Brookfield's Microsoft Agreement Is A Big Deal

Summary

- Brookfield Renewable signed a global renewable energy agreement with Microsoft, setting the stage for over 10.5 GW of solar and wind capacity, largely in the US.

- The deal highlights Brookfield's position for similar agreements with other data center companies.

- The increased use of solar and wind in the US, led by companies like Brookfield, is transforming the energy landscape.

Justin Paget

Introduction

My February article talks about the way Brookfield Renewable’s (NYSE:BEPC) (NYSE:BEP) asset classes are expanding beyond hydro. The article noted how management has a knack for understanding the economics of different types of energy asset classes at different times. For years management has said solar and wind will be more important in the future and a major development has taken place since the time of the article. Brookfield announced the signing of a global renewable energy framework agreement with Microsoft (MSFT) on May 1st. The agreement sets the stage for over 10.5 GW of capacity and it will center on solar and wind in the US. My thesis is that this agreement is a big deal.

The Numbers

The cost and effectiveness of solar and batteries continues to improve right when we need them most as power-hungry data centers stress our resources. Putting this 10.5 GW Microsoft data center deal in perspective, Brookfield’s 4Q23 supplemental shows current wind capacity of 10.9 GW and utility-scale solar capacity of 7.1 GW.

Different asset classes have different capacities so I also like to think about what this Microsoft deal means in terms of long-term average (“LTA”) GWh. This way we can better compare it to hydro which has a higher capacity factor than solar and wind. Brookfield’s 2023 LTA capacity factor for wind was 37% or (35,759 LTA GWh*1000)/(365*24*10,945 MW) while their 2023 LTA capacity factor for solar was 25% or (15,211 LTA GWh*1000)/(365*24*7,073 MW). If this agreement ends up being mostly solar such that we end up with solar capacity of 8 GW and wind capacity of 2.5 GW then we can pencil out some LTA numbers to put things in perspective. 8 GW*365*24*0.25 for solar implies solar LTA of 17,500 GWh. Wind LTA could be about 8,000 GWh when rounded to the nearest 500 GWh from 2.5 GW*365*24*0.37 such that the LTA sum of solar and wind from this deal could be over 25,000 GWh.

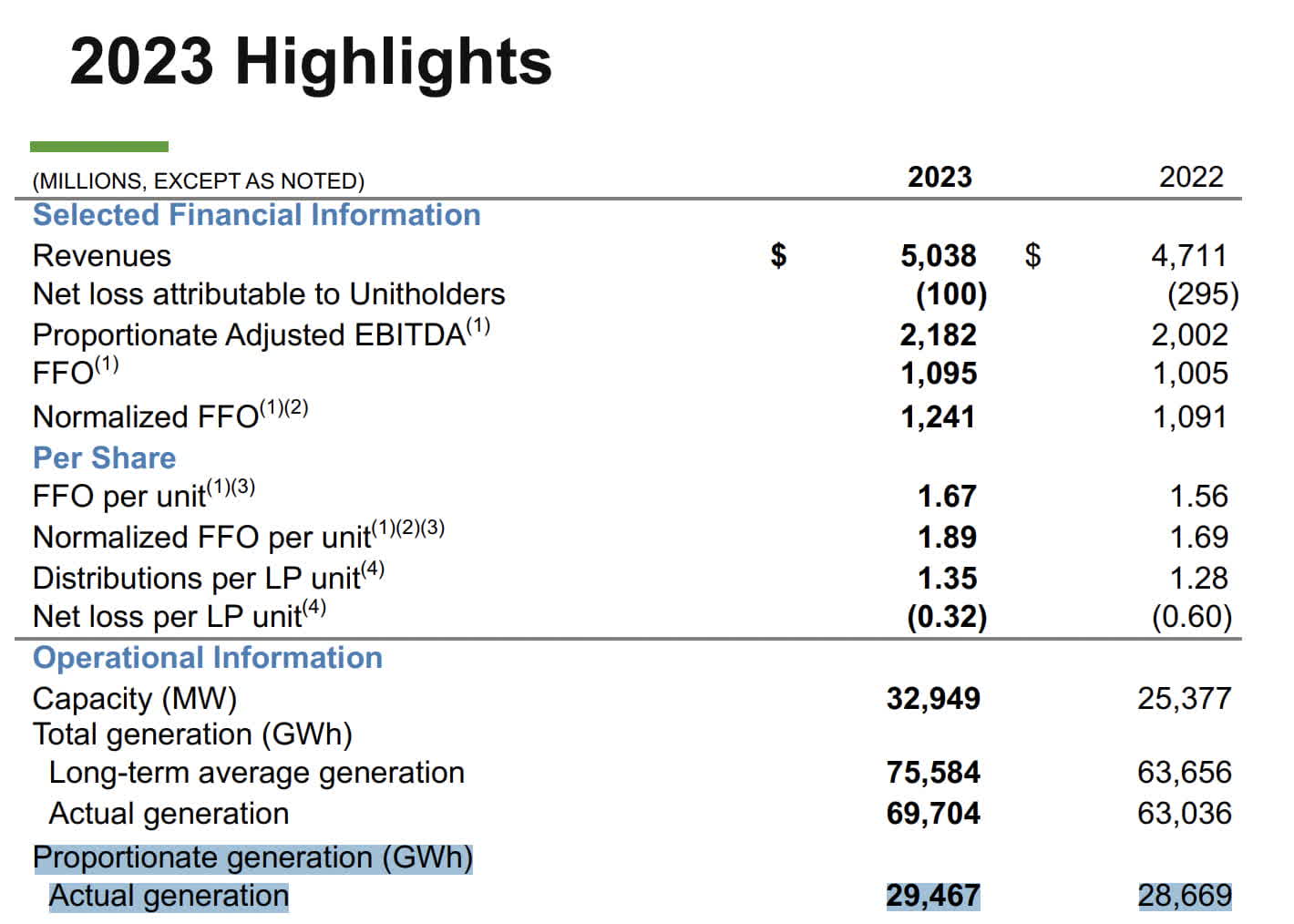

This agreement with one counterparty/offtaker, Microsoft, is prodigious on a relative basis. Looking at Brookfield’s consolidated numbers for all offtakers/buyers in 2023, they had 92,054 LTA GWh in total which came from 38,095 GWh hydro plus 35,759 GWh wind plus 15,211 GWh utility-scale solar plus 2,989 GWh distributed energy & storage. The above LTA numbers including the 92,054 GWh total are based on a December 31st year-end basis whereas the lower LTA number of 75,584 GWh in the highlights below is what Brookfield could have done during the year with the assets they owned:

2023 highlights (4Q23 supplemental)

The above proportionate generation number of 29,467 GWh includes some non-renewable generation such as biomass and power transformation such that it is slightly higher than the 29,082 GWh proportionate number from the renewable table.

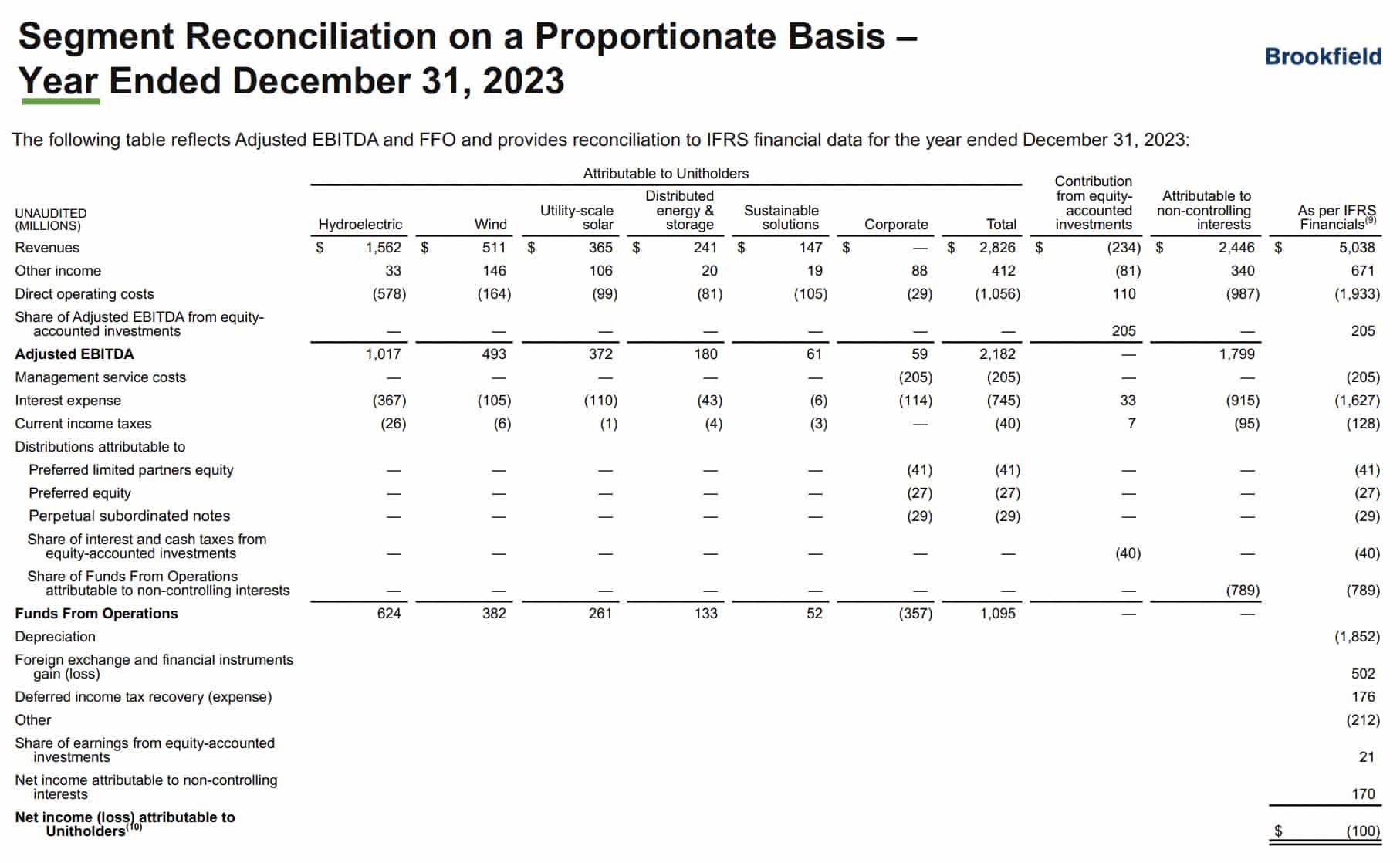

This deal will bring significant incremental FFO and revenue into the picture and we can put this in perspective by looking at the current FFO and revenue for solar and wind. Before we do so, it is helpful to clarify the difference between proportionate numbers and consolidated numbers in the financial tables. Slide 24 of the 4Q23 supplemental shows proportionate FFO for 2023 was $1,095 million on proportionate revenue of $2,826 million. Consolidated numbers are shown on an IFRS basis and there isn’t any standardized meaning prescribed by IFRS for FFO. As such, consolidated FFO isn’t shown while consolidated revenue is $5,038 million:

2023 reconciliation (4Q23 supplemental)

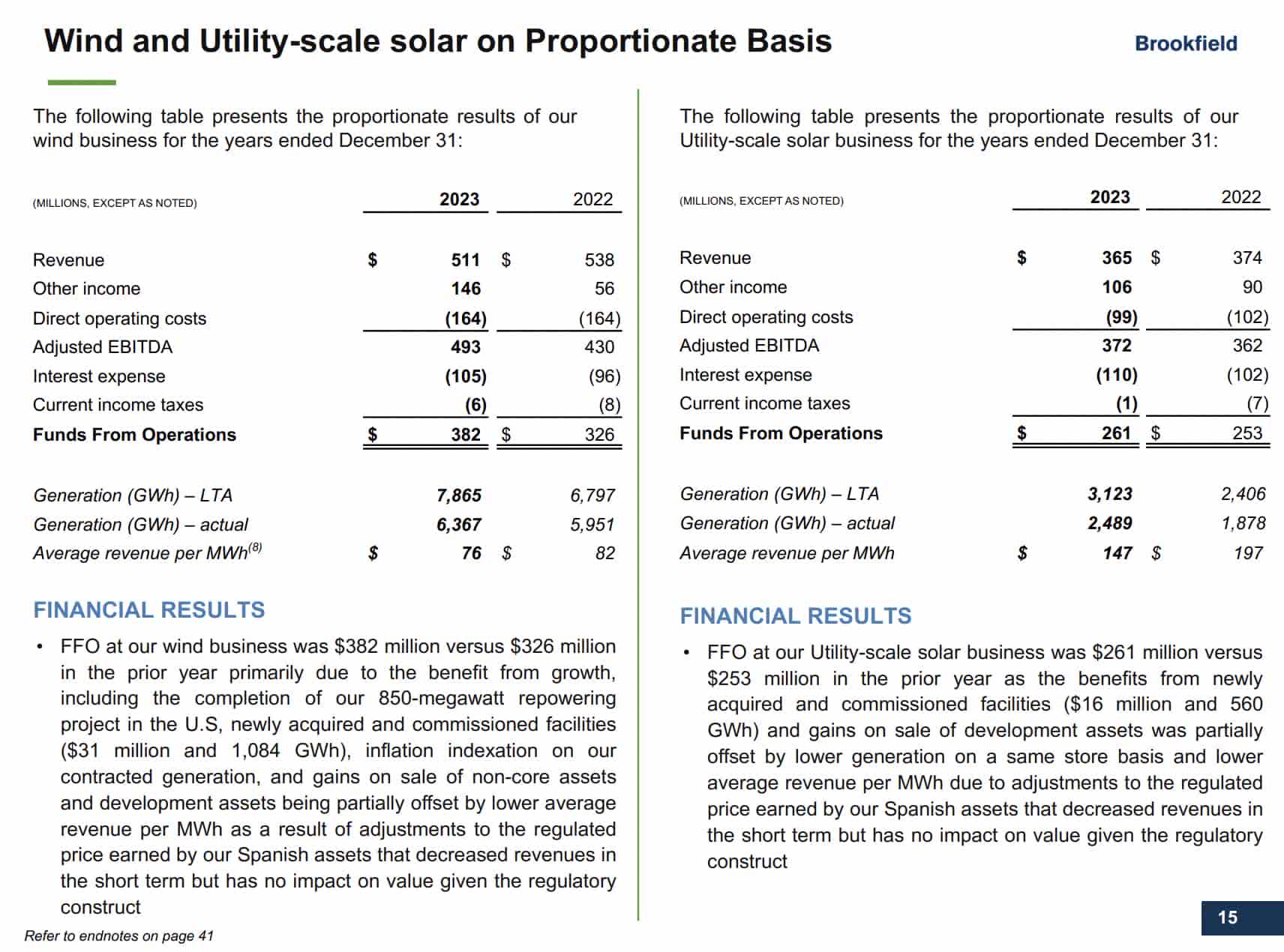

Per the 4Q23 supplemental, Brookfield had 2023 utility-scale solar revenue of $365 million on 2,489,000 proportionate MWh such that the average revenue per MWh was $147. The 4Q23 supplemental says the average revenue per MWh for wind in 2023 was $76 when adjusted to net the impact of power purchases:

solar and wind (4Q23 supplemental)

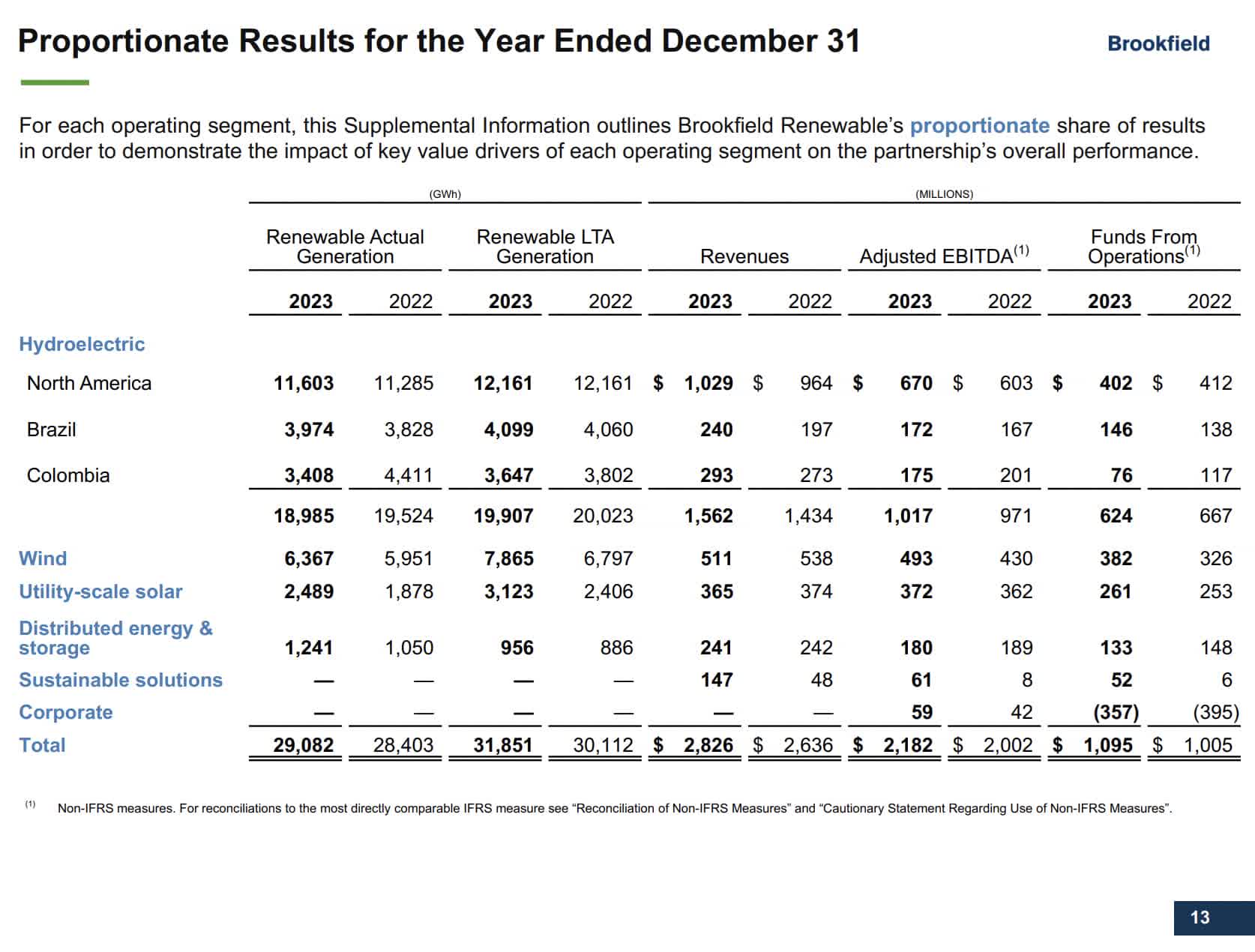

Looking at proportionate results, hydro is still the heavy hitter with FFO of $624 million on revenue of $1,524 million from generation of 18,985 GWh but this Microsoft deal is the type of consideration which will change everything:

proportionate segments (4Q23 supplemental)

If most of this deal ends up being proportionate and our solar/wind GWh generation estimates above are accurate enough to hit the side of a barn then the financial implications are tremendous. 17,500,000 MWh of solar times $147 revenue per MWh could mean solar revenue of more than $2.5 billion. 8,000,000 MWh of wind times $76 could mean wind revenue of more than $600 million. Additionally, both solar and wind have shown nice FFO margins historically and I expect this to continue moving forward.

The deal is huge in and of itself but it also shows Brookfield is uniquely positioned for similar deals with other data center companies per comments from CEO Connor Teskey in the 1Q24 call (emphasis added):

While this partnership is a first of its kind, given the significant scale of investment required to meet the increase in energy demand, we believe we are uniquely positioned to be a key enabler of growth for the largest technology players through similar arrangements.

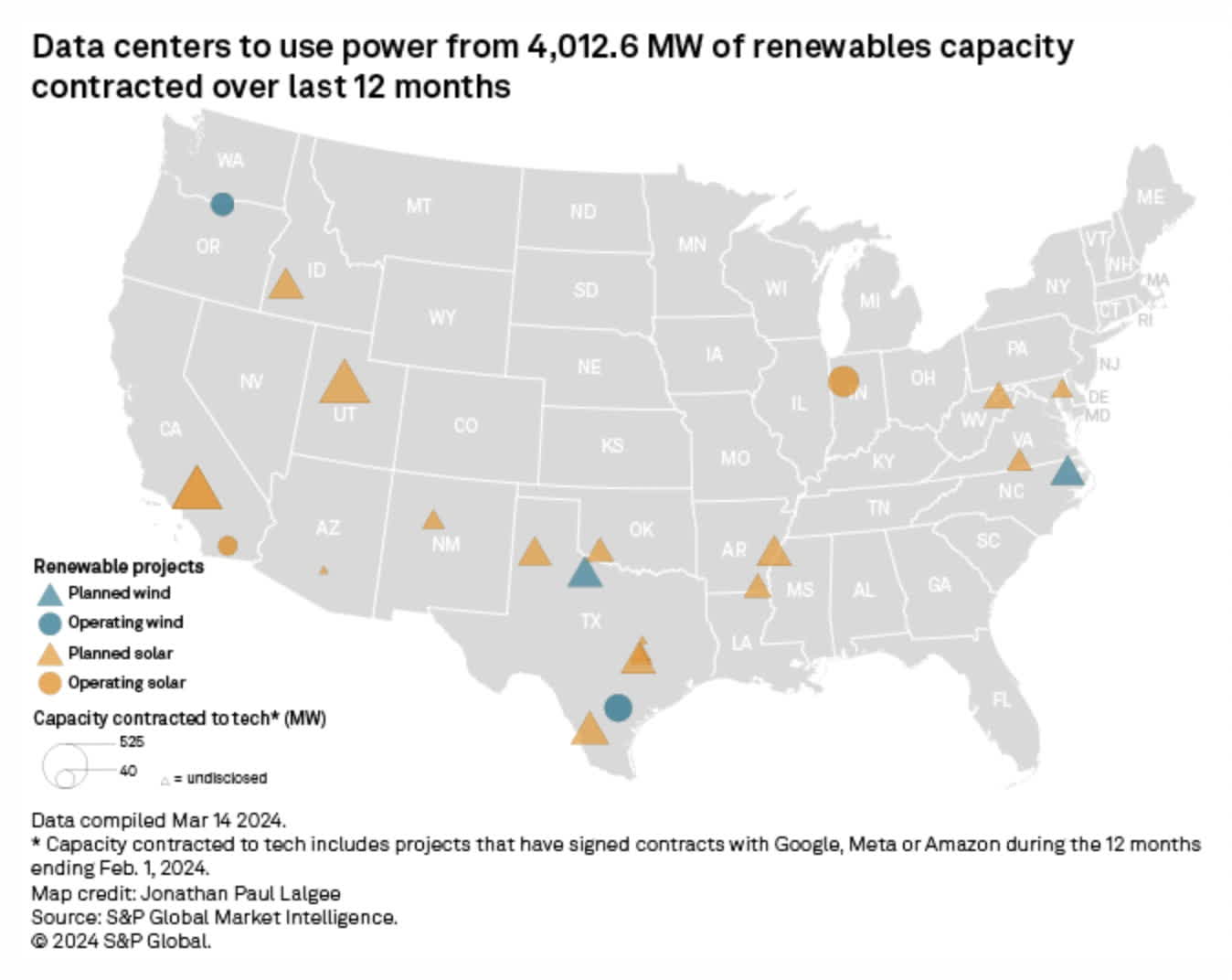

The prospects for Brookfield are enticing given recent developments. Canary Media says Arizona recently added its biggest grid battery to date for a Google (GOOGL) (GOOG) data center. A March 2024 S&P Global article says datacenter hyperscalers secured over 4,000 MW of renewable capacity in the 12 months ending February 1st. Amazon (AMZN), Meta (META) and Google were cited for these 24 projects::

planned data centers (S&P Global)

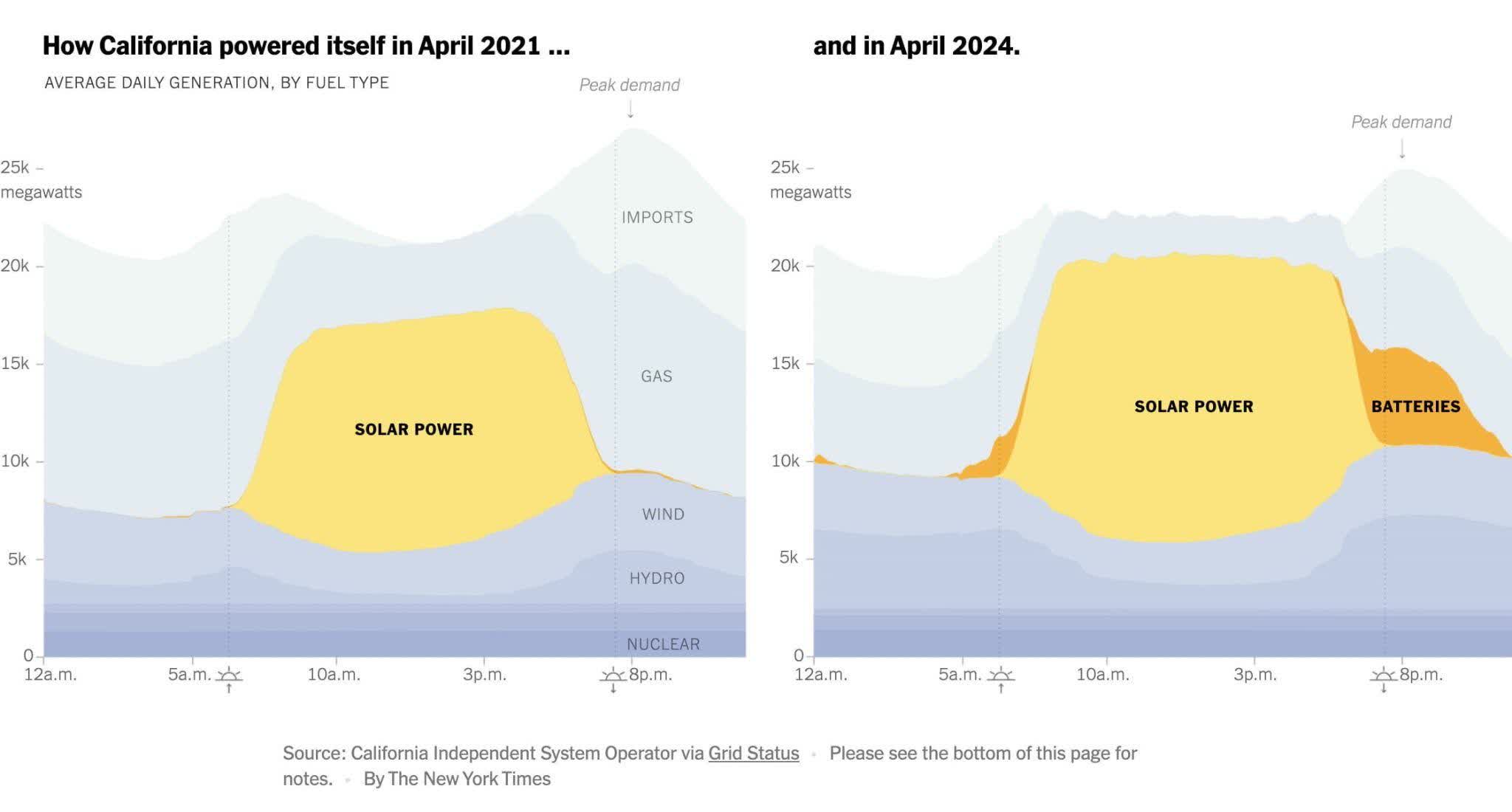

The increased use of solar and wind is happening across the country and Brookfield is a leader in this area. Per the NY Times, California has changed substantially since 2021 as the state now powers itself more with solar and batteries and less with natural gas:

California power (NY Times)

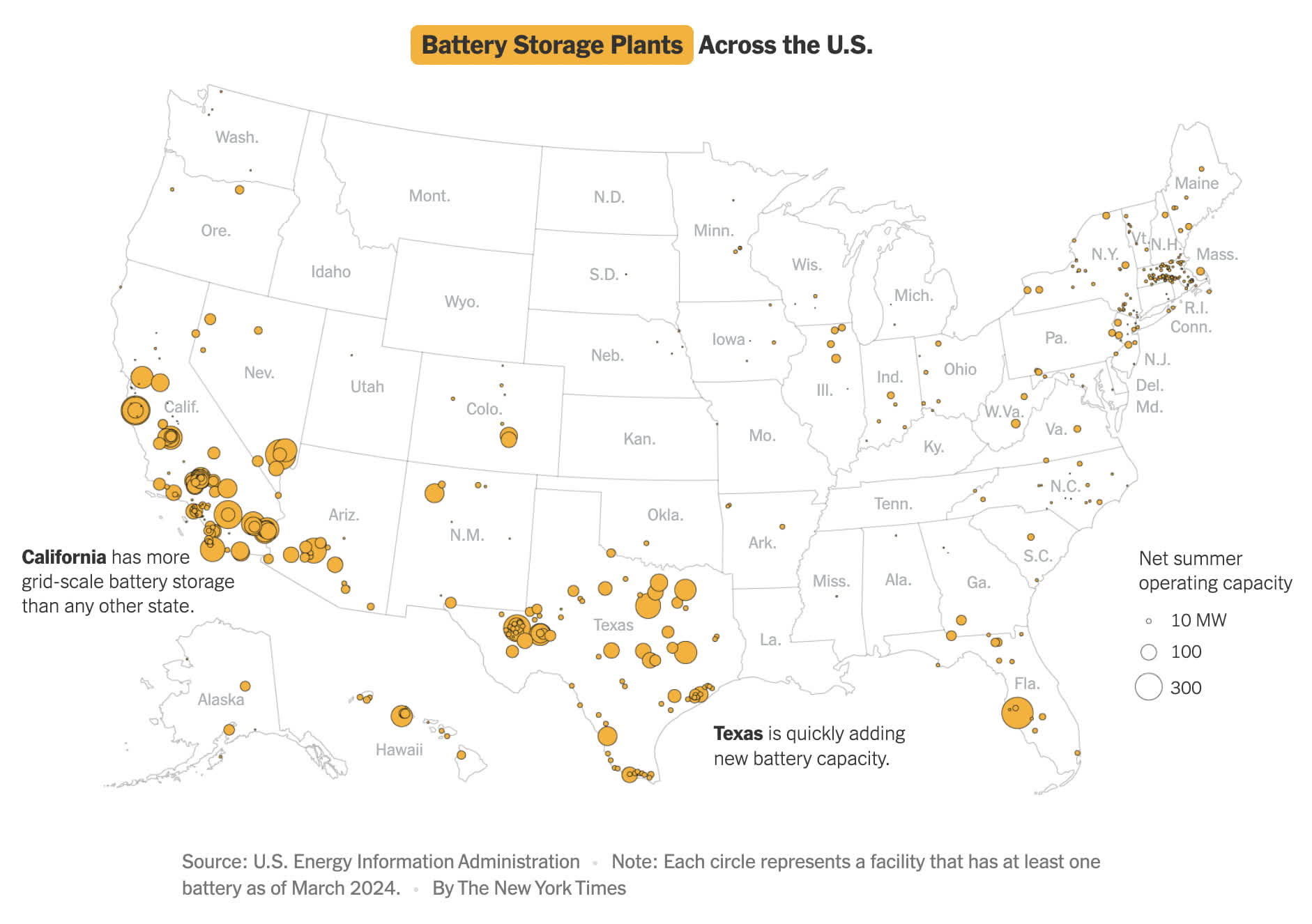

Per the New York Times, California and Texas lead the way with battery storage but other states are on the move and this map will continually change as Brookfield and others provide more solar/battery combinations for hyperscale cloud companies:

US battery plants (NY Times)

There is risk inherent with a deal of this size; it could face significant challenges, but I think this is unlikely given Brookfield’s track record and Microsoft’s insatiable demand for renewable electricity generation.

BEPC was $23.11 per share on April 30th, the day before this Microsoft deal was announced. By May 9th it reached a price above $30 per share. Today it is close to the May 9th level and I believe it is a hold. The deal makes Brookfield Renewable significantly more valuable but the stock price has risen prodigiously as well to reflect the new economics.

US investors should be careful about the K-1 implications with BEP and consider looking at BEPC as an alternative.

Disclaimer: Any material in this article should not be relied on as a formal investment recommendation. Never buy a stock without doing your own thorough research.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.