ConocoPhillips Knocks It Out Of The Park With Purchase Of Marathon Oil

Summary

- Marathon Oil Corporation shares closed up 8.4% after the announcement of its acquisition by ConocoPhillips in a $22.5 billion all-stock deal.

- The transaction values Marathon Oil appropriately compared to similar companies, but the energy space as a whole appears undervalued.

- ConocoPhillips will gain significant assets in Equatorial Guinea and expects to generate $500 million in annual synergies from the acquisition.

- The terms of the deal make ConocoPhillips a big winner, though investors may want to consider a stake in Marathon Oil as well.

mtcurado

May 29th was a very good day for shareholders of Marathon Oil Corporation (NYSE:MRO). Shares of the company closed up 8.4% after news broke that the business would be acquired by energy giant ConocoPhillips (NYSE:COP) in an all-stock transaction, valuing the firm at $22.5 billion on an enterprise value basis. This nice bit of upside is certain to make investors happy. But to many, the long-term picture might be disappointing. Relative to similar companies, this transaction does value Marathon Oil appropriately. However, the space as a whole does look moderately undervalued.

At the end of the day, this move might leave some investors with a bad taste in their mouths because it might be perceived as leaving value on the table. But it is undeniable that ConocoPhillips is walking away with a pretty good outcome. And this is without factoring in the $500 million, or more, of annualized synergies that management expects from the transaction. In addition to this, ConocoPhillips announced that it is boosting its dividend rather significantly.

When you add all of this together, I find every reason in the world to be optimistic about the conglomerate. And because of the all stock structure of the deal, buying Marathon Oil makes even more sense, since buying it today is more or less the same as picking up its acquirer discounted. Because of this, I believe that both companies warrant a solid "buy" rating at this time.

Another mega deal

The last two years have seen a number of major transactions in the energy space. Earlier this year, for instance, Exxon Mobil (XOM) completed its purchase of Pioneer Natural Resources in a transaction initially valued at $64.5 billion on an enterprise value basis. And just the other day, shareholders of Hess Corporation (HES) voted in favor of the company being acquired by Chevron (CVX) at an enterprise value of $60 billion (though that deal is still facing challenges). This is just a sample of the multibillion dollar transactions going on in the U.S. energy market.

Author

Not to be left out of the picture, it is clear now that ConocoPhillips has decided to strike. And frankly, this move makes a lot of sense. According to the terms of the agreement, shareholders of Marathon Oil will receive 0.2550 of a share of ConocoPhillips for each share of Marathon Oil that they currently own. This translates to an enterprise value of roughly $22.5 billion that includes $5.4 billion worth of net debt. Stripping this out, we end up with an equity value of $17.1 billion.

ConocoPhillips

Strategically, this transaction is incredibly logical. As you can tell from the image above, the two firms have a great deal of overlap across major oil and gas producing regions here in the U.S. This is especially true of the prolific Eagle Ford, where the two companies control a combined 490,000 net acres. This acreage is responsible for producing around 380,000 boe (barrels of oil equivalent) per day of oil and gas. There's also the Bakken, which involves around 800,000 net acres of land and that is responsible for 220,000 boe per day of production between the two companies. Then there is the Delaware Basin, which is in the famous Permian Basin.

The two companies will control a combined 800,000 net acres that will produce 580,000 boe per day. Add on top of this other assets that the firms control, like the 1 million net acres that ConocoPhillips controls in Alaska and the 50,000 boe of oil, natural gas, and NGLs that Marathon Oil gets from the STACK/SCOOP in Oklahoma, and it's not difficult to see that the result is a true behemoth in the U.S. energy market.

Although the management team at ConocoPhillips is playing up the role that these overlapping assets will play in value creation for investors, I would argue that one of the most attractive aspects of this transaction would be the assets that ConocoPhillips will come to control in Equatorial Guinea as a result of this move.

In an article published on May 17th of this year, I went into depth regarding these operations and how much value they could result in for shareholders eventually. My goal is not to rehash those details here. Instead, I recommend that you read that article. Having said that, for this year alone, Marathon Oil estimated that EBITDAX from the firm's Equatorial Guinea assets would be between $550 million and $600 million, with the equity affiliate portion of this coming in at between $200 million and $250 million. And over the span of five years, the company expects EBITDAX of between $2.5 billion and $3.5 billion from those operations.

ConocoPhillips

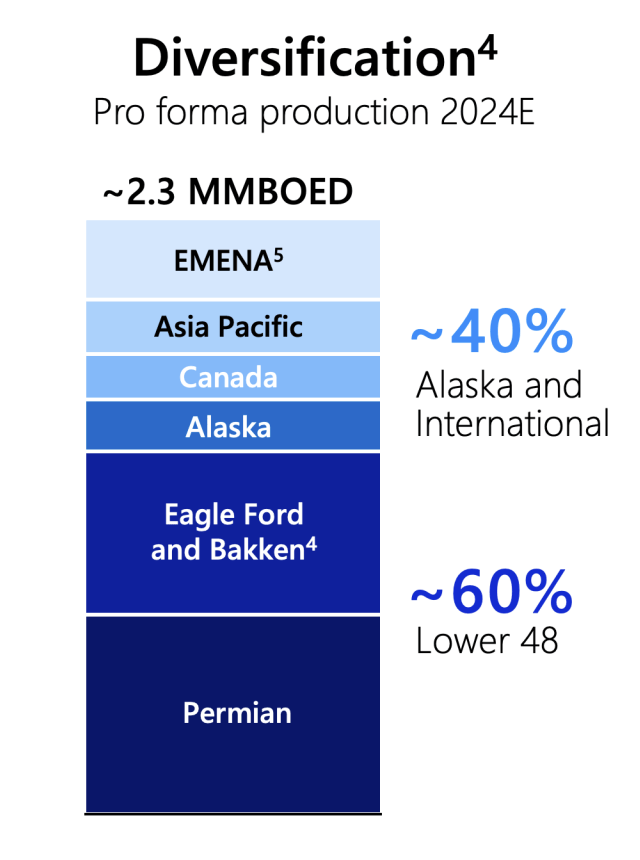

The end result of this will be one of the largest oil and gas companies on the planet. Around 60% of the pro forma production of the company will come from the Lower 48 states. The remaining 40% of the 2.3 million boe per day of output will involve Alaska, Canada, the Asia Pacific region, and all other international operations like Equatorial Guinea. And what should be really exciting for investors of ConocoPhillips is that this will result in over 2 billion boe of resources, with an average cost of supply for WTI crude of less than $30 per barrel coming over to the energy giant.

ConocoPhillips

If everything goes according to plan, ConocoPhillips expects to generate at least $500 million worth of synergies on an annualized basis within a year of closing on this purchase. Around $250 million of this is expected to come from general and administrative costs. Cutting out duplicative operations, including those at corporate, will certainly play a role in this cost savings. Another $150 million worth of savings on a run rate basis will come from operating costs and commercial optimization activities. This includes consolidating field operations. And then you have what management calls capital optimization that should save around $100 million annually. According to management, a lot of this will involve reducing drilling and completion costs.

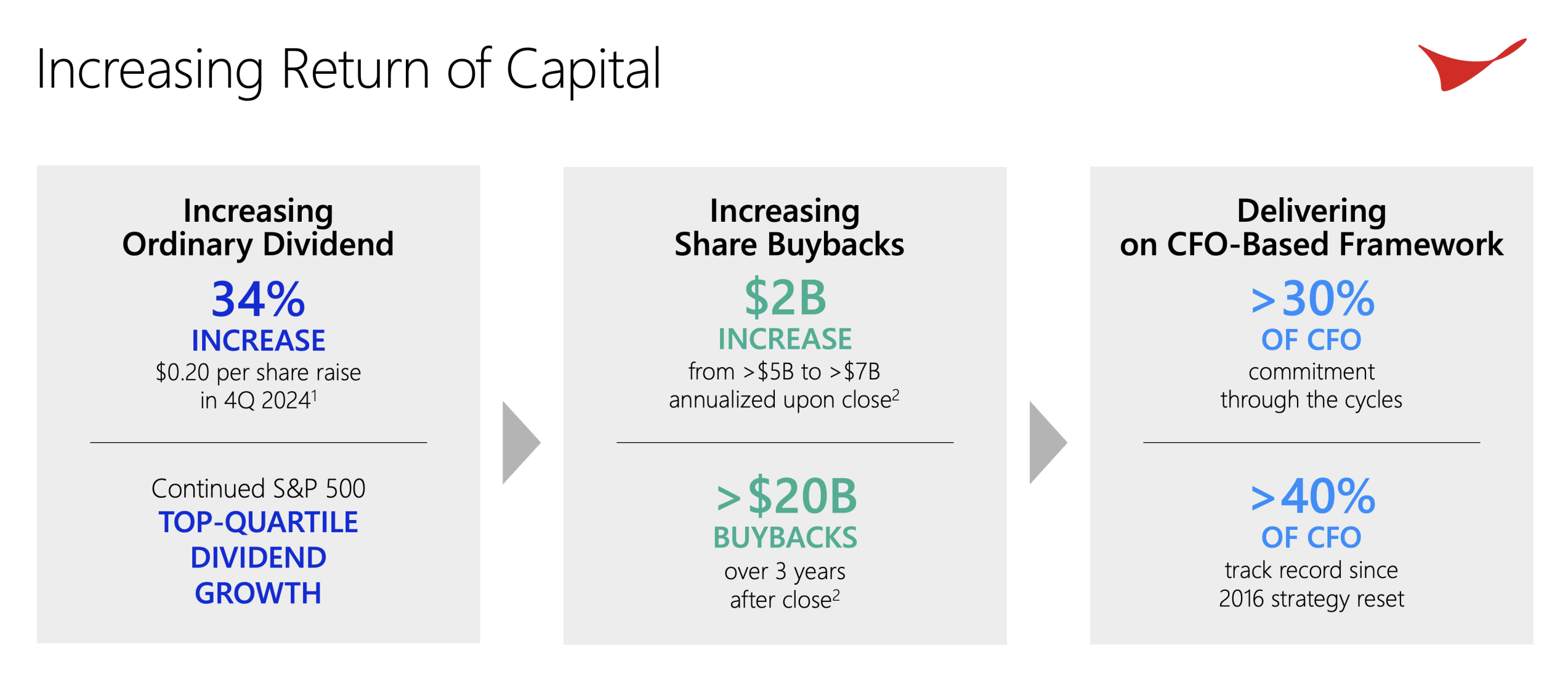

These savings, combined with about $2 billion of planned asset sales, will empower ConocoPhillips to supercharge its return of capital to shareholders. Previously, management had planned to buy back around $5 billion or more worth of shares each year. That number has now been increased to more than $7 billion annually. Of course, that will only be after the transaction closes. Over the span of three years following the close of the deal, it's expected that the company will buy back over $20 billion worth of stock.

But that's not all. In addition to this, management has decided, effective in the final quarter of this year and irrespective of whether this deal is completed or not, that ConocoPhillips will boost its quarterly dividend by 34%. That's an increase of $0.20 per share each quarter. Although I don't care much about dividends, many investors do. So this should be viewed in a very positive light by them.

ConocoPhillips

In response to this transaction, shares of ConocoPhillips pulled back by 3.1% on May 29th. This is pretty common when major deals are announced. This is because the market believes that the premium paid for the firm in question should be a net negative for the acquiring company. I view this, at least in this case, as an irrational move lower. Even ignoring the potential synergies that management is forecasting, this transaction looks to be favorable for investors in ConocoPhillips.

Author - SEC EDGAR Data

Using historical results from 2023 and using the forecasted results for 2024 that I calculated in my prior article on Marathon Oil, you can see in the chart above how shares are priced. That same chart also has the valuation of ConocoPhillips using results from last year. In essence, ConocoPhillips is trading it's slightly more expensive stock for the cheaper stock of Marathon Oil. If anything, shares of both companies deserved to increase in response to this development. In the table below, I also demonstrated how this purchase seems to be appropriate relative to other firms in the space. On a price to earnings basis and on an EV to EBITDA basis, two of the five companies that I compared Marathon Oil to ended up being cheaper than it. This number increases to three of the five when using the price to operating cash flow approach.

| Company | Price / Earnings | Price / Operating Cash Flow | EV / EBITDA |

| Marathon Oil Corporation | 11.0 | 4.1 | 5.2 |

| APA Corporation (APA) | 3.2 | 2.8 | 3.8 |

| Ovintiv (OVV) | 6.8 | 3.5 | 4.1 |

| Permian Resources (PR) | 14.6 | 3.0 | 6.3 |

| EQT Corporation (EQT) | 29.5 | 6.4 | 8.5 |

| Chesapeake Energy (CHK) | 12.0 | 6.2 | 4.3 |

Even though I believe that ConocoPhillips is picking up Marathon Oil for a good price, this is not a statement on my part that I believe that the two companies should trade at parity. With a net leverage ratio of 1.25, Marathon Oil is more heavily levered compared to ConocoPhillips, with its net leverage ratio of 0.50. But as the chart below illustrates, this acquisition will only increase the net leverage ratio of ConocoPhillips modestly to 0.61. That's barely a change at all in the grand scheme of things.

Author - SEC EDGAR Data

At the end of the day, acquiring stock in Marathon Oil is essentially buying ConocoPhillips discounted in any scenario other than the transaction between the two companies failing. This is because, even after their share price movements on May 29th in response to this deal, there is still a 2.5% spread between the price at which Marathon Oil is trading and the price at which it is being purchased given where shares of ConocoPhillips closed out for the day.

There is also a small chance of further upside for investors in the company. This is because, after the deal was announced, news broke that Devon Energy (DVN) could step in to make an offer for Marathon Oil. While this is purely speculative, it was reported in October of last year that Devon Energy was considering making a major acquisition in the hopes of expanding its U.S. shale operations. The company even reportedly held preliminary talks with Marathon Oil because of the complementary assets that they have. Shares of Devon Energy even closed down 3.5% on May 29th, almost as though investors were assigning a fairly high probability of this turning into a bidding war. If this came to pass, the upside could be quite attractive. But investors shouldn't bank on it occurring.

Takeaway

All things considered, I believe that the acquisition of Marathon Oil by ConocoPhillips is a big win for the latter. Even if synergies are not realized, there's a lot of value here for investors to benefit from. Add on top of this the decision to increase share buybacks and the distribution rather considerably, and I see no reason to be anything other than optimistic if you own shares of ConocoPhillips.

As for Marathon Oil shareholders, I think the picture is a bit more complicated. If I were an investor, I would feel as though I didn't get the fair value needed from this transaction. Having said that, buying up Marathon Oil right now could make a lot of sense. It is essentially buying ConocoPhillips discounted in any scenario other than one in which the deal does not close. In addition to this, there is some small probability that a bidding war could break out over Marathon Oil that could push shares even higher. Because of these factors, I believe that both companies warrant a "Buy" rating at this time.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.