Prada: Stand Out Luxury Stock (Rating Upgrade)

Summary

- In a slowing luxury market, Prada stands out for its double-digit revenue growth and rising net margins.

- It's little wonder then that it's trading at a premium compared to other luxury stocks, and there can be justification for an even higher premium.

- If it maintains its current performance, the stock has good prospects for the rest of 2024 and its ability to grow in challenging times also makes it a long-term buy.

resulmuslu/iStock Editorial via Getty Images

Since the last time I wrote about the luxury fashion stock Prada (OTCPK:PRDSF) (OTCPK:PRDSY) in November last year, its price is up by 35% and the total returns are even bigger at 37%. This is an impressive increase, and in stark contrast with my Sell rating on it at the time, which was based on slowing down in its sales growth, compounded with the likelihood of a slowdown in the luxury sector and its elevated market multiples compared with peers.

Rise in luxury stocks and company level developments

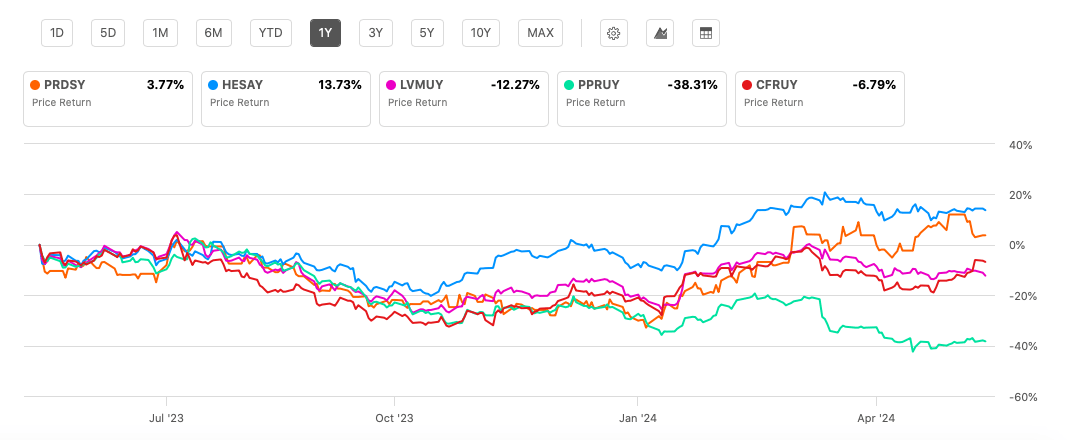

Until early January, this appeared to be investor thinking as well, as the stock was down by almost 10% from November. However, a pickup in the luxury stocks after that was also beneficial for Prada (see chart below).

Company specific developments have further reinforced its price uptick, setting Prada apart from its peers. Here are three financial developments that stand out for the company now.

Price Returns, Top 5 Luxury Stocks (By Market Capitalisation) (Source: Seeking Alpha)

#1. Robust revenue growth

When I last checked, numbers were available up to the first nine months of the year (9m 2023). While the net revenue growth for the period wasn't the worst at 12.4% year-on-year (YoY) in reported terms, the number had dramatically slowed down to 3.4% in the third quarter (Q3 2023) on weakness across its key markets. The US was a particular downer, with a continued contraction in sales.

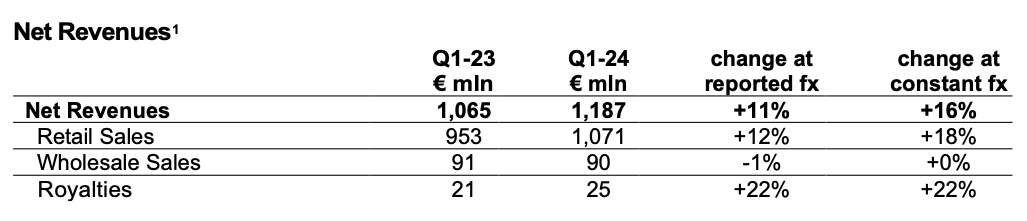

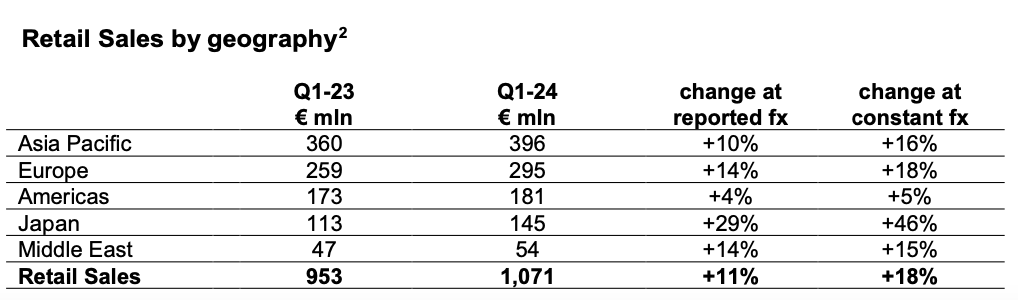

However, the risk of an extended drag didn’t materialise as the company’s full year 2023 sales grew by 13% at current exchange rates. At constant exchange rates, they grew by 17%, same as that for 9m 2023, as Prada saw an 18.1% growth in Q4 2023. Similarly, in Q1 2024, growth rates have corrected only a bit as the Asia Pacific and European have been supportive and the Americas have seen some uptick as well (see Table 1 and 2 below). In other words, despite signs of initial risks, the luxury market slowdown hasn't really impacted the company.

Source: Prada

Source: Prada

#2. Racing ahead of peers

As a result, Prada stands out among luxury stocks. Among the biggest five luxury stocks by market capitalisation, Hermès (OTCPK:HESAY) is the only other one to maintain double digit growth, with sales growing by 13% YoY in Q1 2024 at current exchange rates and 17% at constant exchange rates.

By contrast, LVMH (OTCPK:LVMUY) saw a revenue contraction in Q1 2024 of 2% in reported terms and even organic growth at constant exchange rates was just 3%. Similarly, Cartier owner Richemont (OTCPK:CFRUY), whose financial year ended on March 31, 2024, saw a sales contraction of 1% at actual exchange rates in Q4 FY24 and only 2% growth at constant exchange rates. The worst performing of the lot, however, was Gucci owner Kering (OTCPK:PPRUY), which saw a 11% drop in reported revenues in Q1 2024 and a 10% decline in comparable terms.

The key point here is that Prada’s superior growth, which could earlier be chalked up to the luxury market upswing is no longer so, but reflects its edge over its peers. This in turn can justify its relatively higher market multiples that are discussed later here.

#3. Exceptional profit increase

Finally, the company’s profits have seen robust growth. When I last wrote about Prada, I had expected a solid 23% net profit growth in 2023. In actual fact, it far surpassed the figure, with a 44.2% increase instead. Its net margin also jumped to 14.2% compared with 11.1% in 2023. Incidentally, this was one factor I had pointed, which could continue to buoy the stock.

My projections, however, were based on expectations of continued weakening in demand in Q4 2023. Clearly though, that wasn’t the case. Further, both cost of goods sold and operating expenses grew at a slower rate than revenues, at 4% and 11.1% respectively, resulting in improved profits, right from the level of the gross margin.

Outlook and market multiples

If the company sustains its revenue growth rate at current exchange rates for the full year 2024 and the net margin stays constant at the level seen in 2023, the net income would come in at EUR 748 million (USD 808 million). This results in a forward price-to-earnings (P/E) ratio of 24.4x. The figure is actually slightly lower than the 24.9x level the last I checked, and it isn’t too bad compared with peers either.

It’s still way behind Hermès at 49.87x, which always trades at a significant premium to luxury stocks in any case. But it’s not much farther ahead than LVMH at 23.46x, Richemont at 20.47x and even Kering at 21.89x considering its superior performance. The average forward P/E of these stocks is 28x, indicating a 15% upside to the stock. Normally, I would exclude Hermès from the average since it's an outlier, but an exception is made here because Prada is showing similar characteristics in terms of both a better performance than other stocks and also a relatively higher P/E.

Another way to assess if there’s actually upside to Prada, is to consider its long-term forward P/E. For the past decade, it averages 32.1x, which is also higher than the current levels, reflecting an even bigger 30% upside to the stock.

Besides this, the dividends are worth considering too. While the stock’s forward yield of 1.87% isn’t eye-catching, this is due to the price rise it has seen. The 5-year yield on cost is actually a healthy 5%.

What next?

All-in-all, Prada looks really good right now. It has stood out in recent months with its superior performance compared with peers. The company’s impressive net income growth in 2023 is also hard to miss. Its performance is now comparable only with Hermès, which has historically traded at a far higher P/E than other luxury stocks. While the extent of Prada’s premium isn’t as high, there is certainly a case for it having one. If it can continue to maintain its growth rates and high income levels, the stock is a good buy even for now.

The bigger point of the Prada story, though, is about the long-term too. It has managed to show its mettle so far in the luxury market slowdown, indicating that it can show an edge even in challenging times. Its CAGR for revenues at 8.6% and 26.7% for net income over the past five years further underlines its strength, making it a buy for the long-term, even if it does see a wobble in the near term. I’m upgrading Prada to Buy based on the likelihood of long-term capital gains as well as passive income from it.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.