Astec Industries: Expect Underperformance To Continue For As Long As Backlog Is Declining

Summary

- Astec Industries has been underperforming the broader market by quite a bit in recent months due to weak financial results.

- Despite improved 2023 fiscal year results, 2024 is showing signs of trouble with falling backlog and declining revenue and profits.

- The company's valuation looks fairly valued compared to similar firms, but with ongoing issues, keeping the 'sell' rating for now seems prudent.

Jasonfang/E+ via Getty Images

Back around the middle of November of last year, I ended up revisiting a company by the name of Astec Industries (NASDAQ:ASTE). Odds are, even if you haven't heard of the company before, you have had exposure to its industry. That is because the company is focused on producing and selling equipment and components that are used in road building and other construction related activities. Conceptually, I think this is an interesting space to play in. However, I ended up downgrading the stock from a ‘hold’ to a ‘sell’ because of mixed financial performance and declining backlog.

So far, that call has proven to be successful. Since that article was published, shares are down 3.2% at a time when the S&P 500 is up 24.2%. Given the time that has passed, we also have a better look into the performance of the business. While the 2023 fiscal year proved to be quite strong for shareholders, 2024 is shaping up to be problematic. Backlog continues to fall while both top line and bottom-line results worsen.

From a valuation perspective, the company is looking much better now than it did previously. But relative to similar firms, including firms that don't have these problems, the stock looks fairly valued at best. Given this mix, I was almost tempted to upgrade the stock back to a ‘hold’. But when you consider the other opportunities that are out there, I suspect that shares will probably continue to underperform the broader market moving forward. Because of that, I'm keeping the company rated a ‘sell’ for now. But it would not take much for this to turn to an upgrade.

Tough times

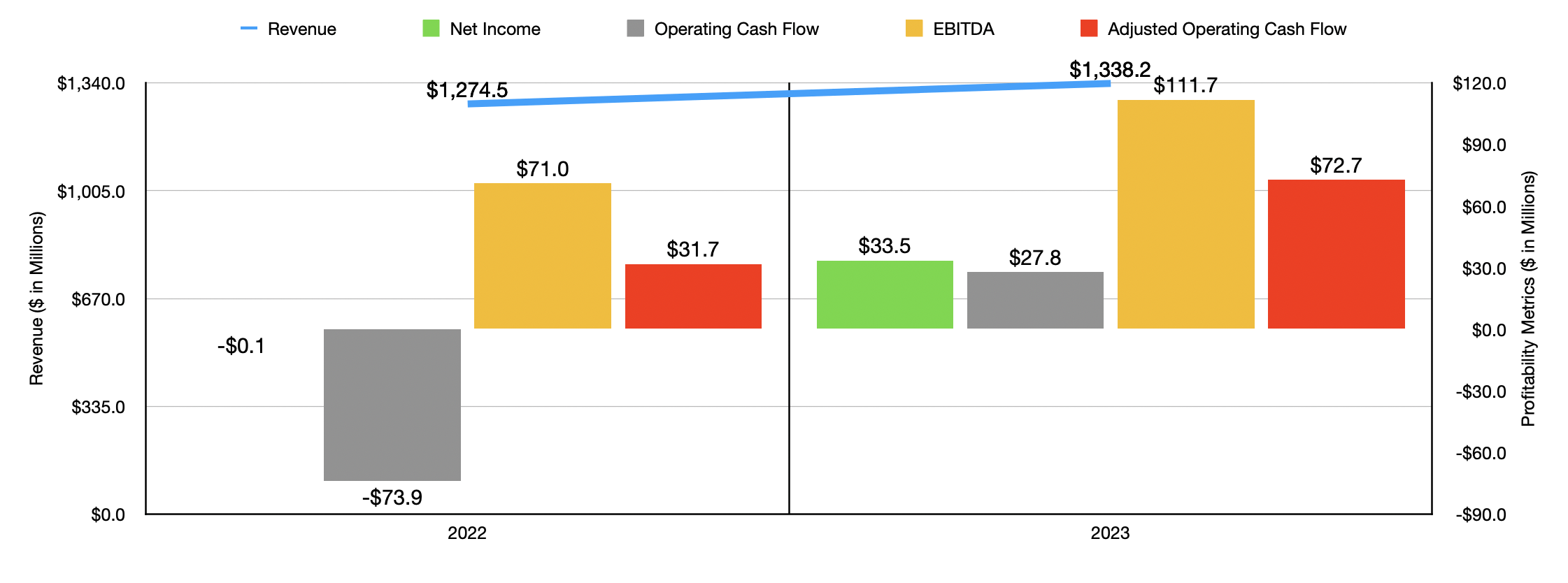

If you were to look at only the complete annual data provided by management, you would think that I was crazy for calling Astec Industries a ‘sell’. In 2023, revenue for the company came in at $1.34 billion. That's 5% above the $1.27 billion generated in 2022. With the rise in sales also came improved profits and cash flows. Net income, for instance, went from a loss of $0.1 million to a gain of $33.5 million. Operating cash flow turned from negative $73.9 million to positive $27.8 million. If we adjust for changes in working capital, it more than doubled from $31.7 million to $72.7 million. And lastly, EBITDA for the company popped up from $71 million to $111.7 million.

Author - SEC EDGAR Data

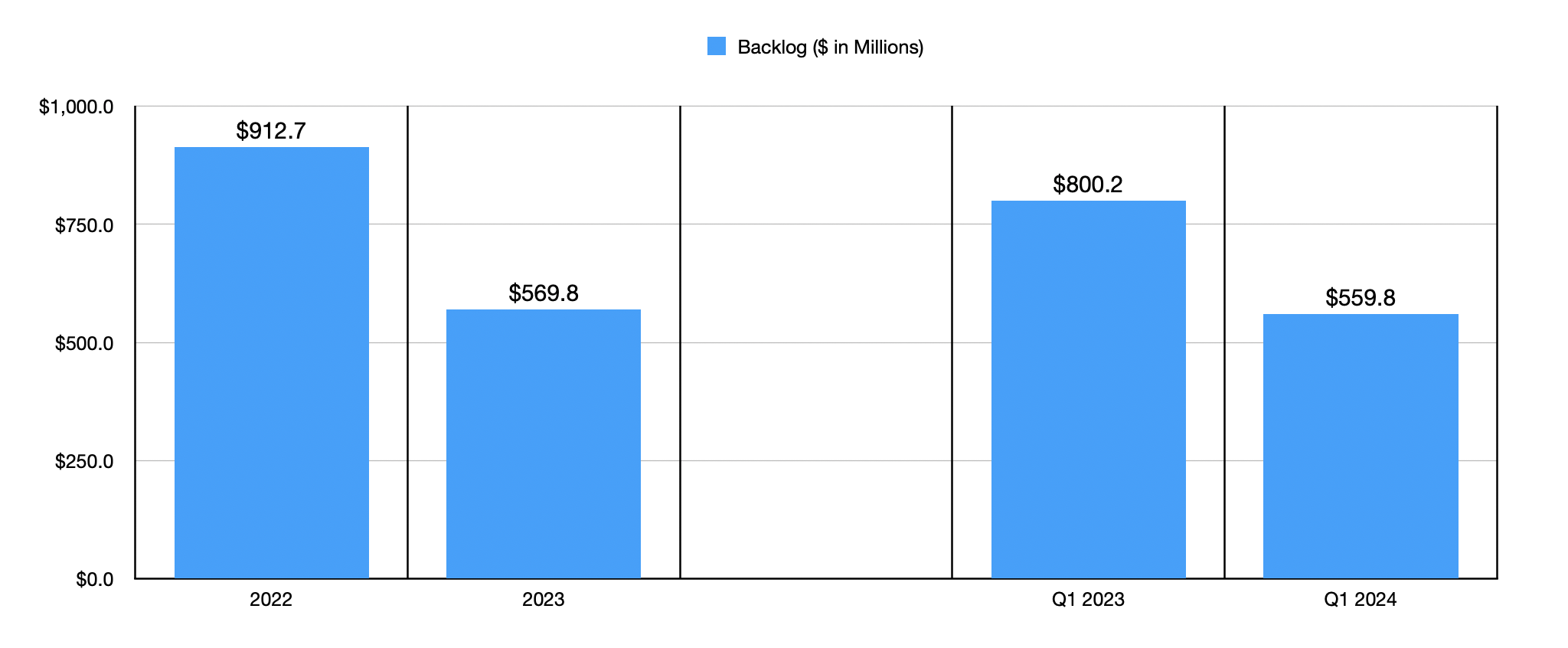

Unfortunately, bad signs were already beginning to show up last year. At the end of 2022, the company had a backlog on its books of $912.7 million. By the end of 2023, backlog had fallen to only $569.8 million. That's a year-over-year decline of 37.6%. Even though top line and bottom-line results in 2023 were far better than what was seen the year prior, you can't continue that trend forever if backlog is taking such a tumble. Sure enough, by the first quarter of 2024, things started looking really awful.

Author - SEC EDGAR Data

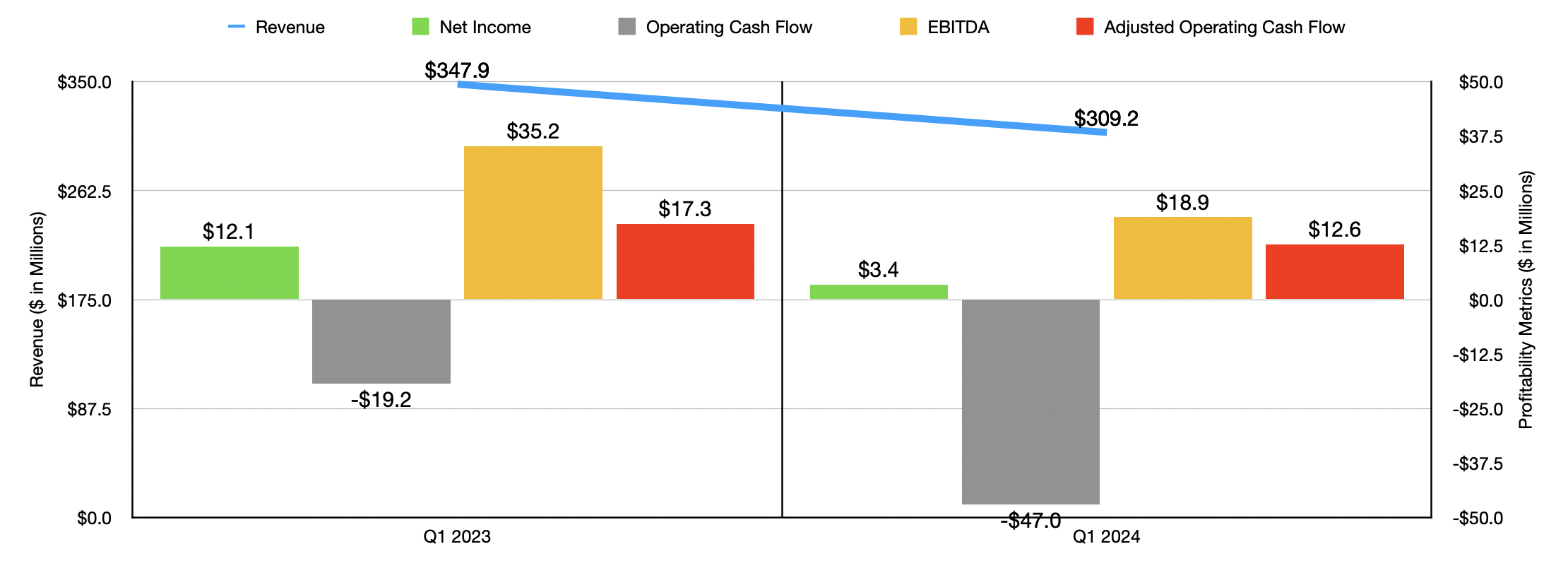

During that quarter, revenue for the business came in at $309.2 million. That's 11.1% lower than the $347.9 million reported for the first quarter of 2023. Management attributed this to a couple of factors. For starters, a decline in volume and a drop in product mix negatively impacted operations. In equipment sales, this hurt to the tune of $40 million. And when it came to service and equipment installation revenue, the decline was $7.7 million. Freight revenue and used equipment sales dropped by $1.8 million and $1.7 million, respectively. The company did benefit from higher revenue coming from parts and components. These added a combined $12.5 million to the company's top line. But clearly, this was not enough to offset the weaknesses elsewhere.

Author - SEC EDGAR Data

The bottom line for the company took a real hit during this window of time. Net income plunged from $12.1 million to $3.4 million. But it wasn't alone. Operating cash flow went from negative $19.2 million to negative $47 million. On an adjusted basis, it pulled back from $17.3 million to $12.6 million. Finally, EBITDA for the company was cut by nearly half from $35.2 million to $18.9 million. These results might be tolerable if we were seeing some improvement involving backlog. But that, sadly, has not been the case. Backlog fell to $559.8 million. This was below the $569.8 million reported at the end of 2023, and it was down from the $800.2 million reported for the first quarter of 2023.

Author - SEC EDGAR Data

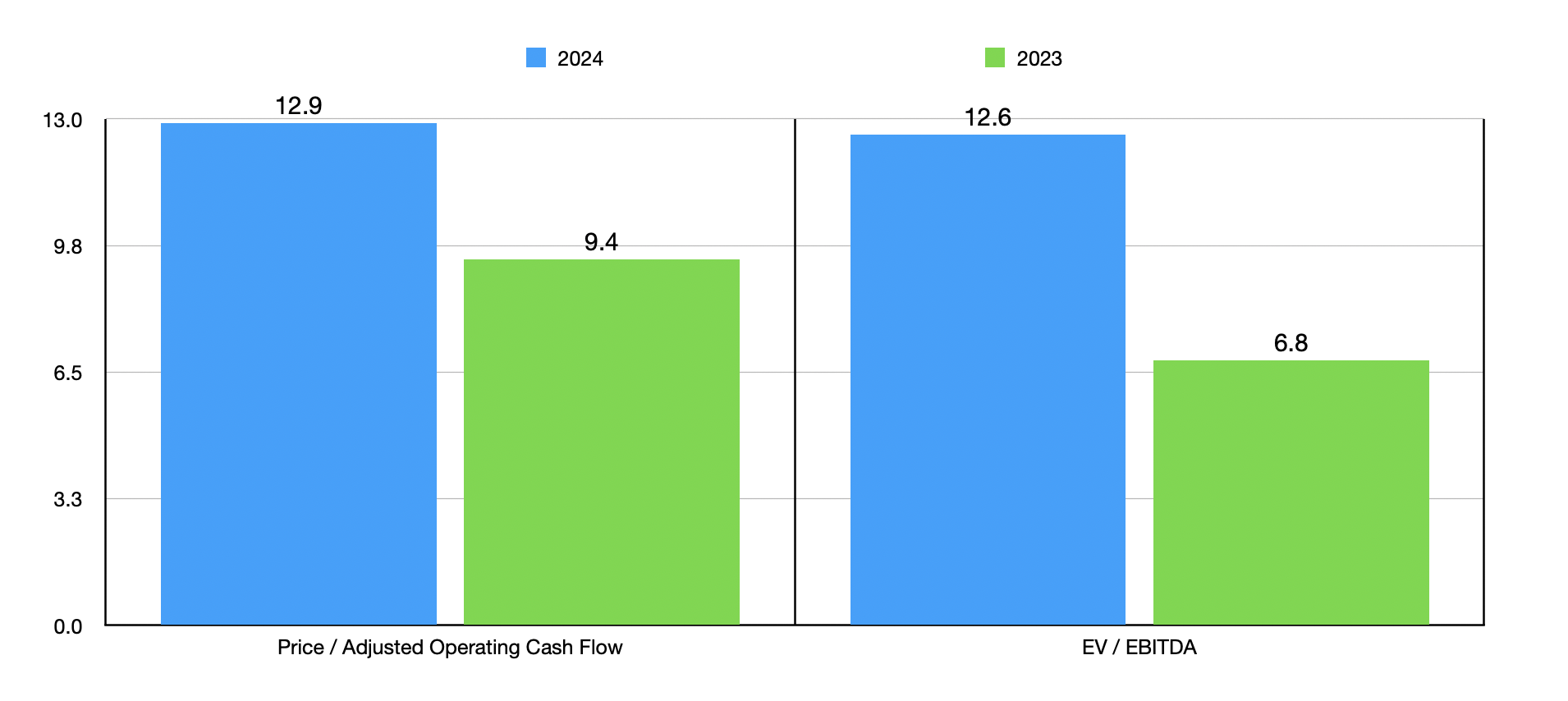

We don't really know what to expect for the rest of the year. Even if we just annualize results experienced so far, things don't look too bad. This would give us adjusted operating cash flow of $52.9 million and EBITDA totaling $60 million. Using these figures, I was able to value the company as shown in the chart above. This chart includes not only the estimates for 2024, but also historical results for last year. On a forward basis, I would argue that shares look more or less fairly valued. When we compare the company as I did in the table below to five similar firms, that picture holds true as well. If we use the 2023 figures, then two of the five firms ended up being cheaper than Astec Industries on both a price to operating cash flow basis and on an EV to EBITDA basis. But if we use the forward estimates for 2024, this number increases to three of the five companies in both instances.

| Company | Price / Operating Cash Flow | EV / EBITDA |

| Astec Industries | 12.9 | 12.6 |

| Douglas Dynamics (PLOW) | 11.0 | 10.5 |

| The Shyft Group (SHYF) | 9.2 | 25.7 |

| Wabash National (WNC) | 4.3 | 3.9 |

| The Manitowoc Company (MTW) | 22.9 | 6.2 |

| Wabtec (WAB) | 18.5 | 16.8 |

Takeaway

Typically, this kind of valuation, both on an absolute basis and relative to similar firms, would be enough for me to upgrade the stock from a ‘sell’ to a ‘hold’. However, to see backlog continue falling and considering the impact that could have on subsequent quarters in the form of even lower cash flows, I think that the risk tilts slightly in favor of the bears. I wouldn't go so far as to say that shares deserve downside. But when you consider a business that is shrinking and that's trading at a fair value, it's difficult to imagine an outcome where the stock starts to outperform the broader market. If we could get trading multiples on a forward basis to be in the high single digit range or if we start to see backlog truly stabilize, my thoughts on the matter will almost certainly change. But out of an abundance of caution, and the desire for a margin of safety in my investing, I think that keeping the company a ‘sell’ for now makes the most sense.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.