zones, while significantly expanding the M Zone.

Overall, I see these recent developments as a positive, and it was coupled with the news that Norman MacDonald will be appointed as Board Chair, succeeding Sean Roosen (who has since resigned). On another positive note, Osisko has closed the double stream transaction at the CSA Mine (silver/copper), added a couple of solid royalty assets on Costa Fuego and Namdini with the latter set to begin paying by this time next year, and we continue to see overwhelming positive news flow across the portfolio, including a potential up-lift in production from its most significant royalty due to the Odyssey South internal zones. Let's take a closer look at the Q3 results, recent developments below, and whether the stock is worthy of investing following what's been a busy year.

Windfall Mineralization - Osisko Gold Royalties (2-3% NSR) - Osisko Mining Website

All figures are in United States Dollars unless otherwise noted with C$.

Q3 Results

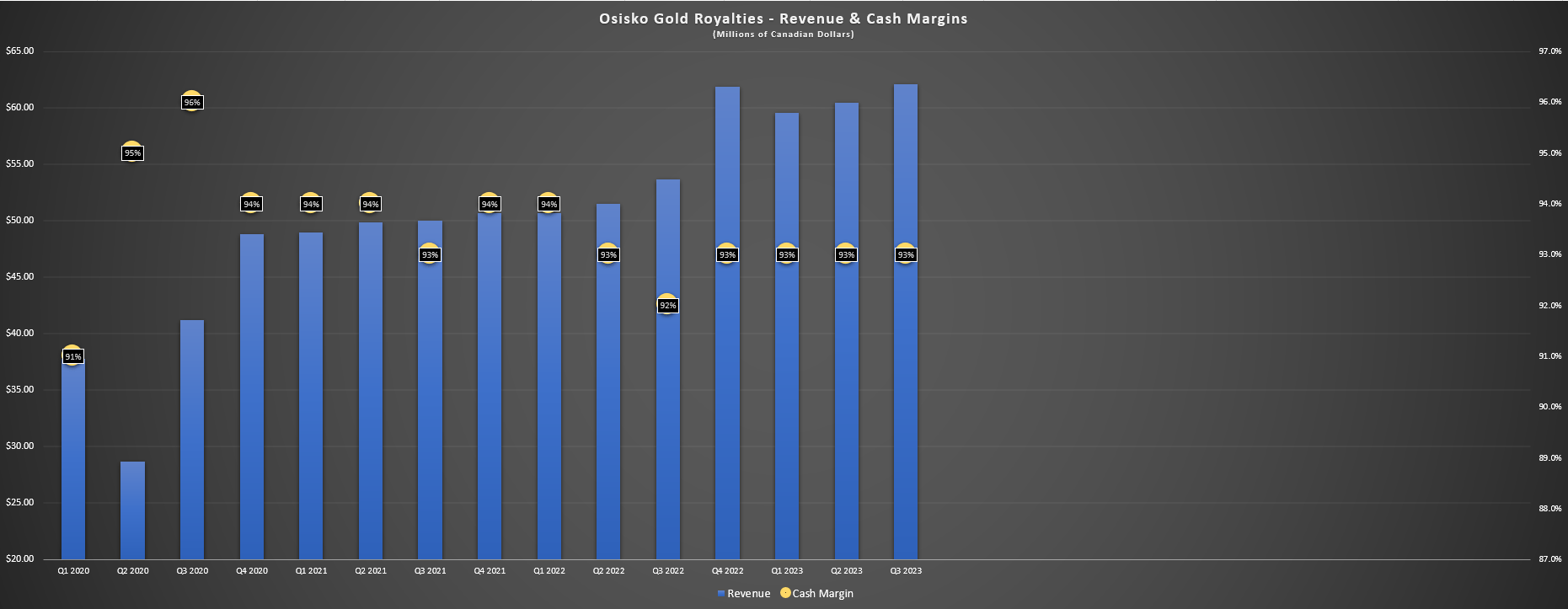

Osisko released its Q3 results earlier this month, reporting quarterly revenue of C$62.1 million, a 16% increase year-over-year. This was driven by higher metals prices which offset a slight dip in gold-equivalent ounces [GEOs] earned (~23,300 vs. ~23,900), with the company reporting an average realized gold and silver price of $1,928/oz and $23.57/oz in Q3, up from $1,728/oz and $19.23/oz in the year-ago period. Meanwhile, cash margins improve further to 93% (Q3 2022: 91.8%), with C$57.7 million in cash margin, pushing year-to-date cash margin to C$126.2 million and year-to-date operating cash flow of C$136.3 million, with Osisko ending the period with C$70.8 million in cash and ended with the quarter with C$500 million in available liquidity. On a negative note, we did see a C$17.5 million impairment at Renard due to low diamond prices and the decision to temporarily suspend operations and place itself under CCAA protection to enable it to restructure its business.

Osisko Gold Royalties - Revenue & Cash Margins - Company Filings, Author's Chart

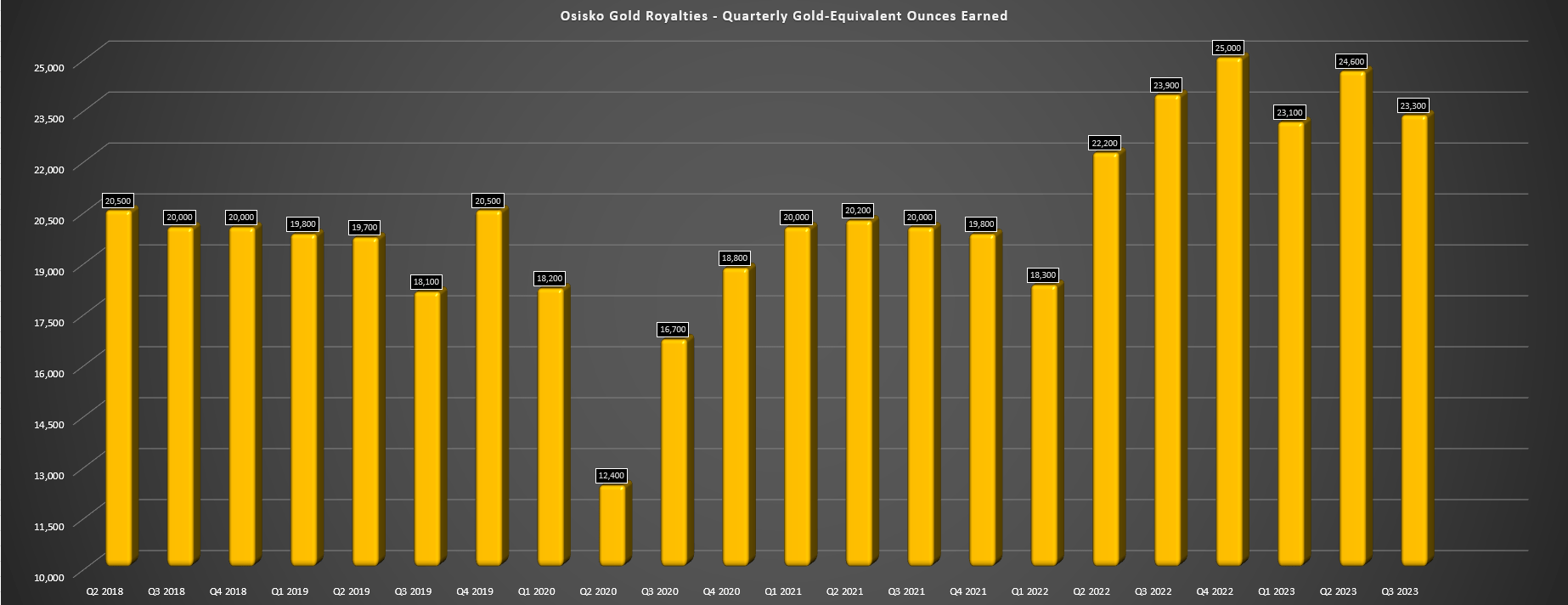

Osisko Gold Royalties Quarterly GEOs Earned - Company Filings, Author's Chart

Digging into the attributable production results, the company saw higher attributable production from Malartic, Ermitano, Bald Mountain, Sasa, and its new CSA Mine stream offset by lower production from Eagle, Eleonore, Island Gold, Seabee, Lamaque, Mantos, and Renard. However, attributable production has been higher at most assets despite the production dip at some assets in Q3, with Eagle having a better year and contributing ~6,300 GEOs, Island contributing ~2,300 GEOs, Mantos contributing ~9,400 GEOs, CSA already contributing ~2,900 GEOs, and Canadian Malartic contributing over 25,000 GEOs. And from a new asset standpoint, Osisko added a royalty on Cuiu Cuiu next to Tocantinzinho (Brazil) where it already has a royalty for $5.0 million, a 1.0% NSR (copper) and 3.0% NSR (GOLD) royalty on the Costa Fuego copper-gold project in Chile ($15.0 million), and a 1.0% NSR on the Namdini Mine in Ghana for $35.0 million.

Looking at the latter two assets, investors may be familiar with Namdini which saw a bidding war (Cardinal Resources) a couple of years ago between Nordgold, Shandong Gold and Engineers & Planners Company. The interest in the asset is not surprising given that this is an asset capable of producing ~360,000 ounces in its first three years (287,000 ounces over 15-year mine life) at an attractive sub 2.0 to 1.0 strip ratio and average grade of 1.13 grams per tonne of gold, making this a very low cost asset (translating to ~3,600 GEOs per annum starting in 2025 or ~$7.0 million in cash flow to Osisko). As for Costa Fuego, the most recently completed PEA highlights estimated production of ~95,000 tonnes of copper (~4,000 GEOs attributable to Osisko), and ~49,000 ounces of gold (~1,500 GEOs) in the first 14 years, translating to over 5% production growth from its current attributable production profile at a very attractive acquisition price. Let's take a look at other recent developments below:

Recent Developments

Mantos Blancos

Beginning with Mantos Blancos where Osisko holds a 100% silver stream, the ramp-up to 20,000 tonnes per day has been much slower than expected (Q3 2023: ~14,200 tonnes per day), with Capstone (OTCPK:CSCCF) noting that it's working to address plant stability through improved maintenance of the concentrator and tailings system, and that it now expects consistent delivery of nameplate capacity by mid-2024. And despite the hiccups getting up to planned rates consistently (which was expected to translate to higher production for Osisko this year from its silver stream), Capstone shared that it will continue to look at a potential further expansion to 27,000 tonnes per day next year assuming consistent throughput rates are achieved which could provide a further bump to Osisko's attributable production and give it three assets with up to (or exceeding in Canadian Malartic's case) 15,000 GEOs of attributable production, with these including Mantos Blancos, CSA, and Malartic/Odyssey.

CSA Mine

Looking at Osisko's newest stream, Metals Acquisition Limited (MTAL) had a solid Q3 at the high-grade Australian asset, with ~300,300 tonnes milled at an average grade of 3.4% copper (contributing to production of ~9,800 tonnes of copper and ~115,000 ounces of silver) at a much improved operating cost of ~$128/tonne vs. ~$153/tonne in Q1 2023, with further improvements to costs expected in Q4 (headcount of employees/contractors reduced in Q3 which will show up in Q4 results), and room for further improvements medium-term. This is encouraging news for Osisko investors given that the addition of two meaningful streams on an asset (100% silver, 2.25% to 4.88% of payable copper, starting at 3.0%) might have seemed a little risky (on top of an additional 1.5% copper NSR to the owner in the purchase agreement) despite its industry-leading grades given that Osisko would now be taking the entirety of the by-products and some of the primary product at a cost of just 4%.

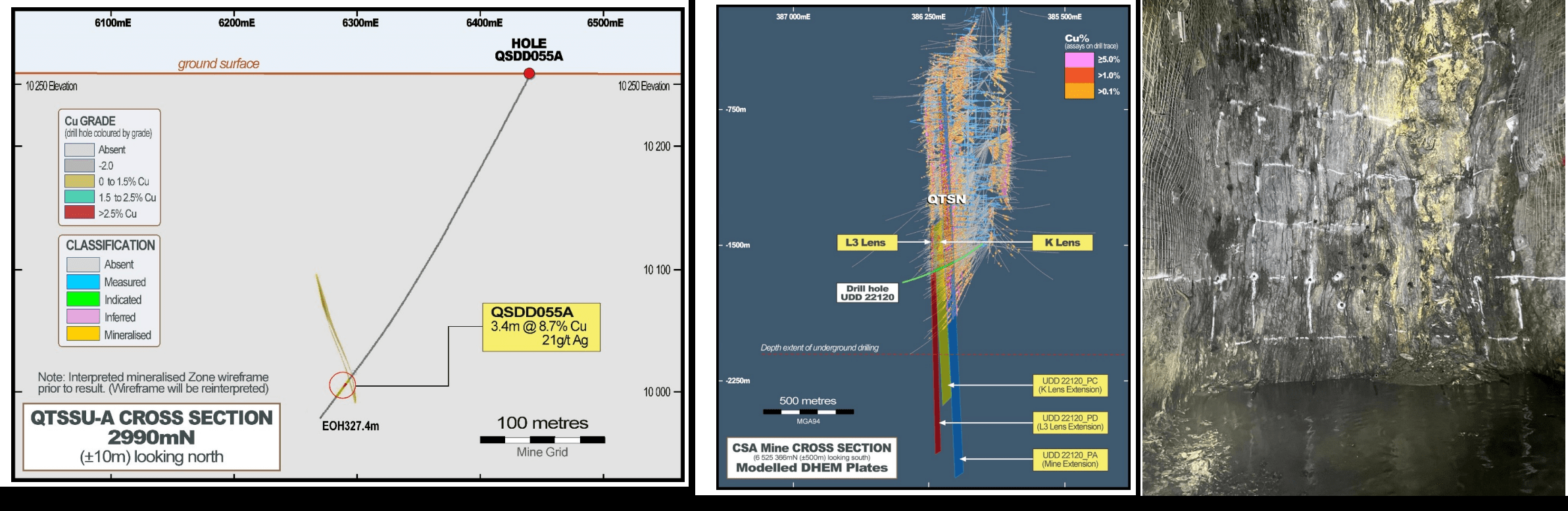

Fortunately, the company looks to be making solid progress on the productivity front which will ultimately improve unit costs and resource/reserve growth also appears to be on the horizon medium-term given successful exploration since the closing of the deal. For starters, we've seen world-class intercepts that include 50.4 meters at 8.9% copper and 36 grams per tonne of silver, 25.5 meters of 12.7% copper and 55 grams per tonne of silver, and 28.7 meters of 10.6% copper and 41 grams per tonne of silver. Not only are these exceptional intercepts with a rock value above $750/tonne, but these should help to convert inferred resources to higher confidence categories and ultimately increase the reserve base at this asset. And with the potential for a cut-off grade and growing reserves,

CSA Mine QTS South Upper, QTS North Mineralization & Downhole EM Plate Modeling - Metals Acquisition Limited

In fact, besides encouraging results from QTS North and QTS Central, the exploration upside when it comes to adding new ounces is also quite noteworthy. This is because the company reported a solid intercept of 3.4 meters at 8.7% copper in definition drilling closer to surface in QTS South Upper, confirming the potential for another high grade resource near surface with resource preparation work ongoing. Meanwhile, downhole electromagnetic [DHEM] surveying suggests the presence of sulphide mineralization extending up to 800 meters below the deepest holes drilled to date at the main QTSN, K, and L3 lenses. So, while definition drilling and resource conversion drilling have been promising, there looks to be considerable upside to the resource at depth as well. Obviously, this is great news for the operator, but also Osisko given that this is now a top-3 high-margin contributor which looks set to continue its strong history of reserve replacement.

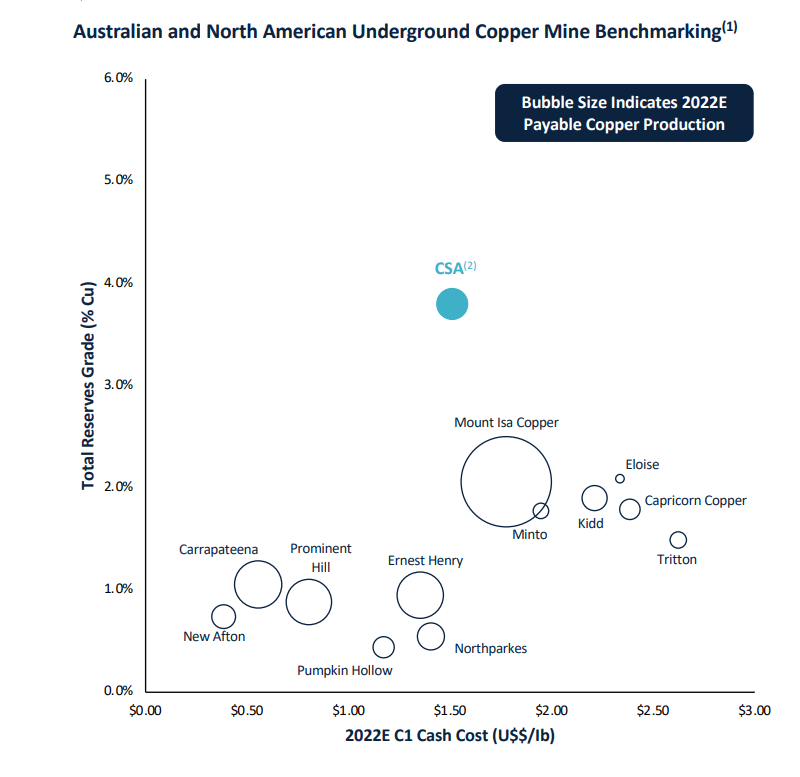

As highlighted below, this is a phenomenal asset to have exposure to and is similar to having exposure to an Island Gold or Macassa in the gold sector (top jurisdiction, industry-leading grades, meaningful exploration upside), giving Osisko another royalty/streaming asset on a world-class project which could make it more appealing to a potential suitor.

Copper Reserve Grade & Costs - Australian and North American UG Copper Mines - Metals Acquisition Limited Presentation

Island Gold

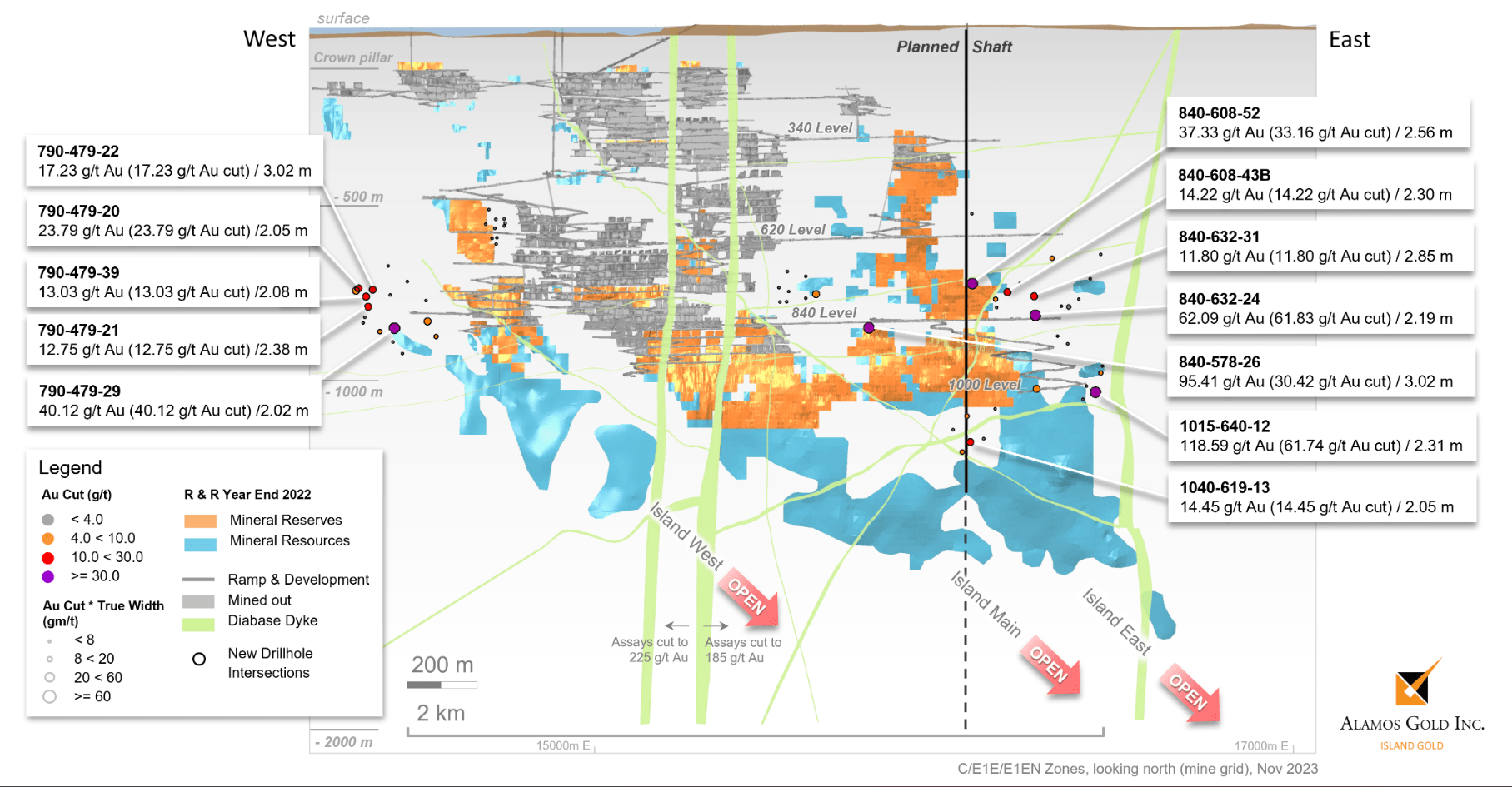

As for Island Gold where Osisko holds a 1.38% - 3.0% NSR, Alamos Gold (AGI) continues to see solid progress on its P3+ Expansion which will transform Island Gold into one of the top-10 largest gold mines in Canada from an output standpoint and the lowest-cost mine (sliding in ahead of Macassa) once shaft construction (5.0 meter diameter with 4,500 tonne per day capacity) is completed and production begins in Q1 2026. However, at the same time as production doubles to 280,000+ ounces per annum, Alamos Gold will also be moving more of mining operations towards royalty ground with a 2.0% and 3.0% royalty applicable to Osisko (ounces at lower vertical depths and Island East) vs. the 1.38%. Therefore, attributable production from this asset could start contributing upwards of 6,500 ounces per annum (~$12.5 million in contribution to Osisko) post-2025, up from ~2,500 ounces in 2022.

Island Gold Recent Drill Highlights - Company Website

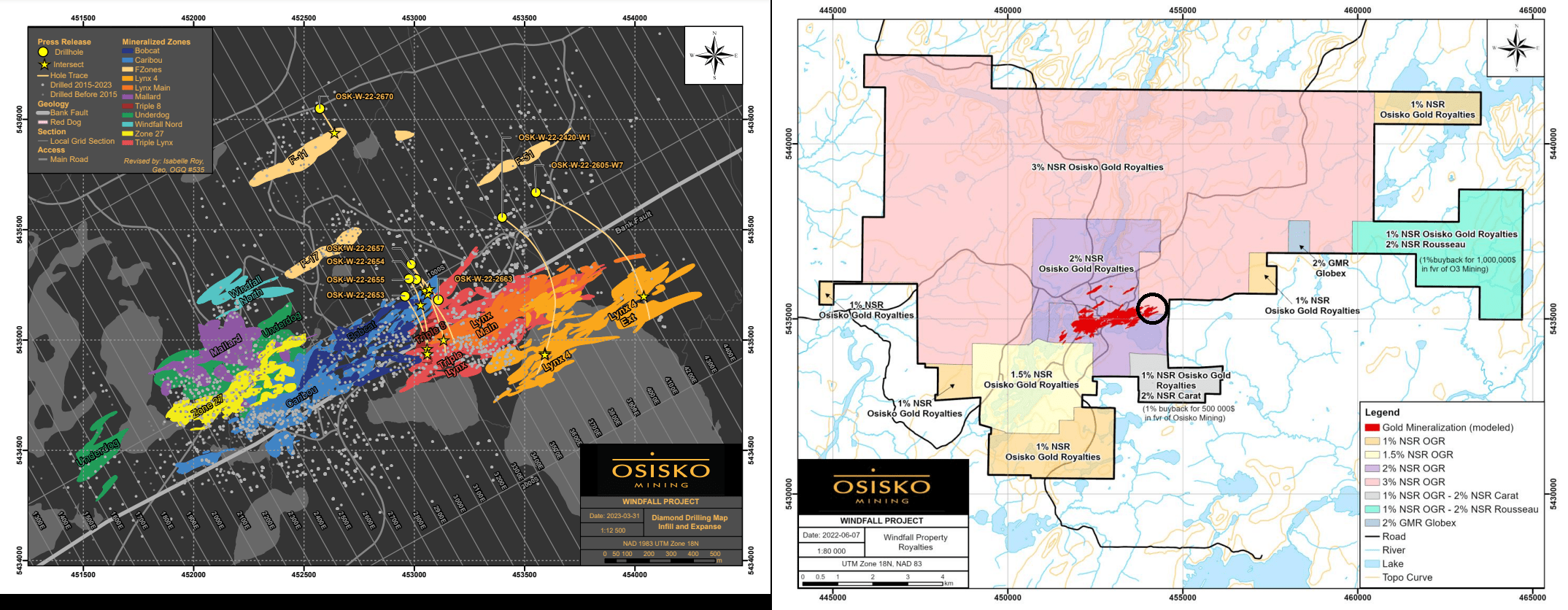

As for exploration results, Alamos reported more monster intercepts from the mine earlier this month, including 3.02 meters at 95.41 grams per tonne of gold, 2.31 meters of 118.59 grams per tonne of gold, and 2.19 meters of 62.09 grams per tonne of gold in Island East. In addition, Alamos reported more high-grade intercepts at Island West and exceptional grades from the NTH4 Footwall Zone (Island East) which included 3.14 meters at 168.03 grams per tonne of gold. Importantly, many of the intercepts reported are on higher royalty ground away from Island Main (Island East at depth and Island West), making these likely future reserves ~45% more valuable to Osisko given the more favorable royalty coverage here. This is similar to what we're seeing at the Windfall Project in Quebec, where commercial production is set to begin by year-end 2026, and drilling continues to make its way onto 3.0% NSR coverage (ounces are more valuable) vs. the primarily 2.0% NSR coverage on the bulk of the reserve base.

Windfall Royalty Coverage & Current Resources - 2022 TR & Recent Drilling Osisko

Odyssey

As for the massive and growing Odyssey Underground (Canadian Malartic), Agnico Eagle (AEM) continues to make solid progress at Odyssey, with the paste plant commissioning on track for Q3 (allowing for a ramp-up to 3,500 tonne per day mining rates) and it also shared that surface construction for Odyssey is 60% complete. And while the current 3,500 tonne per day mining rates might not seem that significant, nor does production of ~6,700 ounces from Odyssey South in Q2, the real production will come in 2027 once East Gouldie comes online. For those unfamiliar, East Gouldie will be the highest-grade and most productive asset at Odyssey where Osisko holds a 5.0% NSR, with mine production by ramp and shaft increasing to 12,000+ tonnes per day by 2030 from this deposit. So, while Odyssey may not be contributing all that much currently, it’s positive to see continued progress here, and it’s a bonus that Osisko could benefit from double-dipping with the future Upper Beaver Mine, with a 2.0% NSR on any material from the Kirkland Lake Camp west of the Quebec border as well as a $0.40/tonne royalty on any ore outside of the Canadian Malartic boundary (which would apply to Upper Beaver).

Corvette & Marimaca

Finally, looking at two assets that don't get as much attention, Corvette and Marimaca, we're seeing solid progress here as well. Starting with the smaller asset, Marimaca, it's certainly positive and a nice vote of confidence to see a strategic investment from Mitsubishi Corporation, in addition to a material increase in the oxide M&I resource to ~200 million tonnes at 0.45% copper, for a total resource of ~240 million tonnes at 0.38% copper or ~1.0+ million tonnes of copper. As highlighted in previous updates, this asset is Northern Chile is quite unique with relatively low capex (even in the potential expanded 50,000 to 60,000 tonne per annum scenario being explored), high-grade near surface mineralization for an early payback, and a relatively low strip ratio. An assuming a higher throughput rate, this could be a more meaningful contributor for Osisko with its 1.0% NSR, with the potential for up to 2,500 GEOs per annum, with the potential for the asset to head into production by 2027.

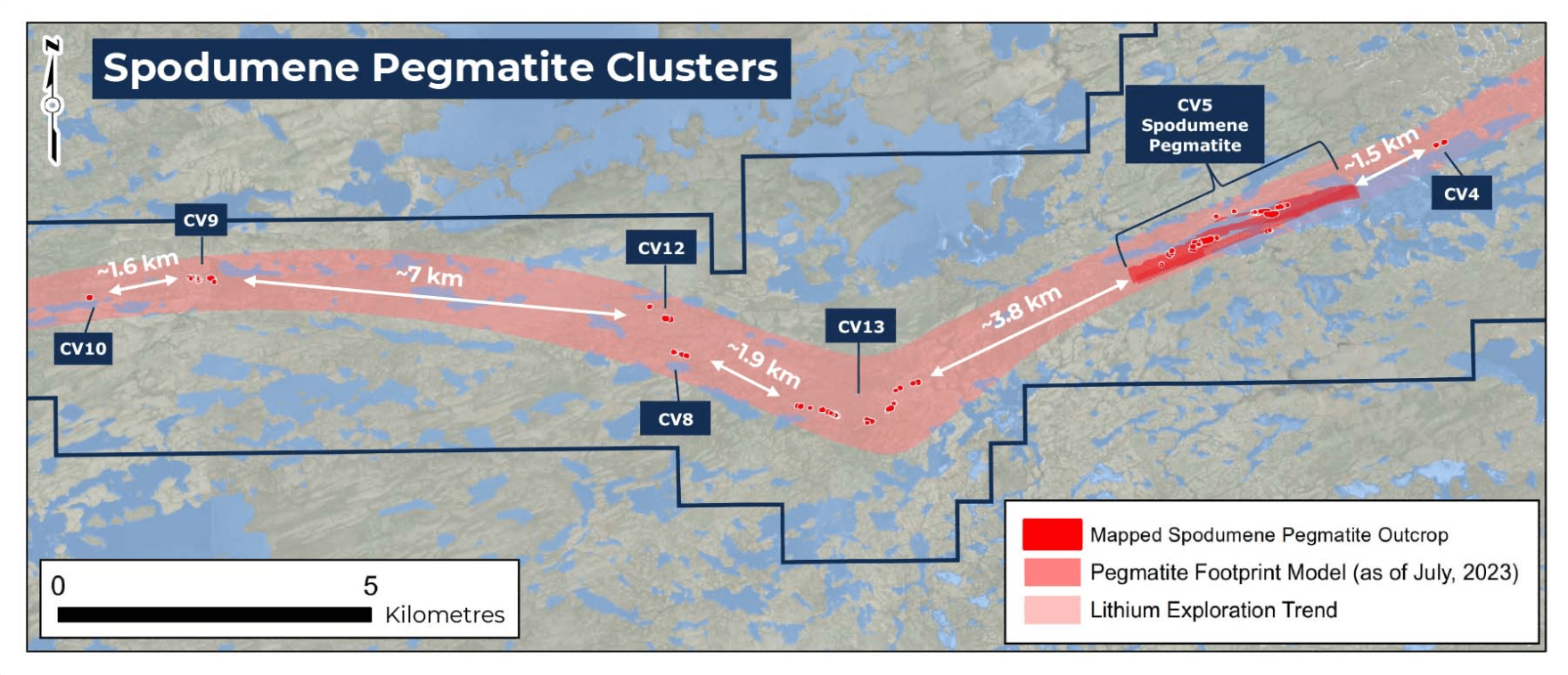

Corvette Spodumene Pegmatite Clusters - Patriot Battery Website

As for Corvette, this previous sleeper asset has is now recognized as one of the best undeveloped lithium assets globally, with a current high-grade resource of ~109 million at 1.42% Li2O that looks set to grow, and it boasts favorable metallurgy (amenable to DMS processing without need for flotation). Ultimately, this asset looks like it could be capable of generating $1.1 billion to $1.4 billion in revenue in its early years depending on spodumene concentrate prices, translating to ~$20 million per annum to Osisko (assumes effective 1.6% NSR) or ~10,000+ GEOs. However, if acquired by a major which certainly looks to be a possibility given that this is arguably a top-5 undeveloped asset (grade/scale) across any commodity in Canada, attributable production could exceed 10,000 GEOs for Osisko.

Recently, Patriot Battery Metals (OTCQX:PMETF) extended the strike length at CV5 (main pegmatite body) to ~4.4 kilometers, made a new discovery at CV9 and discovered a high-grade zone at CV13, and has already received an ~$80 million investment from lithium super-major Albemarle (ALB). And when asked about Corvette at Gold Forum Americas, Osisko's interim CEO Paul Martin stated:

"I'll chime in on our Corvette lithium royalty which is sort of an outlier in our portfolio. Is there a way of horse-trading it perhaps for something that is more in the precious space? We'll wait to see but it's an interesting piece of the puzzle and that's what having a deep development portfolio gives you is some surprises".

- Osisko Gold Royalties, Interim CEO Paul Martin

Patriot Battery Metals noted in December 2022 that it had achieved 79% recovery in dense media separation [DMS] test work, with the potential for a simple DMS processing plant without the requirement for floatation. According to Patriot Battery Metals' recent Technical Report, all 111 claims on the FCI East and West claim blocks at Corvette are subject to a 2.0% NSR held by Osisko Gold Royalties with no buyback provisions (plus a 1.5% to 3.5% sliding scale NSR on precious metals).

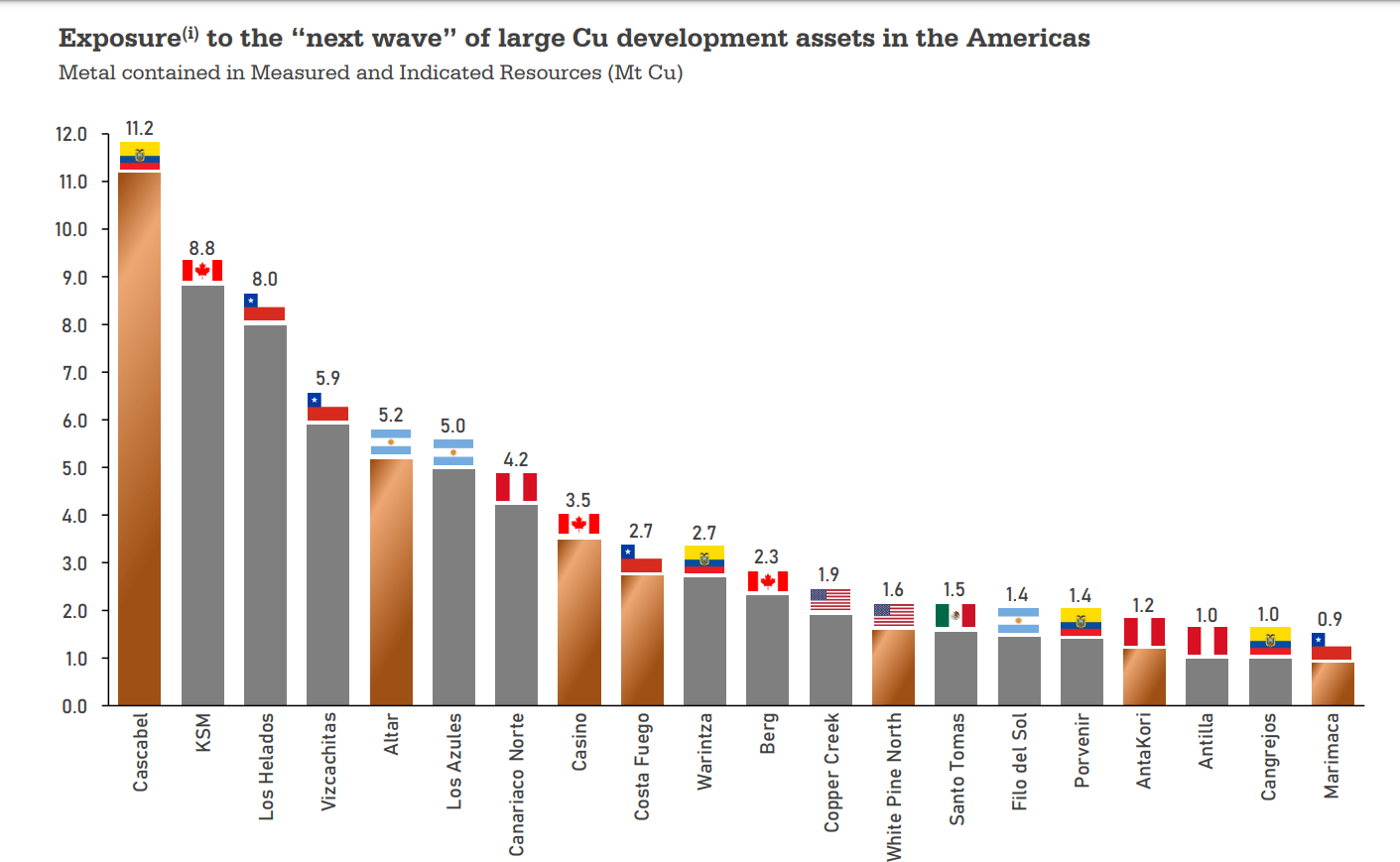

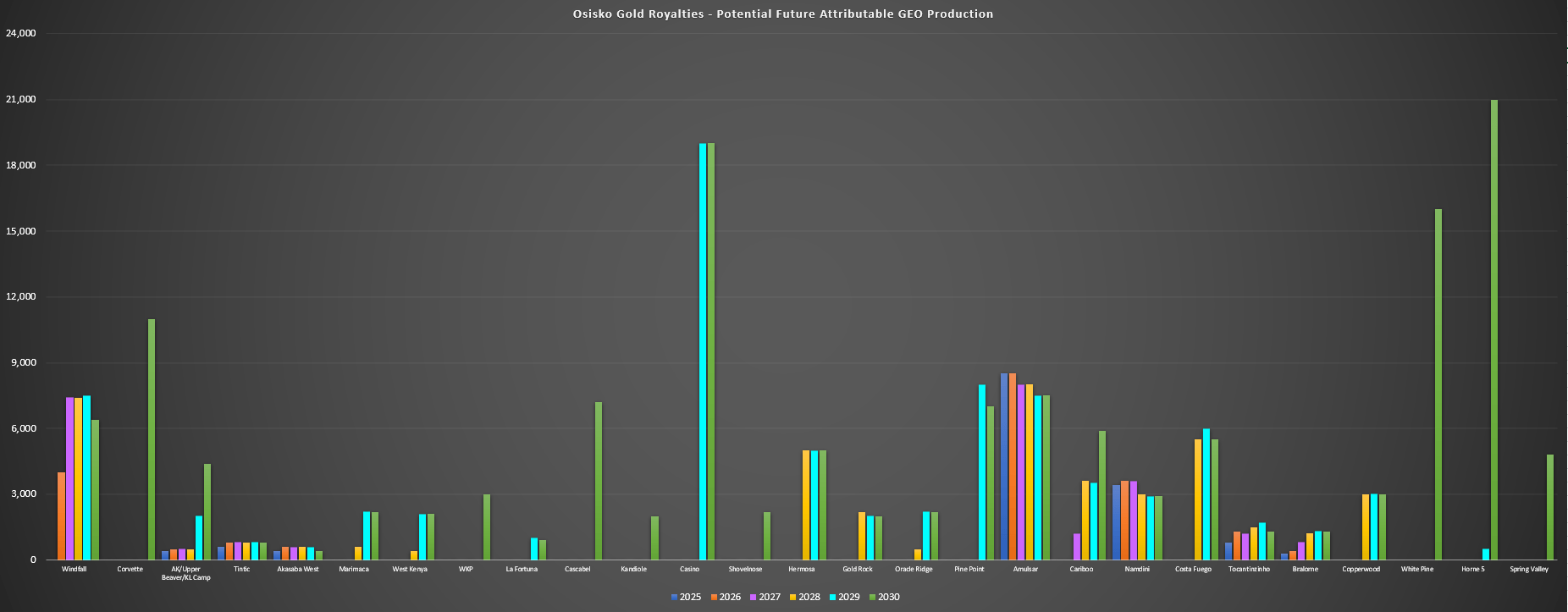

Finally, from a bigger picture standpoint, the below chart highlights potential production profiles of different royalty/streaming assets in the portfolio (does not include all assets), with the assets shown capable of producing upwards of 130,000 incremental GEOs in 2030. As we can see, some of the closer to production assets include Windfall, Amulsar, Namdini, Tocantinzinho, Amalgamated Kirkland, Akasaba West, and Bralorne, while the largest assets that would move the needle the most but without a definitive production date yet include Horne 5, Casino, White Pine, Pine Point, Corvette, Cascabel, Costa Fuego, Cariboo Phase 2, and Hermosa. It's also worth noting that deals completed over the last few years and its existing copper royalty exposure (assuming they go into production) would materially increase Osisko's weighted average mine life, with Osisko now having considerable exposure to the largest undeveloped base metals assets in the Americas as the chart below highlights.

Osisko Exposure (Orange Bars) to Large Copper Development Assets - Company Website

Future Attributable Production Potential (GEOs) to Osisko - Company Filings, Author's Chart & Estimates

Obviously, some of these assets like Casino (~18,000 GEOs), White Pine (16,000+ GEOs) Shovelnose (~2,000 GEOs), Kandiole (~2,000 GEOs) have a less definitive timeline for heading into production and would be less certain than other assets already in construction or held by well-capitalized operators and or with strong partners like Hermosa (4,000+ GEOs), Corvette (~10,000 GEOs), Windfall (~7,000 GEOs in earlier years), Tocantinzinho (~1,500 GEOs in earlier years), Upper Beaver/Kirkland Lake Camp (~4,000 GEOs), Namdini (~3,400 GEOs in early years) and Marimaca (2,000+ GEOs). And importantly, even if we focus on expansions on producing assets (Island, Mantos), newly producing assets (CSA Mine), and assets with a higher probability of going into production by 2030, we should see a 60,000+ incremental increase in production. However, in a better case scenario and assuming a chunky asset or two comes across the finish line and moves into production, this figure could come in closer to 100,000 GEOs.

To summarize, while Osisko is a company with ~95,000 GEOs of attributable production next year with suspended operations at Renard and no further contribution expected from San Antonio without permits (processing of stockpile inventory completed), this is a portfolio capable of producing closer to 170,000 GEOs, translating to ~$300 million in annual cash flow. And in a better-case scenario where some optionality projects that are not getting any value today move into production, this figure could easily increase to 200,000 GEOs (Casino, Horne 5, Back Forty, Hammond Reef, Spring Valley, White Pine, Cascabel). Importantly, most of these optionality assets are in Tier-1 ranked jurisdictions and would not lead to multiple compression but, in fact, multiple expansion, with a combination of higher diversification, greater scale, and increased cash flow from Tier-1 jurisdictions.

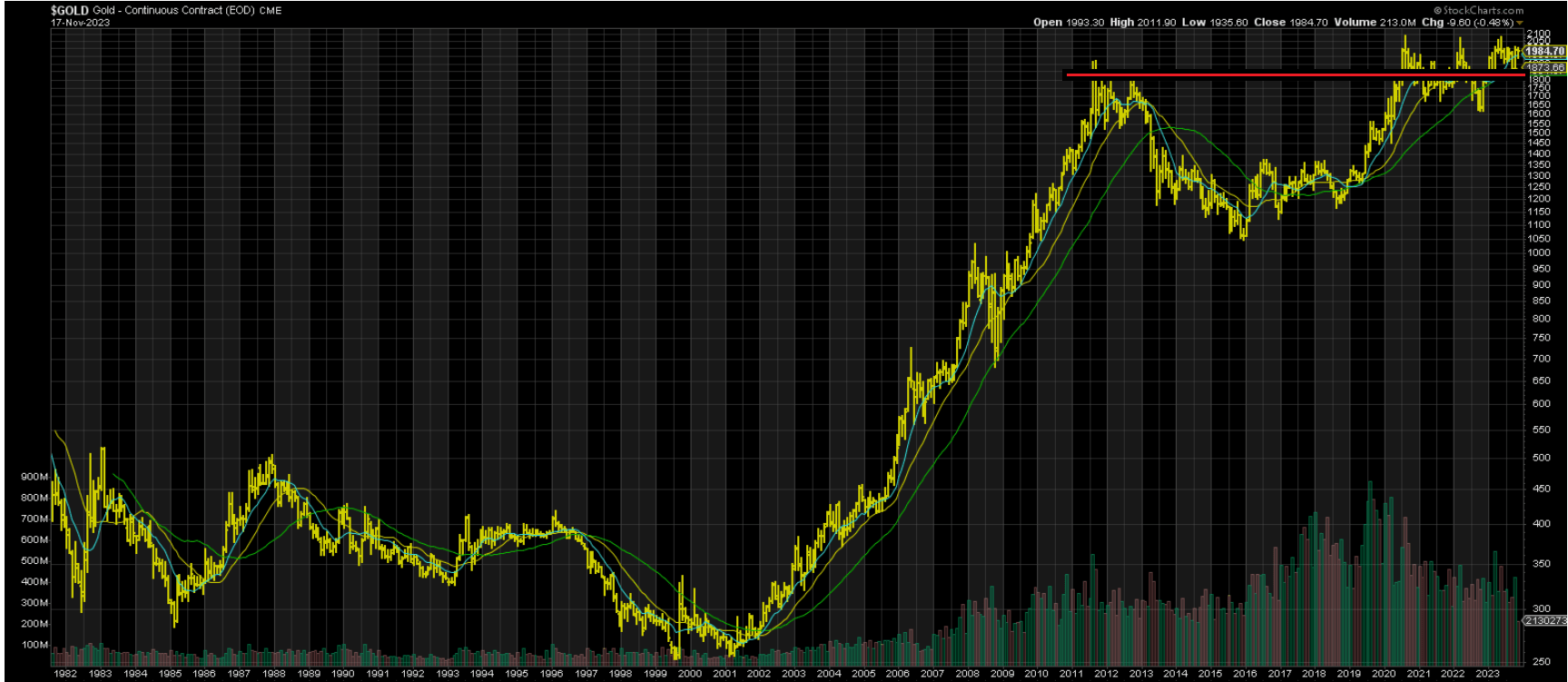

Gold Price Long-Term View - StockCharts.com

Using what I believe to be a conservative multiple of 22.0x cash flow once it scales and sees improved diversification (new assets will dilute Malartic as a percentage of cash flow) and ~192 million shares, this is a stock that could ultimately trade at a ~$7.0 billion market cap [US$36.00] at the end of this decade. Plus, with the gold price continuing to inch higher and the $1,800/oz level looking more like the new floor than the ceiling it was ahead of the secular bear market from 2013 through 2015, I think these 2030 cash flow estimates could end up being conservative.

That said, given the quality of this portfolio and its industry-leading depth with Osisko's tentacles in multiple world-class assets (including Corvette, which could have a similar annual contribution to Eagle), I don't think it's likely that Osisko is around by 2027 (let alone 2030) if it stays at its current multiple. This is because hunting down growth is getting more difficult in Tier-1 ranked jurisdictions for the big three royalty/streamers, meaning that the best use of liquidity and relatively expensive currency might be to scoop up Osisko Royalties while it's still available at a very attractive valuation.

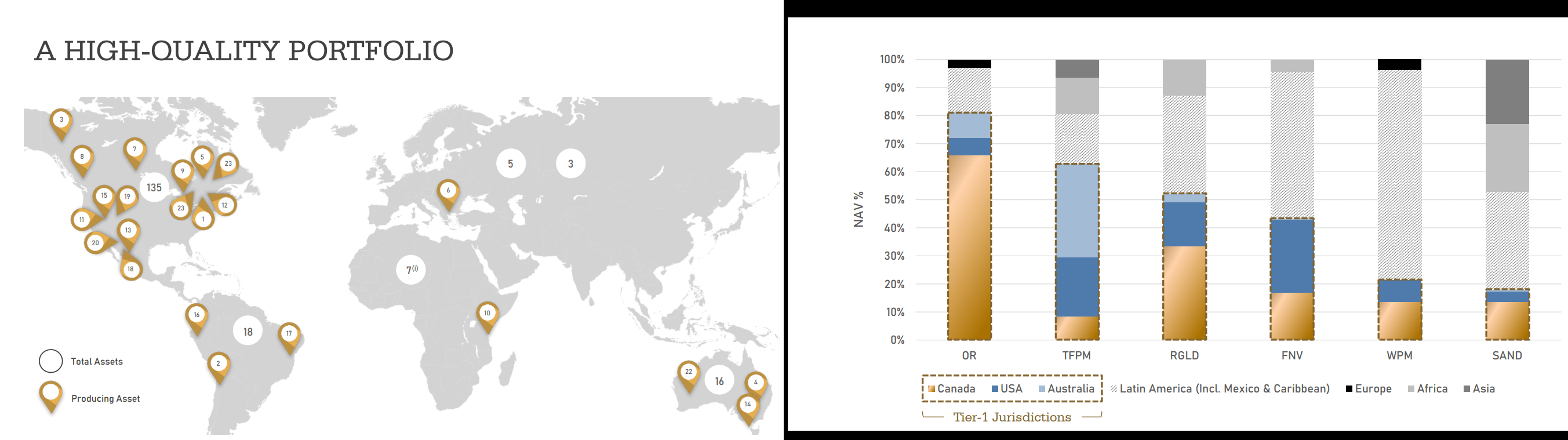

Osisko Gold Royalties - Total & Producing Assets & NAV tied to Tier-1 Jurisdictions - Company Website

On a more current basis and using what I believe to be a conservative multiple of 1.35x P/NAV for a primarily Tier-1 royalty/streaming mid-tier, I see a fair value for the stock of US$18.30, pointing to a 30% upside from current levels.

Summary

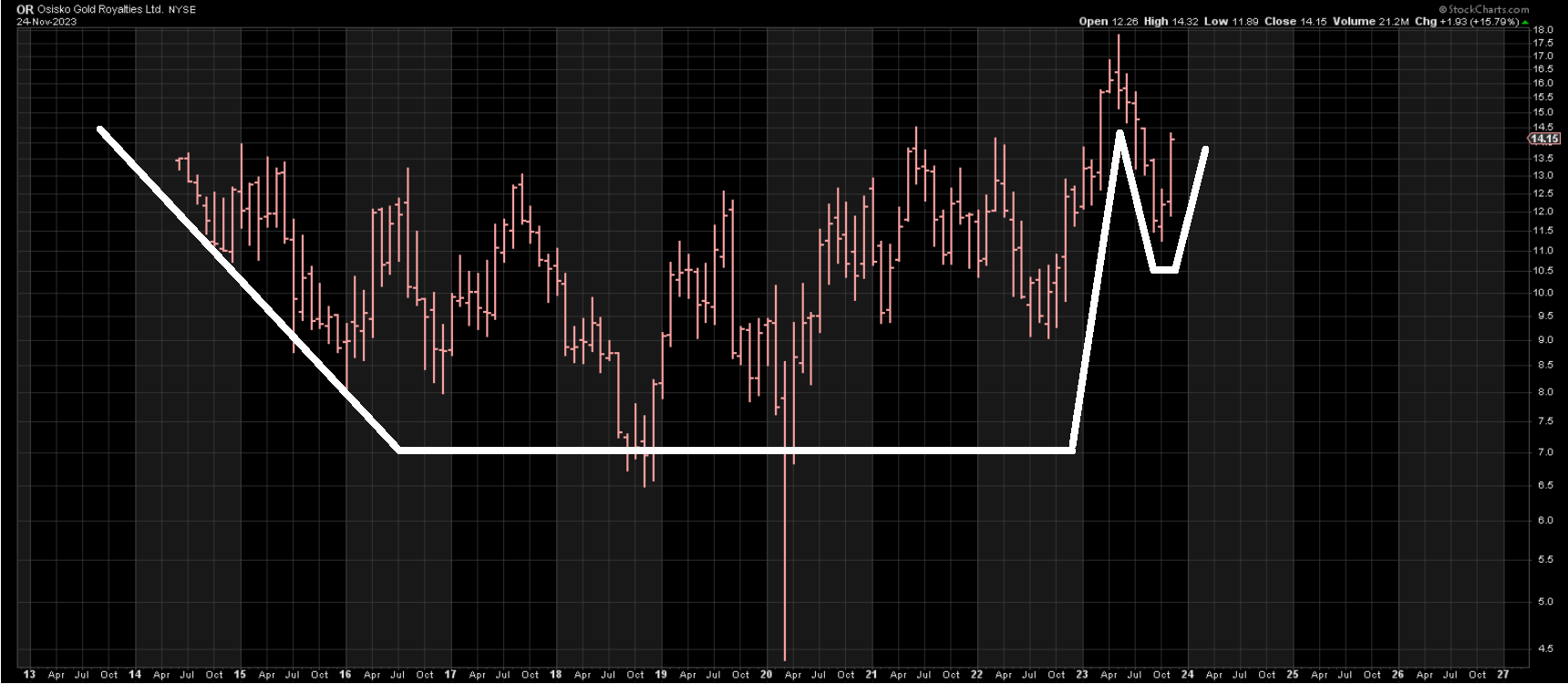

Osisko Gold Royalties' stock flipped from outperformance to severe underperformance over the past several months, but the stock looks to have found a bottom and made a much higher low with added certainty over the past month, with it now having a handle to its 9-year basing pattern. This is coinciding with what looks like a potential turn in sentiment for the Gold Miners Index (GDX) as a whole and this underperformance is entirely unjustified given that Osisko has not seen the margin compression that its peers have over the past two years, making this a case of the baby being thrown out with the bathwater. Plus, the CSA Mine closing is certainly a very positive development that has been overshadowed by recent uncertainty, but this should provide a nice boost to near-term cash flow when combined with Namdini (late 2024 production), Tocantinzinho (mid 2024 production), Amulsar, and a ramp-up in production at Mantos (targeting consistent throughput at 20,000 tonnes per day rates).

Osisko Gold Royalties Long-Term Chart - StockCharts.com

On a medium-term basis, multiple other assets will contribute to growth to 120,000+ GEOs by 2027, including Windfall, higher production on more favorable royalty ground at Island Gold, and potentially Cariboo, more than offsetting negative developments at Renard, lower production at San Antonio, and a slower than planned delivery on first production at Cariboo (previously 2024 according to the operator). This suggests material growth in revenue and free cash flow all while the company has meaningful liquidity to take advantage of new opportunities in the best environment for royalty/streamers in nearly a decade (expensive debt, low equity prices and risk-off environment for developers means royalty/streaming transactions are the more favorable option). In summary, I see Osisko as a name that's well positioned to outperform over the next 12-24 months with the potential for an accelerated re-rating given its status as a top takeover target, and I would view any pullbacks below US$13.30 as buying opportunities.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.