BrightView Holdings: Business Realignment Can Unlock Value

Summary

- BrightView Holdings is realigning its business strategy by integrating tree and golf services into core maintenance branches and divesting non-core U.S. Lawns franchisee.

- Expect its operating margin to improve in the medium term and also a cash flow improvement in FY2024.

- BV's stock appears undervalued compared to its peers, and investors can expect steady returns in the near-to-medium term.

welcomia/iStock via Getty Images

BV Has Upside Despite The Challenges

I have previously discussed BrightView Holdings (NYSE:BV), and you can read the latest article here. As discussed in my previous iteration, the company will continue looking for profitability improvement. However, it will look to refine its approach at the start of Q2. It realigned the business by integrating the tree and golf services into core maintenance branches while divesting the non-core U.S. Lawns franchisee. The sale proceeds will be used to upgrade the lawnmowers, thus improving the operating margin. Also, it will lean away from the residential market to focus on the commercial market.

The decline in new residential construction over the past two years has held back BV’s growth prospect. A change in business strategy may take time to yield results, but I think its operating margin will improve in the medium term. Cash flow improvement in Q1 is another positive indicator of the company’s health. The stock appears undervalued versus its peers. Investors can expect steady returns in the near-to-medium term; therefore, I retain my "buy" call on the stock.

The Strategy Refinement

BrightView adopted two key strategies in Q1 to secure profitable growth and reduce costs. One related to the realignment of organization. This included understanding its customers and their needs to refine the approach. As part of this strategy, it reintegrated the tree and golf services into core maintenance branches. The company aims to grow business with existing customers and enlarge its customer base by implementing the go-to-market strategy.

The other part of the strategy involved divesting the non-core U.S. Lawns franchise business. During Q1, it sold the business for $52 million. It plans to focus on core business and reinvest the proceeds to drive profitable growth by replacing the aging fleet and buying new lawnmowers. With the proceeds from the sale, it can replace the aging fleet and make significant investments where the management decides it can grow profitably.

The Medium To Long-Term Outlook

At the core of BV’s business strategy is to hold onto its customer base. The sale of the lawn franchisee business serves its purposes because the sold business’s end market is a residential business where it is no longer concentrating. It has shifted its focus to the commercial business.

Based on the future drivers, BV re-affirmed its FY2024 outlook. It expects FY2024 revenues to increase by 5% from FY2023 to a range of $2.825 billion to $2.975 billion. Considering the health of the end market and recent trends, BV will continue to seek profitable growth. In January, snowfall picked up. This, and the conversion of the strong backlog of projects, should benefit the topline. Revenues in the snow business can remain flat in FY2024, while revenues from its landscape business can change marginally. Following the cost-management measures, its EBITDA margin can expand by 40 to 80 basis points.

Economic Indicators

FRED data

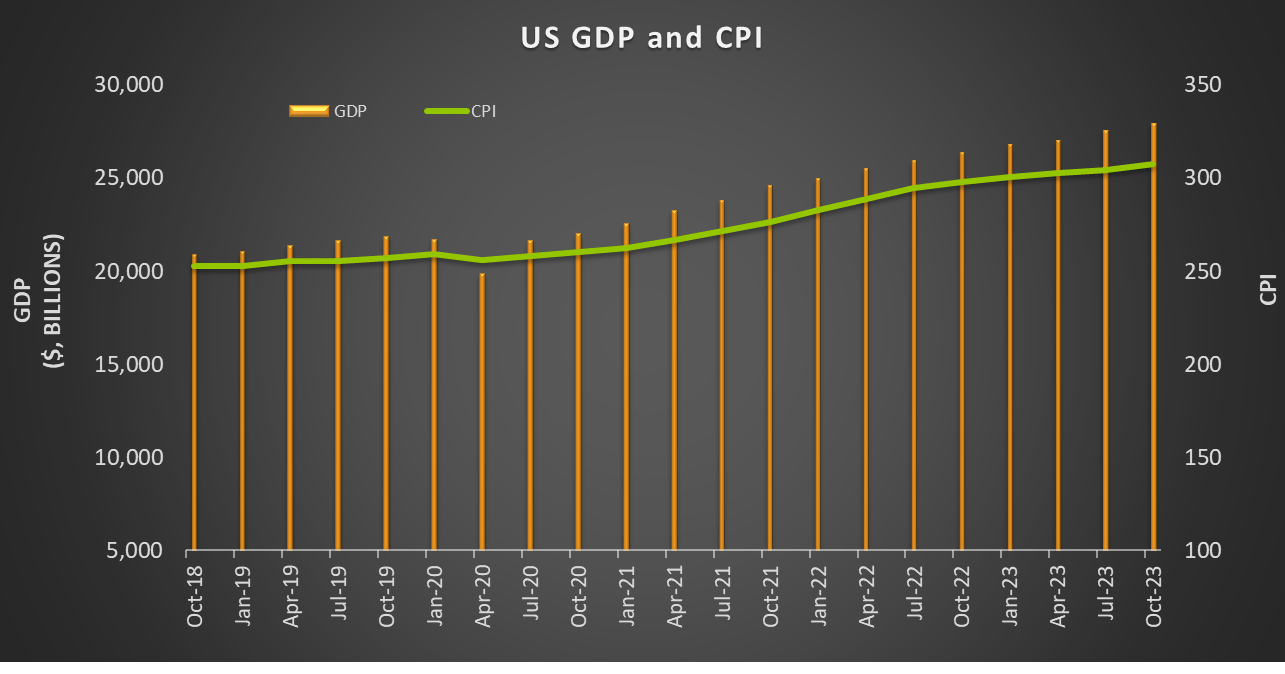

Quarter-over-quarter, the US GDP and the US consumer price index (or, CPI) increased almost equally from Q2 to Q3. Over a longer period (two years), the US GDP growth rate has outpaced CPI. So, the economy does not throw any warning signs for BV's near-term outlook.

End Markets And BV's Strategy

FRED data

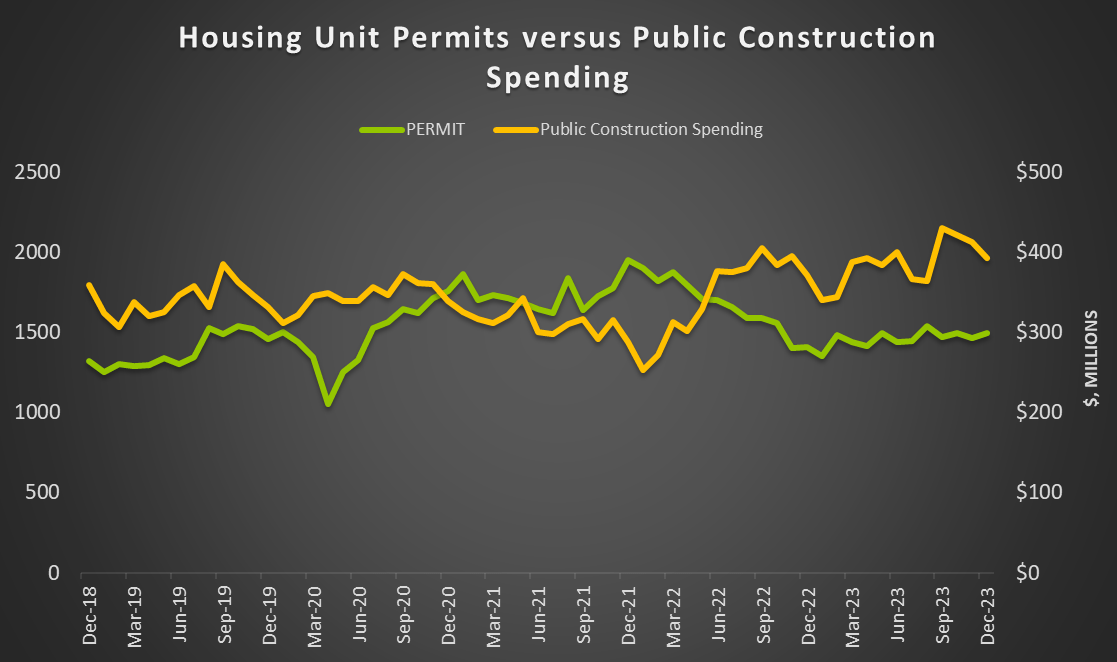

BV lost some interest in the residential market and instead started looking at the commercial business (commercial landscaping) because of the lackluster residential market. Over the past two years until December 2023, the permits for new privately owned housing units declined by 23%. However, after a lull, the market appears to be stabilizing as it moved up marginally in Q4 (Sep-Dec). Nonetheless, the uncertainty over the US economy and a possible recession can make the market nonchalant in 2024.

Over the past two years, public construction spending increased by 36% until December 2023, according to FRED data. Although it declined in Q4, it has far outpaced the dwindling residential market. This validates the company’s approach to concentrate on this market and stay away from the residential market for now.

Analyzing The Q1 Performance

BV's Filings

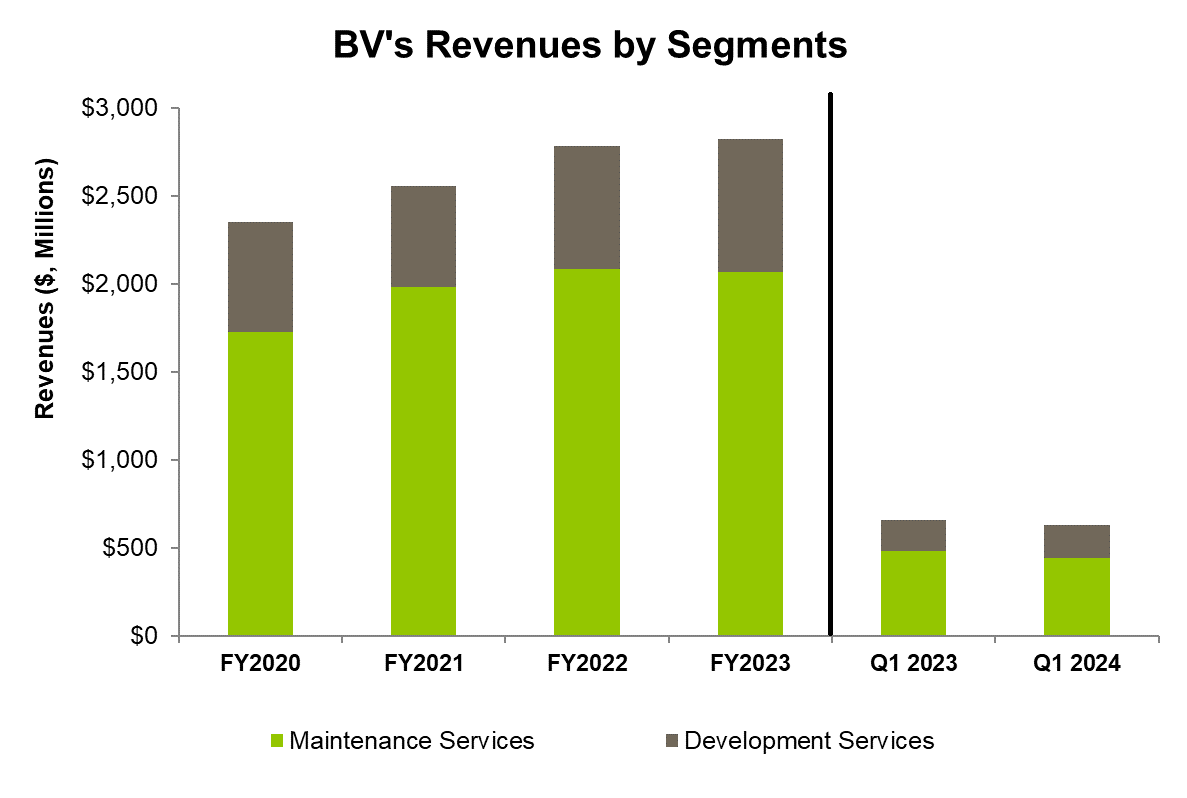

Year-over-year, BV’s revenues decreased by 4.5% in Q1 2024 following a revenue fall in the Maintenance Services segment. Lower snowfall and a decline in the ancillary services caused Q1 revenues to fall by 8.5%. Adjusted EBITDA decreased severely (17% down) due to decreased net service revenues.

On the other hand, an increase in Development Services project volumes resulted in a 6.3% revenue gain in Q1 in the Development Services segment. However, savings from cost management initiatives boosted this segment's EBITDA margin.

Cash Flows And Balance Sheet

In Q1 2024, BV’s cash flow from operations turned positive compared to negative cash flows a year ago. Although the company's revenues decreased, lower accounts receivable and unbilled and deferred revenue led to a rise in cash flow. Free cash flows also turned positive in Q12024 from a year ago. I expect the company to continue generating positive free cash flow as it grows profitably and invests in its core business. In FY2024, the company expects to generate FCF of $45 million to $75 million,

BV's liquidity was $367 million as of December 31, 2023. Its leverage (debt-to-equity) of 0.73x deteriorated (i.e., increased) from a year ago and is lower than its peers' average (SP, HCCI, and CENT). However, its net debt-to-EBITDA improved following the strategic investment from One Rock Capital in Q4. The sale of non-core businesses can further enhance its deleveraging process.

Analyst Rating

Seeking Alpha

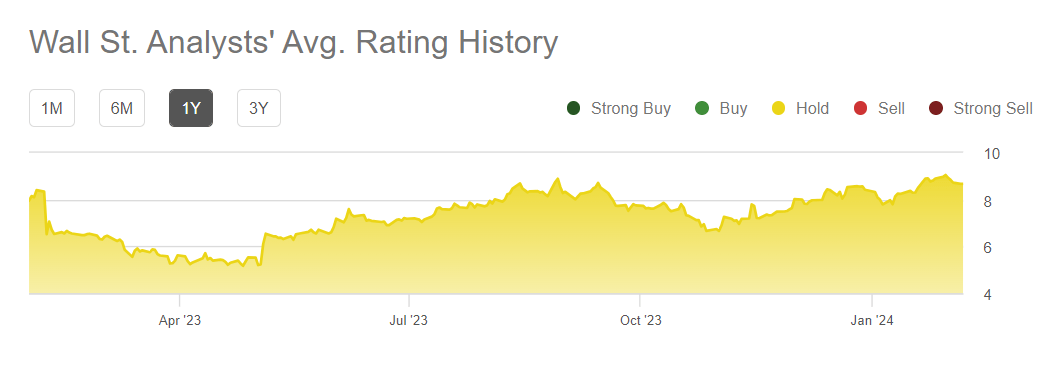

Four analysts rated it a "hold” in the past 90 days, while only one sell-side analyst rated BV a "buy." One of the analysts rated it a "sell." The consensus target price is $9.1, suggesting a 4% upside at the current price.

I think Wall Street analysts are conservative in their expectations and returns from the stock should be higher in the medium term.

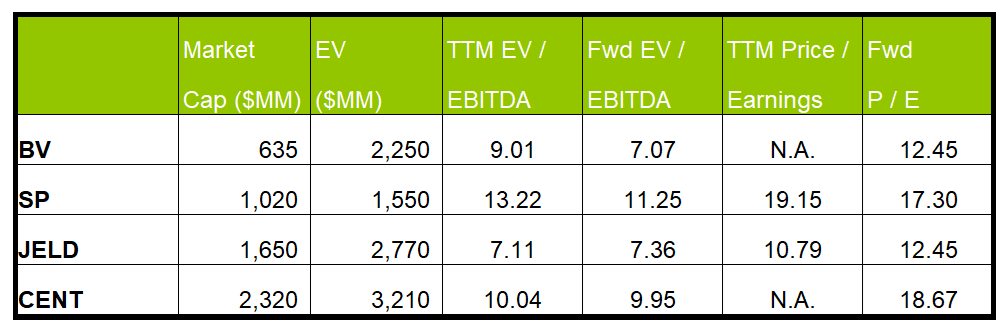

Relative Valuation

Author Created And Seeking Alpha

BV's forward EV/EBITDA multiple contraction is steeper than its peers, which typically results in a higher EV/EBITDA multiple. This means its adjusted EBITDA is expected to rise more sharply than its peers. However, the company's EV/EBITDA multiple (9x) is lower than its peers' (SP, HCCI, and CENT) average (10.1x). So, the stock appears to be undervalued at this level.

If the stock trades at the past average, it can increase by 36% from the current level. If the stock trades at the industry average, it can rally by 33%. Given the near-term drivers, I think the stock may increase less now, but it should back up to yield those returns in the medium term.

Why Do I Retain My Rating On BV?

In my previous discussion on BV, I discussed the company was focusing on improving cash flows and profitability. It pursued high-valued contracts, leading to margin expansion but a lower revenue. Plus, it had a robust balance sheet. I wrote:

BV is currently pursuing a two-pronged strategy: grabbing higher-quality contracts and initiating cost reduction methods like enhancing branch performance, better procurement strategy, and capital allocation. These efforts created higher returns and shareholder value for the investors. I expect its cash flows to remain strong in FY2024 based on improved profitability.

After Q1, BV realigned the organization while it implemented the go-to-market strategy. It also sold a non-core business as opportunities dried up in the residential market. While the topline growth will be limited, the company will focus strongly on profitability. Cash flows and liquidity lay out a solid foundation. Given the undervalued trading multiples, I retain my “buy” rating.

What's The Take On BV?

Seeking Alpha

BV has modified its earlier strategy of procuring higher-quality contracts by realigning the organization and divesting the non-core U.S. Lawns franchise business. Plus, it allowed for significant investments in businesses where it can grow profitably. By shifting its focus away from residential construction to commercial business, it aims to regain the lost ground and improve profitability.

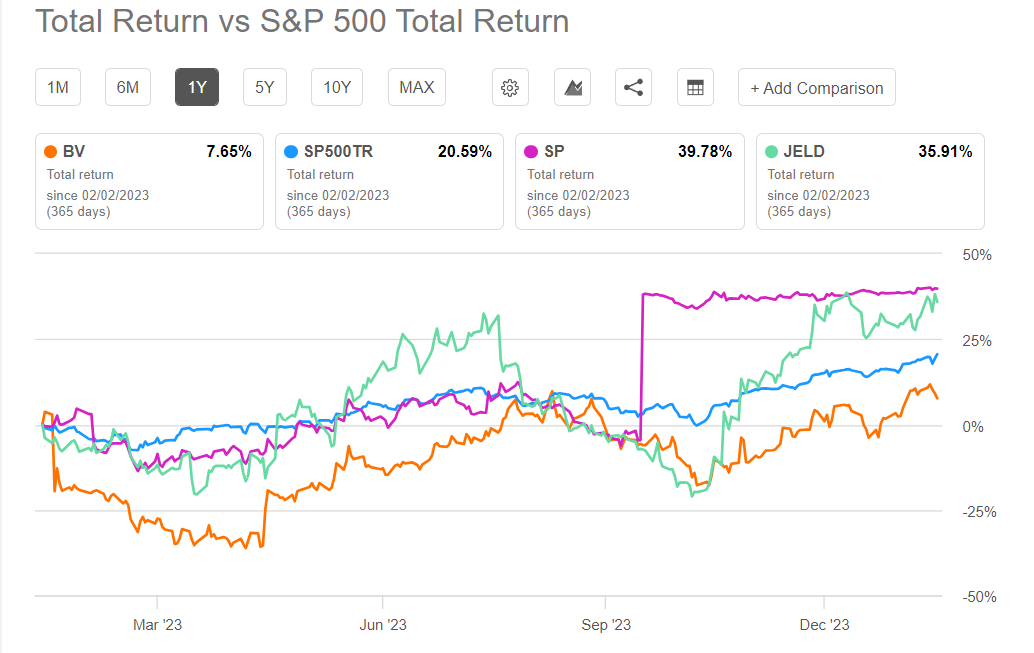

However, the lack of momentum in the residential business and uncertainty over economic growth have put BV in a spot of bother over its short-term outlook. So, the stock underperformed the SPDR S&P 500 Trust ETF (SPY) in the past year. On the upside, cash flows improved substantially in Q1, creating space for deleveraging or M&A activities for rapid growth. The fundamental drivers and the relative undervaluation would prompt investors to “buy” it for medium-term solid returns.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.