REITs Rip As Rates Retreat

Summary

- U.S. equity markets climbed to record highs, while benchmark interest rates dipped to four-month lows as investors rotated from high-flying growth stocks into beaten-down value names following a cooler-than-expected CPI report.

- Headline CPI declined 0.1% month-over-month, which dragged the annual increase to below 3% for the first time since March 2021, while CPI ex-Shelter is again below the Fed's 2% target.

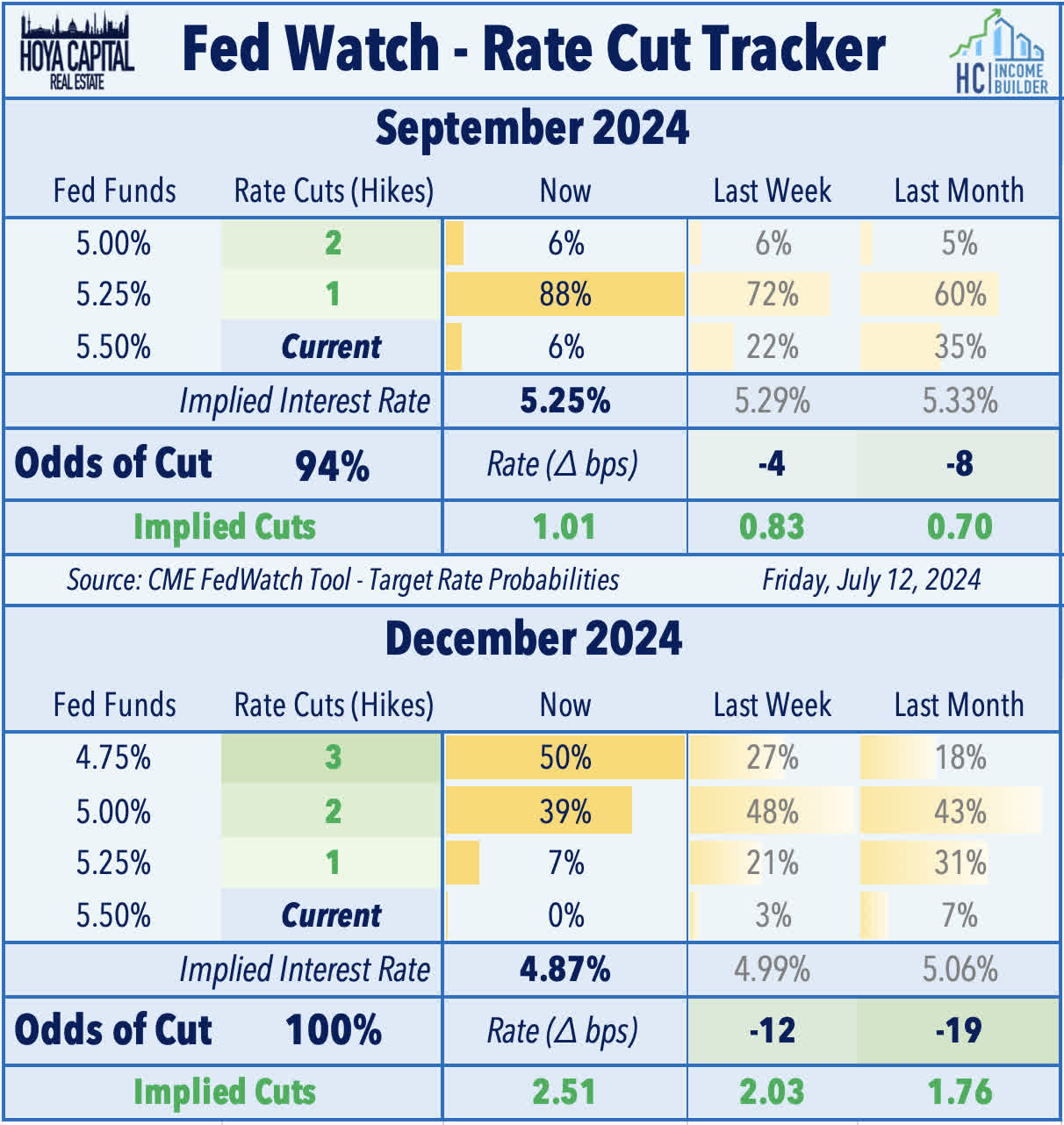

- Combined with recent softness in employment data and relatively dovish Fed commentary, markets now see at least two Fed rate cuts this year, with September now viewed as a near-lock.

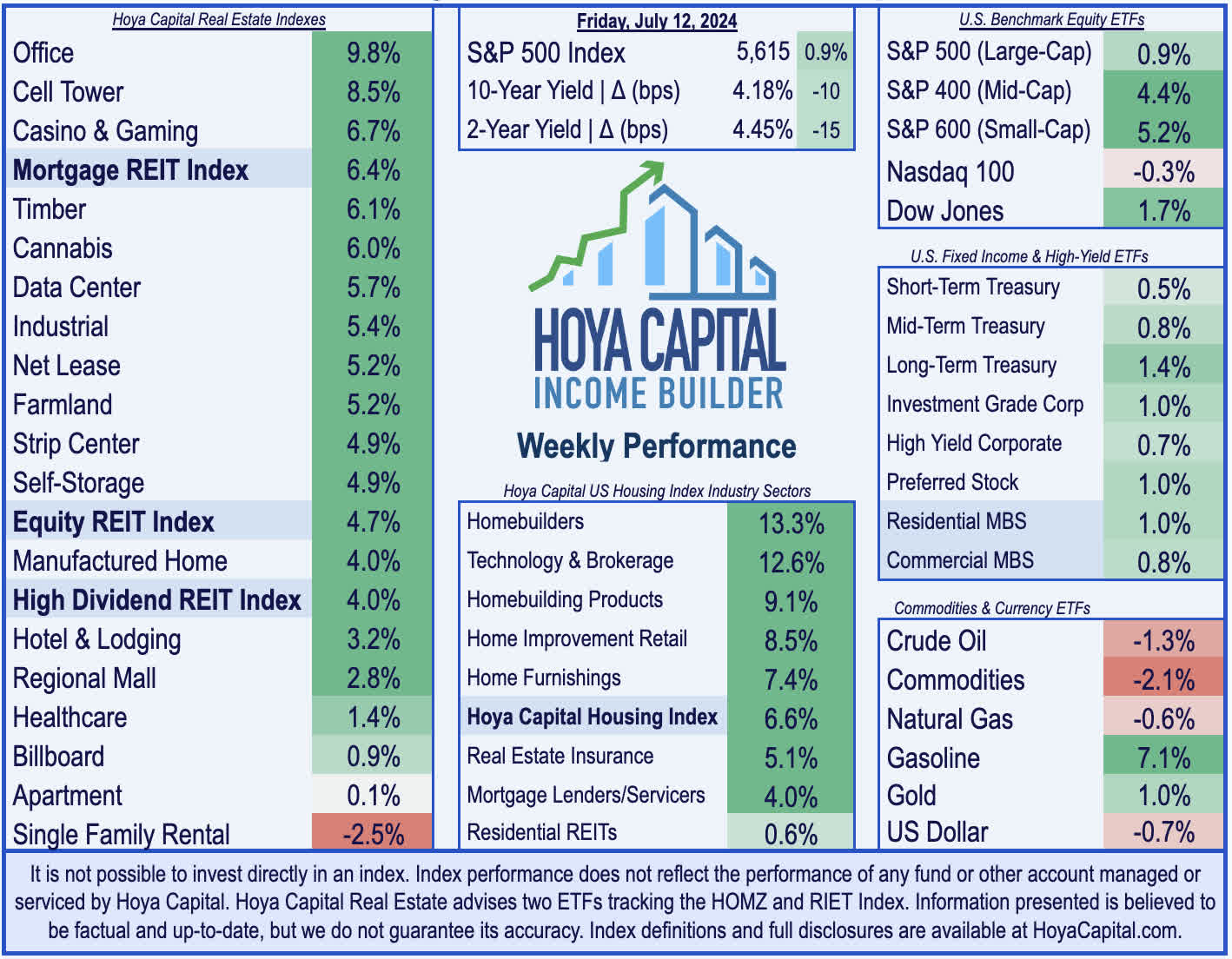

- Real estate equities - the most rate-sensitive market segment - delivered their strongest week of the year as weary investors finally saw some "light at the end of the tunnel."

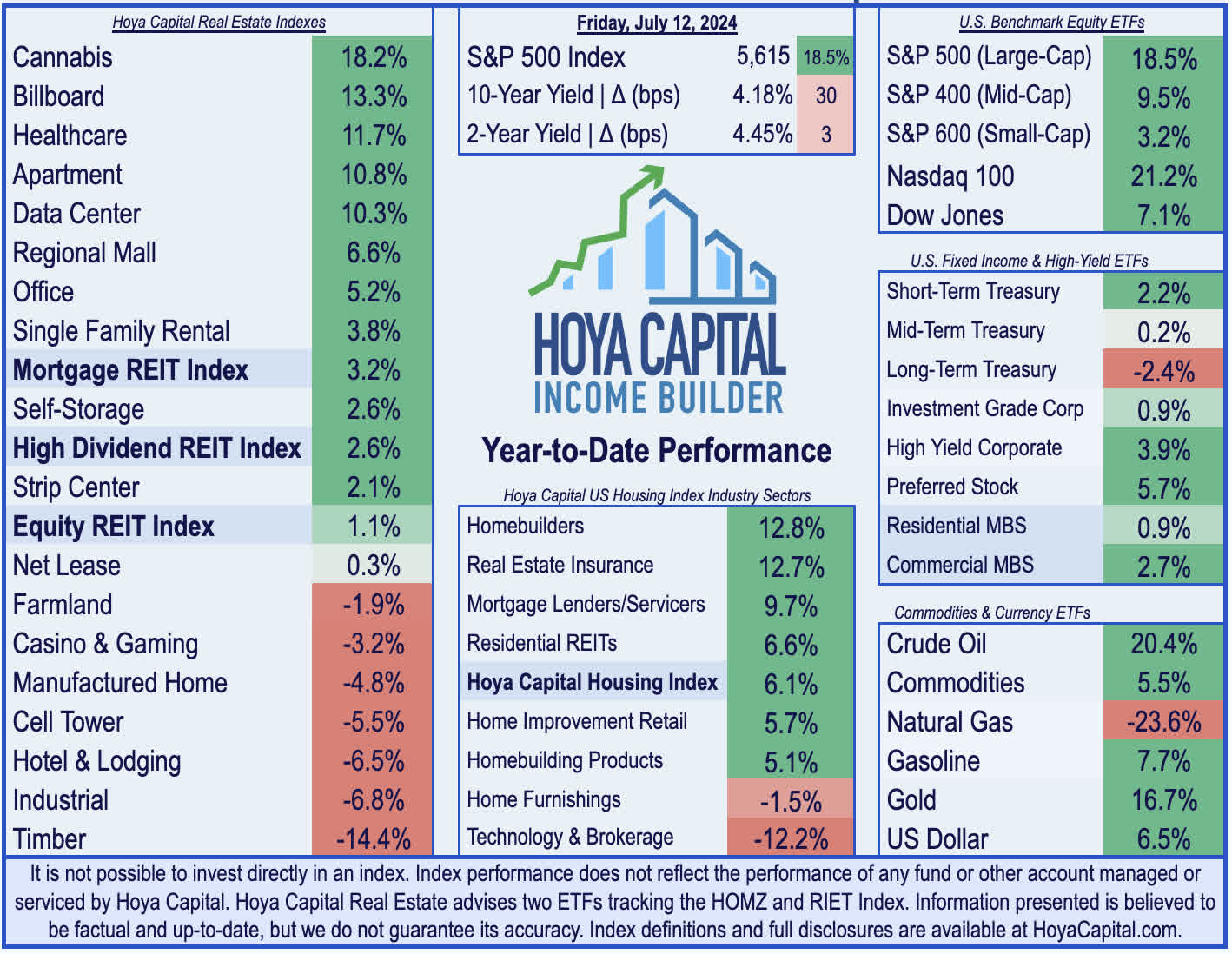

- The Equity REIT Index surged 4.7% on the week, with 17 of 18 property sectors in positive territory. Meanwhile, the Mortgage REIT Index rallied 6.4%, while Homebuilders surged more than 13% on the week.

Aerial_Views/E+ via Getty Images

Real Estate Weekly Outlook

U.S. equity markets climbed to fresh record highs this week, while benchmark interest rates dipped to four-month lows as investors rotated from high-flying growth stocks into beaten-down value names following a cooler-than-expected CPI report. Combined with recent softness in employment data, a lukewarm start to earnings season, and a relatively dovish tone from central bank officials, markets are now pricing in between two and three Fed rate cuts this year, with September now viewed as a near-certainty based on swaps pricing.

Hoya Capital

Posting another series of fresh record highs throughout the week, the S&P 500 gained another 0.9% to lift its year-to-date total returns to nearly 20%. "Value rotation" was the notable trend this week, however, as the Small-Cap 600 surged 5.2% on the week, while the Mid-Cap 400 rallied 4.4%, each chipping away at the historically wide underperformance gap relative to large-cap peers that have accumulated since the start of the Fed's rate hiking cycle. The mega-cap Nasdaq 100 - which has outperformed the Small-Cap index by 40 percentage points since March 2022 - finished lower by 0.3% on the week. Real estate equities - the most rate-sensitive market segment - delivered their strongest week of the year as weary investors finally saw some "light at the end of the tunnel" following a historically poor three-year stretch for U.S. REITs. The Equity REIT Index surged 4.7% on the week, with 17-of-18 property sectors in positive territory. Meanwhile, the Mortgage REIT Index rallied 6.4%, while Homebuilders surged more than 13% on the week.

Hoya Capital

Bond markets rallied following the cooler-than-expected CPI report, shrugging off a lukewarm PPI report on the following day, with traders interpreting the data as a "green light" for the Federal Reserve to begin cutting interest rates later this quarter. The 10-Year Treasury Yield dipped another 10 basis points this week to close at 4.18% - the lowest since late March, having now erased the entirety of the post-debate surge. The more-policy-sensitive 2-Year Treasury Yield dipped 15 basis points to 4.45%, the lowest since early March. Fed Chair Powell stuck to the recent script this week across two days of Congressional testimony, noting that while the "job is not done on inflation," the committee is focused on “considerable softening in the labor market.” Markets have interpreted the Fed's recent emphasis on softening labor market conditions - a shift in tone from its isolated focus on fighting inflation - as an indication that the central bank is laying the groundwork for rate cuts. Swaps markets are now pricing in a 94% probability that the Fed will cut rates in September - up from 75% last week - and imply 2.51 rate cuts in 2024 - the highest since April and up from 2.02 cuts implied last week.

Hoya Capital

Real Estate Economic Data

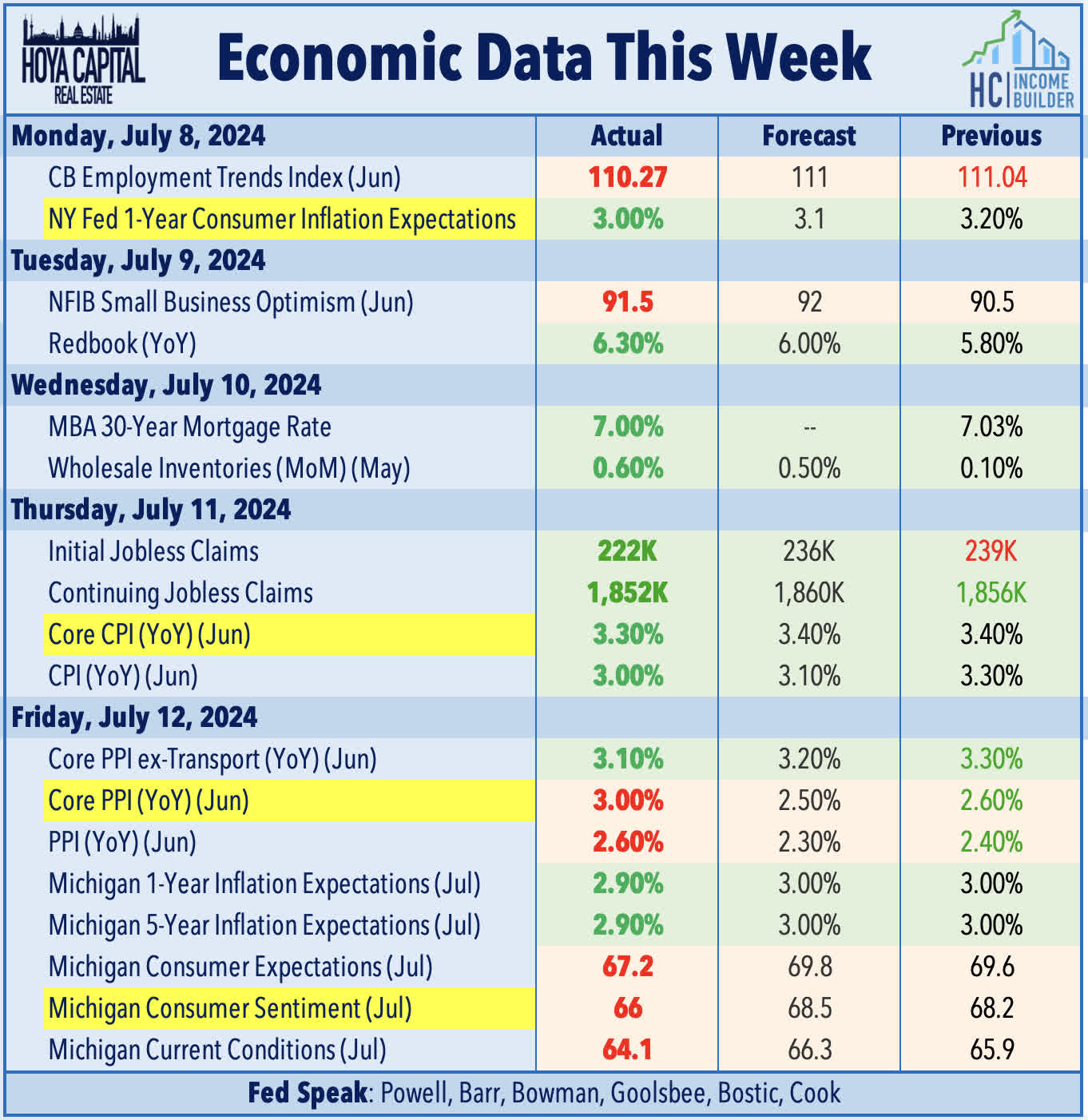

Below, we recap the most important macroeconomic data points over this past week affecting the residential and commercial real estate marketplace.

Hoya Capital

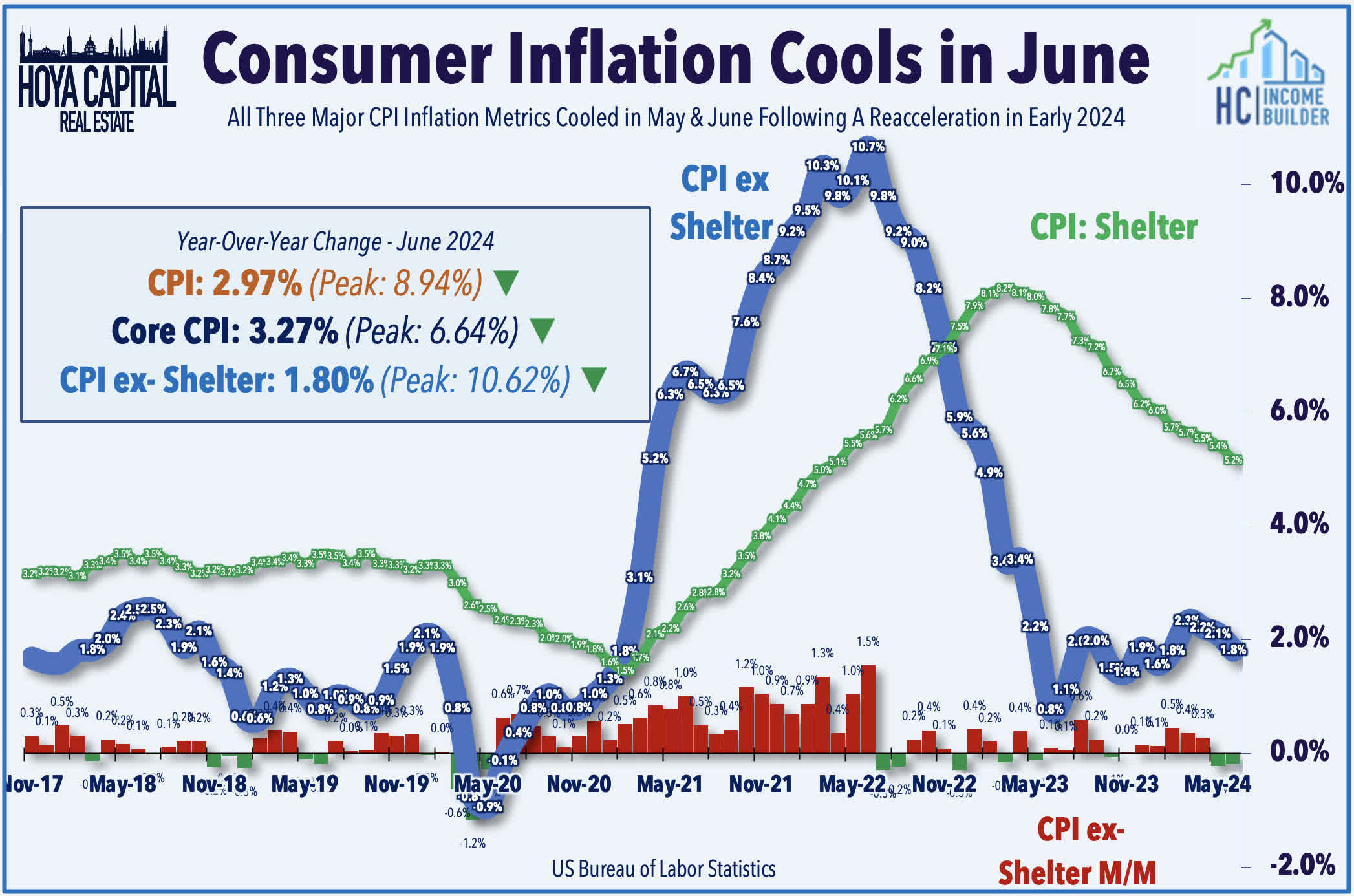

All eyes were on the Consumer Price Index report this week, which posted a downside surprise for a third straight month following three months of hotter-than-expected reports. Headline CPI declined 0.1% month-over-month and increased by 2.97% from a year ago - below consensus estimates of +0.1% and 3.10%, respectively. Core CPI - which excludes food and energy - rose 0.1% on the month and 3.27% on the year, which was also below expectations of 0.2% and 3.4%, respectively. Rents rose 5.2% from a year ago - still well above private market metrics showing 1-3% rent growth - but this annual increase was the lowest since late 2021. A month-over-month decline in energy prices was the most significant downside contributor, while airfares and used vehicle prices also contributed to the decline on the month. CPI-ex-Shelter - the metric we watch most closely given the substantial lags in the BLS' shelter inflation metrics - declined -0.2% for a second straight month, which dragged the year-over-year increase back down to 1.80%. We see a continued - but waning - distortion from the lagged recognition of shelter inflation, which accounted for effectively 100% of the increase in the Core CPI on a monthly basis and 60% of the increase on an annual basis.

Hoya Capital

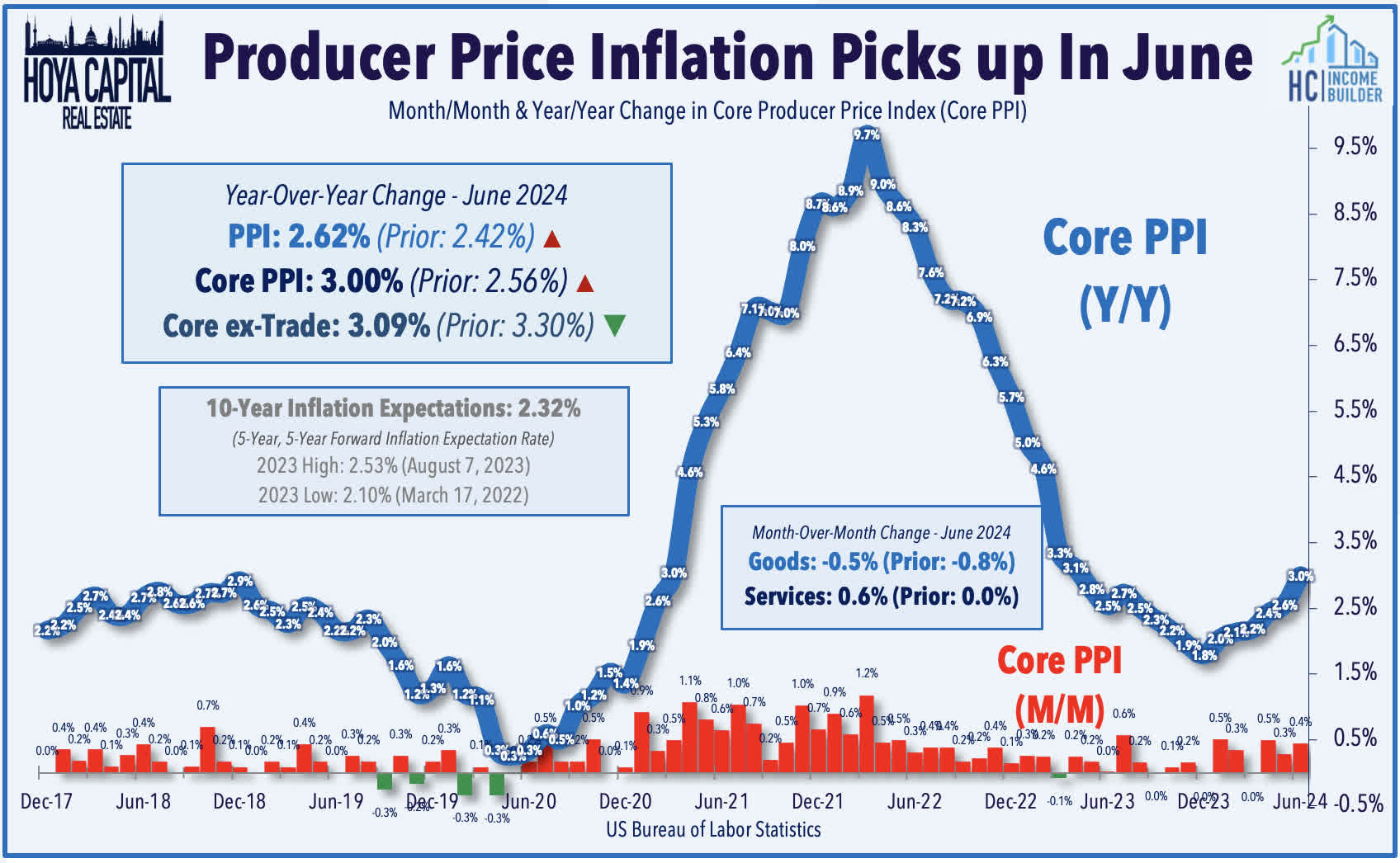

Following the cool CPI report on Thursday, the Producer Price Index report released the following day showed marginally hotter-than-expected wholesale price trends in June, a modest setback amid a stretch of encouraging inflation reports, but the upside surprise in PPI was less concerning under the surface. A jump in trade services costs drove the upside surprise - a typically "noisy' category on a month-to-month basis that measures changes in margins received by wholesalers and retailers. The Headline PPI increased 0.2% in June from the prior month and 2.6% on a year-over-year basis - above the consensus estimates of 0.1% and 2.3%, respectively. Core PPI followed the same pattern, posting a hotter-than-expected 0.4% monthly increase and 3.0% annual increase - above estimates of 0.2% and 2.5%, respectively. Core PPI ex-Trade exhibited more encouraging trends, showing that prices were unchanged in June and moderated to 3.1% on an annual basis. Notably, the handful of PPI categories that are included in the PCE inflation index - including physician and hospital care - were generally below estimates.

Hoya Capital

Equity REIT & Homebuilder Week In Review

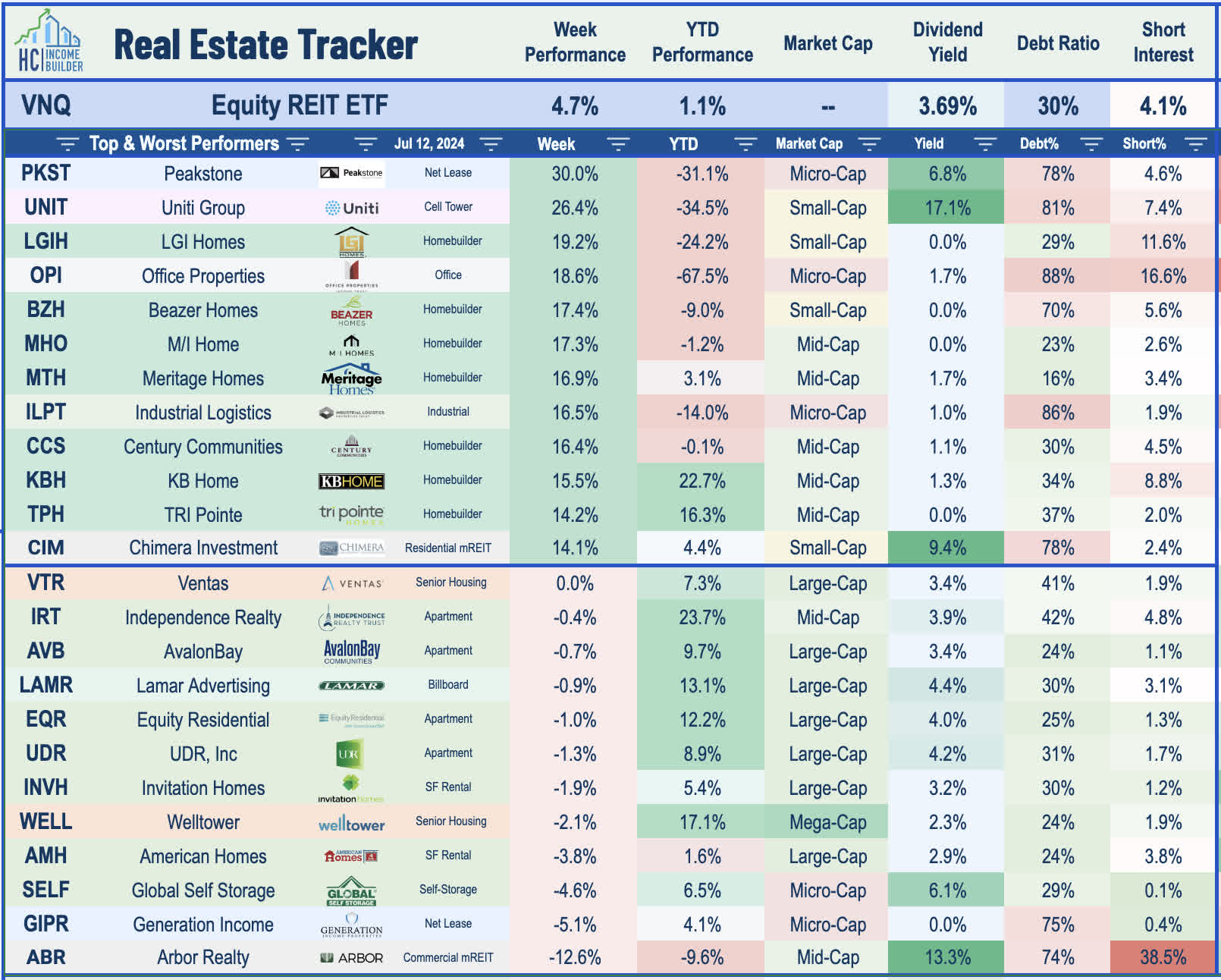

Best & Worst Performance This Week Across the REIT Sector

Hoya Capital

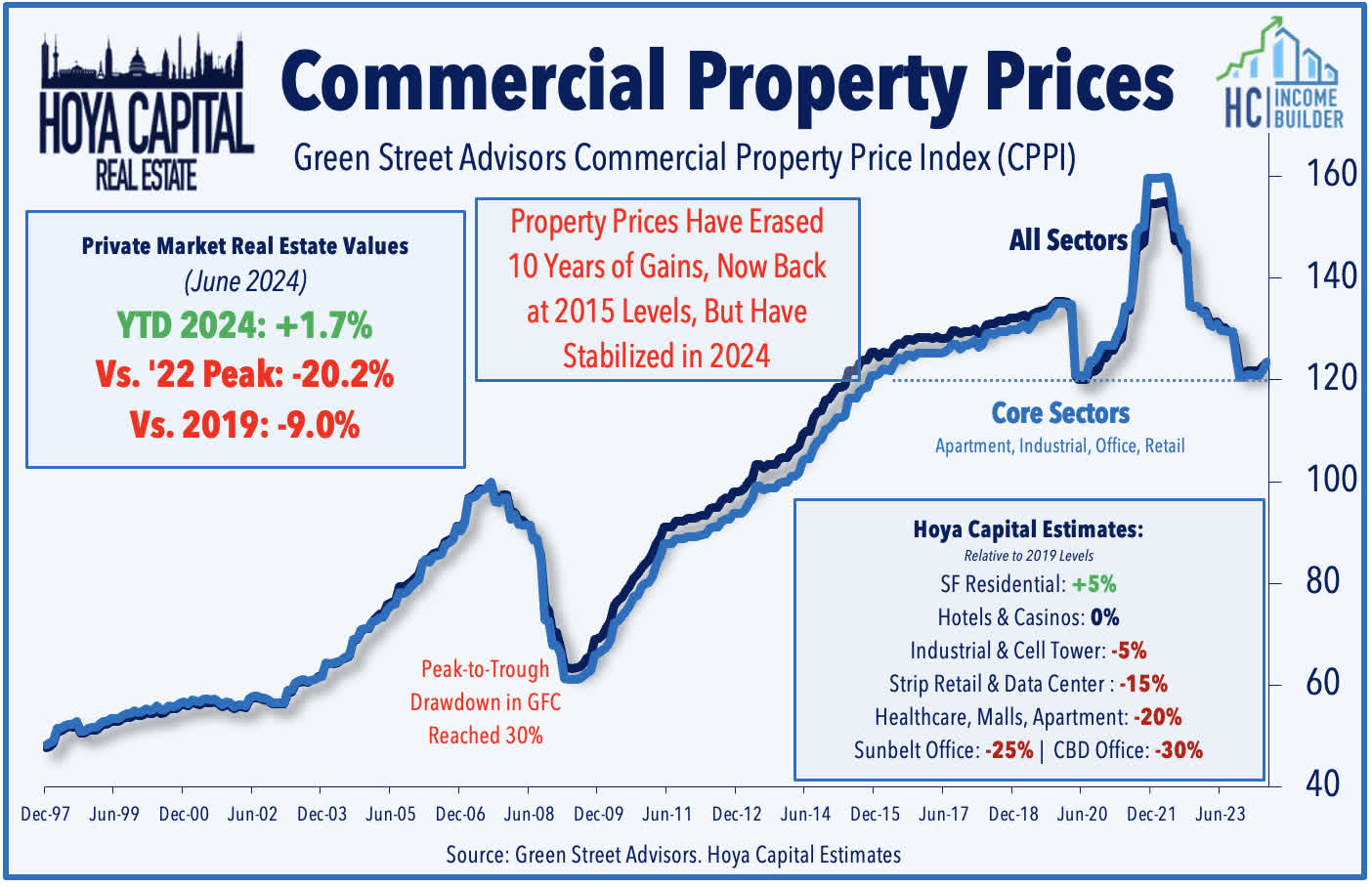

A bottom for commercial real estate? Green Street Advisors released its monthly Commercial Property Price Index ("CPPI") this week, which showed that private-market CRE valuations posted a back-to-back monthly increase for the first time since 2021. The report showed that the CPPI - which had dipped over 20% from the peak in 2022 to the lows in early 2024 - increased 0.7% in June after a similar 0.7% increase in May, which lifted the year-to-date increase in CRE values to 1.4%. Nearly two dozen REITs posted double-digit gains this week, led by many of the most beaten-down small-cap names, and the most rate-sensitive names across the office and net lease space. Notable gainers this week included 25%+ gains from Uniti Group (UNIT) and Peakstone (PKST) - which each erased about half of their year-to-date declines - and 12%+ gains from each of the four largest office REITs - Boston Properties (BXP), Vornado (VNO), Kilroy (KRC), and SL Green (SLG). As we'll discuss in our Earnings Preview report this weekend, real estate earnings season kicks off this coming week with results from a half-dozen names.

Hoya Capital

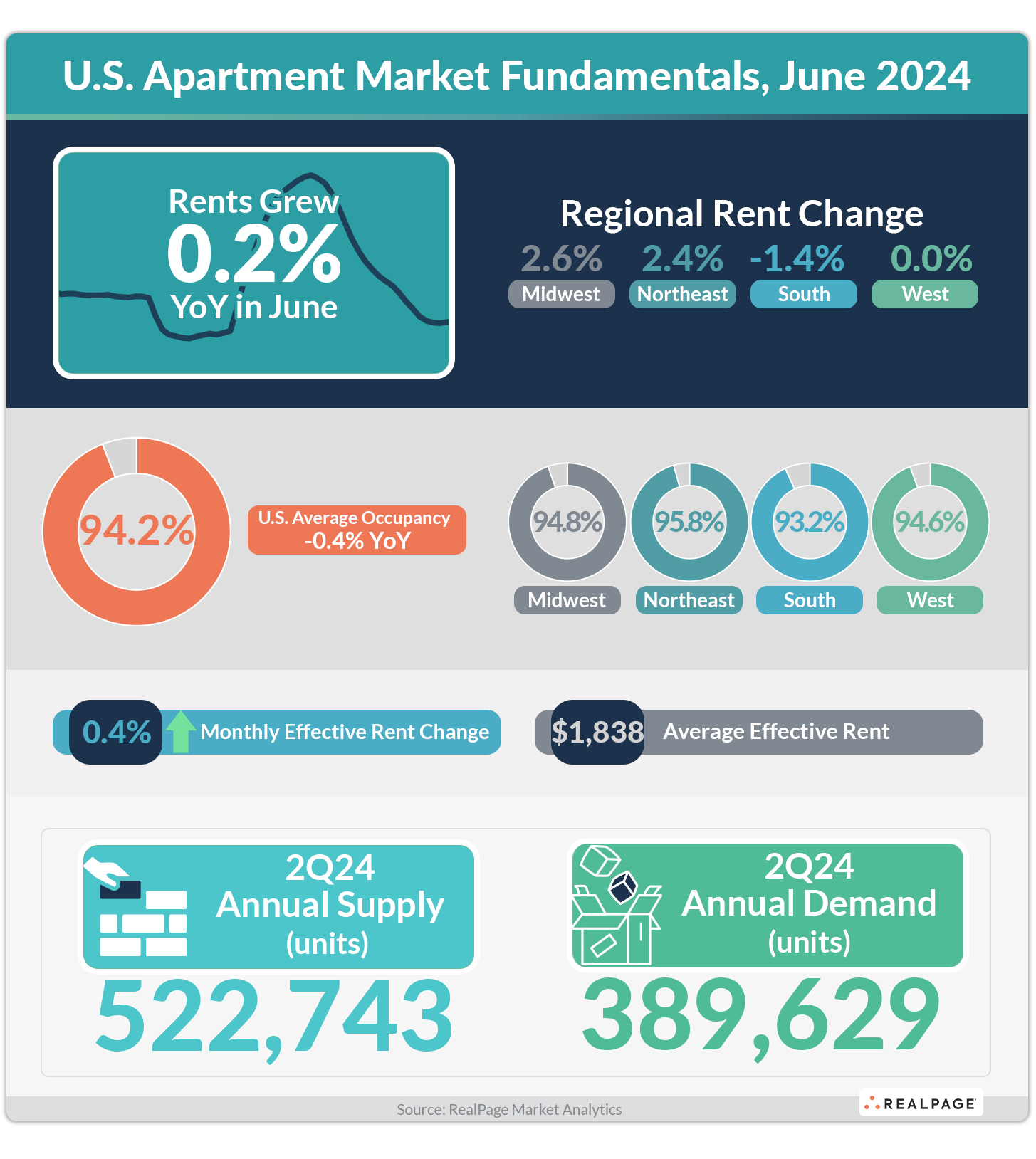

Apartment: A rebound in multifamily property values - which jumped 5% in June alone - has fueled the recent rebound in overall real estate valuations. For multifamily, oversupply concerns have eased in recent months as new construction starts have slowed substantially while demand has been particularly robust. RealPage reported this week that apartment demand "surged" in the second quarter, which has rapidly closed the supply-demand gap. Some 390,000 apartment units were absorbed over the past 12 months, which ranks as the eighth-largest figure on record, trailing only the pandemic-era boom from mid-2021 to mid-2022, and a brief period in 2018 and 2000. The booming demand comes at a critical time for the multifamily market, which has seen a record quantity of new units delivered - more than a half-million - over the past twelve months, with this pace expected to continue until early 2025 before moderating into 2026. The strong demand has also prevented a further deterioration in rental rates, which remained marginally positive on a year-over-year basis in June, with 0.1% annual growth at the national level. RP highlights an especially strong recent correlation between rent growth and supply levels over the past quarter, with high-supply cities - including Austin, Atlanta, and Dallas - continuing to see rents decline, while limited-supply cities have posted mid-single-digit rent increases.

Hoya Capital

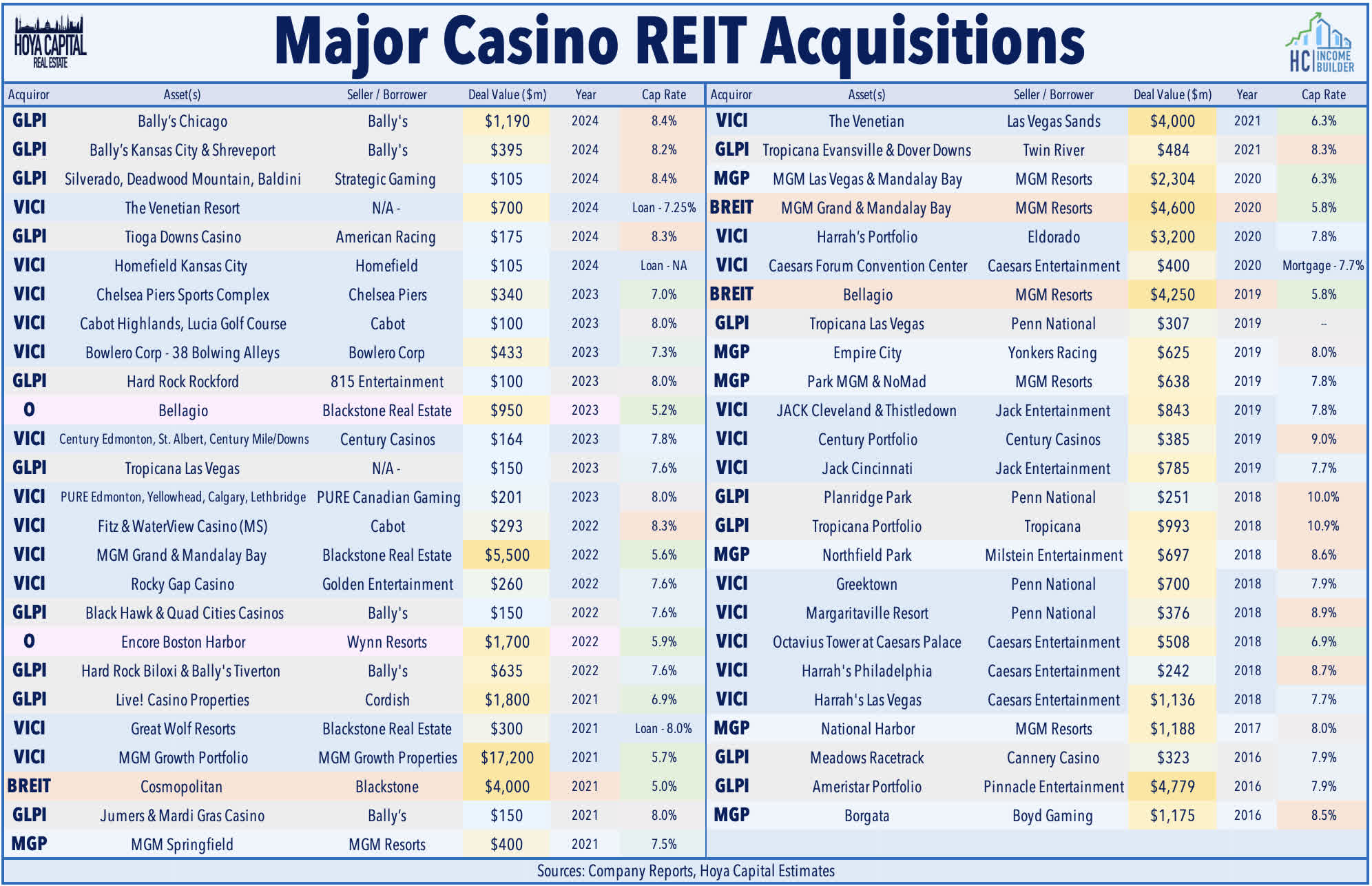

Casino: Gaming and Leisure Properties (GLPI) - which we own in the REIT Focused Income Portfolio - rallied 8% this week after it announced a series of deals with casino operator Bally’s Corporation (BALY) totaling over $1.5B. First, GLPI will acquire the real property underlying Bally’s Kansas City and Bally’s Shreveport resorts in a sale-leaseback deal for $395M in total consideration. The properties - which will continue to be operated by Bally's - will be added to the existing master lease agreement with an incremental annual rent of $32.2M, representing an 8.2% initial cash capitalization rate. Second, GLPI also reached a $1.19B deal to acquire the land and fund the development of a new Bally's casino in Chicago at a total cash yield of 8.4%. GLPI will pay $250M for the pre-developed land, upon which rent will commence under a new lease carrying a 15-year initial term with an initial cash yield of 8.0%. GLPI will then fund the construction hard costs of up to $940M at an 8.5% initial cash yield. The rent coverage for the lease is expected to be in the range of 2.0x – 2.4x. Third, GLPI and Bally’s agreed to adjust GLPI’s existing purchase option for Bally’s Lincoln to reflect a purchase price of $735M, reduced from $771M. The adjustment results in the initial cash yield of 8.0% (previously 7.6%). GLPI has also been granted a call right beginning in October 2026, which gives GLPI the option to acquire the property prior to the expiration of the current option period.

Hoya Capital

Industrial: A pair of industrial REITs provided preliminary operating metrics this past week, which both showed relatively solid leasing activity in the second quarter, pushing back on concerns of more significant weakness in logistics demand. Terreno (TRNO) rallied more than 7% after it reported that it signed 500k SF of new and renewed leases in Q2 (down slightly from the 700k SF in Q1), while achieving cash rent growth of 45.9% (down from 47.2% in Q1). TRNO's same-store occupancy stood at 96.0% in Q2, down slightly from 96.2% in Q1 and the prior year rate of 98.1%. Small-cap Plymouth (PLYM) rallied 6% on the week after its updated showed continued progress in releasing its relatively large slate of leases set to expire this year. PLYM commenced 1.81M SF of leases during the quarter - comprised of 1.61M SF of renewals and 201k SF of new leases - on which it will record an 18.8% blended increase in cash rental rates (18.8% on renewals and 19.5% on new leases). PLYM - which at one point last year had nearly 20% of its leases expiring in 2024 - noted that it signed an incremental 680k SF of leases set to commence this year, having now renewed 63.3% of total 2024 expirations, up from 55.9% at the end of the first quarter. PLYM also noted that it has "six active prospects" for its large 770k SF vacancy in St. Louis that will be vacated by its current tenant at the end of July. Total portfolio occupancy at the end of Q2 stood at 97.0% - up 10 basis points from the first quarter.

Hoya Capital

Net Lease: Several net lease REITs were among the leaders this week as well after providing preliminary second-quarter metrics. Gladstone Commercial (GOOD) rallied 4% after it reported that it collected 100% of rents in Q2 with a quarter-end occupancy rate of 98.5% - down slightly from the 98.9% rate at the end of Q1. Leasing activity has now totaled 2.4M square feet since the start of the year, achieving blended rent increases of 46% compared with the expiring leases. On the M&A front, GOOD announced a series of office property sales and industrial property acquisitions. GOOD purchased a 142k square foot industrial property in Warfordsburg, PA for $11.7M at a 12.3% cap rate. GOOD also sold four office buildings totaling nearly 400k SF at undisclosed valuations. Elsewhere, Global Net Lease (GNL) gained 4% on the week after it provided an update on its strategic disposition plan, noting that it has now completed $321M of dispositions through Q2 2024, including $62M of vacant assets. Ground lease REIT Safehold (SAFE) - among the most rate-sensitive names given the particularly "bond-like" characteristics of ground leases - surged 11% after it announced it has closed on ground leases to facilitate the development of four housing communities in California totaling 781 units.

Hoya Capital

Healthcare: Medical office building ("MOB") owner Healthcare Realty (HR) gained 3% this week after it provided a business update with preliminary second-quarter operating metrics. HR noted that it has signed new leases totaling 432k SF (down slightly from the 440k SF in Q1), including multi-tenant absorption of 122K (up from 57k in Q1). HR noted that multi-tenant occupancy has now increased 371k SF over the past three quarters, representing approximately 110 basis points of positive absorption. HR also noted that bankrupt hospital operator Steward Healthcare has "paid substantially all rent owed for June and July" but HR will set aside a $3M reserve for unpaid rent from March and April. Rent owed for May following Steward’s bankruptcy filing on May 6 is expected to be paid as part of the outcome of the bankruptcy process. Medical Properties (MPW) - which is the healthcare REIT with the most exposure to Steward - has rallied nearly 8% this week on the news. This week, Steward confirmed that it is currently under federal investigation, with CBS reporting that prosecutors from the U.S. Attorney's office in Boston are probing "various allegations including fraud and violations of the Foreign Corrupt Practices Act." Steward operates 31 hospitals nationwide, and is the third-biggest hospital operator in Massachusetts.

Hoya Capital

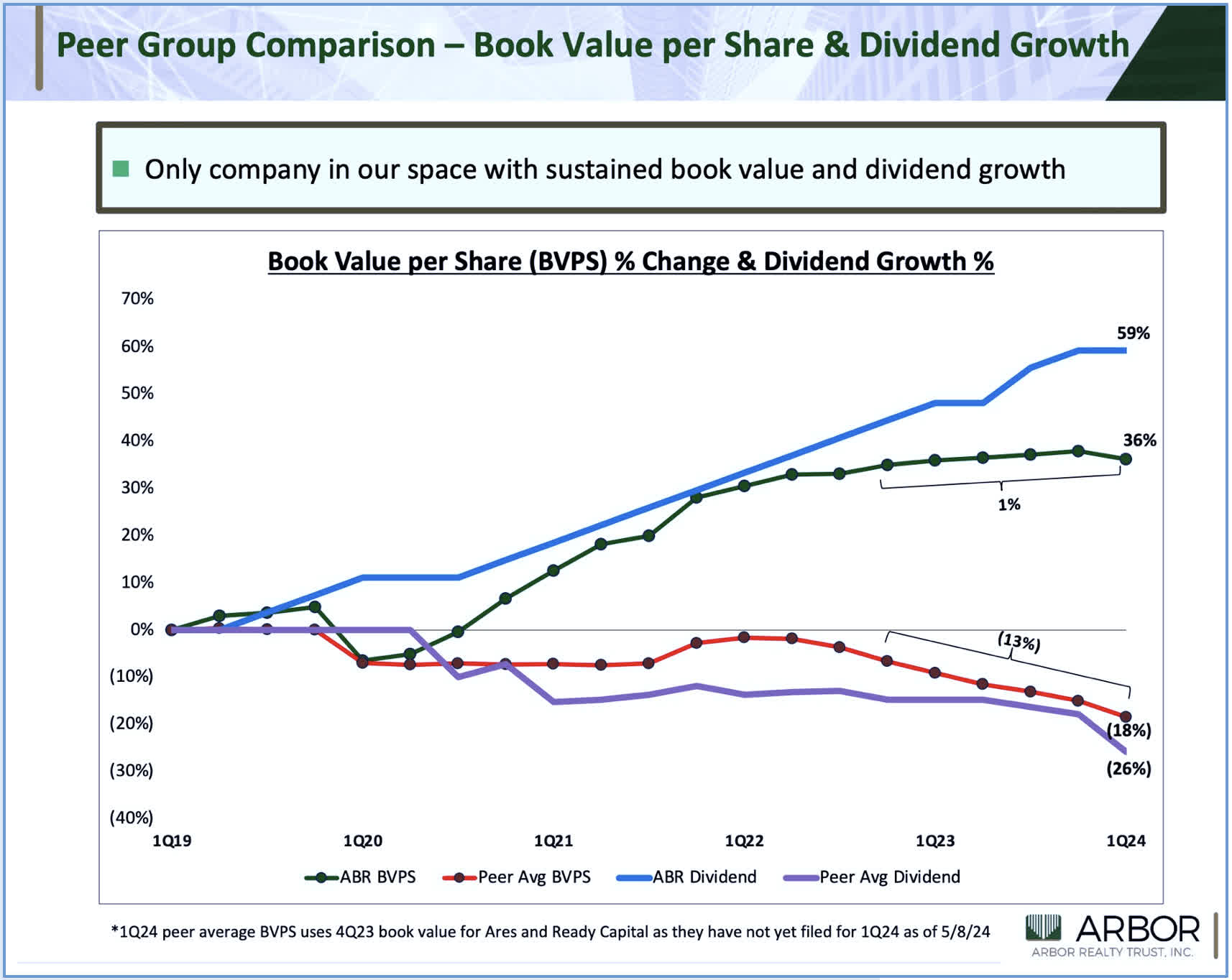

Mortgage: On a related note, multifamily lender Arbor Realty (ABR) - which has been in the cross-hairs of short-sellers over the past year - dipped 12% this week after Bloomberg reported that the firm is being probed by Federal prosecutors, who are "inquiring about lending practices and the company’s claims about the performance of their loan book." Short-focused Viceroy initially targeted Arbor in November 2023 with a short report that ABR's "entire loan book is distressed and underlying collateral is vastly overstated." Viceroy doubled down on the claims this past May, flagging a foreclosed apartment portfolio in Houston, which Viceroy claims Arbor fraudulently acquired with an off-balance sheet entity. ABR's CFO noted in May that this specific transaction occurred in the second quarter and would be "appropriately disclosed" in the coming report. Arbor - which remains the best-performing mortgage REIT on a 5-year and 10-year total return basis - had previously been the target of a short report from Ningi Research. REIT short sellers have delivered mixed results in recent years with notable high-profile "misses" on Welltower (WELL) and data center REITs in which claims of fraud and/or significant overvaluation were generally proven to be unfounded. In several of these instances, short-sellers focus efforts on enlisting regulators to announce inquiries or investigations into the targeted companies.

Hoya Capital

Manufactured Housing: UMH Properties (UMH) - which we own in the REIT Focused Income Portfolio - rallied 4% on the week after it provided preliminary second-quarter operating metrics showing a continued uptick in occupancy rates. UMH - the smallest of three manufactured housing REITs behind Sun Communities (SUI) and Equity LifeStyle (ELS)- noted that it converted 144 new homes from inventory to revenue-generating rental homes during the quarter, now owns approximately 10,100 rental homes with an occupancy rate of 95.0%. During the quarter, UMH sold 105 homes, of which 35 were new home sales, driving gross home sales revenue of $8.8 million as compared to $8.2 million last year. Year to date, overall occupancy has increased by 196 units to 87%, including an increase of 64 units in the second quarter, representing an increase of 195 basis points in its occupancy rate. UMH noted that occupancy gains and rent increases have resulted in a 10.0% increase in total rental revenues in June compared with a year earlier.

Hoya Capital

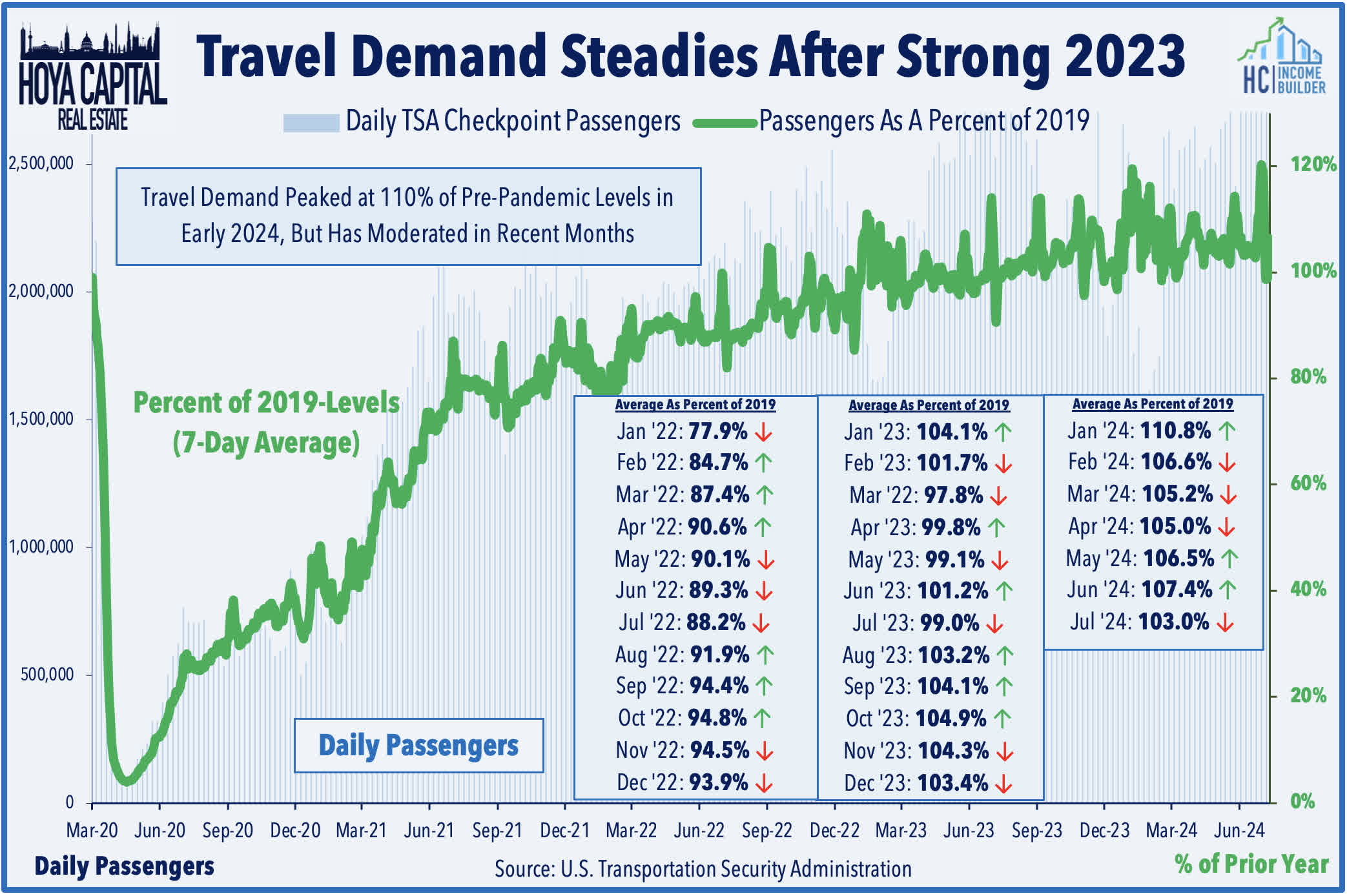

Hotel: Small-cap Ashford Hospitality (AHT) was also among the better performers this week after it provided preliminary second-quarter operating results showing a modest acceleration in comparable metrics. AHT notes that its comparable Revenue Per Available Room ("RevPAR") increased 1.4% year-over-year in the second quarter, an improvement from the -0.9% comparable decline in the first quarter. The outperformance was front-loaded in the quarter, however, with April posting gains of +3%, which cooled to +1.4% in May and -0.1% in June. Elsewhere, Xenia Hotels (XHR) gained 3% after it announced that it completed the sale of the 107-room Lorien Hotel & Spa in Alexandria, VA, for $30M ($280,000 per key), which represents a 21.3x multiple and a 3.1% capitalization rate on EBITDA. Recent TSA Checkpoint data shows relatively steady travel demand thus far in 2024, with domestic throughput hovering around 105% of pre-pandemic levels. Trends over the past several weeks have been slightly softer, however, with July currently pacing to be the weakest in over a year as compared to pre-pandemic levels.

Hoya Capital

2024 Performance Recap

Despite the recent outperformance, real estate equities continued to lag considerably behind the broader equity benchmarks so far this year, and remain the worst-performing GICS equity sector. The Equity REIT Index is higher by 1.1% this year, while the Mortgage REIT Index is higher by 3.2%. This compares with the 18.5% gain on the S&P 500, the 9.5% gain for the Mid-Cap 400, and the 3.2% gain for the Small-Cap 600. Within the REIT sector, 11 of the 18 property sectors are higher for the year, led by Speciality, Healthcare, and Residential REITs - while Timber, Industrial, Hotel, and Cell Tower REITs have lagged on the downside. At 4.18%, the 10-Year Treasury Yield is higher by 30 basis points on the year, while the 2-Year Treasury Yield has risen 3 basis points to 4.45%. The Bloomberg US Bond Index has posted total returns of 0.8% this year, and within the bond market, credit has continued to notably outperform duration. WTI Crude Oil is higher by 20.4% this year, lifting the Commodities complex higher by 5.6%.

Hoya Capital

Economic Calendar In The Week Ahead

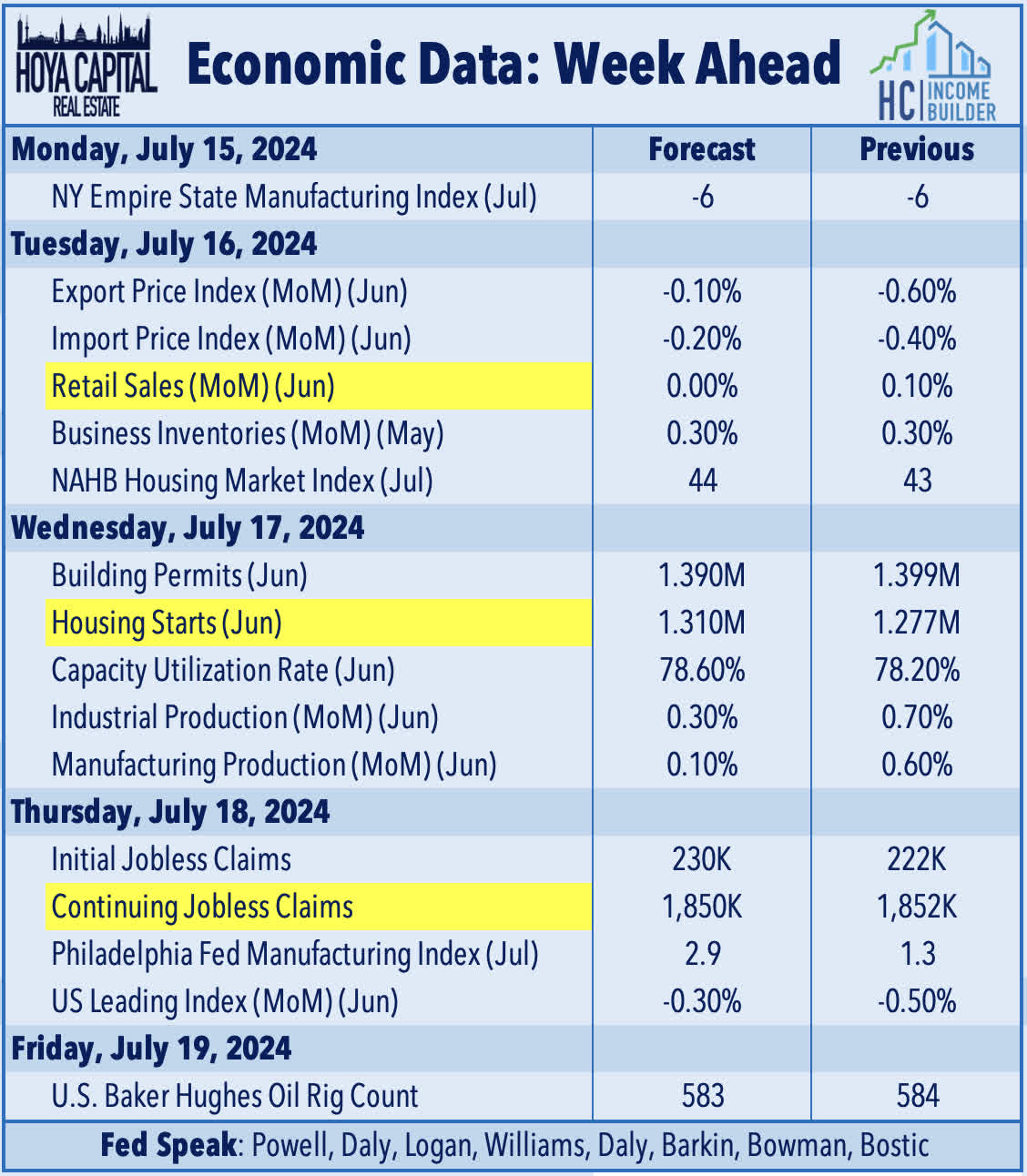

Following a busy slate of inflation data this past week, the health of the U.S. consumer and the state of the housing market will be the primary focus in the week ahead. On Tuesday, we'll see Retail Sales data, which is expected to show another month of sluggish trends in June following two straight disappointing months. Adjusted for inflation, "real" retail sales have declined about 1% year-to-date compared with 2023. On Tuesday, we'll also see NAHB Homebuilder Sentiment data, which is expected to show that builder optimism remained muted in early July, particularly given that the survey period occurred before the latest retreat in mortgage rates. On Wednesday, we'll see Housing Starts and Building Permits data, which is also expected to show that new construction activity remained slow in June, particularly in the multifamily segment, which has posted decade-low levels of starts in recent months. We've postulated that the Fed's rate hiking cycle may have actually worsened the longer-term inflation outlook given the resulting pull-back in housing supply, and the substantial weight of housing in the CPI index. We'll also be watching Jobless Claims data on Thursday to see if this past week's surprisingly solid report was merely a holiday-impacted blip.

Hoya Capital

For an in-depth analysis of all real estate sectors, check out all of our quarterly reports: Apartments, Homebuilders, Manufactured Housing, Student Housing, Single-Family Rentals, Cell Towers, Casinos, Industrial, Data Center, Malls, Healthcare, Net Lease, Shopping Centers, Hotels, Billboards, Office, Farmland, Storage, Timber, Mortgage, and Cannabis.

Disclosure: Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index. Index definitions and a complete list of holdings are available on our website.

Hoya Capital

Editor's Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

- Risdawaty purba·2024-07-19bkkkLikeReport