UiPath: Harbinger Of Things To Come

Summary

- UiPath's Q1 results were reasonable, but soft guidance and the CEO's resignation caused the stock to decline.

- Weakness in the macro environment and execution issues were cited as reasons for the company's performance.

- While UiPath appears undervalued, the company still needs to demonstrate that its business will not be disrupted by generative AI.

- UiPath's GAAP profitability will likely need to improve before its valuation really begins to matter. In the meantime, UiPath is well positioned to support the share price through buybacks.

everythingpossible/iStock via Getty Images

UiPath's (NYSE:PATH) Q1 results were reasonable, but soft guidance and the sudden resignation of the CEO sent the stock spiraling lower after earnings. Weakness was attributed to the macro environment, although the company also highlighted execution issues. This is not that surprising given that expectations for looser financial conditions have shifted dramatically in recent months on the back of sticky inflation.

I previously suggested that while UiPath's valuation appeared low, investor skepticism of the business would likely prevent the stock from moving higher. I didn't expect such soft guidance from UiPath though, which has fed into uncertainty regarding the impact of AI on the RPA category.

UiPath’s narrative is weak at the moment due to LLMs and rapid changes in the capabilities of AI. While the company continues to embed generative AI capabilities in its products, many of these efforts are still nascent. UiPath’s valuation was reasonable going into earnings, but its growth is modest, and the company still isn’t profitable on a GAAP basis. It is not really clear where the stock will find a floor, but UiPath is cash flow positive and has a sizeable cash balance which can be directed towards buybacks.

There is a broader problem in tech where many companies are making large investments that appear unlikely to generate sufficient returns and this hasn’t been priced into the market yet. While the macro environment is not helping, this really comes down to product cost and the customer value proposition. I significantly reduced my exposure to software earlier in the year, given that valuations had moved higher despite continued deterioration in financial performance for most companies. UiPath, Salesforce and Workday are all examples of the difficulties many companies will face in coming quarters.

Market Conditions

UiPath suggested that its business began to slow in the second half of March and into April, which was attributed to macro conditions. Deal scrutiny has reportedly increased, and sales cycles have lengthened as a result, with several large expansion opportunities closing at a reduced size or pushing out of the first quarter. This behavior is broad-based but is most pronounced amongst smaller mid-market customers. Macro weakness is expected to persist going forward, helping to explain UiPath’s soft guidance for the remainder of the year.

UiPath doesn’t believe that this is the result of competitive pressure though, stating that its win rate remains strong and is consistent with what the company has seen historically. While UiPath continues to believe that AI and generative AI are tailwinds, there does seem to be some headwinds, as customers try to understand which tasks they can automate with AI and which tasks are better suited to UiPath’s platform.

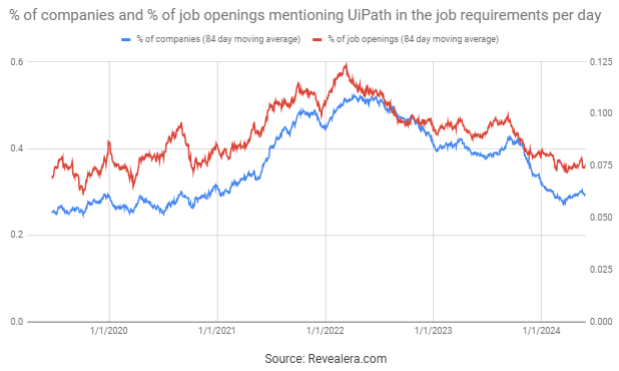

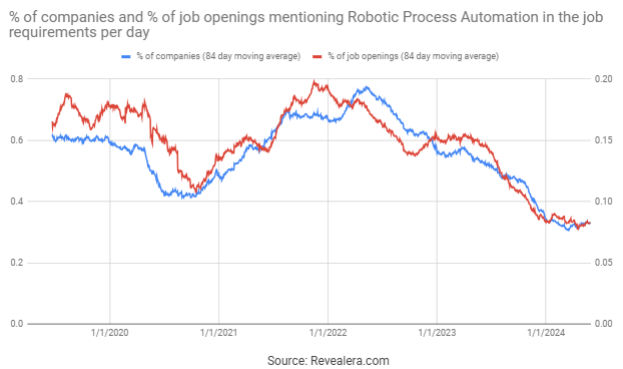

UiPath job openings have fallen off meaningfully in recent months, which may have been a warning of deterioration in the company’s fundamentals. This isn’t really backed up by the number of job openings mentioning UiPath in the job requirements, which have been fairly steady in 2024. Robotic process automation as a category has been under pressure over the past few years though.

Figure 1: UiPath Job Openings (source: Revealera.com)

Figure 2: Job Openings Mentioning UiPath in the Job Requirements (source: Revealera.com)

Figure 3: Job Openings Mentioning Robotic Process Automation in the Job Requirements (source: Revealera.com)

UiPath Business Updates

While UiPath beat on revenue and earnings in Q1, guidance was extremely soft, and this, coupled with the resignation of the CEO suggest serious issues. The reason for the resignation may be benign, but its sudden nature and UiPath’s weak guidance are not a good look.

While UiPath has been hit by macro headwinds, the company has also noted execution issues, including contract execution challenges on large deals and certain sales compensation changes. UiPath recently reduced incentives for multi-year deals, which may have overly impacted the company due to ASC606 accounting and the importance of on-prem software to UiPath's business. UiPath’s recent growth investments have also fallen short of expectations. The company has proposed generic changes around increasing customer focus and improving efficiency, but there is little that inspires confidence. The primary short-term change appears to be a change in sales comp to incentivize multi-year deals.

From a product perspective, UiPath is focused on leveraging AI to increase the capabilities of its platform and address more use cases. The company has stated it is happy with the progress of its AI products and will continue to invest in this area despite the cost. Given UiPath's decelerating ARR growth and the inability of the company to expand its customer base in recent quarters, it is difficult to see any AI tailwind though.

UiPath's AI ambitions are illustrated by its investment in Holistic, a company founded by leading AI researchers. Holistic is developing foundation models and eventually wants to achieve artificial general intelligence. UiPath is also collaborating with Holistic, which appears to be based around AI agents.

Intelligent Document Processing and Test Automation are reportedly bright spots at the moment. UiPath recently introduced Context Grounding, a new feature within UiPath's AI Trust Layer that helps to improve the accuracy of GenAI models. This is presumably some sort of RAG type feature. UiPath also recently announced the release of Autopilot for developers and testers into general availability.

UiPath recently achieved FedRAMP authorization, which should boost the company's cloud business going forward. There is already customer interest, with UiPath closing several deals in Q1. UiPath also recently announced an expansion of its partnership with Microsoft, including an integration with Copilot for Microsoft 365.

Financial Analysis

UiPath generated approximately 335 million USD revenue in Q1, an increase of 15.7% YoY. Some of this weakness appears to have been the result of multi-year deals and the relatively large contribution of on-prem software to the business, with UiPath's license revenue only up around 4% YoY. UiPath’s ARR totaled 1,508 million USD in Q1, up 21% YoY. While net new ARR was soft, this probably indicates that UiPath's results weren't as bad as they appeared on the surface. UiPath expects 300-305 million USD revenue in Q2, an increase of only 5.3% YoY at the midpoint. ARR is expected to be 1,543-1,548 million USD, up 18% YoY.

Figure 4: UiPath Revenue Growth (source: Created by author using data from UiPath)

UiPath's current situation is perhaps best highlighted by its customer base, which has been relatively stagnant over the past 6 quarters. UiPath's dollar-based gross retention was 98% in Q1, indicating that churn is not a significant problem. The company's net retention rate was 118%, illustrating that UiPath is still driving expansion within existing customers. As a result, UiPath's larger customer count continues to increase at a healthy pace, with the number of customers with ARR in excess of 1 million USD increasing 20% YoY.

Figure 5: UiPath Customers (source: Created by author using data from UiPath)

UiPath's GAAP operating loss was 49 million USD in the first quarter, inclusive of 89 million USD of stock-based compensation expense. The company remains near operating breakeven though and is generating significant free cash flow. With growth softening in coming quarters, UiPath's margins are likely to come under pressure. The company's high gross profit margins and low churn should see the company transition to profitability in coming years though.

Figure 6: UiPath Operating Profit Margin (source: Created by author using data from UiPath)

Conclusion

UiPath's current share price is likely to prove an attractive entry point in time, but the company has obstacles to navigate in the near term. I don't think the exit of the CEO is an issue, outside of the negative signal it sends about the company's prospects. More importantly, UiPath still needs to demonstrate it can maintain its relevance in the face of AI and that Microsoft is not a threat.

UiPath's valuation will eventually matter but this may require the company's profit margins to improve so that it is reasonably priced based on earnings. In the meantime, UiPath has 1.9 billion USD in cash, cash equivalents and marketable securities, no debt and expects to generate 300 million USD free cash flow in 2024. This is beginning to look substantial relative to UiPath's roughly 7.5 billion USD market capitalization.

Figure 7: UiPath Relative Valuation (source: Created by author using data from Seeking Alpha)

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

- YNWIM·05-31Great analysis on UiPath's Q1 results and future prospects.LikeReport