Bristow Group: Contract Wins, Undervaluation Make It A Buy (Rating Upgrade)

Summary

- VTOL plans to add to its fleet size in 2024 and has secured long-term contracts with the U.K. and Irish coast guards.

- The company has growth opportunities in Brazil, West Africa, and the Gulf of Mexico, but faces challenges with supply chain continuity.

- Despite facing headwinds, VTOL's management expects revenue and adjusted EBITDA growth in FY2023 and FY2024, and the stock is relatively undervalued.

nielubieklonu

VTOL Rides The Industry Tailwind

I previously discussed Bristow Group (NYSE:VTOL), and you can read my latest article here. In that piece, I found that its asset utilization improved in many geographies as demand improved and supply plateaued. In the current iteration, I find VTOL plans to add to its fleet size in 2024 following the revival of international offshore project FIDs. It also struck long-term contracts with the U.K. and Irish coast guards for search and rescue operations. The change in order value and durations will help it improve its average pricing and cash flow generation.

However, heavy equipment can also run into difficulty with supply chain continuity, as happened in the recent past. The company's leverage has deteriorated since my last coverage, while its free cash flows have remained negative. The stock is relatively undervalued. Because the positive industry factors are already in play, I see the stock recovering and consider it a "buy" for the medium term.

The Push Has Come To Customer Growth

VTOL's Q3 2023 Earnings Presentation

Bristow has growth opportunities in Brazil, where the energy market is expanding, and the company has won a couple of contracts in the past two quarters. West Africa is another growth region, particularly Nigeria, where the company has a positive outlook. In the Gulf of Mexico, a large market, the company witnessed a recovery following various offshore FIDs. Here, the company started a few new contracts recently, including one relating to AW139 (medium helicopter) and the other being an S92 (heavy helicopter).

VTOL's Q3 2023 Earnings Presentation

It also sees demand surpassing the supply of S92 in this region and the possibility of further contracts. However, investors should note that the demand in the GoM is not as sharp as in the other high-growing regions, and the rates are also relatively low in this region. It plans to add 11 new helicopters to its fleet in 2024. Its search and rescue contracts are typically ten years long. So, in the near term, I do not expect the company's performance to improve vastly, but it is beginning to reach a point of inflection.

The company's contract pricing varies widely for various durations. Bristow estimated that the rates are the highest for the five-year contracts. Its contracts typically have an average maturity of two and a half years. Currently, it can renew the contracts at much higher prices from higher flight hours from short-term exploration campaigns. The renewed rates see approximately a mid-20% hike, depending on the geography or aircraft type. The company will see the full impact of the price raises in 2024.

Challenges And Solutions

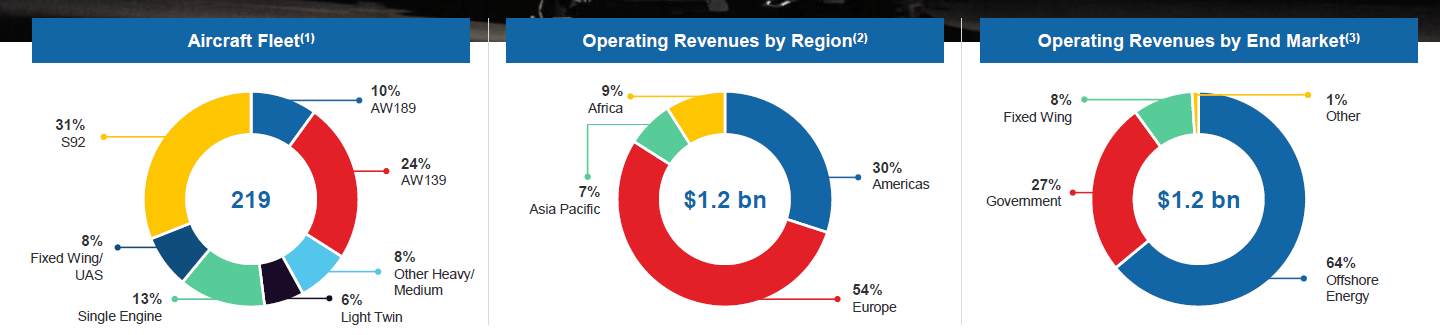

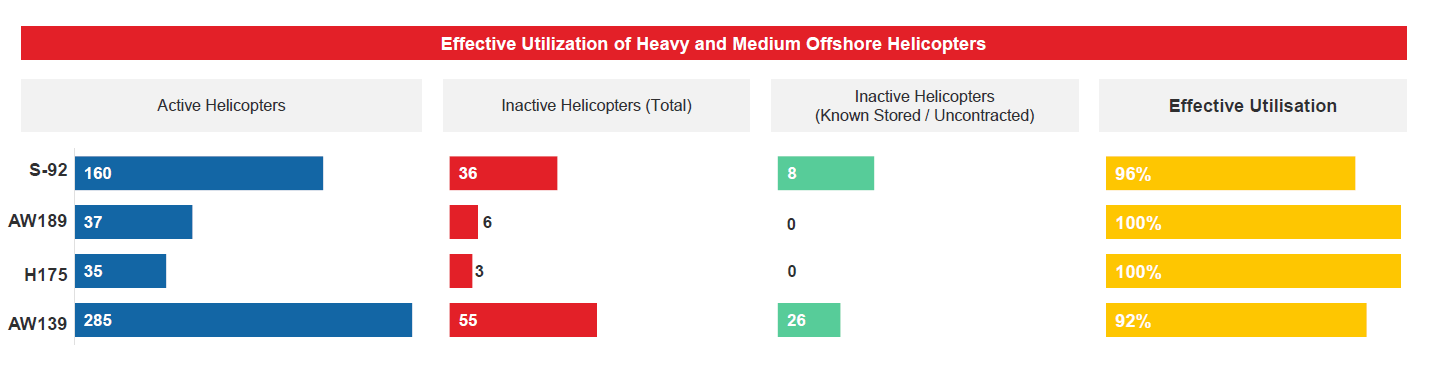

VTOL has a large fleet of S92 helicopters, which account for 67% of its heavy helicopter portfolio and 22% of its total fleet size. Keeping that heavy machinery means maintaining a strong supply chain. However, during 2022 and in 1H 2023, it saw the adverse impact of the recent supply chain delays on its maintenance and costs.

It now explores the secondary market for purchasing components and fulfilling its inventory. It also seeks extensions on life and components to keep the helicopters in service. This multifaceted approach will likely keep the contracted aircraft working for its customers.

Q4 2023 Outlook

VTOL's Q3 2023 Earnings Presentation

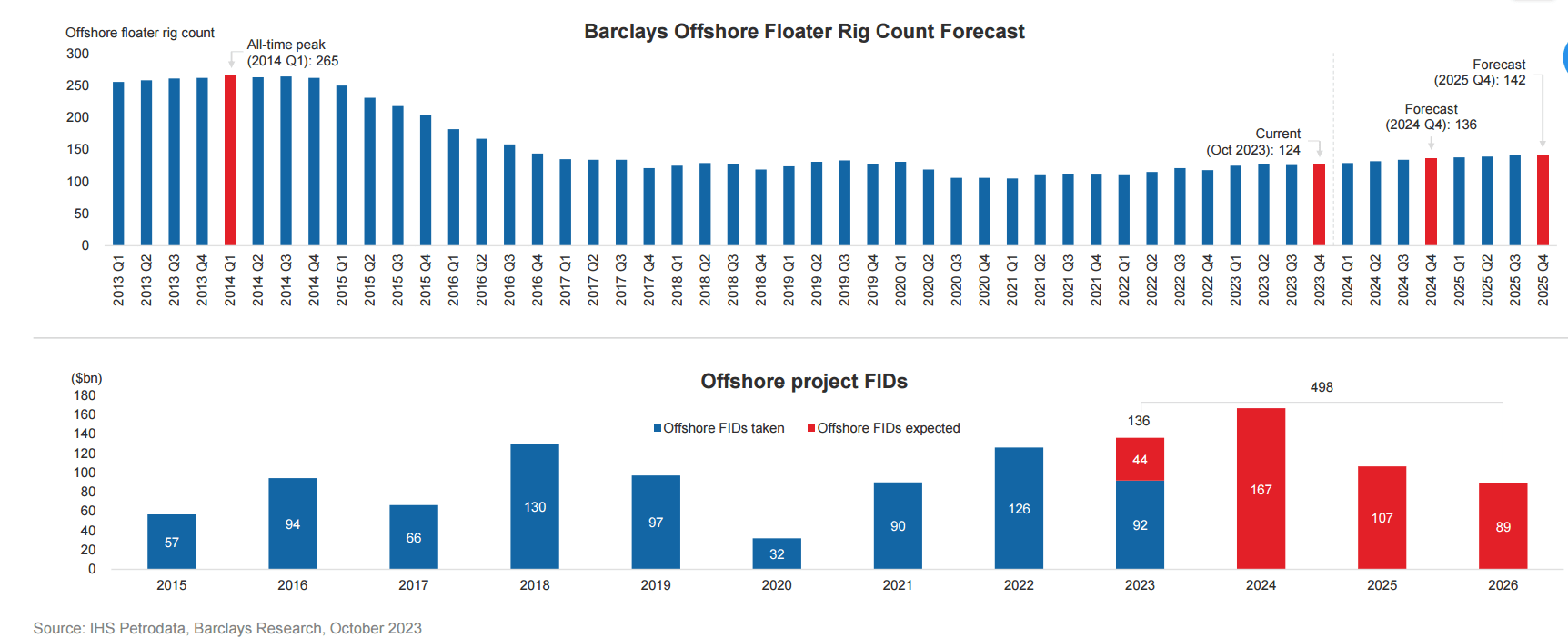

In Q4 2023, I expect VTOL's revenues to increase based on the momentum in project FIDs (final investment decision). According to the estimates shown in the company's Q3 earnings presentation, 44 FID projects were due to be added in the final leg of 2023, on top of 92 FIDs already initiated during the year. Another 167 are to be added in 2024. This augurs well for VTOL's near-term revenues.

However, I do not think its operating margin will gain ground because of the continued pressure from the supply chain. However, my take on VTOL is not limited to its next-quarter performance but considers the medium-term growth drivers stacked in favor of the company. This prompted me to change my call on the stock.

FY2023 Outlook Explained

VTOL's Q3 2023 Earnings Presentation

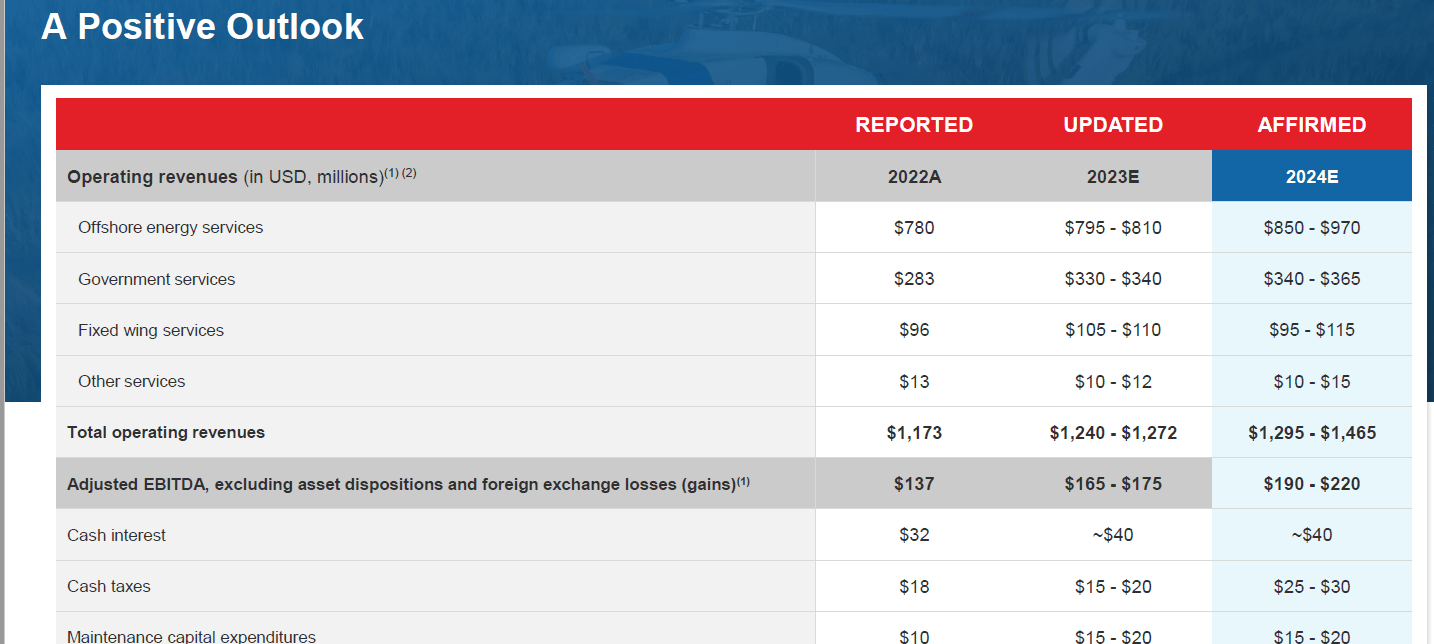

In FY2023, VTOL's management expects revenues to grow by 7% (at the guidance mid-point), while the adjusted EBITDA growth would be 24% compared to FY2022. However, in Q4, its adjusted EBITDA can decline versus Q3 due to seasonality in Canada and Australia. In FY2024, the company's adjusted EBITDA can increase by 20% compared to FY2023's mid-point guidance, due particularly to offshore energy growth. The company's projects, initiated in Brazil, Norway, and the Gulf of Mexico, will increase its EBITDA in 2024.

Despite the positive outlook, the company faces a few headwinds. These include the adverse impact of a strengthening U.S. dollar on its financial results and the supply chain challenges concerning the parts delays for the S92 helicopter. The entire offshore industry faces the impact of these component delivery delays. Nonetheless, the company's management believes that it will recover following the multiyear growth cycle in the offshore energy industry.

Because a significant part of VTOL's business arises in the UK and Norway, the value of the GBP and NOK relative to the U.S. dollar will affect VTOL's financial results. In Q3, the company's net income was boosted by $4.5 million of foreign exchange gains, partially offset by the weakening of the GBP versus the USD.

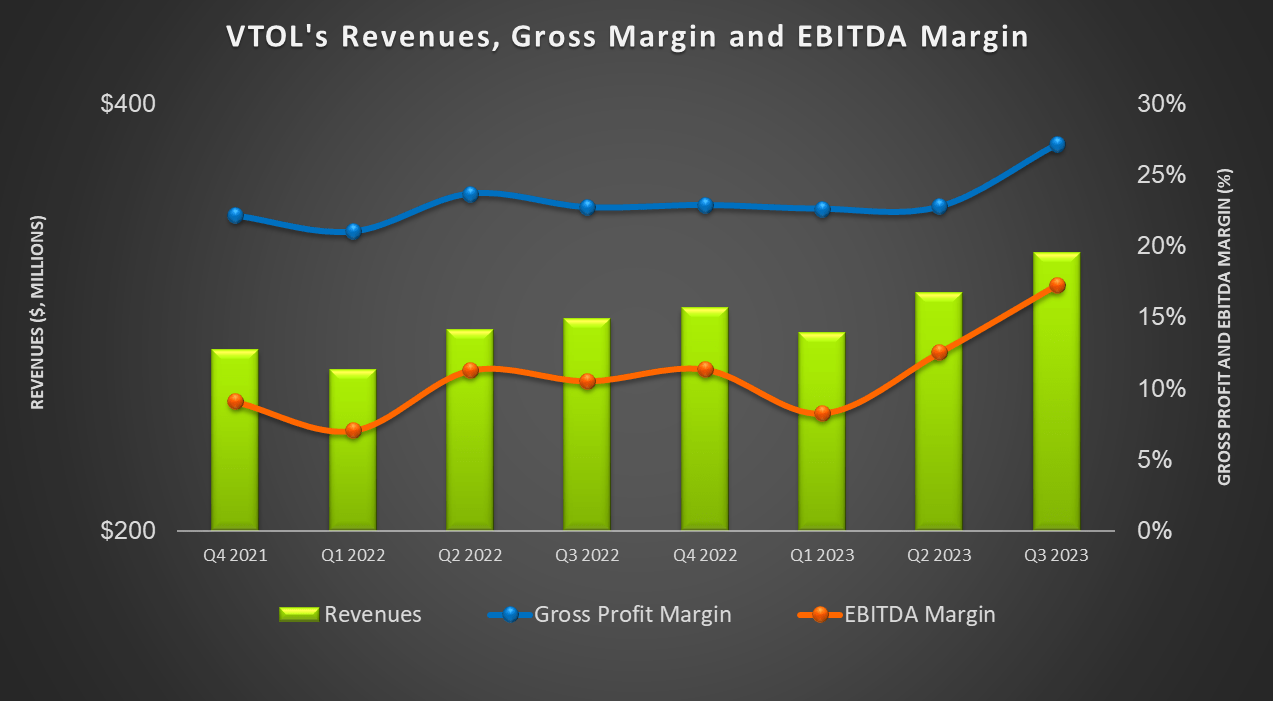

Q3 Performance Analyzed

Seeking Alpha

VTOL's revenues grew by 6% from Q2 to Q3, while its adjusted EBITDA increased by 46%. Its Fixed Wing business appears to have recovered from the pandemic as the ongoing fleet enhancement takes effect. Its Government Services business has benefited from including government search and rescue contracts in various countries.

Investors may note that government contracts are typically long-term contracts providing stable and high-return cash flows. The Offshore Energy business is believed to be in the early stages of a multiyear growth cycle. I expect the company's aircraft utilization and hourly rates will improve in this business, generating significantly higher cash flows.

Cash Flows and Debt

In 9M 2023, VTOL's cash flow from operations increased due, in part, to higher revenues. Capex increased more significantly. As a result, free cash flows (or FCF) remained negative and steeped more into the negative territory compared to a year ago.

VTOL's debt-to-equity (or leverage) also deteriorated to 0.68x compared to 0.65x at the start of the year. As of September 30, its available liquidity was $274 million. With a new £55 million secured equipment financing related to the UK search and rescue contract, its debt level can potentially rise further in 2024.

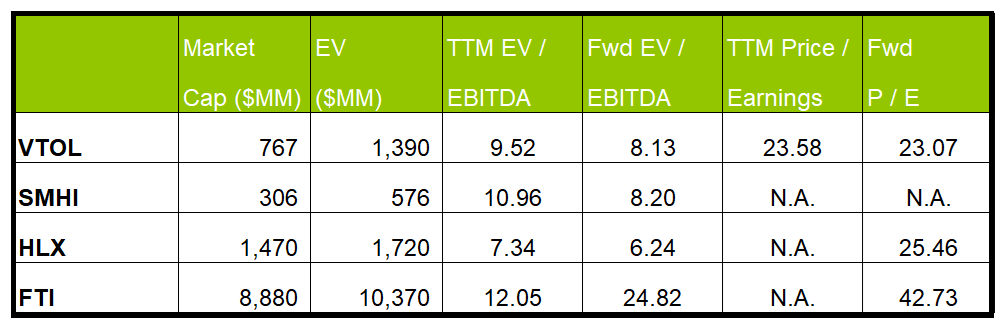

Relative Valuation And Expected Returns

Author Created and Seeking Alpha

VTOL's forward EV/EBITDA multiple versus the current EV/EBITDA multiple is expected to contract more steeply than its peers, which implies that its EBITDA is expected to rise more sharply next year. This typically results in a higher EV/EBITDA multiple. The company's EV/EBITDA multiple (9.5x) falls below its peers' (SMHI, HLX, and FTI) average. The current multiple is in line with its past five-year average. So, the stock appears to be undervalued compared to its peers.

If it trades at the past average in the medium term, it can climb 59% from the current level. If it trades at the industry average, it can zip by 77%. However, given the industry challenges, I think the stock price will increase but may produce less returns than mentioned above.

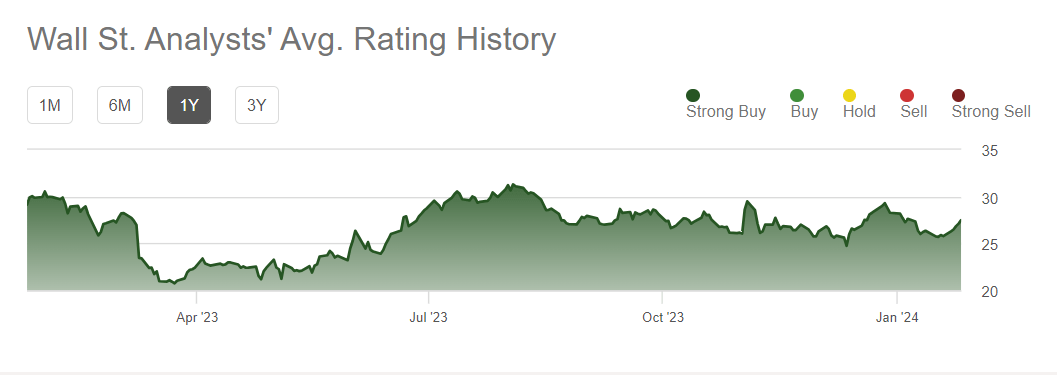

Analyst Rating

Seeking Alpha

Two Wall Street analysts rated VTOL a "buy" (including "Strong Buy"), while none recommended a "hold" or a "sell." The consensus target price is $27.5, which indicates ~44% upside potential at the current price. I think Wall Street analysts are at a reasonable ballpark with their expectations from the stock.

Why Do I Upgrade My Call?

In my previous article, I discussed VTOL had pricing traction because the overall capacity of the offshore helicopter diminished while demand improved. Its asset utilization improved in the US Gulf of Mexico, Brazil, and the North Sea. On the other hand, supply chain issues disruption affected the S-92 helicopter supplies. Free cash flows were negative. I wrote:

The company won new contracts in the US Gulf of Mexico, Brazil, and the North Sea, which would improve asset utilization in 2023. Also, the offshore energy services market is viewed to be at a multiyear growth cycle, which would be hugely beneficial for the operators like VTOL.

After Q3 2023, VTOL started benefiting from a higher demand for offshore helicopter services in Brazil and West Africa. The Gulf of Mexico is still under pressure but appears to be recovering. Its contract renewal rates are improving, too. Much of the gains from the price hikes will be reflected in FY2024. The company's balance sheet and relative valuation appear quite attractive. So, I believe the stock is apt for a "buy."

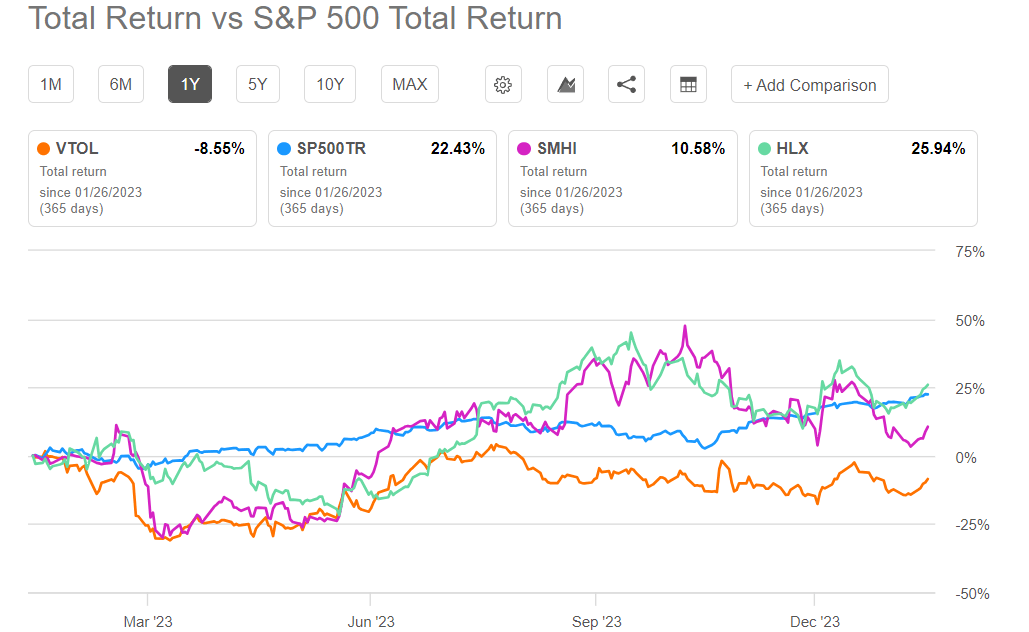

What's The Take on VTOL?

Seeking Alpha

VTOL has recently added $300 million of contract awards with the U.K. and Irish Coast Guard. It also looks to add to its fleet size in 2024, which, along with the long-term duration of the contracts, should augment its medium-term outlook well. The shift in its drivers is the recent FIDs in international offshore, primarily in Brazil and Nigeria. A higher share of heavy helicopters and a longer search and rescue-type project awards duration will improve its average pricing and lend more stability to its cash flow generation.

On the flip side, in the recent past, many transporters in the energy industry faced supply chain issues. Although the company adopted several strategies to address it, its operating profit has recently decreased. The relative strengthening of the USD versus other currencies is another concern. So, the stock underperformed the SPDR S&P 500 ETF (SPY) in the past year. Given the stock price fall in the past month and a relative undervaluation, I suggest a "buy."

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.