Ranger Energy Services Steadies On Focused Growth Strategy

Summary

- Ranger Energy Services has limited room for growth due to weak natural gas prices and lower utilization leading to higher labor costs.

- The company has found some solutions to its challenges, including selective bidding and focusing on production-oriented wireline jobs.

- Despite the challenges, RNGR has achieved strong cash flows and has sufficient liquidity, making the stock appear undervalued compared to its peers.

Евгений Харитонов/iStock via Getty Images

Ranger Has Limited Room For Growth

My last article on Ranger Energy Services (NYSE:RNGR) discussed why the company relocated its assets and crews to the Permian from Haynesville due to weak natural gas prices. In late 2023, the natural pricing softness continued to haunt it. It caused lower utilization, leading to higher labor costs. But the company has also found a few suitable answers to its challenges. Selective bidding and focusing on production-oriented wireline jobs improved its prospects. It also expanded the wireline business and relied on the resilient high-specification rig business to generate steady cash flows.

In 9M 2023, its cash flows increased remarkably, allowing it to achieve the shareholder returns target through dividends and share buybacks. It also has sufficient liquidity. The stock appears undervalued compared to its peers. I expect the stock price to move sideways in the near-to-medium term and would ask investors to "hold" the stock.

The Market And Strategy

Seeking Alpha

In the recent past, before Q3, RNGR, like many other oilfield services companies, took a hit from lower drilling activities. During the first nine months of 2023, the US rig count dipped by 19%. However, completion activity remained resilient during this period, as indicated by the relatively fewer changes in frac spread count (2% rise). So, RNGR adjusted to the shift by redeploying idle assets. However, investors may also note that such redeployment affected its utilization adversely in some cases. Plus, it has a significant exposure to gassier basins in some regions.

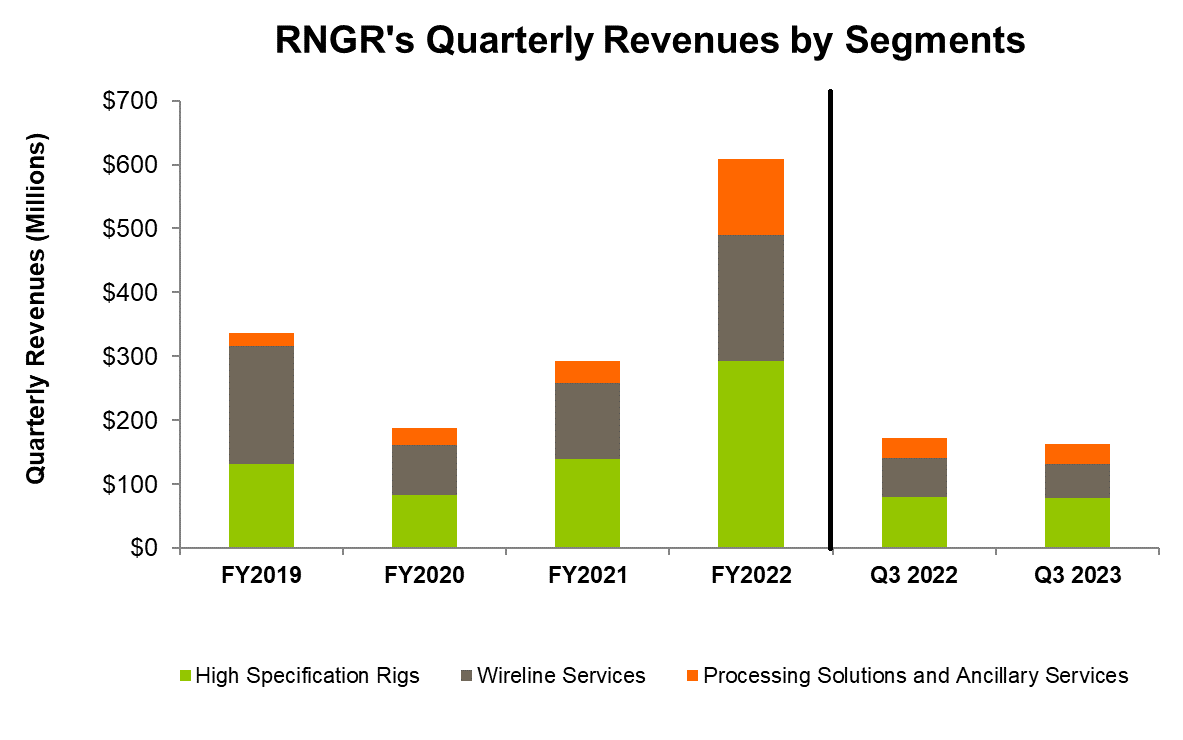

Much of RNGR's assets are allocated to production-focused work, which allows it to keep the baseline activity relatively unaffected. This, despite the fall in onshore activity in the US, is noteworthy. In Q3, it signed an agreement with a major integrated US onshore operator, which can increase its market share in this region. The company looks to position itself to cater to larger customers while consolidating vendors to gain momentum in 2024. So, the fact that its revenues from the High Specification Rigs segment remained unchanged from Q2 to Q3 showed the robustness of its production-focused business model.

Understanding The Outlook

RNGR's Q3 2023 Earnings Presentation

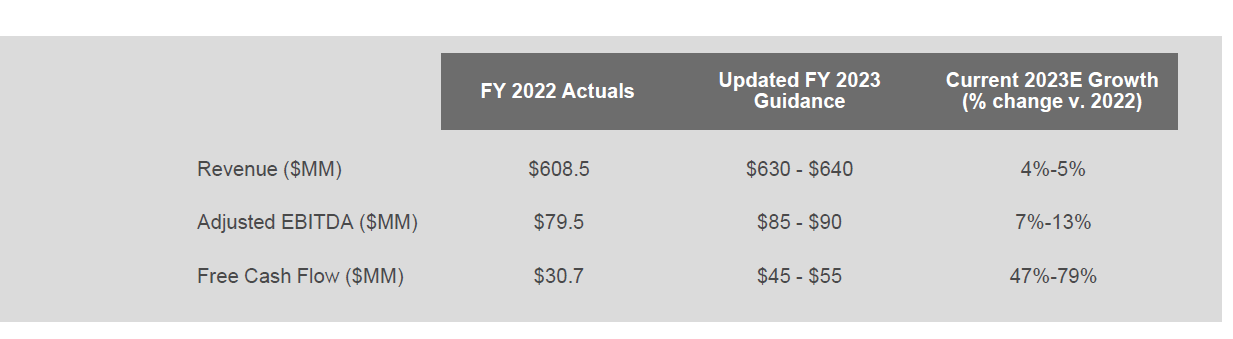

RNGR expects increased activity levels in 2024 because its management believes the rig count will bounce back in 2024. Although energy operators will be cautious about capex, the consolidation in the industry through M&As will create a tight demand-supply situation. It also thinks that the energy companies providing more efficient solutions will gain market share.

In Q4, some of the challenges, including the trough in the US onshore activity and the typical seasonality, can cause RNGR's financial results to deteriorate. The company deployed new assets in October, which, in my opinion, can moderate the impact of the seasonality. The recent acquisition can push its growth rate. During Q3, it purchased pump-down assets for its Wireline business. The pump-down assets can be easily integrated through its existing service lines.

Analyzing Q3 2023 Results

RNGR's Filings

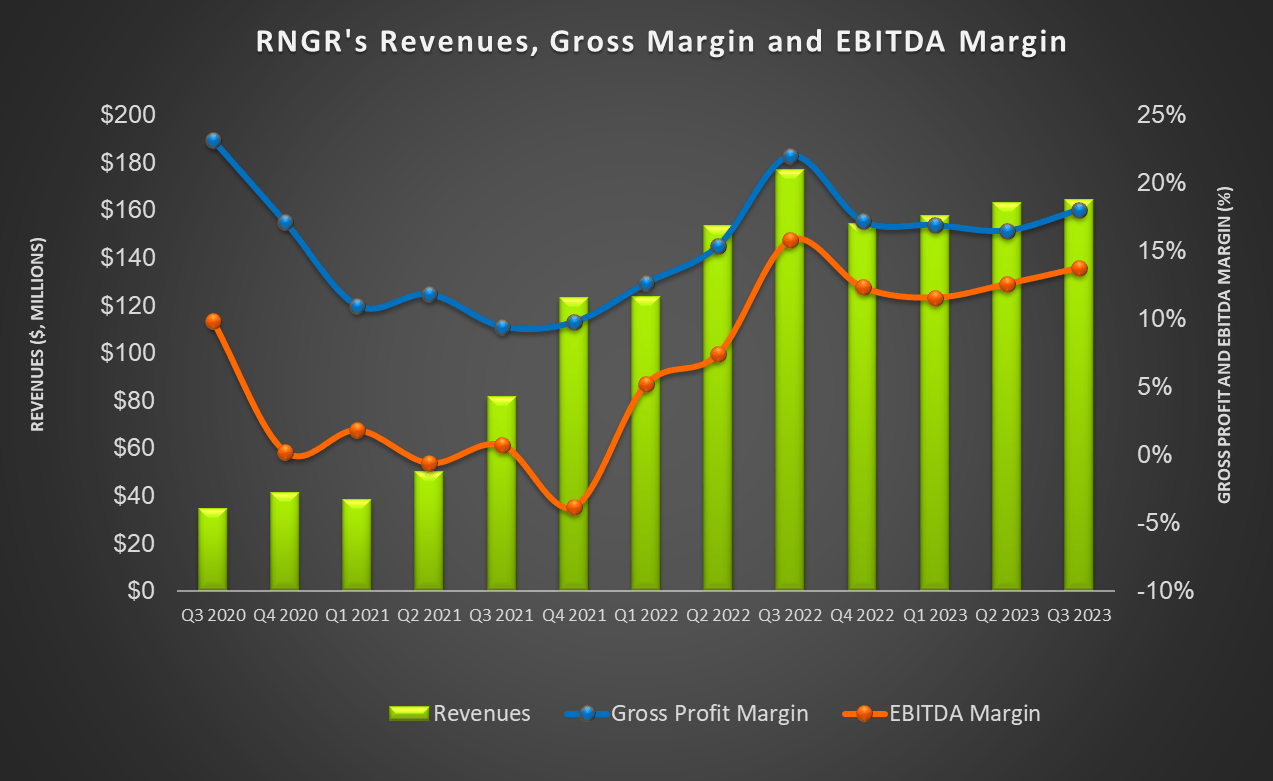

In Q3 2023, revenues in the High Specification Rigs segment decreased by 1% compared to a year ago. Adjusted EBITDA in this segment decreased by 8% during this period. Lower utilization due to several rig changeouts caused labor costs to rise. Pricing, on the other hand, improved and partially offset the effects.

The Wireline Services segment saw a 12% year-over-year revenue fall in Q3, while its adjusted EBITDA declined by 35%. Its pricing declined both in the Coil business and Rentals business in Q3. Much of the changes were in the South where pricing and competition affected its margin. In the North, however, the company's pricing improved. The company aims to improve margins through selective bidding and focusing on production-oriented wireline jobs.

Revenues in the Processing Solutions and Ancillary Services segment witnessed a 3% fall year-over-year in Q3 2023. The adjusted EBITDA decreased by 38%. Activity decline squeezed its Coil and Rentals businesses, causing revenue and EBITDA to decline in this segment.

Other Risk Factors

In addition to seasonality and customer budget exhaustion that can lower RNGR's topline and EBITDA in Q4, I see external risks. These are concerning the energy price volatility and geopolitical risks. OPEC's decision to control production continues to affect the price of energy. The natural gas price, in particular, has remained depressed. The 2022 invasion of Ukraine by Russia has injected uncertainty into the global economy. As a result, the energy companies - operators and oilfield services companies like RNGR, for example - can see their results affected by global factors.

Cash Flows And Repurchases

RNGR's debt-to-equity was 0.04x as of September 30, 2023 - an improvement over 0.07x since the start of 2023. Its net debt was insignificant on September 30. Its liquidity was $70 million as of that date. During Q3, it repurchased 781,000 shares for ~$0.6 million, which leaves it with nearly $26 million of authorization. It has already exceeded its commitment of 25% annual shareholder return as set earlier.

In 9M 2023, the company's cash flow from operations (or CFO) increased by 1.9x compared to a year ago. It initiated a quarterly dividend of $0.05 per share in August 2023. Its free cash flow (or FCF) also increased tremendously in the past year, allowing for the share repurchase and dividend programs to continue.

Analyst Rating

Seeking Alpha

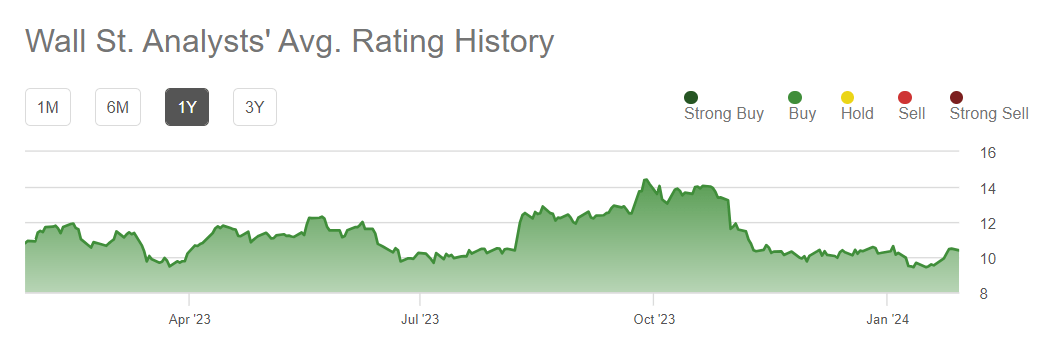

One sell-side analyst rated RNGR a "buy" ("strong buy"), while three recommended a "Hold." None recommended a "Sell." The stock's return potential using the sell-side analysts' expected returns is 32% at the current price.

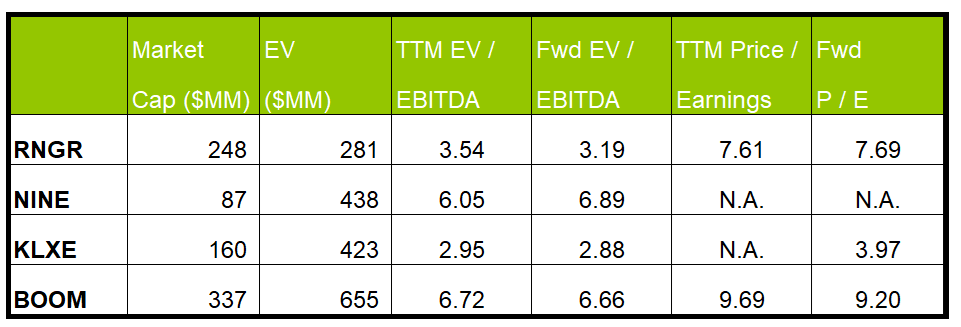

Relative Valuation

Author Created and Seeking Alpha

RNGR's forward EV/EBITDA multiple is expected to contract versus the current EV/EBITDA. Also, the fall will be steeper than its peers, typically resulting in a higher EV/EBITDA multiple. The company's EV/EBITDA multiple (3.5x) is lower than its peers' (NINE, KLXE, and BOOM) average. So, the stock is undervalued versus its peers.

If it trades at the past average (42x), it can climb steeply from the current level. If it trades at the industry average, it can step up by 43%. However, I do not think the stock relive the past high because the industry dynamics have changed. In my opinion, given the drivers, the trading multiple can expand to reflect the industry average, and it can yield a 35%-45% return.

Why Do I Keep My Rating Unchanged?

My earlier articles on RNGR discussed how the company strategically adjusted its geographic asset positioning after expanding the existing wireline business into production-related services through acquisitions. Its market was not conducive because many of its peers revised their prices downwards. Its balance sheet and cash flows were steady, though, by Q1. In my last iteration, I wrote:

RNGR changed its regional asset portfolio mix as the energy price balance shifted following the natural gas prices decline. Crude oil's relative resilience helped keep utilization steady in Q1. The management appears to be confident about the growth prospect in 2H 2023. However, some of the company's segments may see muted growth.

In Q3 2023, lower drilling activity and the weaknesses of natural gas prices accelerated the company's focus on production-focused work. Its High Specification Rigs segment performed relatively well after the change in its strategic stance. The asset redeployment can moderate the adverse impacts that the company will likely face through the typical Q4 seasonality. Although the balance sheet and cash flows strengthened, a lack of robust drivers suggests I maintain my "hold" call.

What's The Take On RNGR?

Seeking Alpha

The activity declines on the completion side from 2022 through 1H 2023 trimmed some of RNGR's growth plans. Also, the company's exposure to gassier basins shrunk its revenues and margin as natural gas prices stayed under pressure. The company responded to the challenges by redeploying assets and pursuing operating efficiencies. It also shifts its focus to large customers to gain market share. Vendor consolidation can also help plug the hole in the operating margin fall.

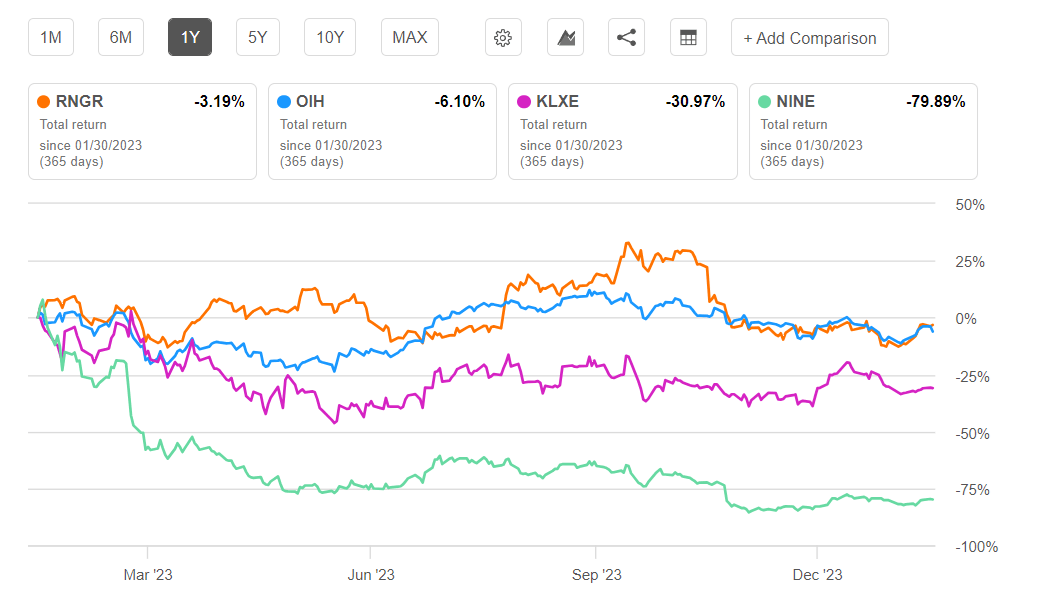

During Q3, it purchased pump-down assets for its Wireline business. Its outlook can improve through selective bidding and focusing on production-oriented wireline jobs. So, the stock marginally outperformed the VanEck Vectors Oil Services ETF (OIH) in the past year. It has achieved the commitment to return 25% of its annual cash flows through share repurchases and dividends. However, the near-term growth challenges prompted me to stick to my "hold" call.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.