Sunnova: Strong Growth But Needs More Scaling To Become Profitable

Summary

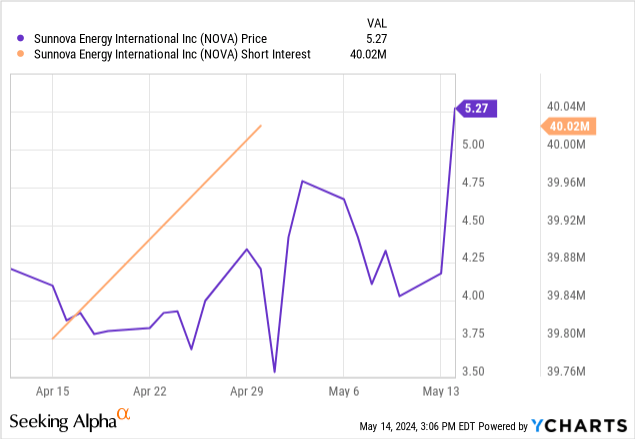

- Sunnova Energy International is benefiting from a short squeeze, with a short interest of 40 million shares making up a third of the share count.

- The company provides solar energy services to over 440k customers in the US and growing its revenues nicely even though it will take a while to be profitable.

- The company has a lot of debt (11x its revenues) but most of the debt belongs to its financing arm, which provides financing to customers. Still doesn't make it risk-free.

- The company's full year guidance calls for profits but it's an adjusted metric that includes tax credits and excludes items so be cautious.

anatoliy_gleb

Sunnova Energy International (NYSE:NOVA) is a solar energy company whose stock has been benefiting greatly from this week's short squeeze as the stock had a short interest of 40 million shares prior to this week which makes up almost a third of the company's existing 122 million shares (as of last quarter). In this article, we'll cover this stock in terms of business, operating metrics, valuation and risks.

Data by YCharts

Data by YCharts

Business Overview

Sunnova is an energy service company that provides solar energy related services to more than 440k customers in 50 US states and territories. The company offers a variety of energy-related services including but not limited to designs, installations, operations, maintenance, repairs, replacements, upgrades, optimizations and monitoring. It also has a side business that includes products such as home security systems and home heating & air conditioning services but the main part of the business is production, storage and distribution of renewable energy.

The company sits in the midst of an energy revolution where there is tremendous demand for electricity in general as well as renewable electricity specifically. Between the rise of electrical vehicles, higher consumption of electricity due to data centers and higher demand from AI-powered industries, there is going to be an increased demand for electricity products for a very long time. Furthermore, America's traditional power grid has been aging and in need of replacement and some of this will need to be replaced with renewable energy sources, which creates further demand. On top of the demand for energy itself, there is also additional demand for storage and management of the energy, which is another line of business as a whole.

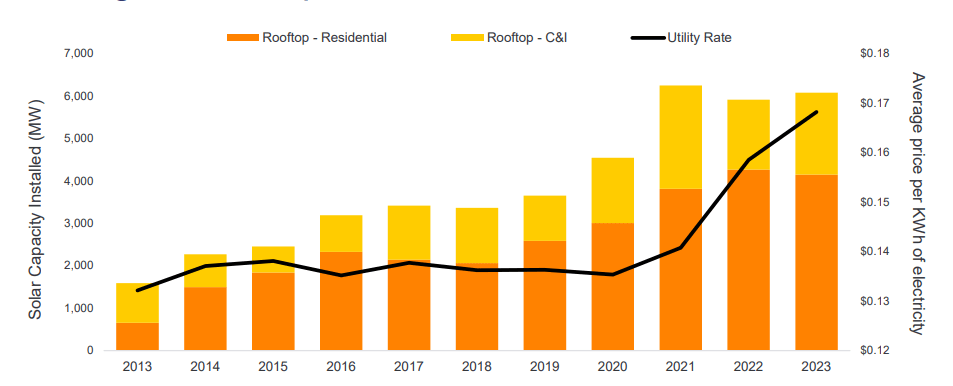

As technology improves, solar panels are getting exponentially better each year in terms of technology, efficiency and cost. Just a decade ago renewable energy was prohibitively expensive but now prices are coming to a level where soon enough there might not be much price difference between traditional energy and renewable energy which should help with demand even further. Also it's noteworthy to mention that "traditional electricity" has also seen its unit price rise significantly in recent years due to inflationary pressures and many local utility services across the country have been raising their prices at healthy levels in recent years which further helps reduce the gap between traditional electricity and renewable electricity prices.

Utility Prices & Solar Adoption (Sunnova)

On the negative side, many renewable energy companies including Sunnova have yet to show profits and are suffering from high levels of debt. Sooner or later, this industry will have to go through some sort of consolidation where bigger players merge with smaller players in order to reach sufficient scale for profitability.

Typically, the company works with local dealers in each state and region in order to provide the best prices and services in each location without physically having presence everywhere. Recently, the company announced that it signed an exclusivity deal with the Home Depot (HD) which will allow it to exclusively market its solar and battery storage products and services in more than 2,000 Home Depot locations within the US. The company is also investing further into other initiatives such as Adaptive Technology Center and Virtual Power Plant network for its long-term plan of becoming a sustainable play and expanding its national reach.

New Developments (Sunnova)

Operating Metrics

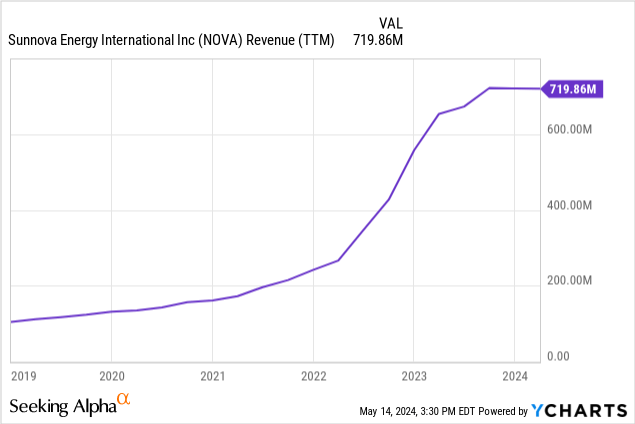

From a revenue side, the company has been growing nicely in the last 5 years. Since 2019, NOVA's revenues are up by almost 600% driven by higher customer volume, addition of new products and services and being able to charge higher prices. During this time, the company expanded from just a few states to all 50 states, increased its network of dealers, signed partnerships with retailers such as the Home Depot, added a variety of new services and products such as improved batteries and storage units and this helped fuel its revenue growth which is likely to continue for the foreseeable future as the demand for renewable energy continues to rise in the country.

Data by YCharts

Data by YCharts

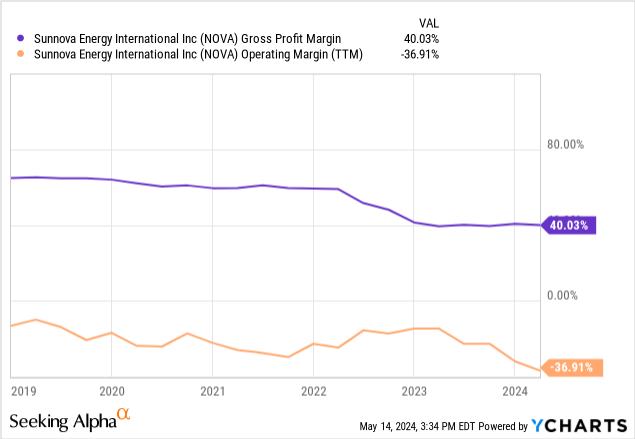

From a profitability point of view, things don't look as bright though. This problem is not specific to this company though. It can be said about most renewable energy companies that they haven't really reached a sufficient scaling that would allow them to show any profits. These companies are simply too small, trying too aggressively grow, and it may be a while before they can show profits. NOVA's gross profit margin dropped from 60% to 40% in the last 5 years, whereas the company's operating profit margin dropped from -10% to -37% during the same period. By itself, lack of probability may not be a big deal since this is a growth company and growth comes first, but it can be a problem when low profitability is coupled with high levels of debt.

Data by YCharts

Data by YCharts

Debt Structure

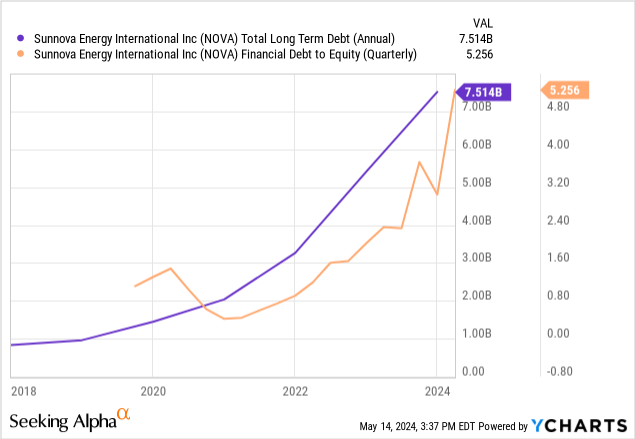

The company's debt levels are alarmingly high. In fact, the company's long-term debt of $7.5 billion is almost 11 times its annual revenues of $720 million. Even with assuming an eventual profit margin of 10%, it would take about 100 years for the company to pay off its debt. The current debt levels corresponds to 5.2x times its equity which is up significantly from 3.0x times last year.

Data by YCharts

Data by YCharts

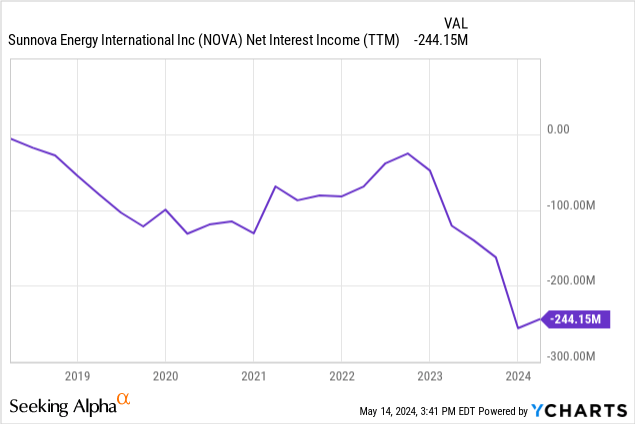

In the last 12 months, the company spent $244 million on interest payments, which is a third of its revenues. This is very high.

Data by YCharts

Data by YCharts

To be fair, not all debt is equal and there is something investors should notice about this company's debt structure. The company offers financing to its customers, including traditional financing, leasing options and power purchase agreements. Think of this like how car companies like Ford (F) and GM (GM) have huge amounts of debt in their balance sheet but most of the debt actually belongs to their finance arm rather than automotive arm. These companies provide financing to their customers, and these loans appear as company's own debt on their balance sheet. This company's debt structure is also similar where most of its debt is actually obligations from its customers who use its financing.

This doesn't make it less risky though because it's still debt that needs to be paid and if the economy were to enter a recession and some clients were unable to pay their financing or leasing obligations, the company would have to pay it, which would be very costly. If the rate of loan failures from customers was high enough it could even create a situation where the company could possibly default on its own debts.

Valuations

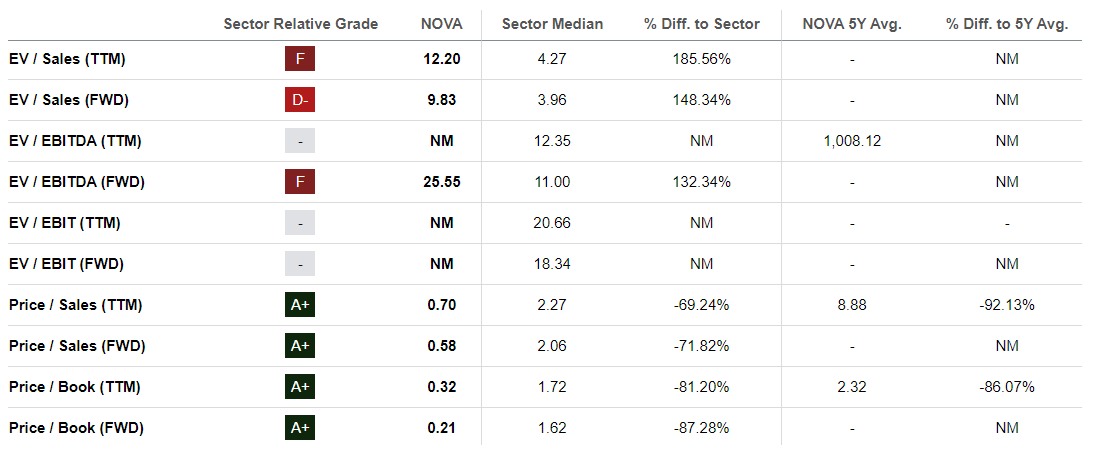

It's very tricky to calculate valuation of a company that doesn't have net profits. For NOVA, there are a few metrics that might be relevant such as Price to Sales or Price to Book Value. The company currently trades at 0.70x times its trailing sales, 0.58x times its forward sales and 0.32x times its book value. Investors don't expect this company to reach profitability anytime soon.

Valuation (Seeking Alpha)

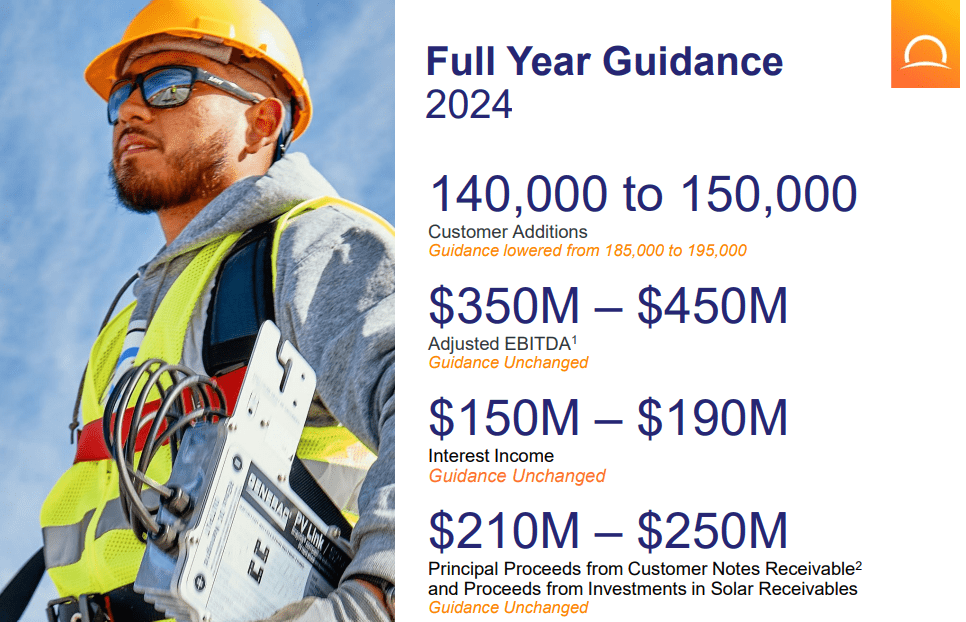

Interestingly enough, the company's full-year guidance for 2024 calls for adjusted EBITDA of $350 million to $450 million. If we take the midpoint of this value it would give us $400 million and if the company were to achieve this number, its current market cap of $500 million would look pretty cheap as it would be only 1.25x times its adjusted EBITDA. Keep in mind that the company's definition of adjusted EBITDA is highly liberal and excludes many items that you wouldn't want to exclude from an income statement though. It also includes a generous ITC (Investment Tax Credit) which may or may not be repeatable in the future.

Full Year Guidance (Sunnova)

Conclusion

This is an interesting company that's positioned in a growing market and posting a lot of growth but needs to scale up more in order to reach profitability. Also the company's debt levels are alarming but most of it belongs to its customers' debt and leasing obligations, similar to how a car company's debt might be mostly from its financing arm. This is still a speculative play and it may continue rallying based on short squeeze but conservative investors should probably keep their positions size small on this one as it hasn't yet proved itself to be profitable and sustainable.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.