Geospace Technologies Will Likely Move Sideways For Now (Rating Downgrade)

Summary

- GEOS' oil & gas business underperformed in Q2 due to slow project execution and lower fleet utilization, putting pressure on its topline and margin.

- Despite short-term challenges, GEOS' growth potential in the offshore industry and focus on adjacent and emerging markets should help stabilize revenues.

- The stock is reasonably valued compared to peers, but the deferral of large rental projects and negative cash flows may impact near-term performance.

shotbydave/E+ via Getty Images

GEOS Will Get Past The Current Slowdown

I discussed Geospace Technologies Corporation (NASDAQ:GEOS) in the past, and you can read the last article here, published on January 4. In Q2, its oil & gas business underperformed due to the slow execution of projects and lower utilization of the marine OBX rental fleet. Operators' lack of capex commitment following the emphasis on shareholder returns will pressure GEOS' topline and margin. Cash flow turning south in 1H 2024 is another matter of concern for the investors.

However, I think the offshore industry's growth potential will eventually overcome the challenges and improve asset utilization. The company's initiative to increase the share of revenues from adjacent and emerging markets will reduce the typical energy market volatility. GEOS continues to hold a solid balance sheet with sufficient liquidity. The stock is reasonably valued compared to its peers after a 20% fall over the past month. Given the short-term challenges and my expectations of a steady recovery in the medium term, I view it as a "hold."

Why Do I Downgrade My Rating?

In my last iteration on GEOS, published on January 4, I discussed how the company established a stable platform with increasing rental revenues. It received several contracts for its Mariner Ocean bottom nodes and monitoring products. However, gaps in utilization in some OBX rental contracts created pressure. I wrote:

Increased activity in the offshore energy market has led to higher demand for deep and shallow water nodes. This primarily increased demand for GEOS' Mariner technology products. Among the key projects, rental terms for a contract were scheduled to start shortly. With an improved cash flow and a solid balance sheet, it warranted a "buy" rating.

Since then, the recovery has been slower than expected as operators focused on shareholder returns while growth took a backseat. Some large rental projects were deferred, and the benefits will accrue in the coming quarters. GEOS' rental fleet of OBX ocean bottom nodes will likely see improved utilization as offshore E&P activities rebound. Similarly, government funding has been slow to come to the rescue. On the other hand, the company's Quantum product line has applications in government security agencies, CCS, and geothermal energy. Cash flows turned negative again in 1H 2024. Considering the company's robust balance sheet, I will downgrade my rating to a "hold."

Business Outlook

Seeking Alpha

In the near term, energy exploration-focused activities, including seismic data acquisition activities, can continue to slide because of the lag between crude oil price recovery and its effect on energy activities. GEOS' rental fleet of OBX ocean bottom nodes will likely see improved utilization as offshore energy exploration and production activities recover. During the past downturn, many operators allocated cash on stock buy-back programs and dividend payments. With a steady crude oil price, I expect reinvestment capital into exploration activities to increase in 2H 2024.

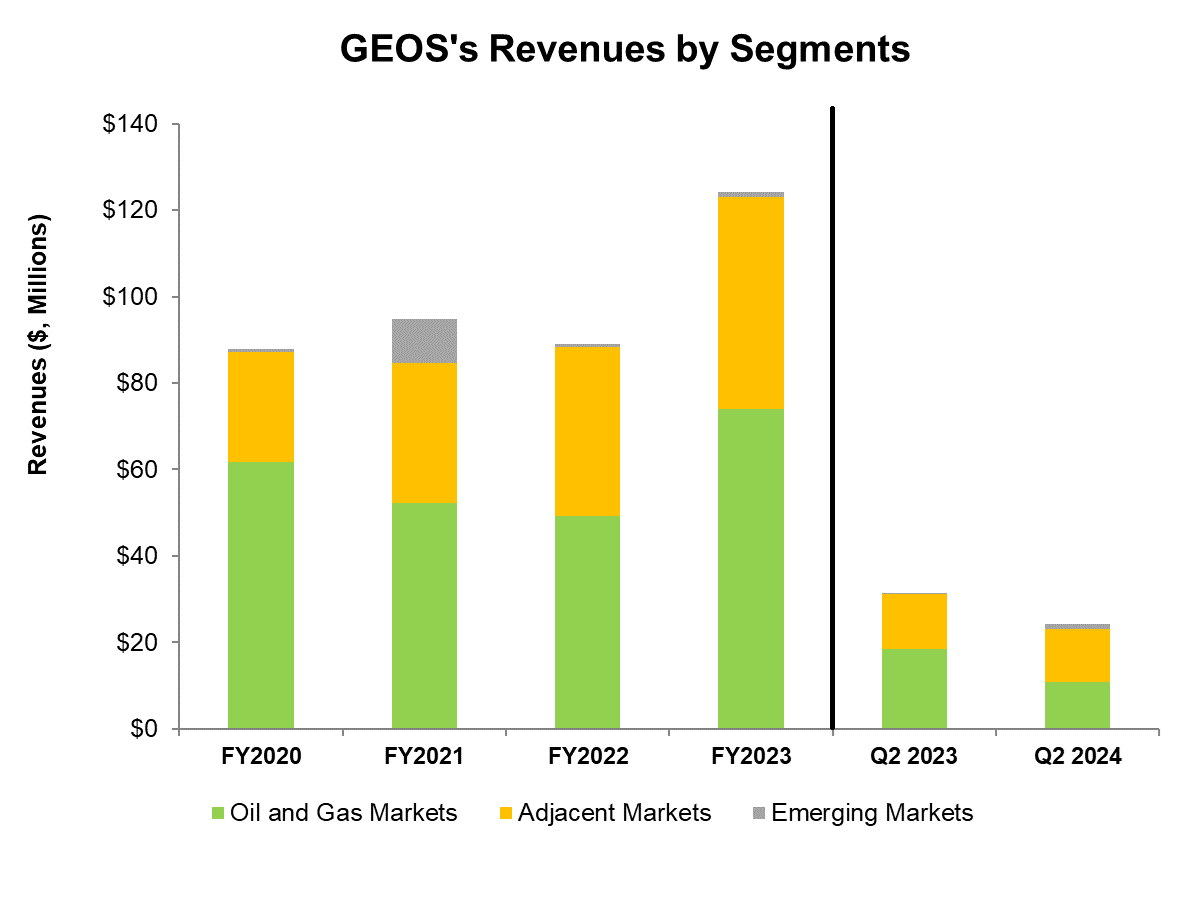

GEOS' adjacent markets segment revenue generation in Q2 2024 was among the best in its history. This reflects the company's efficiency in creating a stable source of revenue from this segment. The company expanded product lines here, which enabled it to minimize the volatility that is often associated with the oil and gas market segment.

The revenue share from the emerging market portfolio increased from 1% in Q2 2023 to 6% in Q2 2024. This followed a recent fulfillment of the DARPA contract. Its emerging market business primarily consists of the Quantum product line, which includes SADAR - a detection system. This system is used mainly in border and perimeter security surveillance and cross-border tunneling detection. The technology also has applications in carbon capture and storage (or CCS) and geothermal energy. Various government agencies requiring real-time seismic data, including the US Department of Defense, Department of Energy, and Department of Homeland Security, use this technology.

Challenges

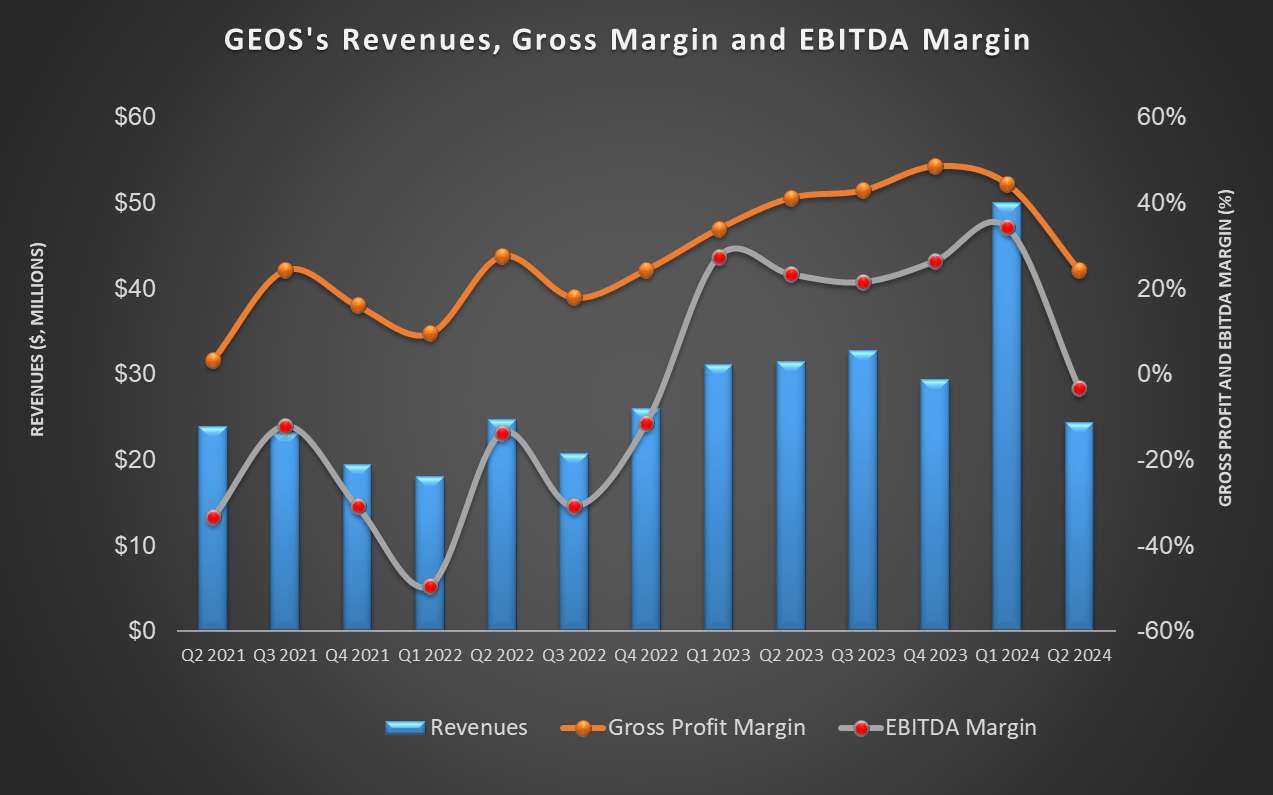

In Q2, GEOS' revenues from rental products declined by 65% compared to a year ago. In recent times, the company has not announced any large rental projects, and the current revenue originates from past projects. It is likely that some of the projects "slipped," and actual rentals from these projects can start to show by Q4 2024. However, the rest of the projects have already been placed and the company requires OBX because current demand will likely exceed capacity.

Recently, some government agencies voiced concerns over the company's Quantum products, particularly in border patrol and its capabilities. While GAO (Government Accountability Office) reports cited that additional money would be spent on some of those projects, this is unlikely to occur before 2025. So, the government budgetary cycles will largely determine the performance of the emerging market segment. I do not see its performance improving before 2025.

My Estimates

Over the past ten quarters, GEOS' adjusted EBITDA has been negative on five occasions. However, I expect the volatility and pressure from low utilization to ease as revenues from emerging markets, applications in CCS, and geothermal energy help stabilize revenues. While its Q2 EBITDA would change little, I expect adjusted EBITDA to increase by 5%- 7% in FY2024.

Q2 Performance Analysis

GEOS' Filings

As announced in the Q2 earnings released on May 9, In Q2 2024, GEO's year-over-year revenues from the Oil and Gas Markets segment decreased by 41%. Various project deferrals and lower utilization of the marine OBX rental fleet caused revenues to decline in Q2 2024. However, I expect increased rental contracts for ocean bottom nodes after they complete maintenance in the Houston facility. The segment's operating income turned to a loss in Q2 from a profit a year ago.

Revenues in the Adjacent Markets segment remained relatively unchanged year-over-year in Q2. Operating income, however, decreased. Low demand for its water meter products and industrial sensor products put pressure on the segment's performance. GEOS' revenues from the Emerging Markets segment increased significantly, although its share of total revenues is low (~5%).

Cash Flows And Liquidity

In 1H 2024, GEOS' cash flow from operations remained negative and deteriorated over the previous year, despite higher revenues. As a result, free cash flow stayed negative in 1H 2024. With zero debt, GEOS has a distinct advantage over some of its peers (FTI and SLB). Its capex budget for FY2024 is 14% lower than FY2023.

As of March 31, its liquidity (cash and short-term investment) was $51 million. The company is authorized to repurchase up to $5 million in share buybacks. However, with a negative FCF, I doubt the company will attempt to repurchase before cleaning house.

What Does The Relative Valuation Imply?

Author Created and Seeking Alpha

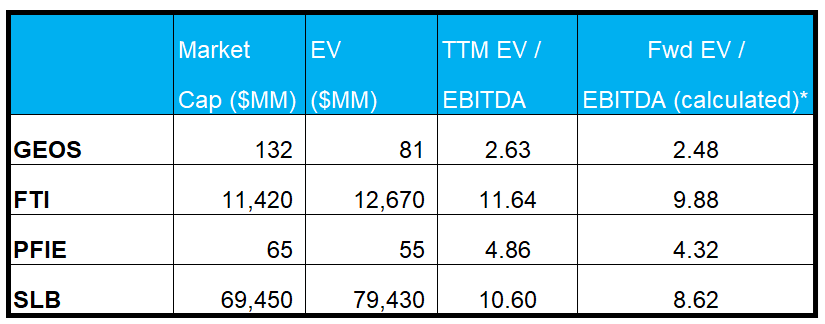

GEOS' current EV/EBITDA multiple (2.6x) is much lower than its five-year average (18x). So, it appears to be undervalued versus its past. If the stock trades at its five-year average, it would provide a 355% upside potential. However, the industry environment has vastly changed over the years and I do not see the stock trading anywhere close to its past average. The stock price decreased by 22% since my last publication on January 4. The stock plummeted after recording an unimpressive Q2 result on May 9.

The forward EV/EBITDA multiple for GEOS' peers is expected to contract versus the current multiple, which implies a rise in EBITDA for its peers in the next four quarters. The sell-side forward EV/EBITDA multiple for GEOS is not available. Nonetheless, applying my estimated growth rate (as discussed earlier in the article) will translate to $32.8 million of adjusted EBITDA in the next four quarters. This means GEOS' forward EV/EBITDA multiple (2.5x) would contract at a lower rate than its peers, which typically results in lower current EV/EBITDA. GEOS' current EV/EBITDA multiple (2.6x) is steeply lower than its peers' (FTI, PFIE, and SLB) average. So, the stock appears to be reasonably valued with a positive bias.

As I discussed earlier in the article, I expect 5%-7% adjusted EBITDA growth in 2024. Feeding these values in the EV calculation and assuming the forward EV/EBITDA multiple holds, the stock can trade between $10.2 and $10.4, implying a marginal 2.5% upside. However, given the impact of the project slip-ups in the recent past, I also think investors can expect downsides in the short term.

Risk Factors

EIA and Seeking Alpha

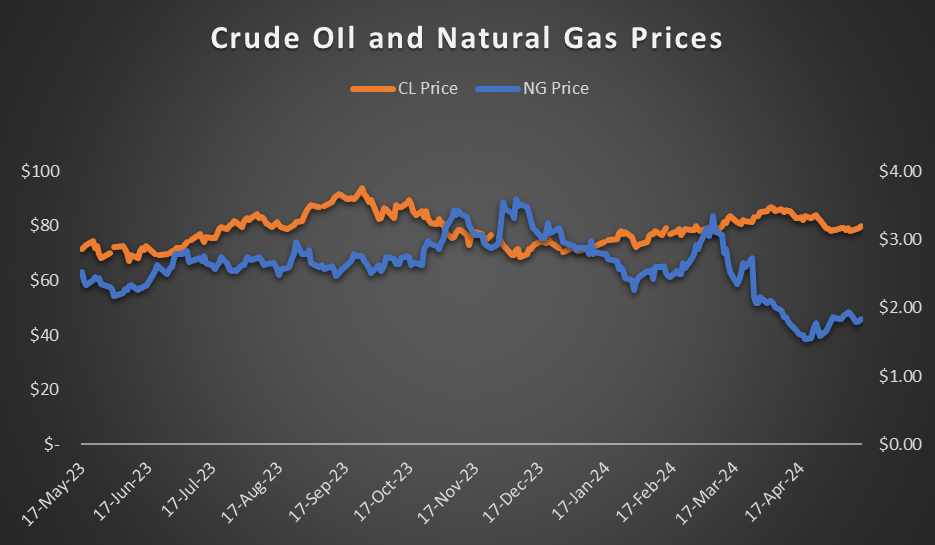

Over the past year, energy prices have diverged, as illustrated in the graph above. Crude oil prices have stabilized, increasing by 12% in the past year. Natural gas prices have been volatile, gathering pace in early 2024 due to the typical demand pattern in winter. However, they failed to sustain the momentum, declining steeply over the past few months, although they appear to be recovering in recent weeks.

When commodity prices correct or decrease, upstream operators' capital spending budgets typically contract in response. The geopolitical instability around some international geographies has contributed to the pricing weakness. The other risk factors relate to foreign policies and trade relations with foreign partners. In FY2023, customers outside the United States accounted for approximately 50% of GEOS' revenues. In the past, trade wars and restrictions impacted the company's financials. Given the changing geopolitical environment, such instances can affect the company's revenues and margins in the future.

What's The Take On GEOS?

Seeking Alpha

GEOS' growth momentum has been thwarted in the near term due to the lag between crude oil price recovery and seismic data acquisition activities. Over the medium term, I expect increased activity in the offshore energy market to lead to higher utilization for its rental fleet of OBX ocean bottom nodes. The company's diversification strategy has reduced earnings volatility. Effective use of new product lines, including a detection system, has significantly increased its share of revenues from non-energy activities.

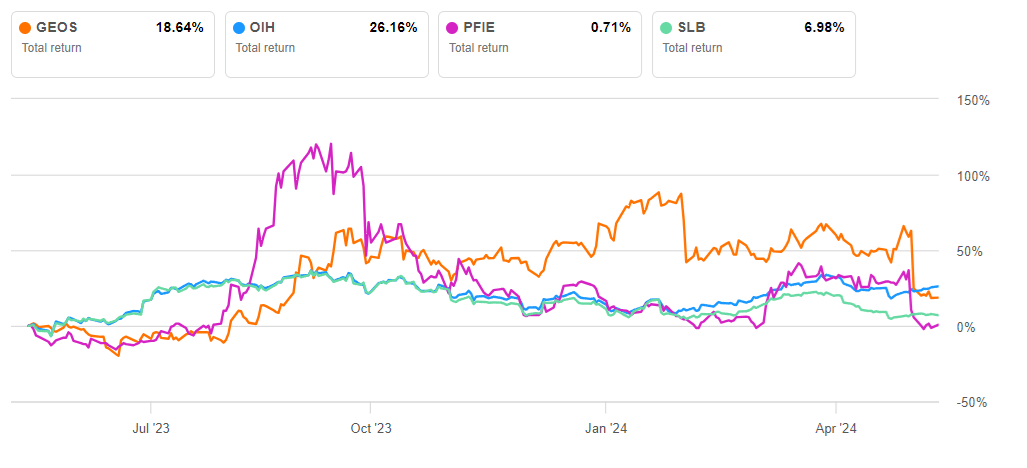

However, the likely deferral of large rental projects can adversely impact its near-term revenue generation. So, the stock underperformed VanEck Vectors Oil Services ETF (OIH) in the past year. Cash flows deteriorated in 1H 2024. Negative cash flows may also have caused the capital budget to shrink in FY2024. The stock's relative valuation appears fair to me. Given my expectation of marginal EBITDA growth, I expect the stock price to produce marginally positive returns in a year. So, I rate it a "hold."

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.