Weak Non-Farm Payrolls In May Can Pull Rate Cuts Forward

Summary

- Considering the Fed's close watch on labor market figures, the May figures will be key as they may well confirm that a slowdown is indeed underway.

- After a weak April, the employment situation is forecast to be sluggish again. This ties in with muted economic trends seen in GDP, corporate profits and even other labor surveys.

- Along with the likely start of a rate cut cycle for other central banks, this can pull the Fed's rate cuts forward too.

- A weaker economy and lower interest rates suggest plenty of ideas on what to buy and what not to right now. For the short term, the broad indexes look avoidable, while geopolitically driven stocks are worth considering.

shapecharge

From a purely analytical perspective, the unfolding of macroeconomic trends in the US economy has been fascinating in recent times. The Fed has held rates steady, but the economy was surprisingly resilient, as seen in both the labor market and GDP growth figures.

Even as the GDP growth numbers finally let up in Q1 2024, the Fed remained hawkish due to both an uptick in inflation and strong jobs numbers. Specifically, in regards to the labor market, in its latest FOMC statement, the Fed maintained that "Job gains have remained strong, and the unemployment rate has remained low."

But the labor market print that followed the meeting and the forecasts for the next release, might change the reserve's mind. Especially, as other central banks inch closer to rate cuts, which can be a leading indicator for what the Fed will do next.

Here, I look at the recent job markets trends and what to expect from the next employment report. And why this, along with the actions of other banks increase the probability of rate cuts sooner rather than later. Finally, investment options in the current stage of the macroeconomic cycle are explored.

What to expect from the employment report

That the US economy's slowing down became obvious when the first quarter (Q1 2024) figures came in, with sub-trend growth of 1.6%, which was then revised down to 1.3%. The labor market weakness that followed in April only confirmed this further.

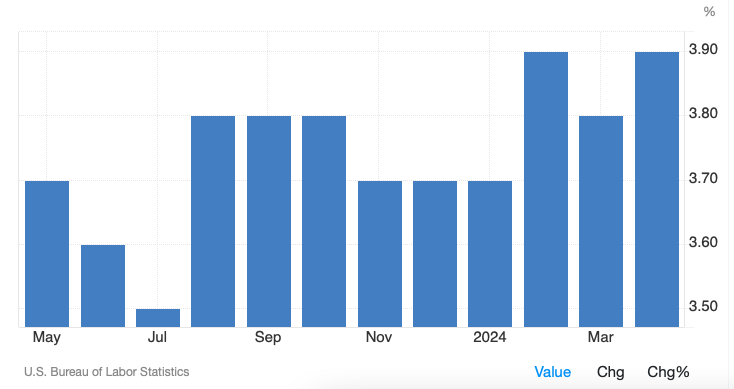

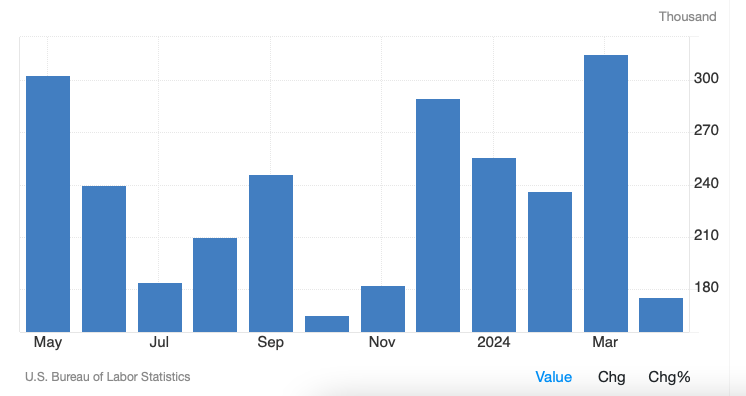

The unemployment rate rose to 3.9% in April, rising back up to the levels seen in February (see Chart 1 below), which were the highest levels seen in two years. But the big negative surprise was in the non-farm payroll figures, which rose by just 175,000 (see Chart 2 below), the slowest increase in six months and almost 28% lower than the average job gains over the past 12 months.

Chart 1: Unemployment Rate (Source: Trading Economics)

Chart 2: Non-farm Payrolls (Source: Trading Economics)

At any other time, this could be seen as a one-off. After all, both the unemployment rate and non-farm payroll figures have seen bounce backs after a single month of weakness in the past. Except that besides the GDP print, the projections and other incoming data suggest otherwise:

- Economists expect unemployment rate to have remained unchanged in May from the previous month. Non-farm payrolls to see yet another month of below-average increase of 190,000. The actual figure could be even lower going by last month's trend. 240,000 job increases were forecast for April, but the number came in much lower.

- The downward GDP growth revision for Q1 2024 on weaker consumer spending already signals a bigger slowdown than earlier estimated. But corporate profits fell by 1.7% quarter-on-quarter as well, a particular disappointment compared with expectations of a 3.9% increase. And the Job Openings and Labor Turnover Survey [JOLTS] also showed that job openings in April were down to the lowest levels in over three years.

Why it's important

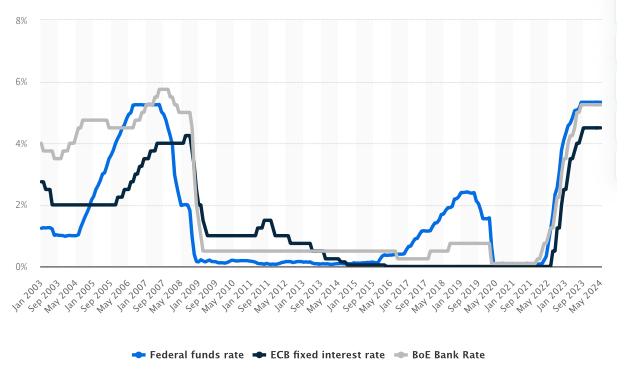

Essentially, the report will confirm further what's already becoming clear. That the slowdown is here and interest rates might now be higher for much longer. This is particularly so as the rate cut cycle is ready to start internationally, and monetary policy cycles tend to move broadly in tandem (see chart below).

Source: Statista

According to a recent report by Mark Wall, Chief Economist, Europe and team, "there is no questioning of the wisdom of cutting rates on 6 June". They expect a 25 basis points cut in policy rates to 3.75%, even as they forecast the cycle to proceed slowly. Looking farther ahead, the Bank of England [BoE] is seen cutting rates in August as well.

There's a bigger case for rate cuts in these economies, to be fair, as both inflation rates and GDP growth are slower compared to the US. And there isn't perfect alignment in interest rate cuts, either. However, if other central banks are starting to cut rates, it suggests that the focus is firmly moving from inflation management to supporting the real economy. The same can follow for the Fed too, especially with the next labor market report confirming the upcoming turn of the interest rate cycle.

Where to invest

So there are two key points to note when making investment decisions based on the macroeconomy now. One, a slowdown is here. And two, interest rate cuts are likely, sooner than later. Here are a few ideas on what to avoid, consider and buy.

Avoid short-term index investing

First, let's look at the S&P 500 (SP500). Up by over 25% in the past year, it doesn't indicate any signs of an economic slowdown. I'd continue to maintain caution, though. Especially with the recent dip in corporate profits, in addition to the real economy trends, there could be a downside surprise this year.

My own estimates, based on expectations of the macroeconomy, point to a flat index on average for the year compared with 2023. This indicates that the risks of a crash later in the year have only increased now, going by the recent uptick in the index. From a longer-term perspective, though, there can still be an upside, as evident from the promise in the Nasdaq tracker Invesco QQQ Trust ETF (QQQ).

Consider accumulating real estate

Despite macroeconomic weakness, I also believe it's a good idea to have real estate on the investment watchlist if not, start accumulating the sector now due to lower interest rates. Lower rates can be a balancing factor and buying into the sector now can hold investors in good stead when the cycle turns. I had already mentioned the Real Estate Select Sector SPDR Fund ETF (XLRE) in this regard last September. It's worth noting that after an 8.6% decline over the year then, it's now up by 4.28% (see table below).

US Equities, Performance By Sector (Source: Seeking Alpha)

Selective defensives look good

That buying defensives is a good idea, is a no-brainer at this time. But all defensives aren't made equal, as big price rises have been seen for healthcare stocks like Eli Lilly (LLY), for example, making it a preferable longer-term investment instead.

Right now, I like tobacco stocks like Philip Morris (PM) instead, which offer at the very least a very healthy dividend yield. Moreover, with industry beating revenues from smoke-free products, it has the highest probability for sustaining well over time.

Look towards the geopolitical cycle

It's also a good time to free investing decisions from the particularly unending uncertainty around macroeconomic conditions seen in the recent past. And one way to do so is to consider the geopolitical cycle instead. Defence spending is on the rise, resulting in a 23% increase in the iShares U.S. Aerospace & Defense ETF (ITA) over the past year.

Nuclear energy is another sector receiving a boost from the need for energy independence, and also the bigger drive towards clean energy. It's little surprise that the biggest nuclear energy ETF, Global X Uranium ETF (URA) is up by 41% as a result.

In sum

With the macroeconomy finally playing by the book, as the employment report and particularly weak payroll figures are likely to indicate, rate cuts could happen sooner rather than later. This is especially as the ECB and BoE inch closer to them, an important development as there's a broad alignment in monetary policy.

In making investment decisions, both the weaker economy and lower rates can be taken into account. While broad indices are avoidable for the short-term, real estate can be one to watch now for the medium term investment. Selective defensives like tobacco stocks can assure a nice passive return too, while looking at more geopolitically oriented investments like defence or nuclear energy can break investments free from the macro cycle altogether.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.