Strategic Focus To Realign MSA Safety's Growth Despite Near-Term Challenges

Summary

- MSA introduces new products in firefighting, fixed gas, and flame detection categories to combat recent sales declines.

- Despite short-term challenges, the company aims for above-market profitable growth, focusing on shareholder returns and balance sheet efficiency.

- MSA remains relatively overvalued but shows potential for growth with a "hold" rating.

andreswd

MSA Gathers Steam

I last discussed MSA Safety Incorporated (NYSE:MSA) on April 2, and you can read the latest article here. In recent times, it has introduced products in the firefighting, fixed gas, and flame detection categories to arrest the recent sales declines. In the long term, it has devised strategies that involve pursuing above-market profitable growth. It plans to achieve this through connected solutions and the market trend toward safety product adoption. The strategy's other part includes increasing shareholder returns and achieving balance sheet efficiency.

However, early in 2024, MSA suffered from an adverse contract renewal timing in Latin America and a slower recovery in China. I also suspect excess backlog and sales normalization can offset sales growth in the next couple of quarters. Nonetheless, the cash flow improvement allowed it to increase dividends and increase the share buyback program. The stock remains relatively overvalued. Keeping in view the short-term challenges and long-term potential, I reiterate my “hold” call.

Why Do I Keep My Rating Unchanged?

In my previous article published in April, I found that MSA targeted growth through product redesign and new product development. The stock was relatively overvalued, but positive value drivers warranted a "hold" rating. I wrote:

The company's new product introductions and cost management efforts yielded positive results through margin expansion in Q4. A lower book-to-bill ratio can, however, become a concern in early 2024. I think the company's steps to lower its debt-to-equity ratio following positive free cash flow generation will alleviate some concerns.

In Q1, the company introduced products in the firefighting, fixed gas, and flame detection categories to arrest the sales decline in the industrial PPE category. Despite wobbly sales, the company is firmly set to achieve its long-term targets, including adding recurring revenue streams, adopting the MSA Business System, improving balance sheet efficiency, and repurchasing shares. Its earnings and cash flow improvement should help it realize its potential. However, the stock remains relatively overvalued. I continue to rate it a "hold."

New Products And Production Ramp Ups

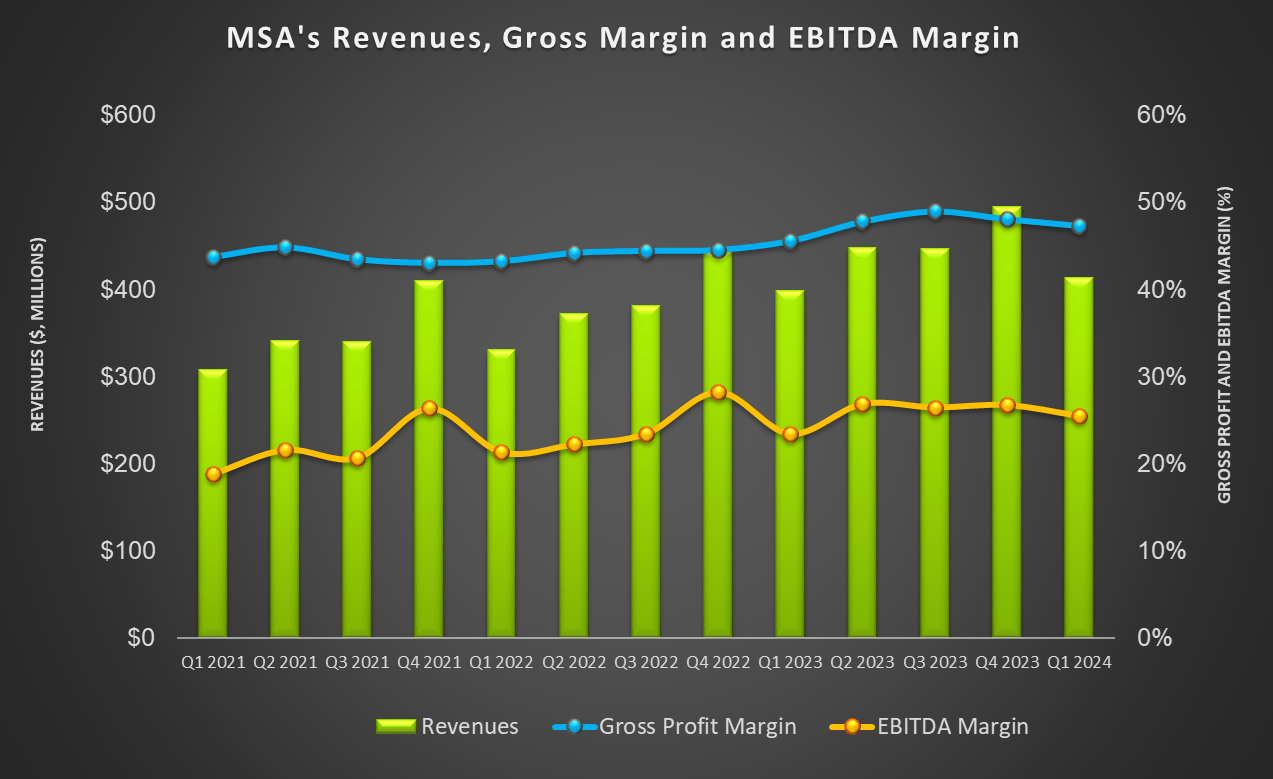

MSA has a steady commercial product pipeline lined up, which calls for a resilient outlook despite an excess backlog and sales normalization for the rest of 2024. The company is diversified across product offerings, geographic regions, and end markets. Even though I expect some regions and industrial end markets to remain challenging, the overall outlook remains balanced due to a robust strategy.

Its recent product introductions include the Cairns 1836 Fire Helmet, which caters to a broad range of firefighter products and solutions. The encouraging response can arrest the sales decline in detection and industrial PPE, which declined to “mid-single digits” in Q1 2024, according to the company’s estimates. The other new launch would be FL5000, a fixed gas and flame detection product. In portable gas detection, its io 4 ALTAIR gas detector continues to perform well, both domestically and internationally.

A Review Of Long Outlook And Strategy

Seeking Alpha

As a result of these initiatives, the company’s management reiterated “mid-single-digit” revenue growth in FY2024. Let us now take a close look at the company’s long-term strategy and financial objectives, which it discussed in a review in May.

In the review, MSA decided to pursue above-market profitable growth. The company’s connected solutions and the trend toward adopting safety products among consumers will likely accelerate growth. It also seeks to offer solutions with recurring revenue streams while keeping an eye on M&A capabilities for rapid growth. It has adopted the MSA Business System to improve operations, pricing, resource allocation, and balance sheet efficiency. And, to deliver sustainable, long-term growth, it has focused on efficient capital deployment. The recent increase in share repurchase authorization indicates how the company plans to achieve this. Also, in May, it raised quarterly dividends by 8.5%.

By 2028, the company plans to generate organic revenues of $2.1 billion—$2.3 billion, an adjusted operating margin of 23.5%—28%, and an adjusted EPS of $10-$11 per share. Compared to TTM 2024 revenues and EPS, this translates to 22% and 56% growth, respectively.

Industry Indicators And My Estimates

tradingeconomics.com

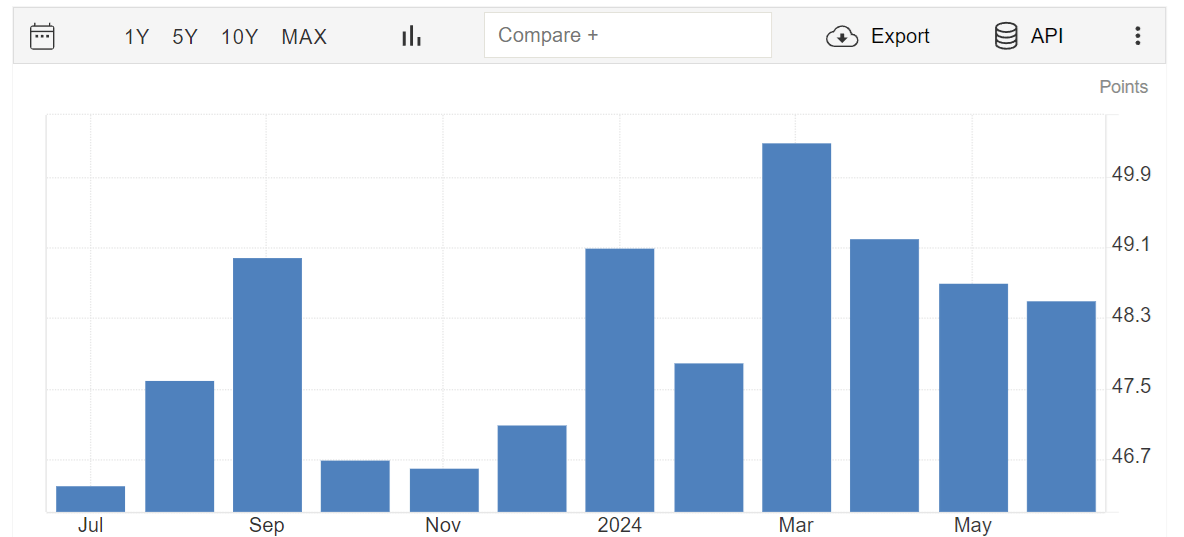

The Producer Price Index declined to 48.5 in June 2024, stretching its losing streak to three consecutive months. The index fell below 50 due to falling manufacturing activity, contraction in production and employment, and lower inventories and backlog. An index below 50 points to activity contraction and can hurt MSA’s outlook.

Over the past 12 quarters, its adjusted EBITDA increased by 8% on average. Given the removal of cost inefficiencies and the initiatives to improve long-term growth, I expect the EBITDA to accelerate while the topline stabilizes. Over the next four quarters, I expect its adjusted EBITDA to increase by 8%-12%.

Management Change

In June, MSA announced that David J. Howells was promoted to the position of President of MSA International. He will oversee the company’s business operations across Europe, the Middle East, Africa and Asia. Earlier, he played a crucial role in transforming the company’s commercial business with a progressive Go-to-Market strategy.

The Q1 Drivers

MSA's Filings

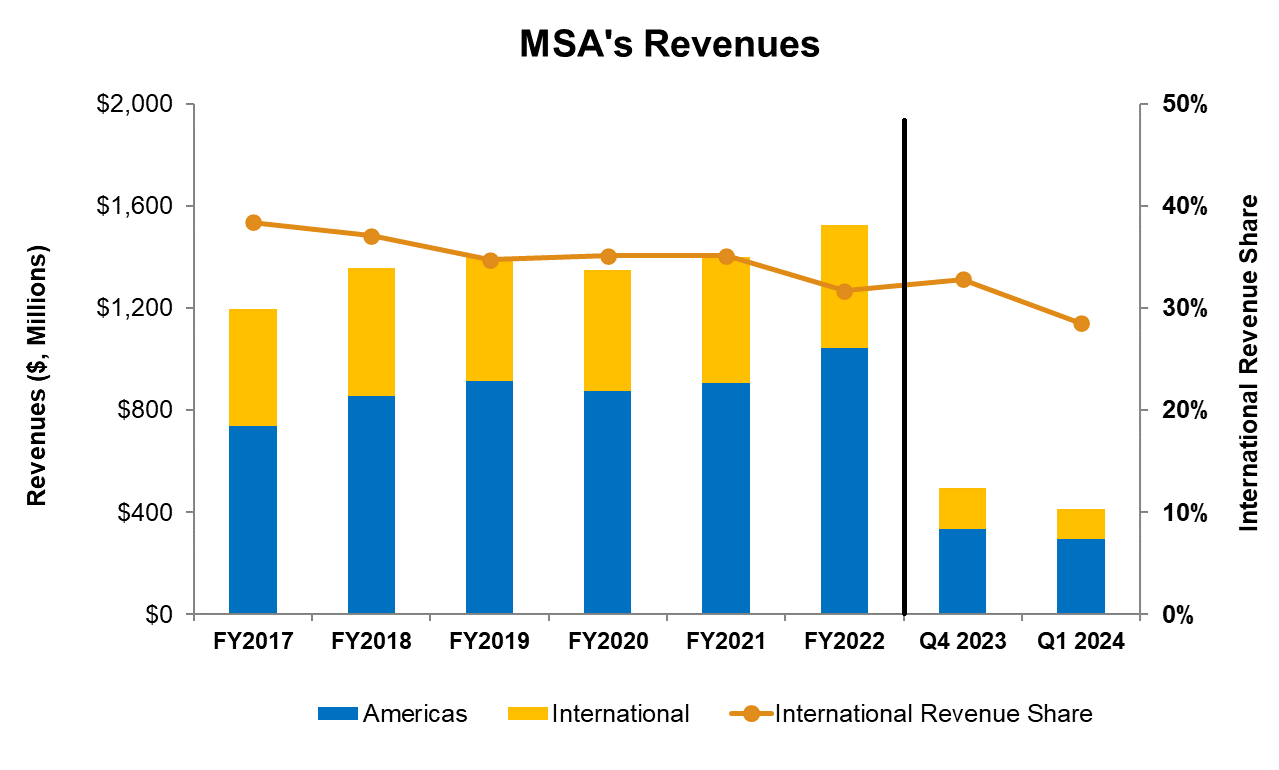

As disclosed in the Q1 press release dated April 29, MSA’s quarter-over-quarter revenues in the Americas declined by 11%. However, this was better than the 28% fall in sales in international territories in Q1. Its book-to-bill was 1x as of March 31.

The pressure on sales emanated primarily from an adverse contract renewal timing in Latin America and a slower recovery in China. Order placed, on the other hand, accelerated in Q1 and early Q2, which points to a potential recovery in sales in 2024. Compared to a year ago, its earnings turned to a profit from a loss.

Cash Flows And Debt Level

In Q1 2024, MSA's cash flow from operations turned positive, compared to a steeply negative CFO a year ago. Although revenues remained nearly unchanged, the cash flow fall was related to the contribution to the divestiture of MSA LLC. Free cash flow (or FCF), too, turned positive in Q1 2024.

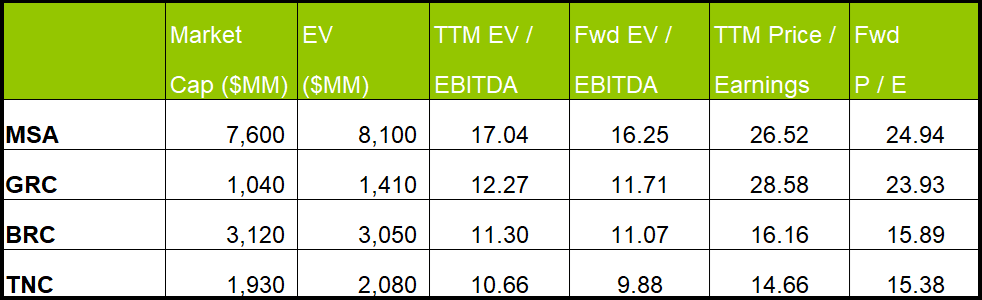

MSA has a higher debt-to-equity ratio was 0.74x as of March 31, 2024. The leverage ratio was also higher than its competitors' (GRC, BRC, TNC) average leverage of 0.52x. Its cash & equivalents totaled $148 million as of March 31, 2024. Due to higher cash flows, its balance sheet looks steady. So, in May, the company disclosed a $200 million share repurchase program, which would replace a previous $100 million buyback program.

Relative valuation

Author Created and Seeking Alpha

MSA's forward EV/EBITDA multiple versus the current EV/EBITDA contracts by nearly the same as for its peers, which typically reflects in a similar EV/EBITDA multiple compared to its peers. However, its EV/EBITDA multiple (17x) is higher than its peers' (GRC, BRC, and TNC) average of 12.8x. So, the stock is relatively overvalued. It is trading slightly below its past five-year average.

MSA's average EV/EBITDA multiple for the past five years was 18.2x. If the stock trades at this multiple, it can increase by 7%. If it trades at its peers' average, the stock price can decline by 26%. Since my last publication in April, where I suggested a "hold," the stock has increased by approximately 2%.

As I discussed earlier in the article, I expect 8%-12% adjusted EBITDA growth in the next four quarters. Feeding these values in the EV calculation and assuming the current EV/EBITDA multiple of 17x holds, I think the stock should trade between $210 and $218, implying an 11% upside.

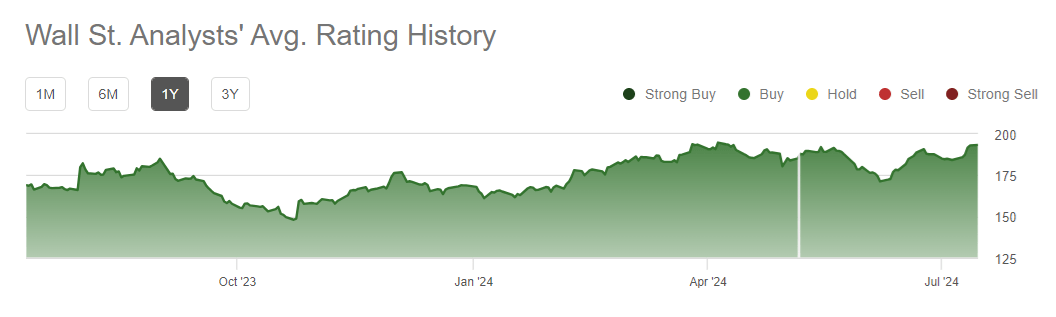

Wall Street Rating

Seeking Alpha

One sell-side analyst has rated MSA a "strong buy." One analyst rated it a "hold," while none rated it a "sell." The consensus target price is $197.5, suggesting nearly a mild upside at the current price. Considering the current drivers, I think the Wall Street analysts are cautiously realistic about their estimates.

Key Challenges

As I discussed above, MSA’s order conversion (i.e., order to sales) was low due to supply chain issues. Typically, supply chain issues affect shorter-cycle products. The company’s short-cycle products include portable gas detection and fall protection. Its detection and industrial PPE product backlog ended higher in Q1 than a quarter ago. The company works closely with its suppliers and builds out its detection portfolio with innovative new products to counter the slowdown in sales.

What's The Take On MSA?

Seeking Alpha

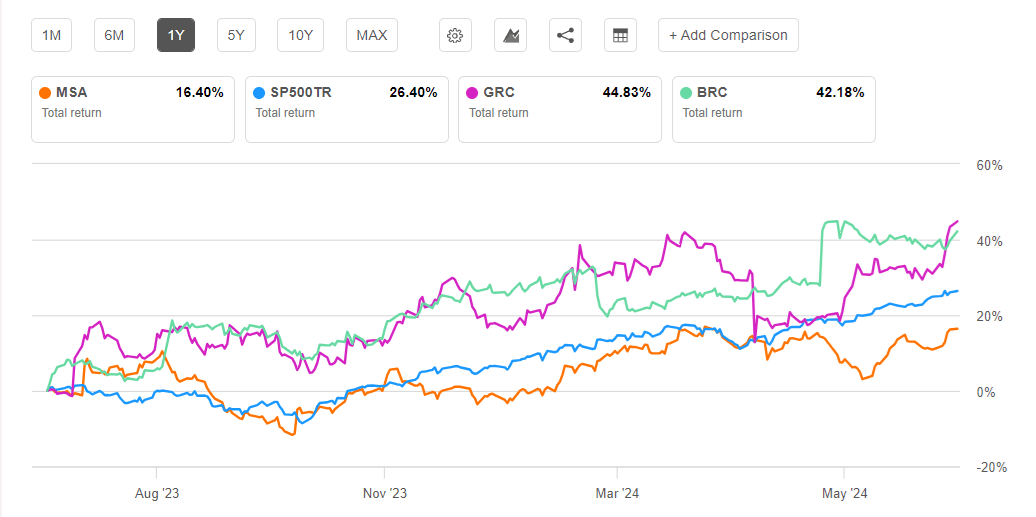

Early in Q2, The US industrial and manufacturing environment stayed under pressure. With a steady commercial product pipeline, the company’s outlook remains balanced despite a challenging end market, relatively excess backlog, and an expected sales normalization in 2024. The stock underperformed the SPDR S&P 500 ETF (SPY) in the past year.

MSA’s primary focus remains on realizing long-term growth and balance sheet efficiency. I think the company’s actions to increase shareholder returns through share repurchase following positive free cash flow generation will boost investors’ sentiment. Its relative valuation appears to be at a premium. Despite that, I think the stock deserves a "hold" call given the strategic initiatives.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.