Initial Report(part2): Intuitive Surgical Inc.(NASDAQ:ISRG), 51% 5-yr Potential Upside (EIP, Gaius ANG)

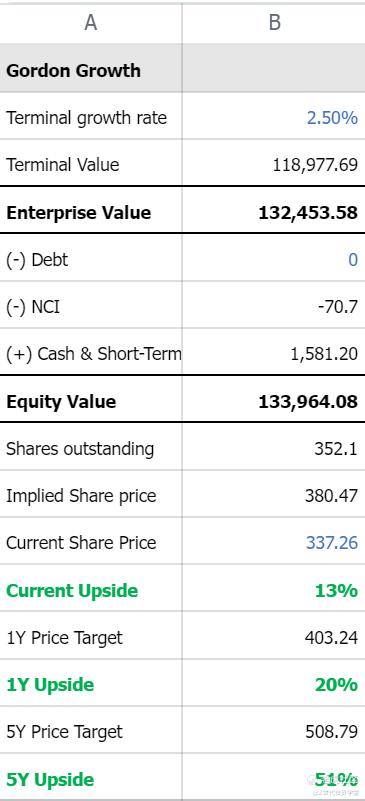

Valuation

I used a DCF valuation to value the company and assumed a revenue growth of 17.2% per year, which was the industry growth projection by Research and Markets. While this number is a rather aggressive choice as an industry growth rate, I used this number as I believed ISRG would benefit disproportionately from industry growth.

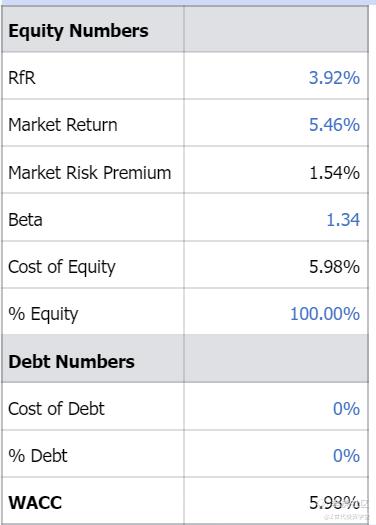

With a closing share price from 29 December 2023, this gives an immediate upside of 13%, a 1Y upside of 20% and a 5Y upside of 51%. A risk-free rate of 3.92% was used, derived from US 10Y Treasury Bond yields at the time of the valuation. For the market return, I used the iShares U.S. Medical Devices ETF 5Y performance as I believed the 10Y performance to be less reflective owing to a very different economic climate.

Risk and Mitigation

Technology Risk

Disruption: ISRG's advantage is contingent on its ability to pursue effective R&D and maintain the relevance of its surgical systems. Innovations in robotic surgery can make its technology obsolete and hurt the company's top-line.

Mitigation: ISRG invests heavily in R&D and has demonstrated the ability to translate that to revenue, reflected in its ROIC of 18.19%, calculated using TTM income statement data.

ESG Risk

Controversy: As a market leader, ISRG could be tempted to use predatory pricing or other anticompetitive behavior to maintain its position. Being in the medical industry, there are also social and ethical concerns regarding the pricing of its products.

Mitigation: This is a risk that is difficult to mitigate and I believe it is important for it to be continuously monitored. I believe ISRG's current performance to be acceptable with room for improvement.

ESG

The company releases an annual ESG report in alignment with leading reporting frameworks such as the Task Force on Climate-Related Disclosures (TCFD) and the Global Reporting Initiative (GRI).

The company has programs in place to ensure its practices are sustainable. Over 99.9% of proprietary waste collected by vendors in North America are recycled and 100% nonpotable water is used for native/adaptive demand for landscape planting. The company has also made over 95% of the surgeon console, 60% of the patient side cart and 20% of the vision side cart components recycleable.

On the social front, ISRG was named a top-scoring company on the Disability Equality Index which measures companies actions to achieve disability inclusion and equity in the workplace. The company has also raised over $20 million to support patient care and vaccinations during the COVID-19 pandemic.

With regards to governance, ISRG's board is diverse, with 27% of the board represented by people of colour and 36% of them being women.

I believe, in general, ISRG has done well on most fronts.

However, in 2021, the ISRG was sued for anticompetitive behavior in the robots aftermarket business and overcharging hospitals for replacement parts. There were also accusations of the company shutting down surgical robots mid-surgery.

My opinion is that some of these allegations may be unfounded since ISRG has stated it does not have the ability to shut down robots remotely and that these issues could have been caused by improper maintenance and use of third party maintenance services.

While pricing for the maintenance and servicing contracts are steep and the contracts could be deemed rather restrictive, the practice of selling a product at lower cost and charging more for O&M or subsequent replacement parts is not a particularly new practice. Printer companies have long been selling printers at a loss and recouping that loss through the sale of ink cartridges, even incorporating microchips into ink cartridges to ensure third-party ink cartridges are not used.

I view ISRG's ESG performance to be acceptable and overall think the company has done a reasonable job navigating the complex and challenging medical services industry.

Closing Remarks

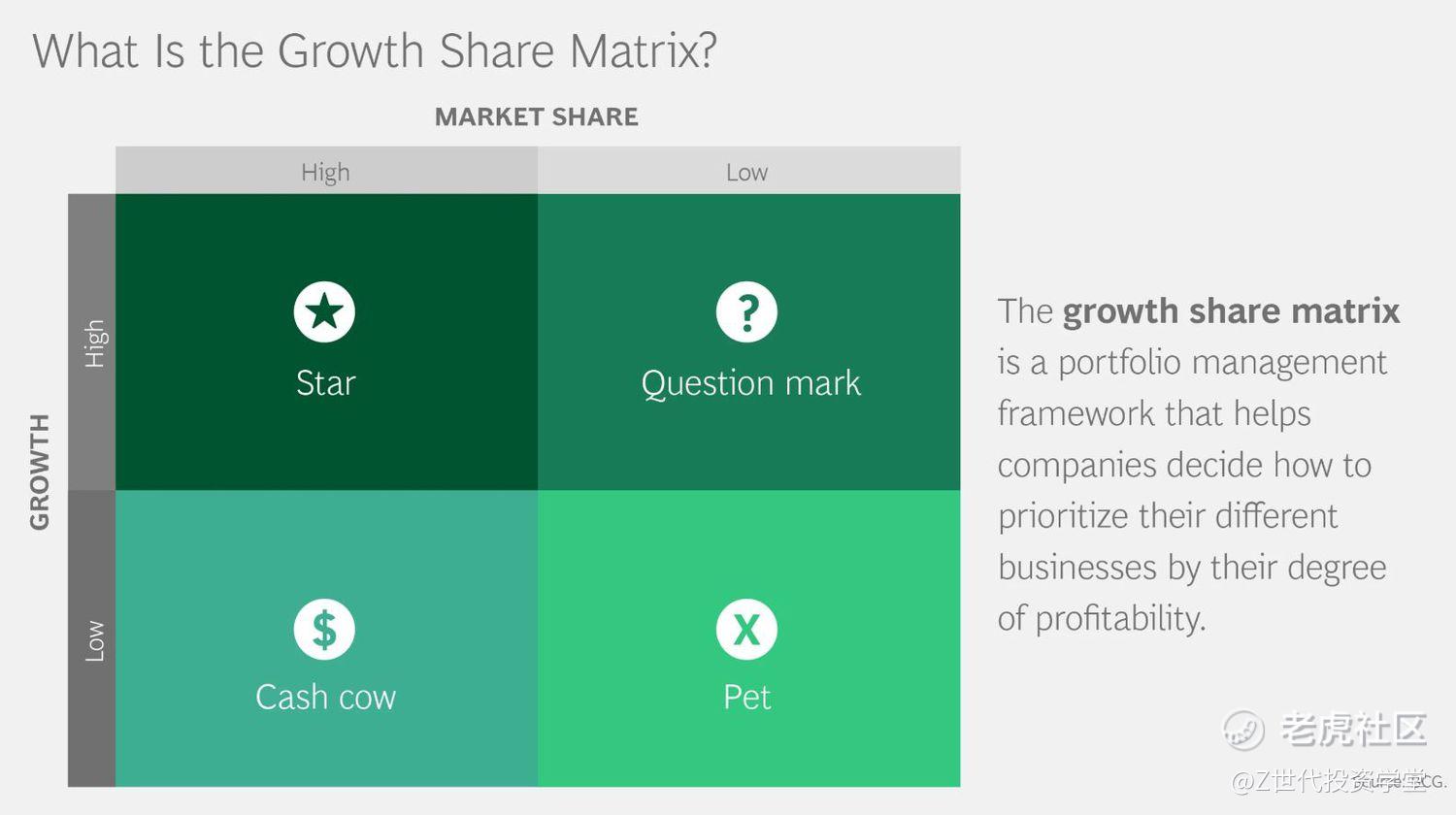

I started looking at this company around the time its Q3 financial results were published. The share price then was around ~US280. While the share price has run up significantly since then and (with hindsight) I wish I executed a position in the company earlier, I still believe the company has room for further upside and will maintain its position as market leader through its superior technology. The robotic surgery industry is a rapidly growing industry and fits into BCG's criteria of a star company, which is personally my favorite type of company to invest in.

Overall, I issue a buy recommendation for this company but would recommend slowing accumulating a position in this company over a longer time horizon while monitoring its position as market leader as well as how it handles controversy regarding its business practices.

*Do note that all of this is for information only and should not be taken as investment advice. If you should choose to invest in any of the stocks, you do so at your own risk.

如果你想了解有哪些前沿科技的投资机会,想学习真投资大佬们的投资秘籍,想投资自己的人生,那就快来购买《大赢家》漫画吧!漫画中采访了许多职业投资人和上市企业,通过有趣的故事传达投资理念,我们相信在阅读的过程,你一定会有所收获。https://product.dangdang.com/29564921.html#ddclick_reco_reco_relate

Modify on 2024-04-02 22:16

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.