indie Semiconductor: Star Performer In The Semiconductor Industry

Summary

- indie Semiconductor has been the fastest-growing semiconductor company out of 224 others over the past two years.

- The company is expected to reach non-GAAP EBITDA breakeven in 4Q23, making it the only semiconductor company that IPO-ed in 2021 to achieve this.

- The strategic backlog grew from $4.3 billion in 2022 to $6.3 billion in 2023, demonstrating strength and momentum in the business even amidst a difficult macro.

- The recent wins suggest that business momentum continues to be strong and further validates indie Semiconductor's product portfolio and technology.

- The company continues to innovate and launch new products into the market to improve its competitive advantage and improve cross-selling within its customer base.

SweetBunFactory

indie Semiconductor (NASDAQ:INDI) had a very remarkable quarter in 3Q23.

I am genuinely impressed by what the company has achieved as a small-cap company even as the overall macro backdrop has been weak and the overall automotive industry showing weakness.

Specifically, according to Morgan Stanley, indie Semiconductor has been the fastest-growing semiconductor company out of 224 others over the past two years.

On top of that, indie Semiconductor is the only semiconductor company that IPO-ed in 2021 and is expected to reach non-GAAP EBITDA breakeven in 4Q23.

I think this highlights just how differentiated indie Semiconductor is compared to other competitors, and more importantly, that its strong growth is sustainable given the focus on profitability as well.

I have written extensively on indie Semiconductor, which can be found here. I have a constructive view of the company given its strong technological differentiation, solid backlog, and strong execution from a competent and quality management team. The follow-up coverage of the company in this article will delve deeper into the recent quarter and highlight why I think indie Semiconductor is a star performer in the industry.

Results surpassed expectations

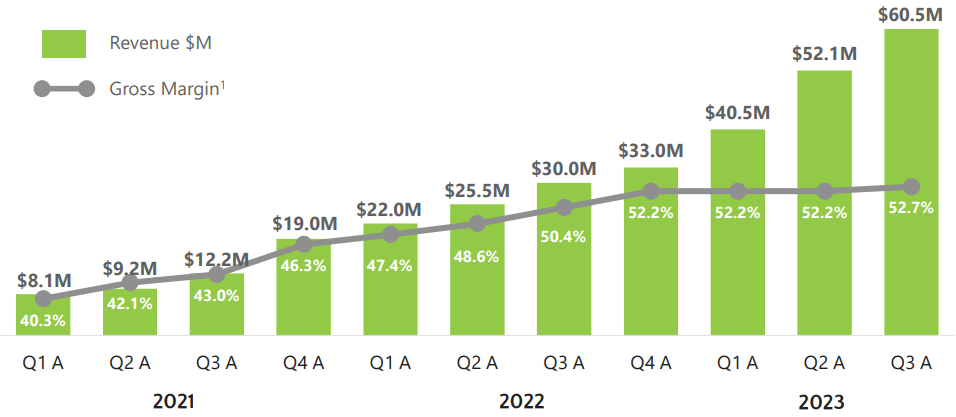

indie Semiconductor's revenue grew 101% from the prior year and 16% sequentially, showing no signs of weakness given the strong backlog the company has, which I will go into greater detail in the next section.

Revenue growth (indie Semiconductor)

While most small caps prioritize growth over profitability, indie Semiconductor is able to achieve both.

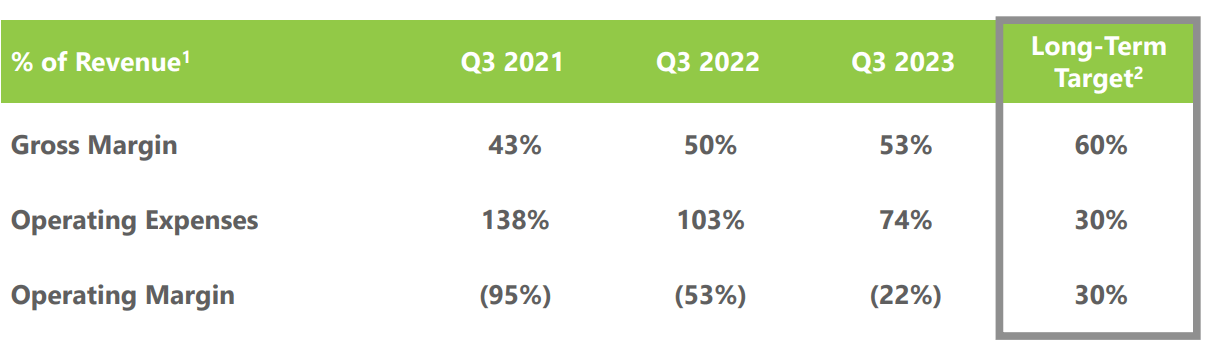

As can be seen below, gross margins improved by 10 percentage points in two years, going from 43% in 3Q21 to 53% in 3Q23. The company is making great progress towards the company's long-term target of 60%.

On top of that management has a long-term target of achieving operating margins of 30%.

Even though indie Semiconductor's operating margins are at negative 22% in 3Q23, the company has improved this by 73 percentage points in just two years. I expect that the company will continue to see improvements in operating margins as operating expenses grow at a slower pace than revenues.

Margin profile (indie Semiconductor)

R&D in 3Q23 was elevated as expected due to multiple product tape-outs. SG&A was also elevated in the quarter as a result of higher international sales and marketing activity.

In 3Q23, indie Semiconductor posted a $0.08 loss per share, which is in line with the company's guidance.

In 3Q23, the company spent $2 million in capital expenditures to expand its quality lab capabilities, making up just 3% of revenues.

indie Semiconductor exited 3Q23 with $161 million in cash on its balance sheet.

The company also completed its warrant exchange tender offer, retiring potentially 27 million shares, and thus, helped existing shareholders substantially reduce the risk of future dilution.

Solid guidance

As I will mention below, indie Semiconductor has a strong strategic backlog that provides visibility into revenues.

For 4Q23, management expects revenues to grow in the range of 112% to 127% from the prior year to $70 million to $75 million.

Based on that growth rate, gross margins are expected to improve 50 basis points from the prior year to 52.7% in 4Q23.

Management expects to spend $30 million in R&D, which is a more normalized level after the recent product tape-outs in 2Q23 and 3Q23. For reference, 3Q23's R&D spend was about $43 million.

Management also expects SG&A to return to 2Q23's level in 4Q23, coming down from $20 million to $9.5 million in 4Q23.

Most importantly, management expects to reach EBITDA breakeven for the first time in the company's operating history in 4Q23.

In 4Q23, management expects $0.01 net loss per share.

To give further color on this, I would highlight that for 2024, management is committed to maintaining a full year of profitability after achieving this breakeven milestone in 4Q23.

This is possible because from an operating expense standpoint, while the nominal value will go up in 2024 when thinking about it as a percentage of sales, the number should come down in 2024.

This is a result of the improvements in operating leverage that will drive the improvements in profitability as indie Semiconductor continues to scale up.

On a high level, the company continues to target 60% gross margins and 30% operating margins in the long term.

Huge backlog grows even larger

For a company with a market capitalization of just $1 billion, indie Semiconductor increased its strategic backlog from $4.3 billion in 2022 to $6.3 billion in 2023. For reference, the strategic backlog was at $2.6 billion in 2021, which means that in just two years, it grew more than two times.

Where did this $2 billion increase in its strategic backlog come from?

This was led by Computer Vision as a result of its acquisition of GEO Semiconductor earlier in 2023, along with post-integration wins like that of Bosch, which also brought in a leading North American OEM and Toyota into the backlog.

About $4.6 billion of the strategic backlog, or more than 70% of it, is contributed by the ADAS segment of indie Semiconductor, which shows me how strong the company's ADAS offering is.

The remaining 30% of the backlog is heavily tilted toward the User Experience segment, while indie Semiconductor's Electrification products are still in an early stage of growth.

More crucially, management stated that these wins that contributed to the $6.3 billion strategic backlog set the stage for indie Semiconductor to generate more than $1 billion in revenues by 2028.

I really like how strong the visibility is for the company given its current pipeline and backlog.

How does this backlog relate to actual revenue generation?

Management stated that for 2024, the company is almost fully booked.

However, given we know that the current strategic backlog is at $6.3 billion, how do we know how much of that will be generated in the near term compared to the long term?

Management gave a rule of thumb where if you divide the strategic backlog by 10, that gives you an idea of where the revenue will be three years plus from now.

With the current $6.3 billion in strategic backlog announced for 2023, this implies that in 2026, we could see indie Semiconductor's annual revenue reach $630 million.

In fact, management made a comment that the majority of the $4.6 billion in ADAS strategic backlog highlighted above will begin to ramp by 2025, while there are only a few wins that are expected to ramp in 2026 and beyond.

Again, I think this highlights the strong visibility management has as a result of its current strong strategic backlog.

Recent wins

I have probably mentioned this multiple times, but indie Semiconductor has a unique sensor fusion strategy as it employs several modalities, like LiDAR, Radar, Computer Vision, and Ultrasonic Solutions, in order to obtain data from the environment and generate comprehensive and accurate perception of the surroundings of the vehicle.

I think this sensor fusion approach has a huge advantage as it does not rely on any one technology winning in order for the company to succeed. Furthermore, the multi-modal approach brings about redundancy and overcomes the limitations of individual sensors. to bring about driving outcomes that are safe and precise.

Within the Computer Vision space, indie Semiconductor secured a key win with a leading North American automotive OEM. This new win is expected to ramp in 2025 and it is also a considerable contributor to the increase in indie Semiconductor's strategic backlog.

This win came from an existing customer and given that this was specifically mentioned in 3Q23 results highlight the significance of this win to the backlog.

For the Radar space, indie Semiconductor sampled its first product to its lead customer in 3Q23, and the potential remains promising.

In terms of indie Semiconductor's LiDAR business, I am impressed by the management team's progress and conviction.

More specifically, the company made progress with its Surya SoC with direct OEM engagements, including with a leading Japanese carmaker, amongst others.

In addition, while it has entered into a development contract with a leading aerial mobility OEM, the company has not yet recorded any LiDAR wins in its strategic backlog to be conservative.

The most promising and exciting for me within the LiDAR space is that based on the interest that indie Semiconductor is seeing in Surya, management stated that they "fully expect material contributions by this time next year to drive to a leadership position as a merchant LiDAR semiconductor supplier and scale dramatically throughout the back half of this decade".

For management to make such a bold claim, I think the interest in Surya, and thus, indie Semiconductor's LiDAR offering is very strong.

Within the User Experience segment, indie Semiconductor continued to ramp its Advanced Lighting solutions with global OEMs.

In 3Q23, the company obtained a Qi2.0 Wireless Charging design win with a leading US carmaker.

Within the Electrification segment, while indie Semiconductor did not post any wins this quarter, the management team highlighted the breadth and large number of customer engagements with leading electric vehicle players like NIO (NIO), Rivian (RIVN), Ford (F), General Motors (GM), Li Auto (LI), Volkswagen (OTCPK:VWAGY), Mercedes (OTCPK:MBGAF), XPeng (XPEV), amongst many others.

Just to further elaborate on this point, given indie Semiconductor's $6.3 billion strategic backlog, this huge backlog covers virtually every car OEM in the world, and it includes 20 Tier 1s within the company's 12 unique product areas.

As a result, this means that indie Semiconductor has some content at all OEMs and all Tier 1s.

While some OEMs and Tier 1s will undoubtedly be larger customers than others, the entire backlog is very diverse and has a large breadth.

With these relationships with OEMs and Tier 1s, it also provides indie Semiconductor with the opportunity to cross-sell different products within its portfolio.

I expect this dynamic to bring further momentum to the business given the early stage in which indie Semiconductor is at today.

New products and technology

As a small company within a competitive automotive semiconductor market, indue Semiconductor has to innovate and bring better products to the table.

And this has been what the company has achieved quarter after quarter.

In 3Q23, the company expanded its automotive Camera Video Processor portfolio, as it released commercially a highly integrated system-on-chip that enables both viewing and sensing capability simultaneously.

After the acquisition of Silicon Radar earlier in 2023, the company also released the very first commercially fully integrated 240 gigahertz radar front-end silicon transceiver in the world. With this new product, indie Semiconductor's portfolio of short-range, high-precision, and millimeter wave radar solutions has been further expanded.

Valuation

Given the improved visibility into 2026 and beyond, I am rolling my 5-year forward forecasts until 2028.

I assume that in 2026 and 2028, management can at least meet their estimates or guidance of around $630 million in revenues for 2026 and $1 billion in revenues in 2028. I do think there's scope to beat this target, but it is good to be conservative for now given 2028 is still five years away.

Likewise, by 2028, I expect the gross and operating margins to be close to or meet the targets of 60% and 30% respectively.

With the pivot to profitability, the price targets can now be based on a P/E multiple. I applied an 80x 2024 P/E multiple here, which amounts to 1-year price target of $11.60.

To be clear, because the company is expected to turn profitable only in 2024, given the low base of its EPS and huge growth in subsequent years as it scales, the 80x 2024 P/E is justified, in my view.

The higher 2024 P/E is due to the fact that it is the first year of positive EPS that indie Semiconductor is posting, and margins are expected to ramp from there. While the P/E multiple is higher than the 22x P/E multiple at which the sector is trading, the higher growth profile, strong execution, and positive idiosyncratic upside need to be rewarded with a higher multiple.

As such, I think that the 80x multiple is justified in the case of indie Semiconductor given its first year of earnings inflection and a long runway for growth ahead.

Conclusion

While the automotive industry has been seeing some weakness, indie Semiconductor has shown that despite it also experiencing some headwinds given it is in the industry, it remains insulated and resilient given the strong growth and results that it has shown.

In particular, I am impressed by the growth in the strategic backlog to $6.3 billion, the recent wins, and continued innovation and new products launched. On top of that, the company has been executing well, scaling the business efficiently, and driving non-GAAP EBITDA breakeven. On top of that, the company has made targeted acquisitions that supplement the current portfolio of the company and has also done a good job integrating the multiple acquisitions made.

This can be attributed to its best-in-class design team, which led to an extensive and innovative product portfolio that continues to expand, a strong relationship with virtually every single automotive OEM and Tier 1 that leads to more effective cross-selling, and it's very scalable supply chain along with its successful acquisitions that it has been making to further augment and complement its capabilities.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.