Cintas Corporation: Still A Bad Fit, Even In Light Of Great News

Summary

- Cintas Corporation saw its shares spike by 5.4% after positive Q4 results and strong 2025 guidance from management.

- Revenue, profits, and cash flows all rose significantly in 2024, with expectations for continued growth in 2025.

- Despite the positive outlook, shares are considered expensive and are rated as a 'sell' due to high valuation compared to similar companies.

JHVEPhoto

July 18th ended up being a really great day for shareholders of Cintas Corporation (NASDAQ:CTAS). The company, which focuses on renting out and selling uniforms to businesses, not to mention other products and services like restroom supplies, mops, first aid kits, and more, saw its shares spike by 5.4%. This was in response to management reporting financial results for the final quarter of the company's 2024 fiscal year and providing guidance for what 2025 might look like. Based on management's own guidance, the 2025 fiscal year is going to be even better than 2024 was. But this doesn't necessarily make the company a great prospect for investors at this time.

To be perfectly clear, I consider Cintas to be a high-quality business. In the long run, I fully expect it's shares to continue rising. But as I detailed in a prior article, published in March of this year, shares do look to be very expensive. In fact, I even went so far as to downgrade the stock from a ‘hold’ to a ‘sell’. But since then, the firm has outperformed the broader market, with shares up 10.5% at a time when the S&P 500 is up 5.7%. In light of this and in spite of the positive outlook provided by management, I do still think that shares deserve to fall from here. Because of this, I have decided to keep the business rated a ‘sell’ for the time being.

A great time for Cintas

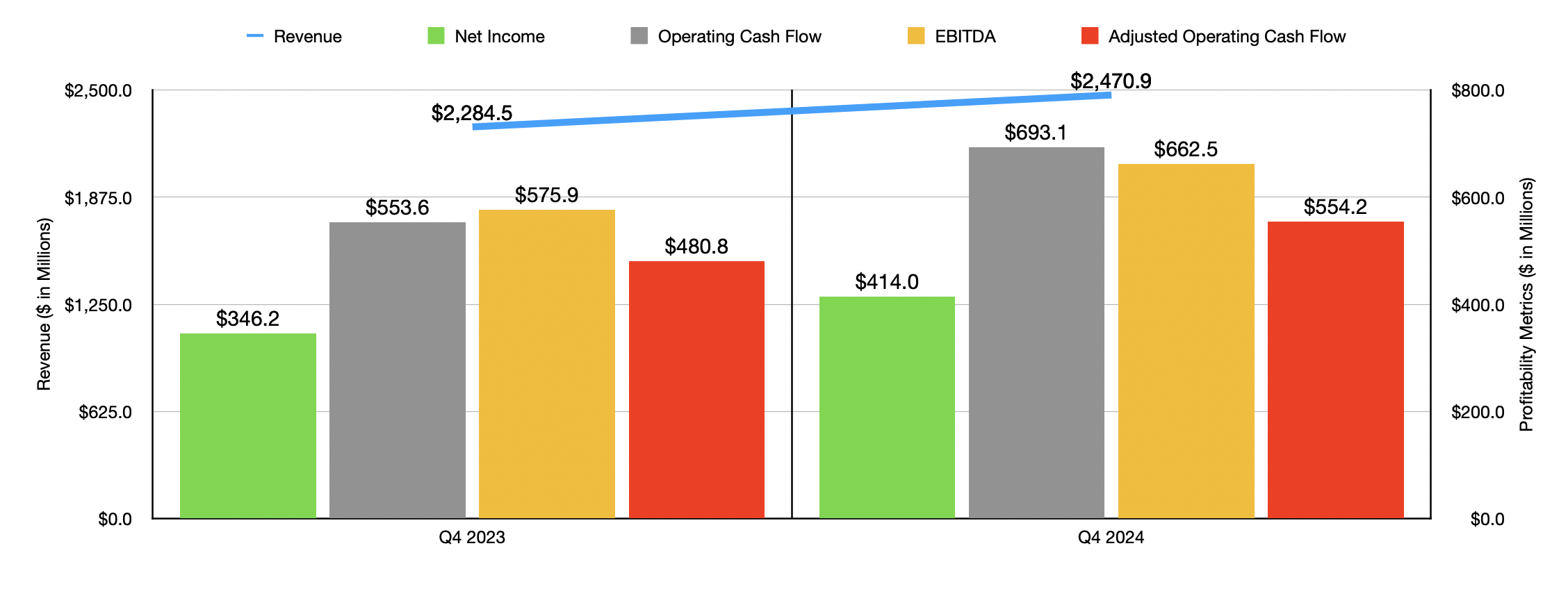

Fundamentally speaking, things are going really well for Cintas at this point in time. For the final quarter of the company's 2024 fiscal year, management reported revenue of $2.47 billion. In addition to being 8.2% above the $2.28 billion the company reported for the final quarter of its 2023 fiscal year, sales also came in line with analysts’ expectations. The largest part of the company has always been its uniform rental and facility services activities.

Author - SEC EDGAR Data

During the quarter, revenue from these operations came in at $1.91 billion. That represents an increase of 7.8% over the $1.77 billion reported one year earlier. Management attributed this to strong growth from new customers, as well as increased demand from existing customers. The latter was largely attributable to the addition of products and services to the company’s slate of options. Management even went so far as to say that growth was consistent across all major product categories, which only underscores how robust and widespread demand for its services actually is.

There was, of course, growth elsewhere as well. Revenue involving first aid and safety services activities grew by 11.2% year over year, climbing from $249.8 million to $277.6 million. Unfortunately, management did not really provide much in the way of detail regarding what caused this upside. In addition to this though, the firm talked about its ‘all other’ operations. These are made-up largely of its fire protection services and uniform direct sale businesses. Revenue here managed to rise by 7.9% from $261.5 million to $282.1 million. One thing I would like to point out is that essentially all of the company’s revenue growth was organic. This means it did not have to rely on acquisitions in order to see nice upside.

On the bottom line, Cintas performed well also. Earnings per share jumped from $3.33 last year to $3.99 this year. Earnings actually came in $0.19 per share above what analysts anticipated. The earnings per share reported by the company implied an increase in net profits from $346.2 million to $414.3 million. All other profitability metrics reported by the company improved as well. Operating cash flow, for instance, expanded from $553.6 million to $693.1 million. If we adjust for changes in working capital, the rise would be from $480.8 million to $554.2 million. And lastly, EBITDA for the enterprise managed to grow from $575.9 million to $662.5 million. These improvements were driven not only by increased revenue, but also by improvements in profit margin. The gross margin for uniform rental and facility services activities rose from 47.7% to 48.6%. Management attributed this to greater operating leverage, as well as sourcing and process improvements. Meanwhile, for the first aid and safety services activities of the business, gross margin jumped from 51% to 55.4%. Robust operating leverage improvements as a result of higher sales contributed a lot to this. However, the company also attributed some of the improvement to a change in sales mix and certain other operational efficiencies.

Author - SEC EDGAR Data

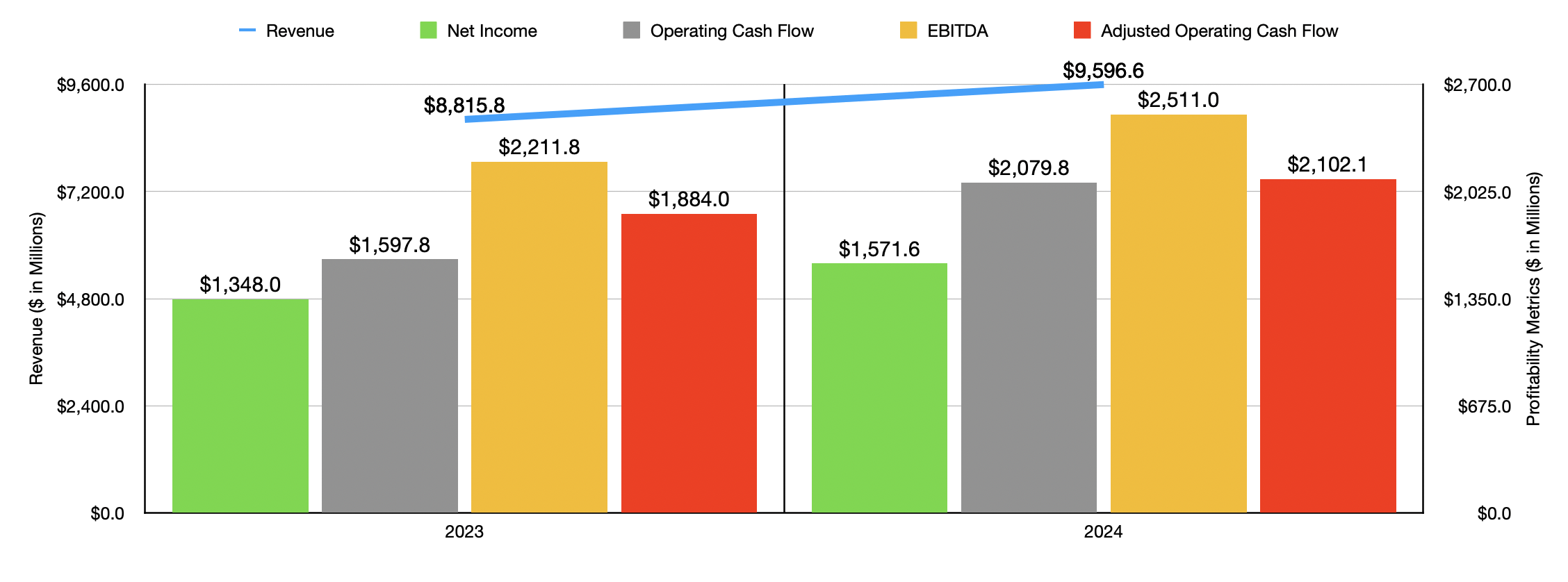

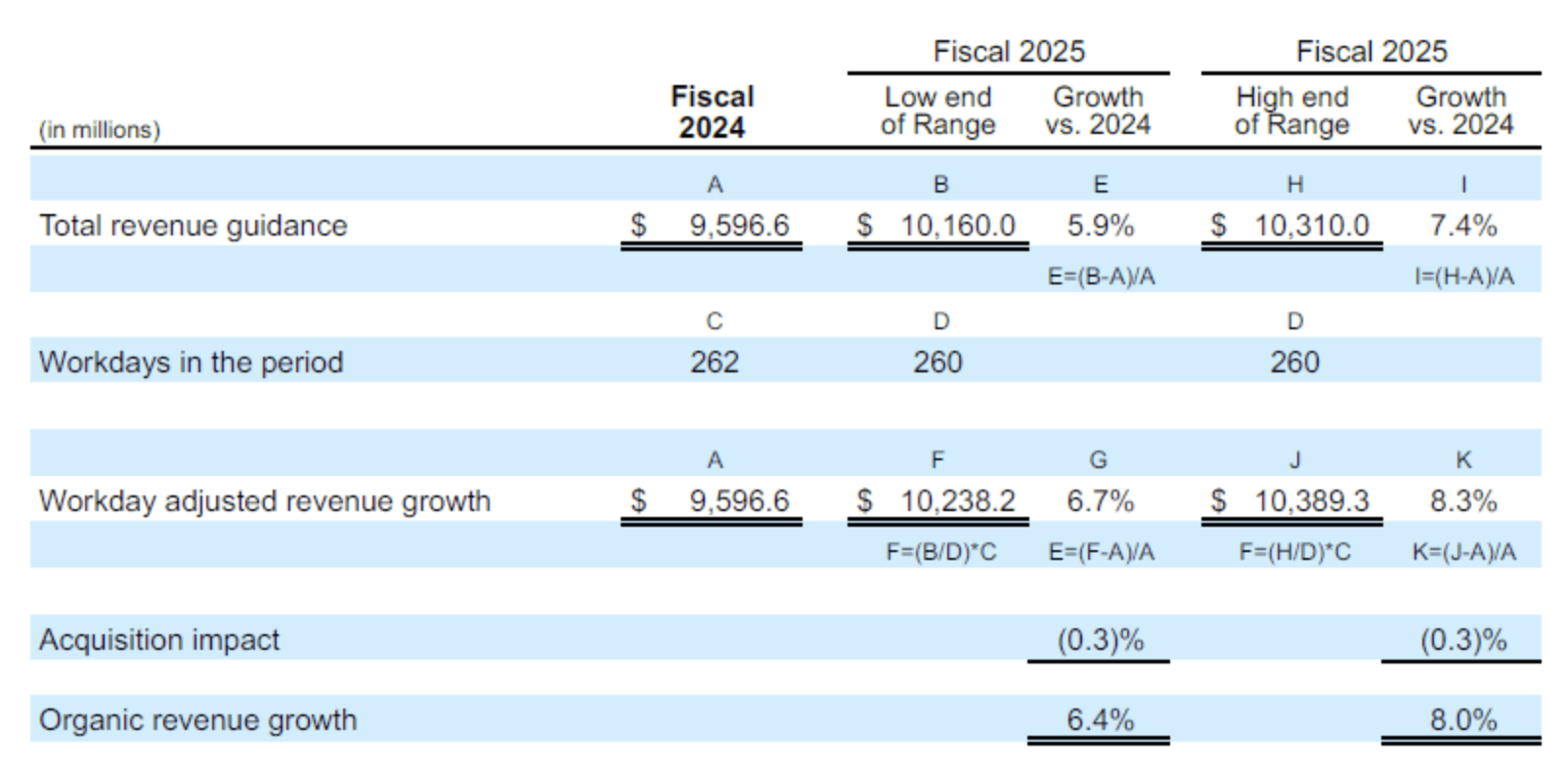

As you can tell by looking at the chart above, financial performance for 2024 as a whole was significantly above what was seen in 2023. Revenue, profits, and cash flows, all rose year over year. And the exciting thing for shareholders is that management expects this trend to continue through the 2025 fiscal year at least. With organic revenue rising by between 6.4% and 8%, overall sales are expected to come in at between $10.16 billion and $10.31 billion. At the midpoint, that would represent an improvement of 6.7% compared to what the company saw in 2024.

Cintas Corporation

Cintas Corporation

With higher revenue should also come an increase in profitability. Earnings per share are now forecasted to be between $16.25 and $16.75 (before factoring in its upcoming four-for-one stock split occurring this September). At the midpoint, we are looking at net income of about $1.71 billion. That would stack up nicely against the $1.57 billion, or $15.15 per share, that management reported for 2024. Estimates were not provided for other profitability metrics. But if we assume similar growth rates for these, this would translate to adjusted operating cash flow of about $2.28 billion and EBITDA of approximately $2.72 billion.

Author - SEC EDGAR Data

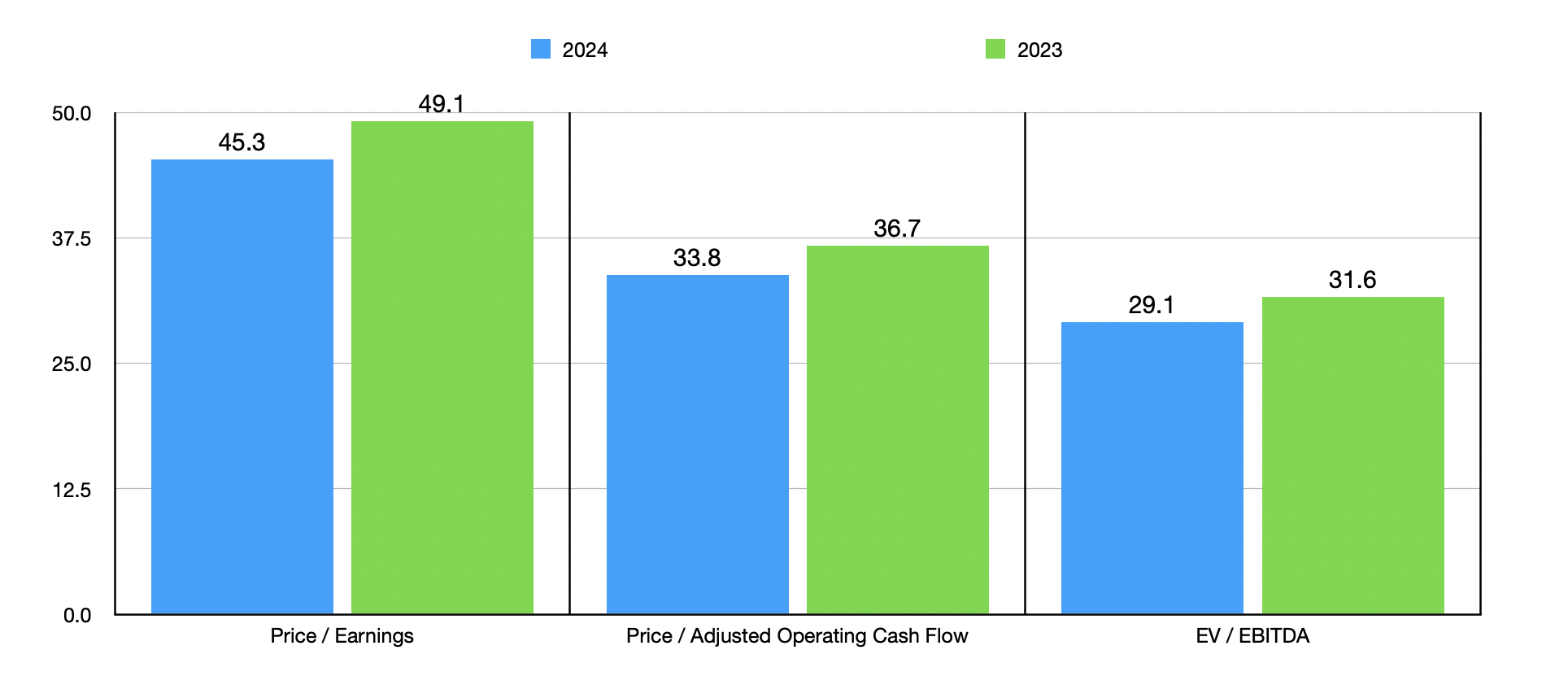

Using these figures, valuing the company becomes pretty simple. In the chart above, you can see how shares are priced using historical results from 2024 and estimates for 2025. Even on a forward basis, I would argue that shares are very pricey at this point in time. This is the kind of valuation that you expect to see from a high-quality, fast-growing tech company. It's not what you expect to see from a $77.2 billion business that's growing at less than 7% per annum. But it's not just on an absolute basis that shares look overpriced. It's also on a relative basis. In the table below, I compared Cintas to three similar enterprises. And using each of the three valuation metrics, I found that it was more expensive than any of them.

| Company | Price / Earnings | Price / Operating Cash Flow | EV / EBITDA |

| Cintas Corporation | 49.1 | 36.7 | 31.6 |

| UniFirst Corporation (UNF) | 26.8 | 13.0 | 11.0 |

| Aramark (ARMK) | 13.8 | 13.9 | 8.0 |

| Johnson Controls International (JCI) | 28.2 | 27.1 | 22.2 |

Takeaway

As much as I think that Cintas is doing a fine job and even though I think that the long-term outlook for the company is positive, this doesn't mean that I think it makes for an appealing investment opportunity at this point in time. The fact of the matter is that shares are very expensive, both on an absolute basis and relative to similar firms. Yes, management is forecasting further growth for the 2025 fiscal year. But even if we value the company based on its forward estimates, it is still more expensive than the comparable businesses I stacked it up against. When faced with a situation like this, even though it may seem crazy given the quality that we are talking about, I have no choice but to keep the company rated a ‘sell’ for now.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.