Ethereum: A More Favorable Backdrop Is Emerging

Summary

- Ethereum's recent performance has been poor relative to peers, which could be due to competition, scaling problems or monetary policy.

- Ethereum is trying to improve scalability using layer 2 networks, but this is a long term initiative.

- Softer inflation data suggests a loosening of monetary policy is imminent, which should be supportive of Ethereum in the near term.

- Longer term, competition and uncertainty regarding how value will accrue within the Ethereum ecosystem may limit the upside.

Oleksandr Shatyrov

Ether (ETH-USD) has performed relatively poorly during the current cycle. While there are valid questions around Ethereum's functionality and adoption in real-world use cases, I think that some of Ether's struggles are simply the result of tighter monetary policy. Declining inflation could lead to lower interest rates later in 2024 though, which may support Ether's price. Inflows into Ethereum ETFs could also provide a boost, although I believe that the fragmentation of demand across competing chains will remain a headwind in the near term.

Supply

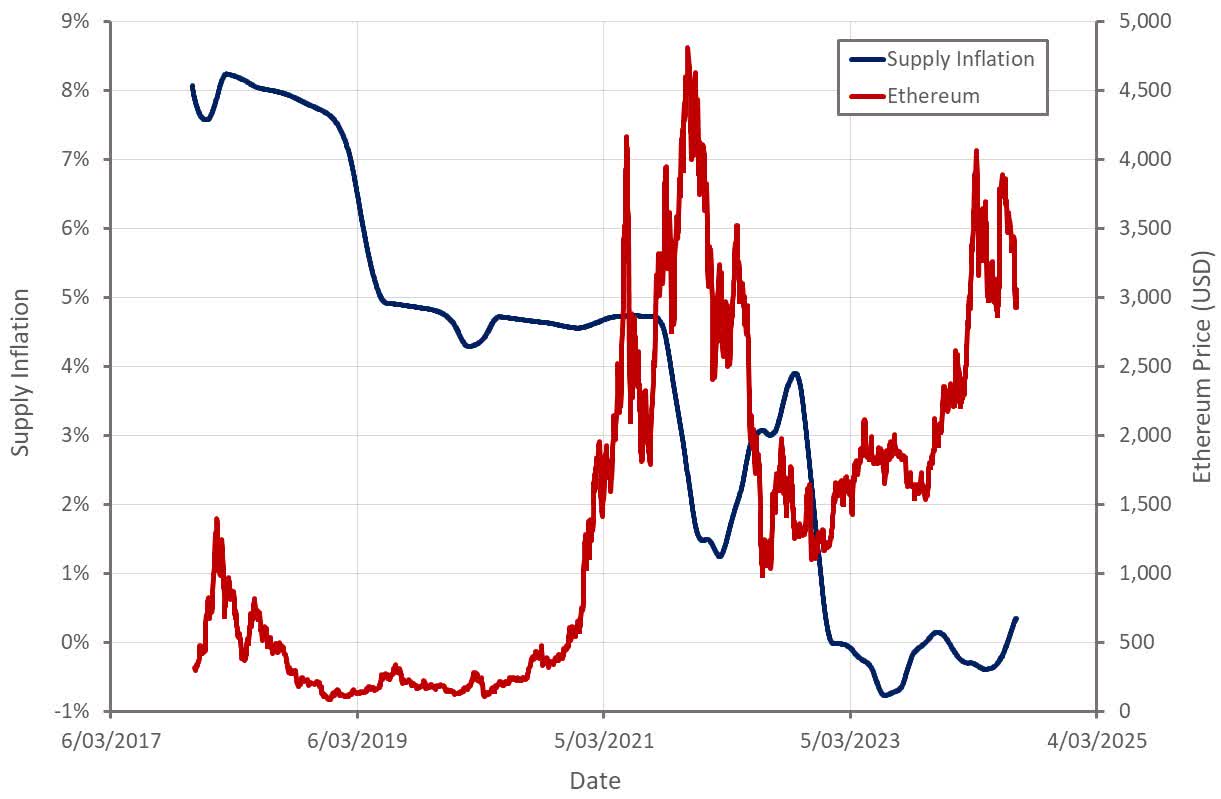

Ethereum became modestly deflationary in 2022 with the switch to proof of stake. This move was widely expected to drive Ether's price higher, although I tend to think the importance of supply changes is generally overstated, particularly when viewed in isolation.

Ethereum is now returning to an inflationary supply to help try and reduce transaction fees, with the Dencun upgrade in March 2024. Inflation is modest, though, and I don't believe this will be an important determinant of Ether's price going forward.

Figure 1: Ethereum Supply Inflation (source: Created by author using data from Yahoo Finance and Etherscan)

Demand

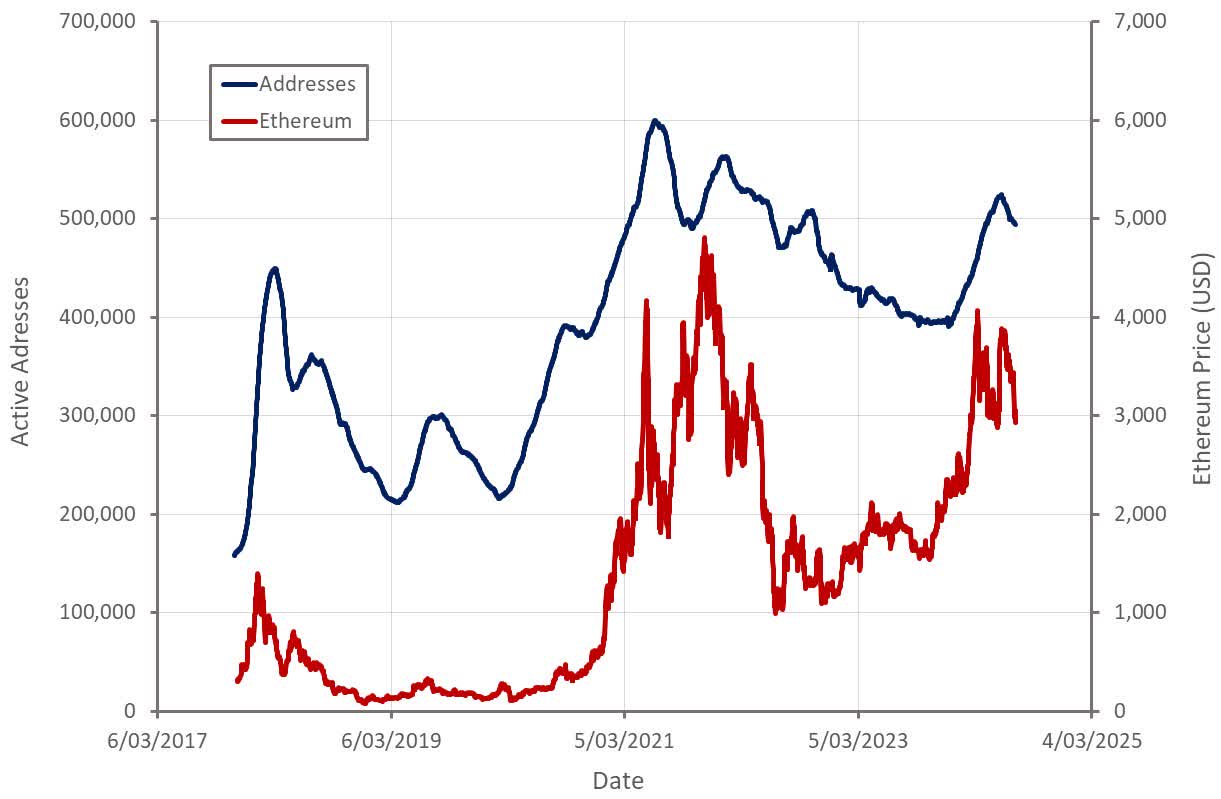

The number of Ethereum active addresses suggests that demand has increased along with price in recent months, although this has been fairly modest. Unlike 2020, price has led demand rather than the other way around, which I think is somewhat concerning.

While DeFi and NTFs created hype in 2021, a similar growth driver hasn't really emerged in the current cycle. This is an area where scalability is hurting Ethereum. Low cost and fast transactions have been driving DeFi and NFT adoption on Solana. Solana has also seen a surge in meme coin activity.

Figure 2: Ethereum Active Addresses (source: Created by author using data from Yahoo Finance and Etherscan)

AI

Artificial intelligence and autonomous agents could be an emerging tailwind for Ethereum. This is because generative AI and agents threaten to create a world where:

- The majority of content is created by AI

- Publicly available information is used to train models without attribution or compensation

- Internet users are unable to determine whether content is real or fake

- The activity of many agents needs to be coordinated

Crypto can help to alleviate some of these issues by:

- Transparently proving ownership

- Providing a source of identity

- Providing economic incentives which coordinate the activity of agents and help allocate resources

It is too early to say how large the impact of AI will be or how these types of issues will be managed, though. For example, ownership, identity and activity coordination could also be provided by a centralized service.

Ethereum ETF

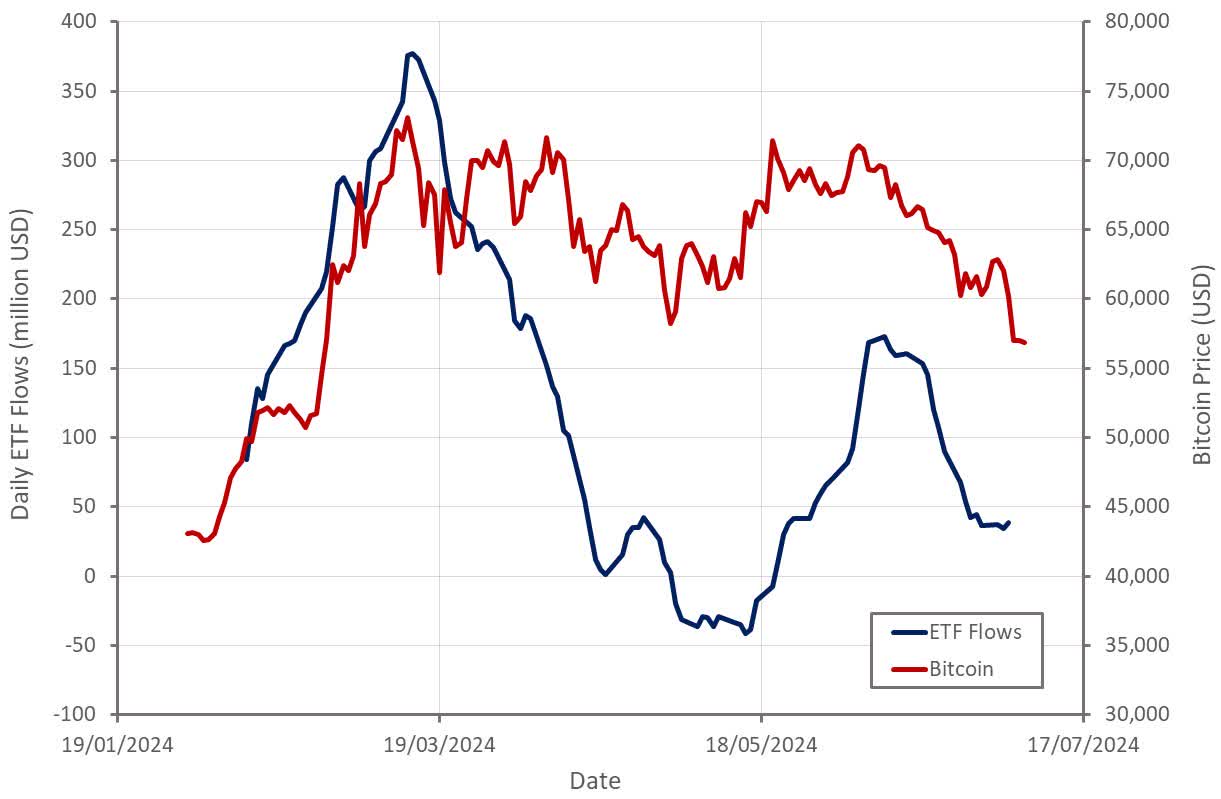

Ethereum's recent ETF approval could be considered a tailwind based on Bitcoin's experience. The launch of Bitcoin ETFs has probably opened up demand somewhat, with ETF flows an important driver of price at the moment. ETF inflows have fallen off in recent weeks, but Bitcoin's price appears to have led this move.

Figure 3: Bitcoin ETF Flows (source: Created by author using data from Yahoo Finance)

Spot Ethereum ETFs are expected to begin trading in the coming days/weeks. While there are likely to be inflows that are supportive of Ether's price, outflows from Grayscale's Ethereum Trust could weigh on the price initially. A similar dynamic occurred with Bitcoin, where there was 6.5 billion USD of outflows from Grayscale in the first month. The fact that Ethereum ETFs will not offer staking rewards to investors may also limit their appeal.

Relative Performance

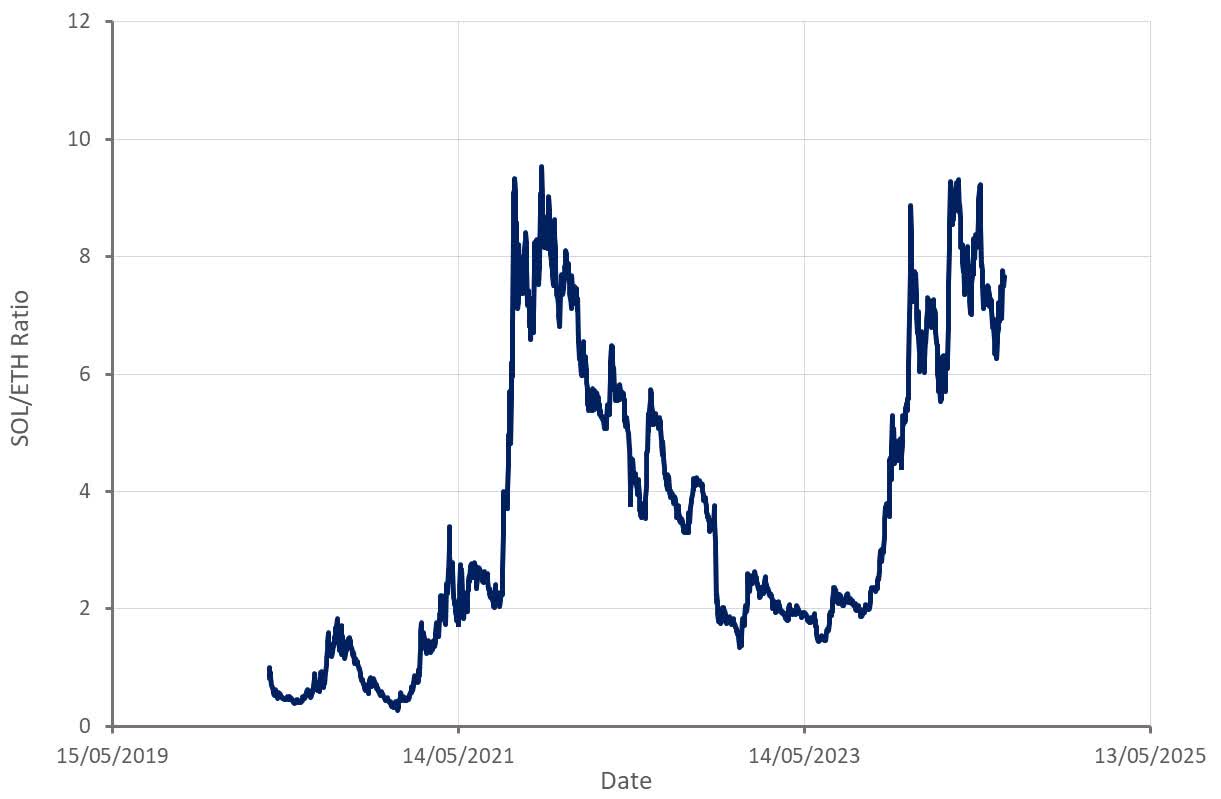

Ethereum's performance has been relatively poor in recent months/years in comparison to some cryptocurrencies, like Bitcoin and Solana. While some of this can likely be attributed to sentiment and financial conditions, Ethereum is also facing competition from within its own ecosystem as well as competition with other blockchains. This is less about competition from any particular chain, as I don't think there is a real competitor to Ethereum at this point in time. Rather, Ethereum is competing against many chains, some of which have managed to craft compelling narratives at various points in time (Solana, Avalanche, Binance).

With the approval of Ethereum ETFs, it has been suggested that other cryptocurrencies could follow, in particular Solana. Solana is still at risk of being classified a security though, and currently lacks a futures-based ETF in the US.

Figure 4: SOL/ETH Ratio (source: Created by author using data from Yahoo Finance)

Financial Conditions

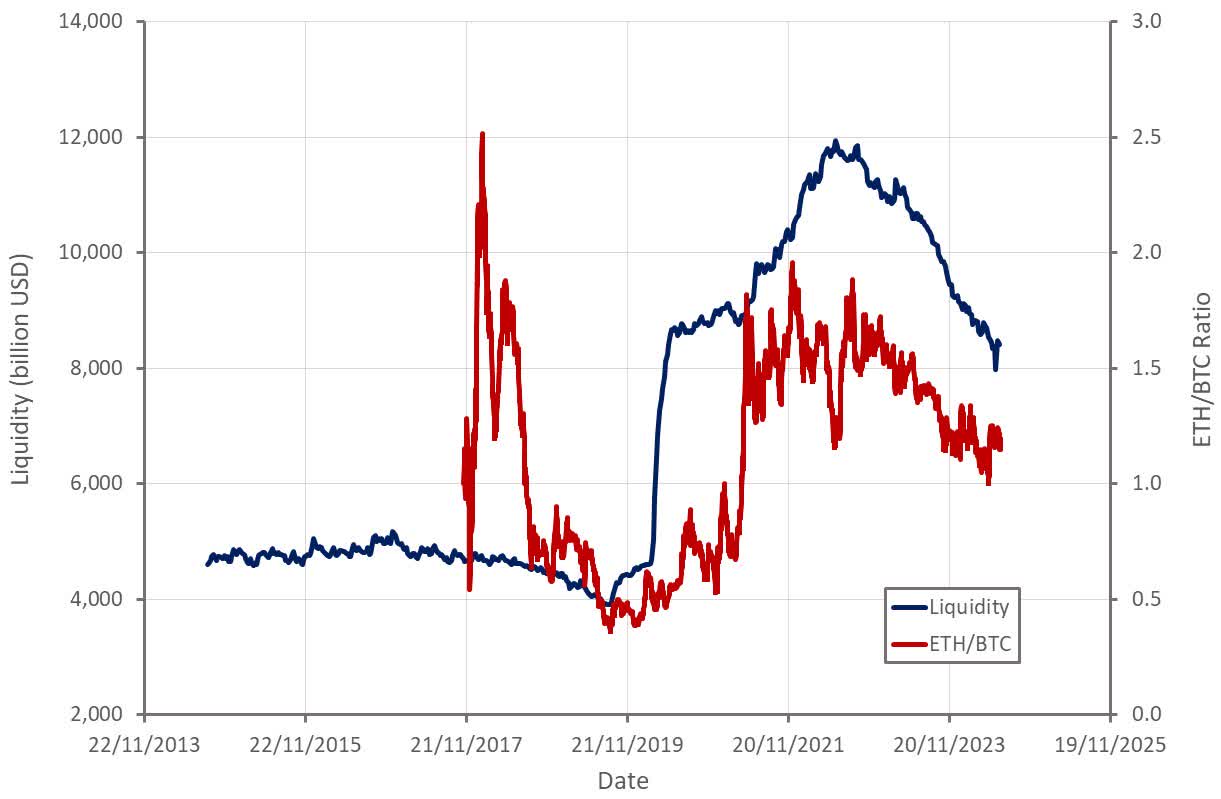

I think that monetary policy could be part of the reason for Ethereum's relatively poor performance in the current cycle. Interest rates remain elevated, and the Federal Reserve continues to drain liquidity from the system. This has had a dramatic impact on some assets and equities, although many assets and equities remain unaffected. Ethereum's underperformance relative to Bitcoin appears to have been correlated with the reduction in the Federal Reserve's balance sheet over the past few years.

Figure 5: Central Bank Liquidity and Performance of Ethereum Relative to Bitcoin (source: Created by author using data from Yahoo Finance)

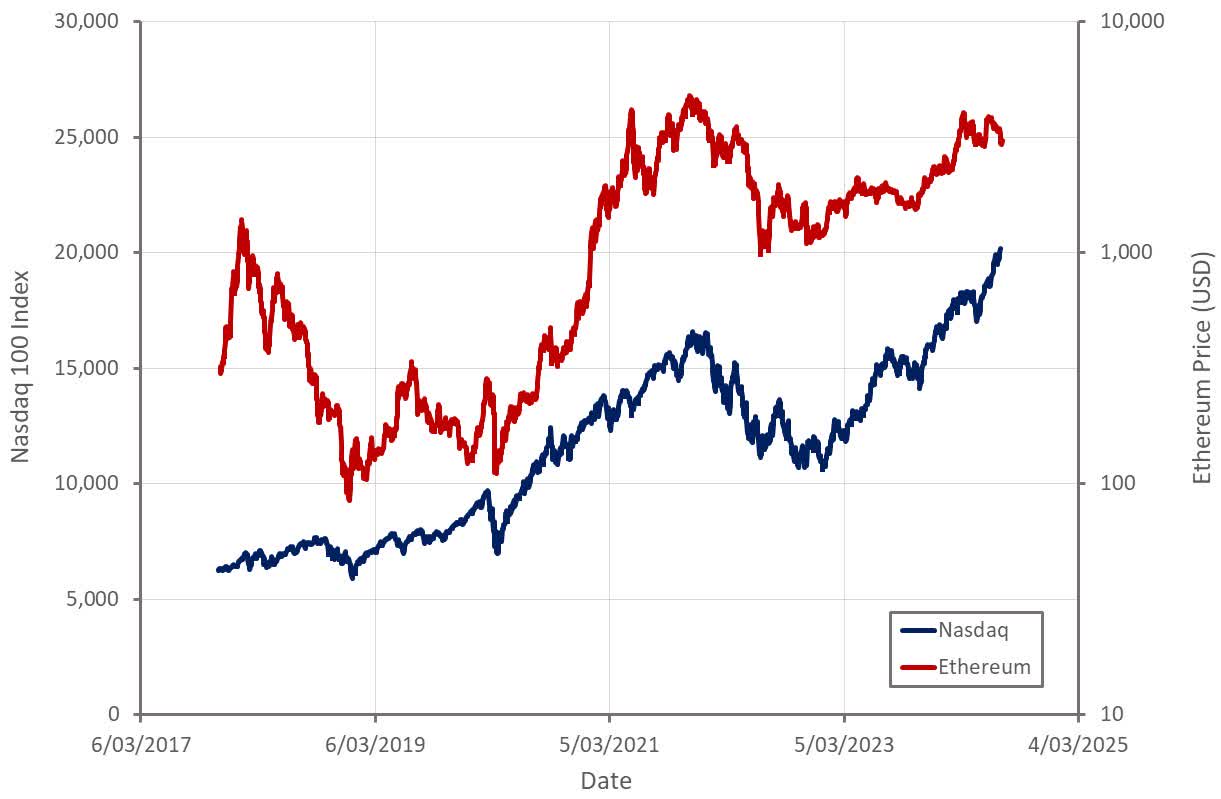

Ethereum is a risk-on asset and generally trades in line with other risk-on assets, like the Nasdaq index. The Nasdaq 100 index has significantly outperformed Ethereum in recent months, though. I think some of this is due to interest rates and quantitative tightening. AI has also been largely responsible for the strong performance of large cap tech stocks.

Figure 6: Nasdaq 100 and Ethereum Performance (source: Created by author using data from Yahoo Finance)

Ethereum Fundamentals

Aside from external forces, there also needs to be consideration of the fact that technical progress has been slow, and that real-world adoption is still limited. Ethereum is prioritizing decentralization, and as a result, scalability remains a problem. Proposals for improving throughput include sharding and moving transaction volumes to layer 2 networks. Sharding involves splitting up block producers so that each producer doesn't have to process every transaction.

Layer 2 networks, including sidechains and rollups, sit on top of Ethereum and are designed to provide faster and cheaper execution. They do this by bundling a group of transactions together and sending them to Ethereum as a single piece of data. Rollups execute transactions but do not need a consensus to verify them and are considered the best option for execution. Optimistic Rollups assume all data is valid and use fraud proofs to ensure transaction correctness, whereas zk-Rollups use zero-knowledge proofs for enhanced privacy and security.

Rather than trying to implement sharding, Ethereum is now pursuing danksharding. In danksharding, bundles of layer 2 rollup transactions are processed together without permanently storing all their data. The Dencun Upgrade was recently implemented, introducing proto-danksharding. Proto-danksharding reduces the amount of data permanently stored on chain. Separate "data availability" layers could also help with scalability by reducing the number of times data needs to be downloaded from the main network.

Ethereum's roadmap includes a number of changes that promise to improve performance, including:

- Single-Slot Finality - blocks are proposed and finalized in the same slot.

- Verkle Trees - combine "Vector commitment" and "Merkle Trees", enabling stateless clients. This is important as stateless clients only require a small amount of storage space to verify new blocks.

- Account Abstraction - Enables smart contracts to initiate transactions. This will support new features, like batch transactions and the ability to recover lost account keys.

These changes will likely take years to implement though and are unlikely to be drivers of price in the near term. Innovations that improve scalability and the user experience could help to drive adoption. I question whether technology is the only thing preventing broader adoption of cryptocurrencies, though.

Conclusion

Ethereum's performance during the current bull market has been relatively poor. While this could be the result of competition or uncertainty about the cryptocurrency's roadmap, I believe much of it has been due to monetary policy. Ethereum is a high beta, risk-on asset, and as such has been negatively impacted by high interest rates and quantitative tightening. With recent inflation data pointing towards a potential easing of monetary policy, there is a chance Ethereum's performance strengthens going forward. This is also supported by imminent ETF inflows and a reduced probability of Ethereum being classified as a security.

Ethereum lacks Bitcoin's digital gold narrative, though, and as such is more dependent on demonstrating real world usage. While lower fees are supportive of usage and transaction volumes, Ethereum is generally limited by throughput but is trying to deal with this through the use of layer 2 networks. Even if Ethereum becomes widely adopted, facilitating a large amount of economic activity, the current roadmap muddies valuation. Presumably most of the value will accrue to the base layer, as I have written before, but this is speculative. As such, I don't expect Ethereum's value to continue rising rapidly longer term, even if near-term factors are supportive.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.