Initial Report(part4): Jinko Solar Holding Co.(JKS), 177% 5-yr Potential Upside (EIP,Leon LEONG)

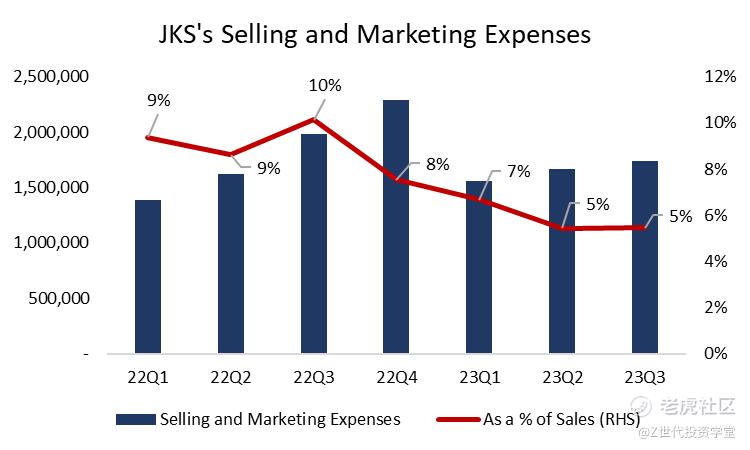

In terms of net profit margins, JKS has done exceptionally well in controlling its operating costs in FY23 and we can see a clear recovery trajectory in net profit margin compared to FY22 (Figure 36). On the other hand, all of its peers have seen net profit margins decline in FY23, signalling poorer control of operating costs, which is worsened by declining solar prices across the entire value chain. While JKS's gross margin expansion has certainly contributed to alleviating its poor profit margins as seen in FY22, another key contributor is its reduction in selling and marketing expenses as a % of sales in the first three quarters of 2023 (Figure 37). This is a key critical point as JKS's module shipments have increased significantly while expenses incurred to market and sell its modules have not increased significantly, implying JKS's stronger presence amongst customers that are looking to purchase solar modules.

With increasing module shipments, JKS appears to have a solid value proposition alongside tight cost control efforts, providing it with a narrow economic moat amongst its peers. JKS's future looks promising even as the solar industry is faced with overcapacity pressures, and I believe it is well positioned in the solar industry to weather through the period of overcapacity and emerge as the leading solar module supplier after the industry consolidates.

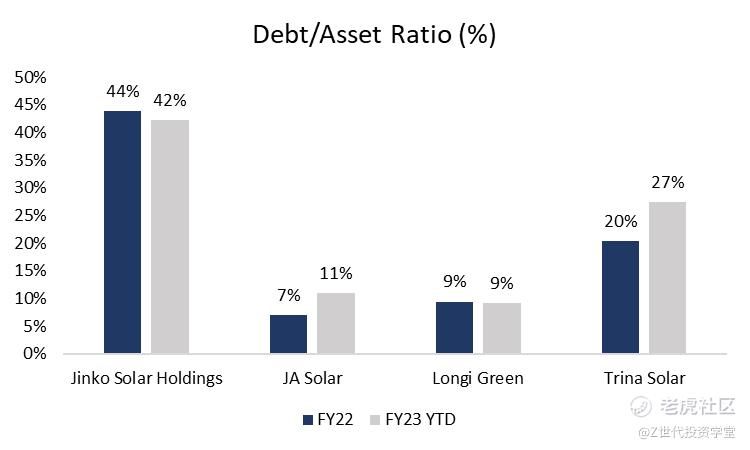

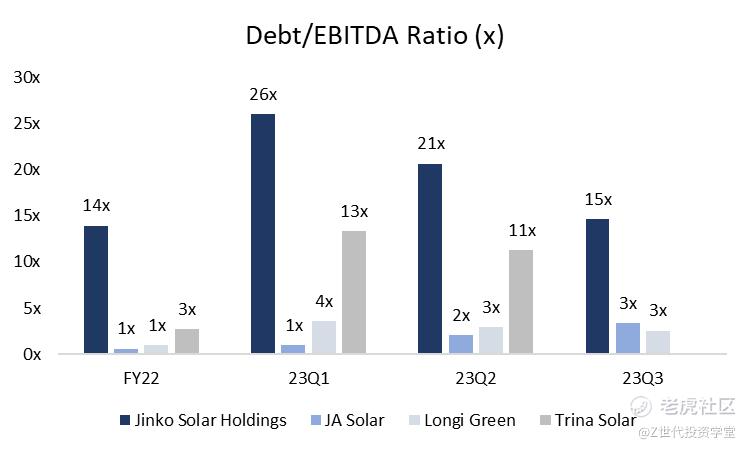

To remain objective in my analysis, I have found some apparent weaknesses in JKS compared to its peers. Most notably, it is highly leveraged compared to its peers, with 42% debt-to-asset ratio as of FY23 YTD (Figure 38). JKS has aggressively expanded its manufacturing capacity with the utilization of debt over the years, which significantly increases default risks if the company's module shipments and module prices fall in light of the solar industry's overcapacity issue. Fortunately, we have seen that in FY23, the Debt/EBITDA ratio of JKS has steadily declined (Figure 39) due to increasing profitability of the company from increasing module shipments and tight cost control efforts. Nonetheless, this remains a key weakness for JKS, especially when prices of solar modules are expected to decline in the short to medium term, which could impact the company's solvency if JKS continues to issue debt to accelerate capacity expansion.

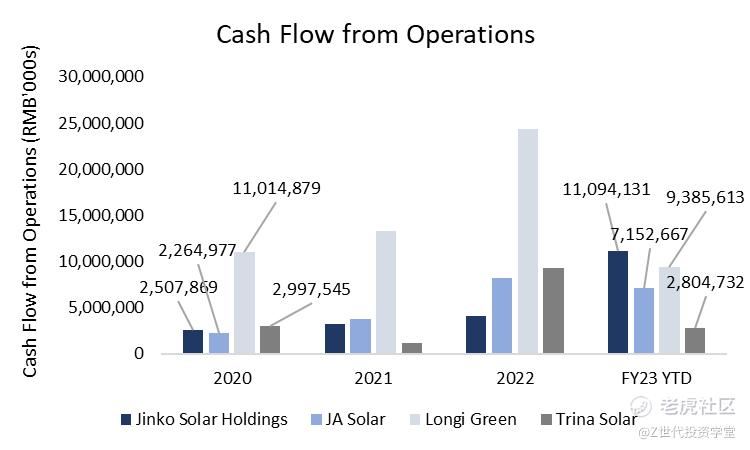

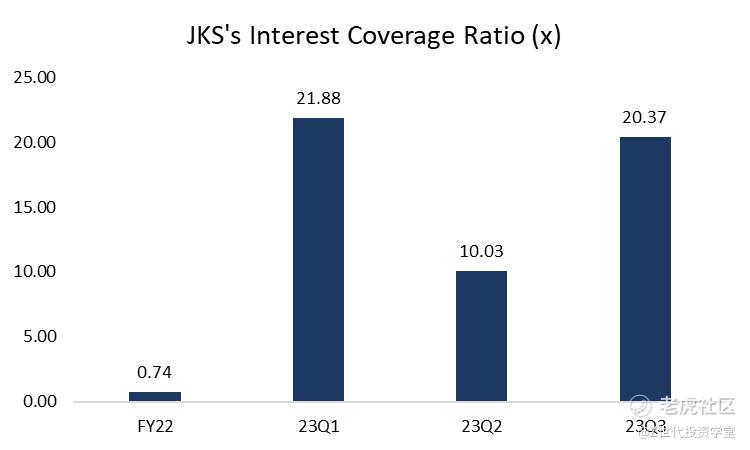

I am also reassured to a certain degree by JKS's increasing cash flow from operations in FY23 (Figure 40), while its peers' operating cash flow generation capabilities have declined substantially. With CAPEX spend being discretionary and a steadily increasing cash flow generation capability, JKS is unlikely to become insolvent despite its highly leveraged profile and from the risks of decreasing industry profitability. JKS's interest coverage ratio has also increased dramatically in FY23, compared to a measly 0.74x in FY22 (Figure 41), which further strengthens my conviction in their ability to meet short term interest obligations on top of their long term debt repayment.

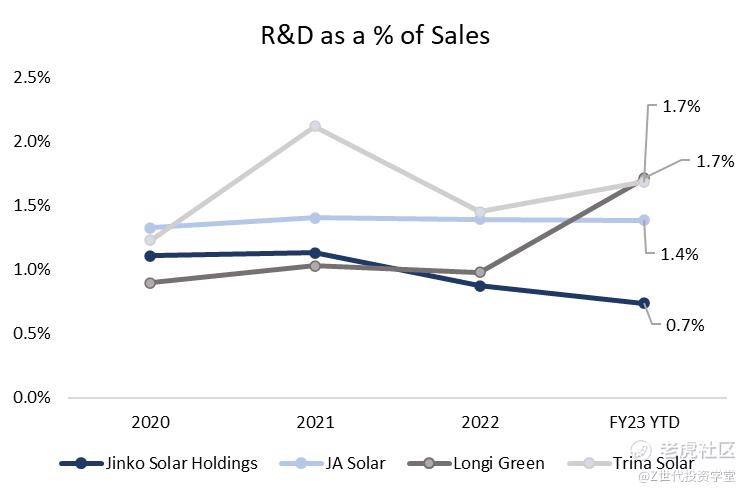

Another important point is JKS's R&D investment glaringly lagging behind its peers, at 0.7% of sales in FY23 YTD (Figure 42), which can be detrimental to its capabilities in retaining its technological moat in the future. However, it does appear that demand for JKS's solar module is still going strong, evident from its outperformance in module shipments in FY23 YTD despite lesser investments in R&D compared to its peers. In fact, while R&D investments have lagged behind its peers from 2020 to 2022, its module shipments have accelerated consistently while module shipment growth of its peers has increased at a much slower pace. This gives me a reason to believe that they are more efficient in converting R&D investments to payoffs, and can play a critical role in sustaining its module shipment growth while controlling their operational costs in light of decreasing solar module prices. This can be an advantage for JKS.

Investment Thesis

1) Narrow technological moat amongst solar module manufacturers creates an opportunity to maintain market share as competition intensifies; JKS's shipments expected to grow healthily

JKS's recent accomplishments and steadfast expansion of N-Type manufacturing capacity has provided it a narrow competitive edge against its competitors, ranking first in the industry from shipments of 30GW of N-Type TOPCon modules in 1H 2023, and is the first in the industry to deliver a cumulative 190GW of solar modules globally as of 3Q 2023.

As mentioned in the competitive landscape analysis above, JKS stands strong with the highest absolute N-Type manufacturing capacity today, and has obsessively expanded its manufacturing capacity in anticipation of an acceleration in solar installations and module demands.

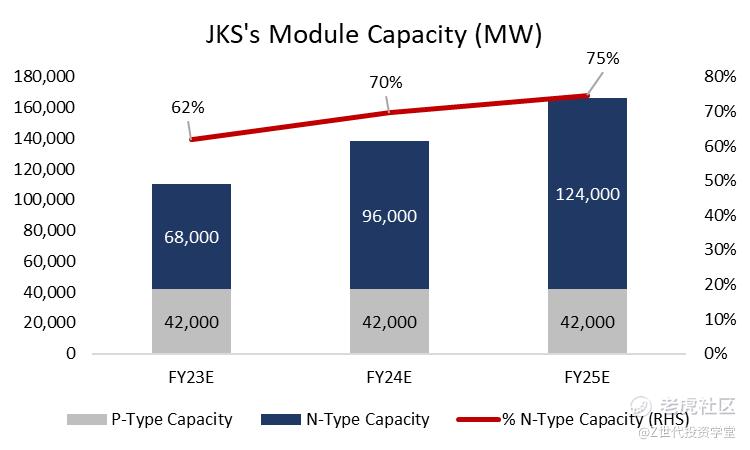

On top of its current dominant position amongst its competitors, JKS commenced construction of its Super-Integrated N-Type Solar Base in Shanxi, China, in September 2023. This manufacturing base will be the largest N-Type manufacturing facility in the entire world, boasting a 56GW manufacturing capacity expansion across wafer, cell and module (28 GW is expected to operational by end 2024 and the other 28GW is expected to be operational by end 2025). If the expansion goes according to plan, JKS's N-Type capacity will nearly double by end FY25 (Figure 43), which I believe will continue to strengthen its value proposition and accommodate rising demand from project developers.

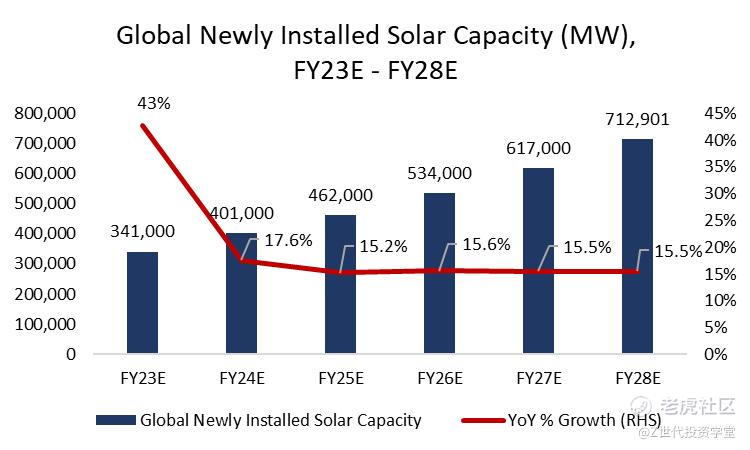

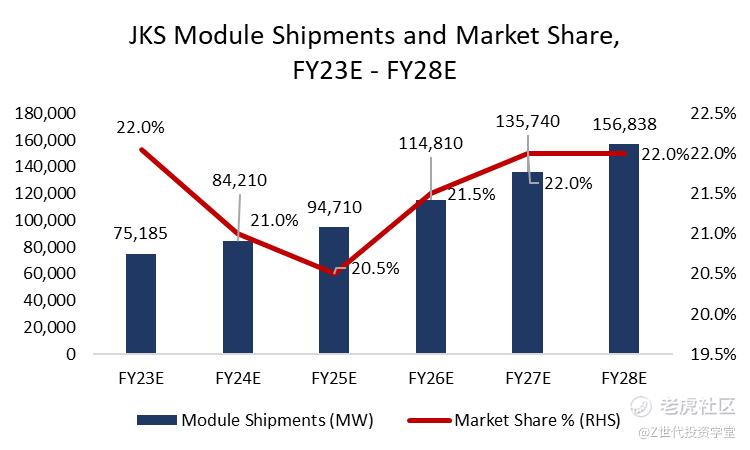

In my base case projections, I utilised SolarPower Europe's forecast for global solar capacity installations, which will continue to grow over 15% annually (Figure 44). With its leading N-Type capacity expansion and continuous innovation in module efficiency, I believe it can retain its market share in the next 2 years, or at the very least, mitigate market share losses from increasing competition within the industry. Thus, I expect JKS's market share in terms of shipments to decline moderately in the next 2 years, before recovering as an overcapacity in the industry will push out weaker players and lead to industry consolidation. Thereafter, I expect market share to increase again from FY26, which would contribute to continuous increases in JKS's module shipments in the next 5 years (Figure 45).

2) Grossly mispriced opportunity from excessive pessimism around solar overcapacity and China's economic downturn; yet fundamentals remain strong while profitability is gaining visibility

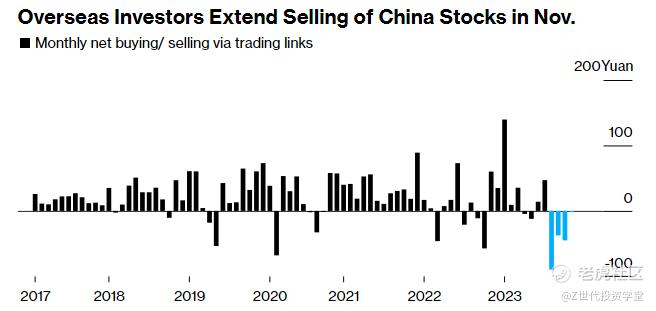

While the market's fear of overcapacity in the solar industry is warranted, I couldn't help but feel that the pessimism for solar module manufacturers has been exacerbated by excessive capital outflows from foreign investors, due to China's economic downturn (Figure 47). JKS is currently trading at 33.50 USD (as of 18 Dec 2023), down close to 19% from the start of the year, and 44% from its peak of 59.86 USD on 23 January 2023 (Figure 46).

Despite the sustained weakening of China's economic conditions, the solar industry relies more on government funding, subsidies and policies rather than consumer sentiments and willingness to spend. Thus, the solar industry should be more resilient despite China's economic downturn, as compared to consumer industries. Moreover, China will still need to double down on its efforts to steer energy efficiency and clean energy installations, to tackle rising energy consumption and reliance on coal capacity expansion. Therefore, I believe it is unlikely that the prolonged economic downturn will slow down solar installations as the Chinese government is likely to continue its support and push for renewable capacity expansion. Falling prices across the solar value chain should also make solar developers' ROI more attractive and hence lead to increasing demand for modules despite China's slump.

Aside from that, the Chinese government has been actively pushing for new policies to put China on a recovery trajectory, even to the extent of exceeding their fiscal deficit limit of 3% to 3.8% in 4Q 2023 to steer intensified and improved fiscal policies. China's third plenum in 2024, which covers economic policies, will be a key catalyst for sentiment revisions by both consumers and investors. I remain optimistic about China's gradual recovery in the next few years, which should lead to some correction in JKS's share price.

Modify on 2024-04-01 23:14

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.