Household Financial Distress Is Rising - Short Ally Financial

Summary

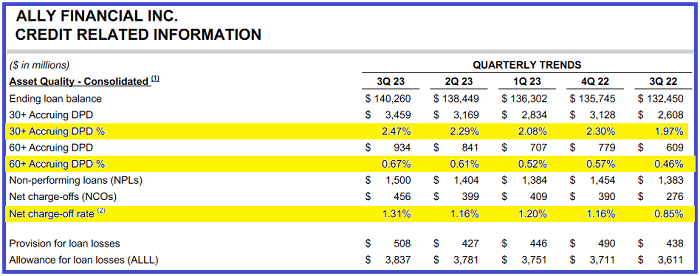

- Auto loan delinquencies and defaults continue to rise as do repossessions.

- While Ally offers mortgages and credit cards, auto loans represent 78% of its finance receivables and loans.

- In Q3, 33% of its auto loan originations were to subprime borrowers, which is consistent with the historical pattern.

- ALLY’s profitability is declining and the riskiness of its balance sheet is rising.

Pekic/E+ via Getty Images

As an indicator of rising consumer stress and stretched household finances, a report from Edmunds.com showed that auto loan borrowers with negative equity were underwater by an average of $6,054. This is the most since April 2020 and well above pre-pandemic averages. Auto loan delinquencies and defaults continue to rise as do repossessions. This is a double-whammy for auto loan lenders because used car prices are falling, which means the value of collateral backing these loans is declining. This also means that recoveries are declining and write-offs are increasing - and will continue to increase. I discussed this with respect to $CVNA in the December 10th SSJ.

This is bad news for Ally Financial (NYSE:ALLY) ($35.17). While ALLY offers mortgages and credit cards, auto loans represent 78% of its finance receivables and loans. For the latest quarter, ALLY's pre-tax income from continuing operations plunged 45.3%. In Q3, 33% of its auto loan originations were to subprime borrowers, which is consistent with the historical pattern. I suspect this will bite ALLY in the ass in 2024.

The 30+-day and 60+-day delinquency rates have been rising steadily over the last four quarters. The charge-off rate rose 54% in Q3 YoY. The declaration of a "delinquent" loan is nebulous, however. This is because lenders will grant an extension (temporary forbearance) up to a certain point. Extended loans are not classified as delinquent. Recall from the last issue that CVNA has granted extensions on over 10% of its outstanding loan balance in September, up from 1.97% in September 2022. While it is likely that ALLY has not extended 10% of its loans outstanding, I have no doubt that it has extended a material percentage (over 5%). Ally is likely massaging its GAAP numbers with the granting of extensions, the deferment of charge-offs and the minimizing of its allowance for loan losses (a non-cash GAAP expense). That's a common source of GAAP earnings management with banks and finance companies.

While the financial distress numbers above may look small in relation to the total size of ALLY's balance sheet, I believe that they understate the true level of delinquencies and defaults that ALLY may be experiencing. Moreover, when loans start to go bad because the economy is in a recession, the rate of default accelerates. I expect this to happen in 2024.

Recall that ALLY was formerly GMAC (the auto finance arm of General Motors). While Obama bailed out GM, GMAC went into Government receivership. It was eventually "sterilized" with Fed and taxpayer funds and IPO'd as ALLY in 2014. Given the subprime credit quality of over one-third of its auto loans, I think it's a good bet that ALLY goes "chapter 22" sometime in the next 2 years, barring a Fed and taxpayer-funded bailout.

The stock has run from $22.50 to $34.92 in two months. ALLY in that respect could be considered a meme stock. From the viewpoint of economics, given the latest data on auto loan delinquency rates at several different banks and finance companies that do auto loans, there's no fundamental reason whatsoever for that big move in ALLY's stock price. ALLY's profitability is declining and the riskiness of its balance sheet is rising.

For this play, I think it makes sense to go out at least six months and use OTM puts. I like the June $30 puts and may start a position this week unless it looks like the standard beginning of a new year rally unfolds. Another interesting high ROR/high-risk play that won't require much capital is the January 2025 $20 puts. Those traded last at 79 cents on Friday. These puts were trading at $2.80 at the beginning of November.

The same analysis holds true for Synchrony Financial (SYF) and Discover Financial Services (DFS). These two companies have a huge percentage of their assets in credit card loans. At least auto loans are secured by the automobiles. Credit card debt is unsecured. The same ridiculous market impulse that caused ALLY's chart to like it does has caused the same with SYF and DFS.

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.