Initial Report(part2): TotalEnergies (TTE) , 38% 5-yr Potential Upside (VIP SEA, Claire CONTRI )

3.1 The Integrated Gas, Renewables, and Power Segment

TotalEnergies’ strategy aims to transform itself into a multi-energy company by profitably growing its portfolio of liquefied natural gas (LNG) and its production of electricity, the two fastest growing energy markets, as well as expanding in decarbonized gas (biogas and hydrogen). The Integrated Gas, Renewables & Power (iGRP) segment is driving TotalEnergies’ ambition in the integrated activities of Liquefied Natural Gas and renewable gases (Integrated LNG) as well as in the integrated electricity chains (Integrated Power). Executing a profitable growth strategy in these promising businesses is helping to achieve TotalEnergies’ ambition to reach carbon neutrality (net zero emissions) by 2050 together with society. The energy transition requires, on the one hand, the electrification of uses through the development of low-carbon electricity production, and on the other hand, a move towards natural gas and low-carbon gases for thermal uses that cannot switch to electricity (long-distance transport).

Thus, to provide more affordable, cleaner, and accessible energy to most people, TotalEnergies is implementing an integrated strategy of profitable growth in the liquefied natural gas and electricity segments. Between 2021 and 2030, TotalEnergies' energy production (excluding Russia), is expected to increase by 4%/y from ~14 to ~20 PJ/d. Half of that growth should come from electricity, primarily from renewable sources, and the other half from LNG. Moreover, the impact of the invasion of Ukraine by Russia on energy markets highlighted Europe's structural dependence on Russian gas pipeline imports. The need to replace all or part of Russian gas has created strong demand for LNG in Europe (+48 Mt in 2022), in a context of limited global LNG supply (+21 Mt) and has generated strong pressures on gas and electricity prices. Thus, both the energy transition made necessary by climate change and the short-term imperatives resulting from the invasion of Ukraine by Russia comfort TotalEnergies' strategy in the areas of LNG and low-carbon energies.

3.2 The Exploration and Production Segment

The Exploration and Production (EP) segment encompasses the oil and natural gas exploration and production activities (excluding LNG) in about 50 countries and the Carbon Neutrality activities affiliated with the EP segment since September 2021.

The average daily production of liquids and natural gas was 2,765 kboe/d in 2022, compared to 2,819 kboe in 2021 and 2,871 kboe/d in 2020. Gas and associated products (condensates and natural gas liquids) represented approximately 53% of TotalEnergies’ overall hydrocarbon production in 2022, compared to 55% in 2021 and 55% in 2020. Crude oil and bitumen represented 47% in 2022, compared

to 45% in 2021 and 2020.

3.3 The Refining and Chemicals Segment

Refining and Chemicals activities include refining, base petrochemicals (olefins and aromatics); polymer derivatives (polyethylene, polypropylene, polystyrene, and hydrocarbon resins), including biopolymers and recycled polymers obtained from chemical or mechanical recycling, as well as the production of biofuels from the transformation of biomass and, since January 1, 2022, the production of specialty fluids, previously reported in the Marketing and Services segment. The Refining & Chemicals activities also include the processing of elastomers by Hutchinson.

TotalEnergies holds stakes in 16 refineries located in Europe, the United States, the Middle East, Asia, and Africa, eight of which are operated by TotalEnergies companies including two biorefineries in France (La Mède, and Grandpuits, which is in the process of being converted). As of December 31, 2022, TotalEnergies’ refining capacity was 1,792 kb/d, compared to 1,793 kb/d at year-end 2021 and 1,967 kb/d at year-end 2020. The refining capacity of the Refining & Chemicals segment totaled 1,785 kb/d at year-end 2022 (or 99% of TotalEnergies’ total capacity). TotalEnergies' petrochemical operations are in Europe, the United States, Qatar, South Korea, and Saudi Arabia. Being either adjacent to or connected by pipelines to TotalEnergies refineries, the vast majority of the petrochemical operations are integrated with its refining operations, thereby maximizing synergies. As of December 31, 2022, TotalEnergies' global petrochemical capacity (olefins, aromatics, and polymers) was 21,885 kt, compared with 21,381 kt at year-end 2021 and 21,299 kt at year-end 2020. This capacity increase in 2022 is mainly due to the start-up of the ethane cracker in Port Arthur (USA).

3.4 The Marketing and Services Segment

Marketing and services include the global supply and marketing activities of oil products and services, low-carbon fuels, and new energies for mobility. It contributes to the transformation of TotalEnergies and proactively supports its customers in their transition towards more sustainable energies and mobility. With a direct presence in close to 110 countries, Marketing & Services (M&S) caters to customers with various energy, mobility, and associated services needs. M&S also caters to a wide range of professional customers in terms of size and industry (transport, manufacturing, agriculture, etc.), and individual customers, through its retail network of over 14,600 service stations and 42,000 public and private electric charging points.

M&S has historically formulated and marketed various ranges of petroleum fuels and lubricants. In addition, M&S develops an increasing number of associated services, both made available within its service stations network (catering, washing, shops, etc.) and to industrial customers. It also offers its clients new energy and mobility services such as biofuels, electric charging, LNG for ships, natural gas, biogas, or hydrogen for other transport modes. TotalEnergies has a strong presence in Western Europe (Benelux, France, Germany) and in Africa, where M&S is among the leaders in petroleum product distribution (regarding the number of service stations).

Industry Overview

4.1 Market Size

In 2022, the global energy and renewables market was valued at USD 2.018 Billion in 2022. It is estimated to reach USD 4.286 Billion by 2031, growing at a CAGR of 8.73% from 2023 to 2031. On the other hand, the oil and gas market was valued at USD 6.989 Billion in 2022. It is expected to grow to USD 8.670 Billion in 2027 at a CAGR of 4.3% from 2023 to 2027. Hence, both sectors are experiencing rapid expansion, driven by the proliferation of emerging clean technologies and increasing concerns over environmental depletion due to energy and oil production.

4.2 Growth Drivers

The growth drivers of the energy, renewables, oil, and gas market will primarily be due to the following growth drivers: energy transition, critical minerals, and technology adoption.

4.2.1 The Energy Transition

Oil and gas companies are increasingly exploring clean energy avenues. However, their direct spending on low-carbon fuels and technologies, excluding investments to boost productivity and reduce emissions from operated assets, constitutes only 4% of their upstream capex. The global upstream industry is expected to generate US$2.5 trillion to US$4.6 trillion in free cash flows from its hydrocarbons business between 2023 and 2030, so lack of capital is not an issue. Instead, the central challenge is scaling innovation while maintaining profitability and shareholder value.

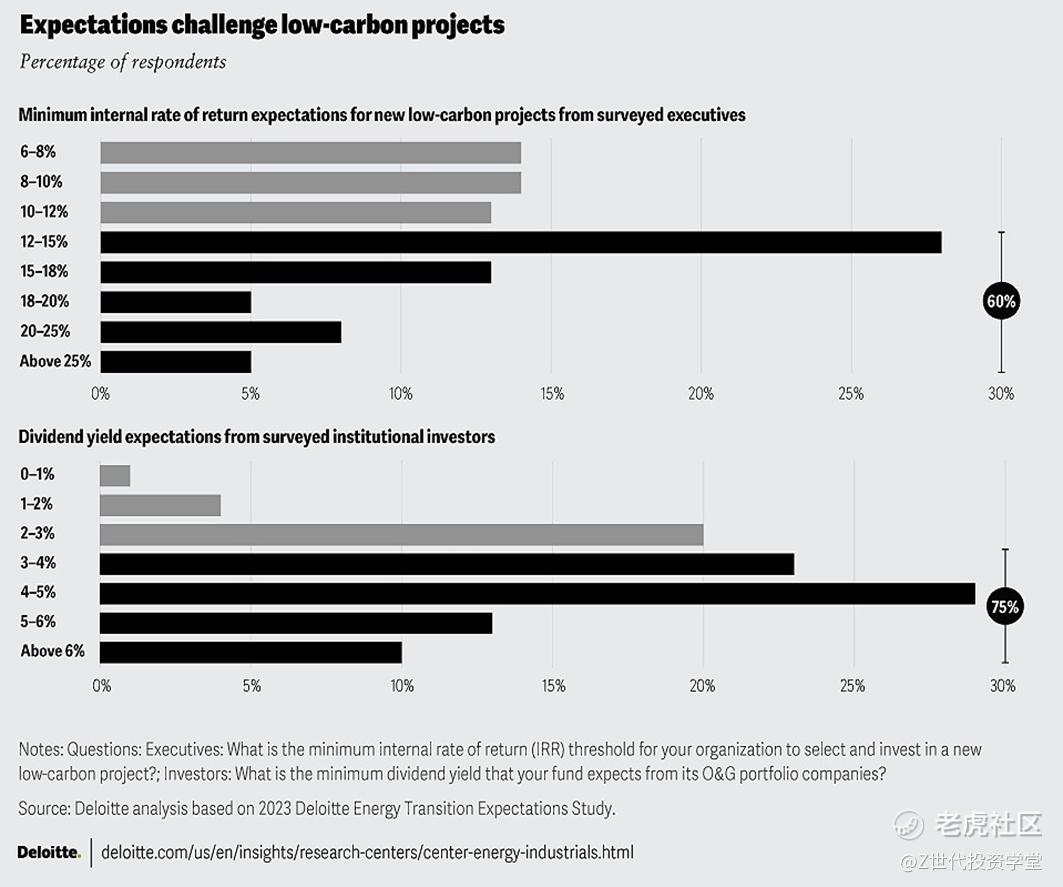

In Deloitte’s survey of Oil and gas executives in July 2023, 60% of respondents stated that they would invest in low-carbon projects if their returns exceeded 12% to 15% (figure 2). In 2022, returns on major renewable electricity projects ranged between 6% and 8%. Thus, the Oil and Gas industry would likely focus its 2024 spending on:

Initiatives aimed at improving operational efficiency and reducing emissions, with more than one-third of surveyed O&G executives citing operational efficiency and direct emissions (scope 1 and 2) reductions as pivotal metrics for assessing energy transition progress and

Low-carbon fuels adjacent to their core or complements their primary operations, with around 37% to 44% of surveyed O&G executives citing natural gas, carbon capture and storage (CCS), biofuels, and hydrogen as critical to their low-carbon investment strategies.

Figure 3

Moreover, since 2021, many new clean energy policies have been adopted or proposed worldwide, including the Infrastructure Investment and Jobs Act and the Inflation Reduction Act in the United States, the proposed European REPowerEU Plan, and the proposed Net-Zero Industry Act in the European Union. Similarly, renewable energy targets in Asia-Pacific and significant renewable energy auctions in South America seek to spur the adoption of clean energy. However, the effective execution of these policies or the progression of these proposals remains important for attracting capital and reducing investment risks.

Therefore, the oil and gas industry’s disciplined, high-return capex strategy may initially yield gradual shifts. But if policies are swiftly implemented and consumers rapidly adopt practices that bolster the scalability and commercial viability of low-carbon solutions, it could fundamentally reshape the medium- to long-term capital allocation strategies of O&G companies.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.