Citigroup: Bold Turnaround Efforts Paying Off, Strong EPS Growth Expected

Summary

- Citigroup has outperformed the S&P 500 by nearly 25 percentage points since late last year as positive sentiment surrounds the once-boring big bank stock.

- The company is undergoing cost-cutting initiatives and seeking better capital market opportunities under CEO Jane Fraser, which appear to be paying off given 20%+ EPS growth expected next year.

- I assert that the stock is undervalued with a high dividend yield, and earnings growth and shareholder-friendly activities could support further bullish price action.

- I highlight key price levels to watch with earnings due out next month.

VV Shots

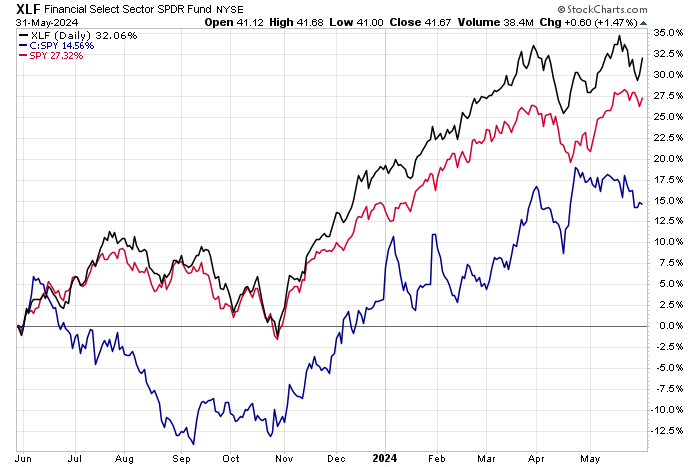

The Financials sector has been a quiet winner ever since the S&P 500 bottomed out in late October last year. Over the last 12 months, the Financials Select Sector SPDR ETF (XLF) is up 32% with dividends included, outpacing the SPX by some five percentage points.

What's interesting is that one sometimes overlooked large cap in the space, Citigroup (NYSE:C), has outperformed the S&P 500 by nearly 25 percentage points the Q4 nadir. Jamie Dimon and JPMorgan Chase (JPM), as well as Goldman Sachs (GS), garner the most attention in the banking niche. But Citi, under CEO Jane Fraser, is undergoing cost-cutting initiatives as it seeks to streamline operations while taking advantage of the potential for better capital market opportunities later this year.

I have a buy rating on the stock. I see shares as undervalued given Citi’s earnings trajectory while shareholders are rewarded with a high dividend yield.

Financials Sport Alpha Since Late 2023, Citigroup Shares Outperforming SPY

Stockcharts.com

According to Bank of America Global Research, Citigroup (C) is a leading global diversified financial service company that provides consumers, corporations, and governments with a broad range of financial products and services. The bank offers services such as consumer banking and credit, corporate and investment banking, securities brokerage, transaction services, and wealth management. Citi operates and does business in more than 160 countries/jurisdictions in North America, Latin America, Asia, and Europe/Middle East and Africa (EMEA).

At the start of the Q1 earnings season, Citi posted a solid start to the year. Q1 GAAP EPS of $1.58 beat the Wall Street consensus forecast of just $1.17 while revenue of $21.1 billion, down 2% from year-ago levels, was a significant $700 upside surprise. With many of its streamlining efforts now in the rearview mirror, earnings growth is front and center. The management team has a target of hitting 4-5% annual revenue growth with an 11-12% return on tangible common equity by 2026.

After years of lackluster dividends and little in the way of significant buybacks, I believe Citi could more aggressively pursue share repurchases over the coming quarters, which would result in a healthy total shareholder yield. Much will depend on upcoming on Citi's stress test results and the bank continuing to hit regulatory capital ratio requirements. As it stands, Citi’s CET1 ratio is 13.5%, comfortably above the industry minimum. The company may also look to divest assets, akin to what we have seen General Electric (GE) do with much success over the last few years.

Risks

Risks include challenges incorporating so many structural and strategy changes at the micro level while macro risks include an ongoing slow capital markets situation and higher regulatory costs for large money-center financial institutions.

Valuation

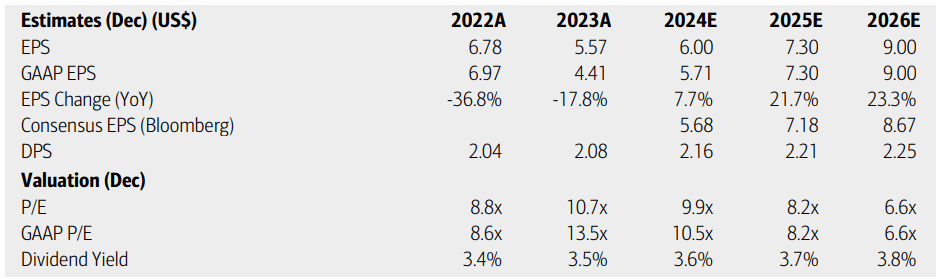

On valuation, analysts at BofA see earnings rising about 8% this year with significant EPS improvements in the out years. The current Seeking Alpha consensus numbers are about on par with what BofA projects while Citi’s top line should remain in the low to mid $80 billion range.

Dividends, meanwhile, are expected to increase modestly over the quarters to come, resulting in a yield that competes well with many of its Financials-sector peers. With the prospect of mid-single-digit earnings multiples looking out to 2026, shares remain attractively priced even after the recent rally, in my opinion.

Citigroup: Earnings, Valuation, Dividend Yield Forecasts

BofA Global Research

Given the turnaround story and 20%+ EPS growth rates expected as soon as next year, the historical 9x P/E multiple is too low in my view. If we assume $6.40 of GAAP earnings over the next four quarters, based on the current consensus outlook, and apply a sector multiple of 10.6x, then shares should trade near $68, making it undervalued. The stock also sells at a major discount to the industry average price-to-book ratio.

I see the $6.40 next-12-month EPS amount as achievable based on its forecast 4-5% revenue CAGR and as the bank refocuses its strategy in the Wealth division to help create stronger top-line revenue. Citi also continues to cut expenses while seeing 6-7% loan growth for the balance of the year. Another catalyst that could help Citi earn significant profit growth in the years ahead is a pickup in capital banking activities such as M&A, IPOs, and corporate debt underwriting. Recent high-profile hires, such as Viswas Raghavan from JPM as Head of Banking and Andy Sieg from BofA for Wealth Management, auger well for improved efficiencies in the years ahead in my view.

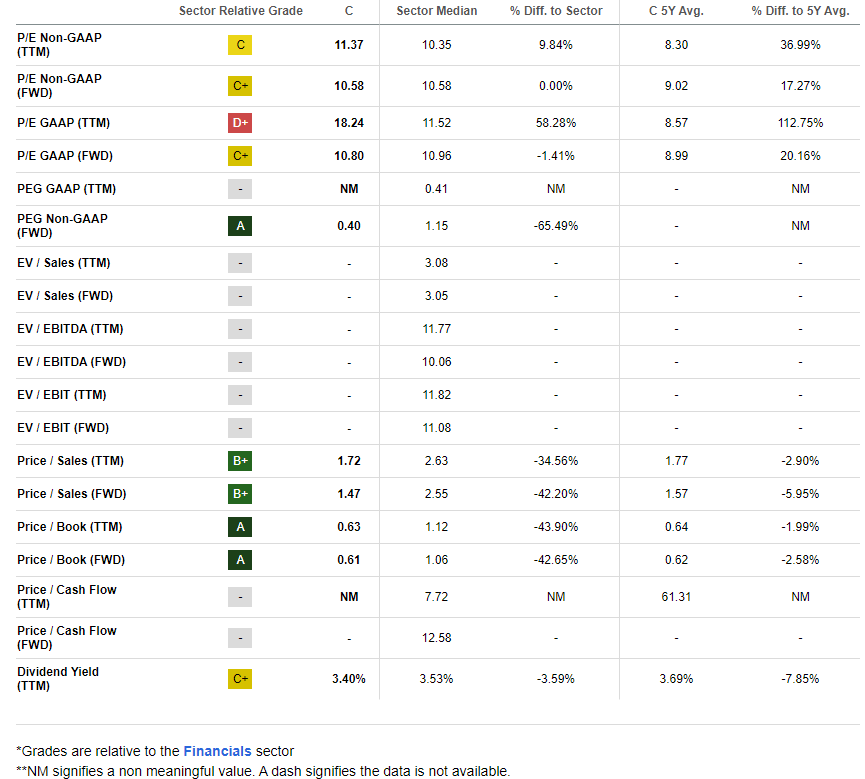

Citi: Low P/E and P/B Multiples, Solid Yield

Seeking Alpha

Compared to its peers, C sports an average valuation rating while its growth grade is stellar. Profitability readings appear weak, but traditional profitability metrics often don’t apply properly to money-center banks. Also, Citi is one of just a few companies that only reports GAAP earnings, not often-friendlier operating profits.

While there have been mixed sellside EPS revisions in the past 90 days, share-price momentum has been very stout. I will highlight key price levels on the chart later in the article.

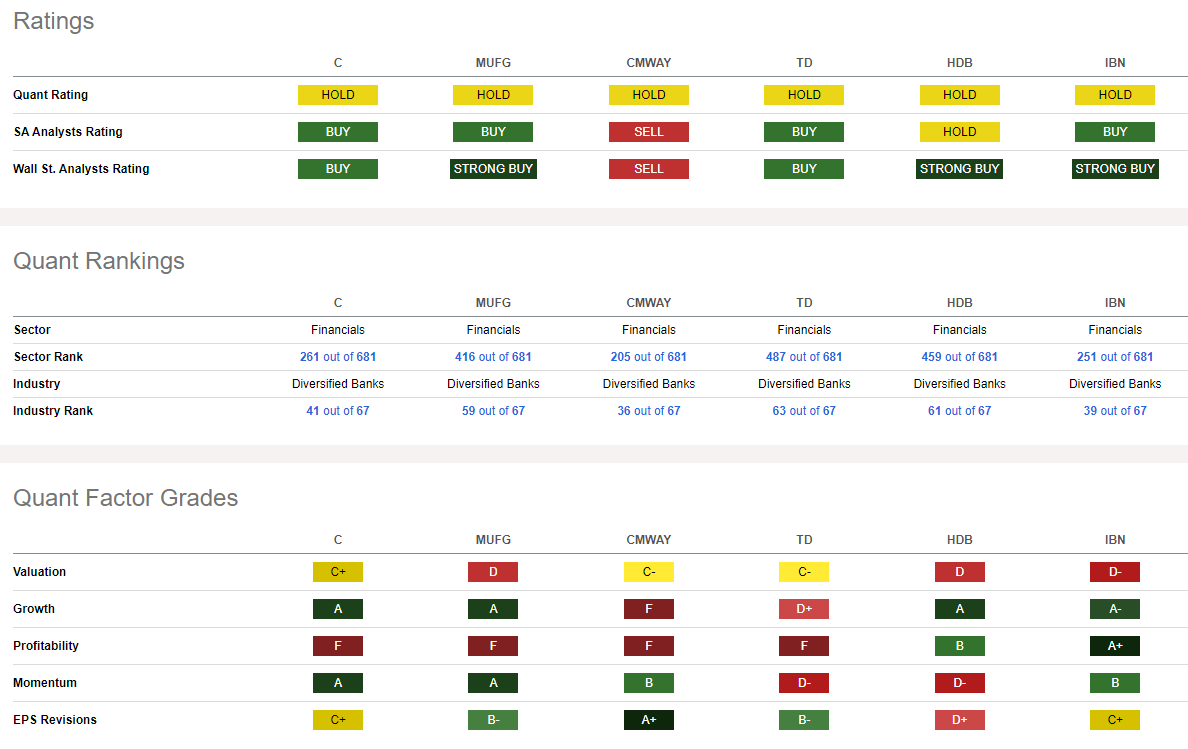

Competitor Analysis

Seeking Alpha

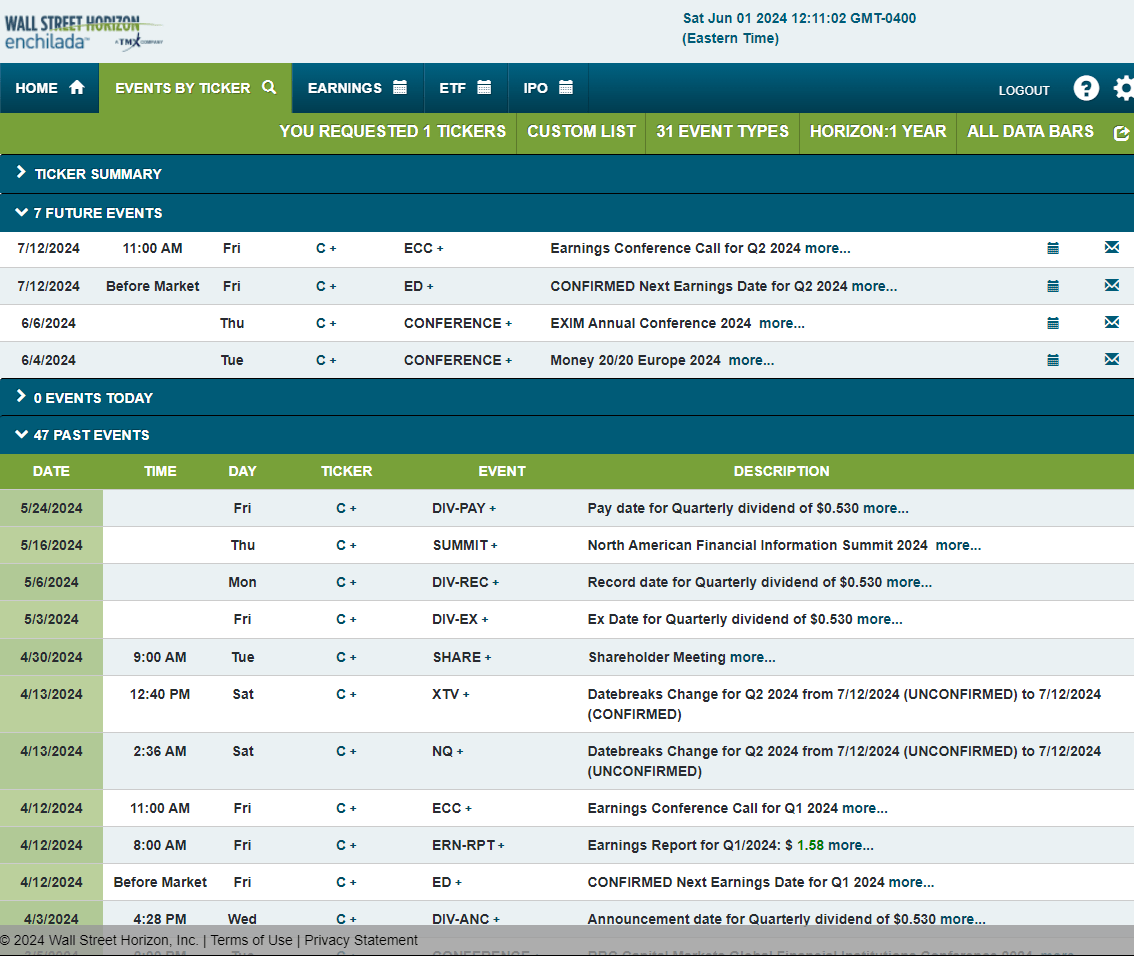

Looking ahead, corporate event data provided by Wall Street Horizon show a pair of upcoming conferences at which Citigroup's management team is expected to speak. The first is the Money 20/20 Europe 2024 conference, followed by the EXIM Annual Conference 2024. Both occur later this week.

After that, Citigroup's Q2 earnings report is confirmed to take place on Friday, July 12th BMO with a conference call later that morning. You can listen live here.

Corporate Event Risk Calendar

Wall Street Horizon

The Technical Take

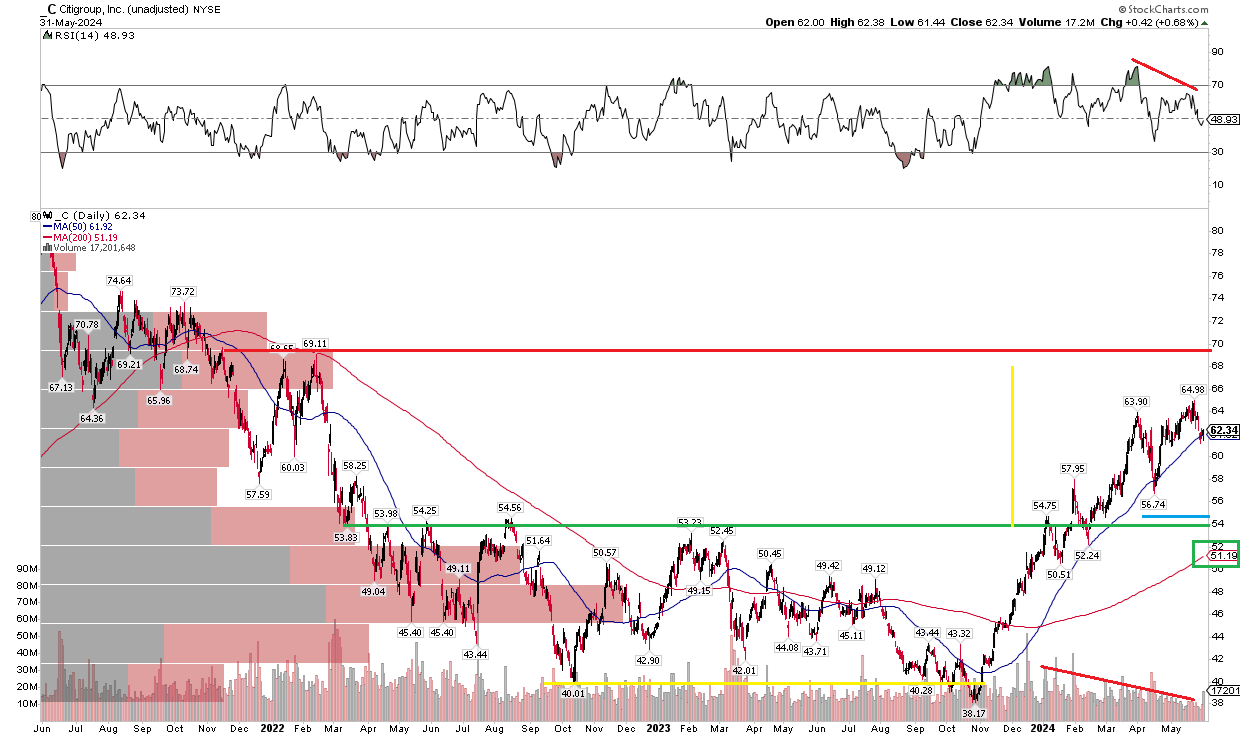

After a protracted bear market, Citi stock has surged off the lows of last October. Notice in the chart below that there was key resistance in the $53 to $55 range, but the bulls were able to reclaim that important level earlier this year. What’s more, the long-term 200-day moving average is positively sloped, suggesting that the bulls are in control of the primary trend.

But take a look at the RSI momentum oscillator at the top of the graph – it printed a clear bearish divergence to price. That tells me a near-term pullback toward support in the mid-$50s could be in the works. Additionally, the 38.2% Fibonacci retracement price from the October 2023 low to the May 2024 peak is $54.70 - right near the area of polarity. So, there is a confluence of support there.

Big picture, I see an upside target to near $70 based on the height of the consolidation zone from Q2 2022 through last December.

Citi: Key Support Near $54, Rising 200dma, Bearish RSI & Volume Are Risks

Stockcharts.com

The Bottom Line

I have a buy rating on Citigroup. I see shares undervalued as earnings accelerate over the next handful of quarters. Shareholder-friendly activities are also a potential upside catalyst while C’s technical chart is mixed, but still broadly trending higher.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

- AaronJe·06-04Undervalued and strong potential for growth! [Grin]LikeReport

- DebbyLily·06-04Great analysis [Applaud]LikeReport