BIGZ: Hasn't Lived Up To Its Potential So Far

Summary

- BlackRock Innovation and Growth Term Trust focuses on small and mid-cap technology stocks, including private companies, with a 12% coverage ratio for covered calls.

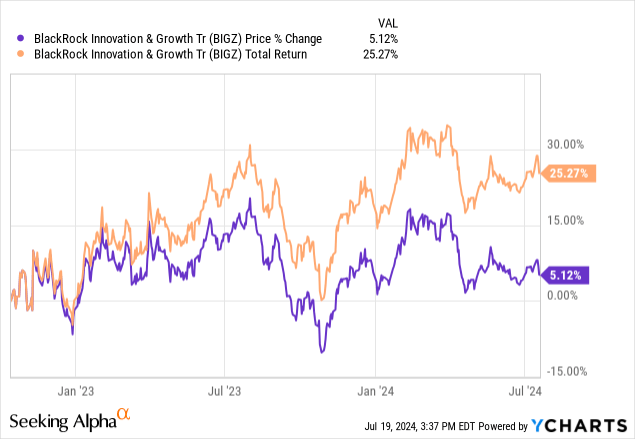

- The fund's performance has been underwhelming since October 2022, up only 5% in share price and 25% in total returns, potentially due to its choice of stocks and private holdings.

- Currently trading at a NAV discount of -13%, the fund pays about 9 cents per share in monthly dividends, subject to change based on NAV fluctuations.

Filograph

BlackRock Innovation and Growth Term Trust (NYSE:BIGZ) is another technology related closed-end fund by BlackRock, which is known for having income focused CEFs that boost distributions by selling covered calls. I've covered this fund last year when it was still relatively new in an article titled BIGZ: It's Too Soon To Judge Yet. The fund was launched in mid-2021 which marked the top for many small-cap and mid-cap technology stocks, which was one of the reasons it was underperforming at the time, so I felt it was too early to judge the fund. Now that some more time passed, we can look at the fund with a more judgmental focus.

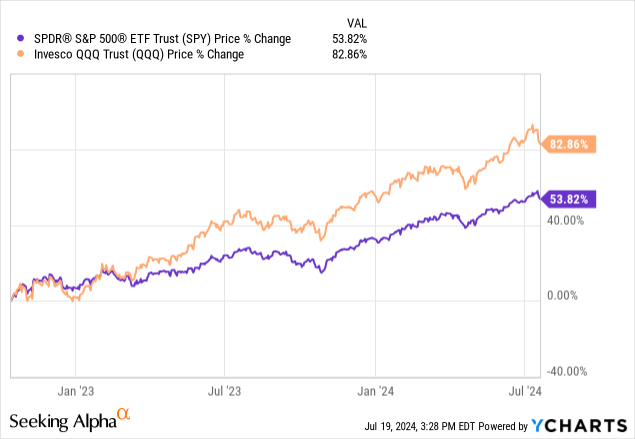

The market has been on a rip since October 2022 and big technology stocks have been doing even better. Since bottoming in October 2022, S&P 500 (SPY) is up 53% (about 56% including dividends) and Nasdaq is up about 83%. This may feel like all stocks were having a big party during this time, but that's not the case. The performance of both indices was mostly driven by big technology stocks, also known as the Magnificent Seven.

Data by YCharts

Data by YCharts

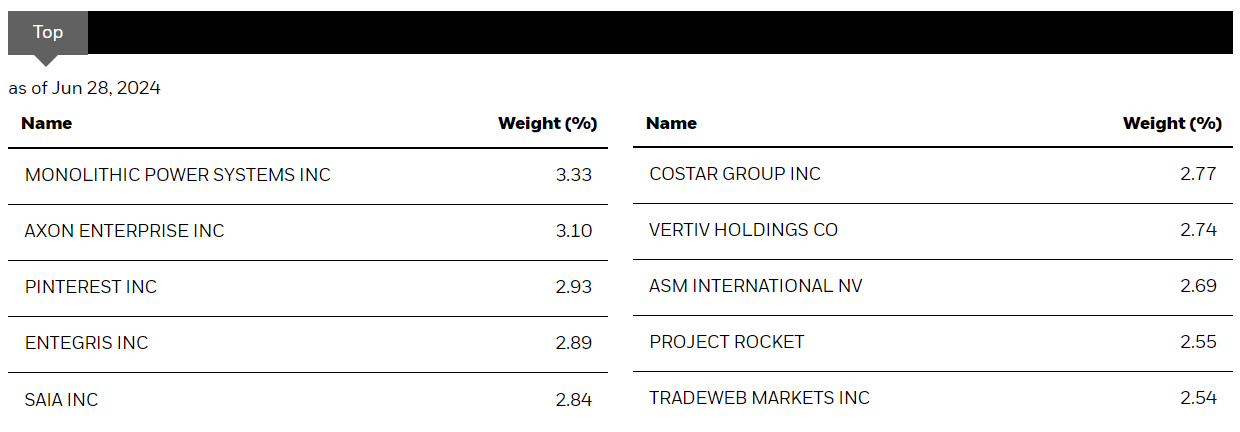

Meanwhile, many small-cap and medium cap technology stocks are still well below their 2021 highs, and this fund mostly focuses on those types of stocks. When we look at the fund's top holdings, we see several stocks whose market cap is well below $100 billion, such as Monolithic Power Systems (MPWR) and Pinterest (PINS). These are not exactly small caps, but they are not mega caps either, which is what everyone seems to be focused on in the last couple of years.

Top Holdings (BlackRock)

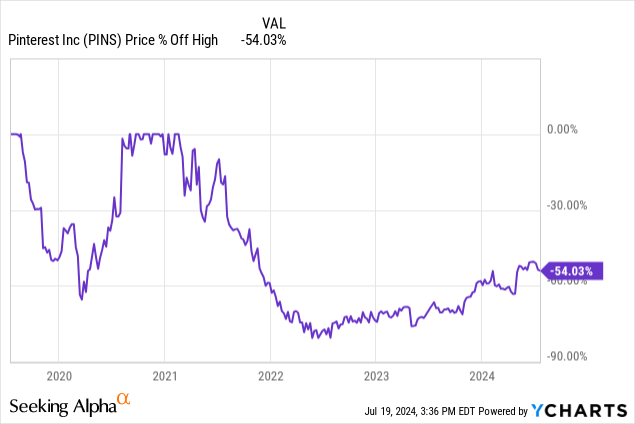

For example, Pinterest is having a great year so far, and it's up 35% year over year, but it's still down more than 50% from its 2021 high.

Data by YCharts

Data by YCharts

Having said that, the fund's performance since the market's bottom in October 2022 is far from impressive. During this period, the fund is up only 5% in share price and 25% in total returns including reinvestment of dividends, which means it's vastly underperforming the market.

Data by YCharts

Data by YCharts

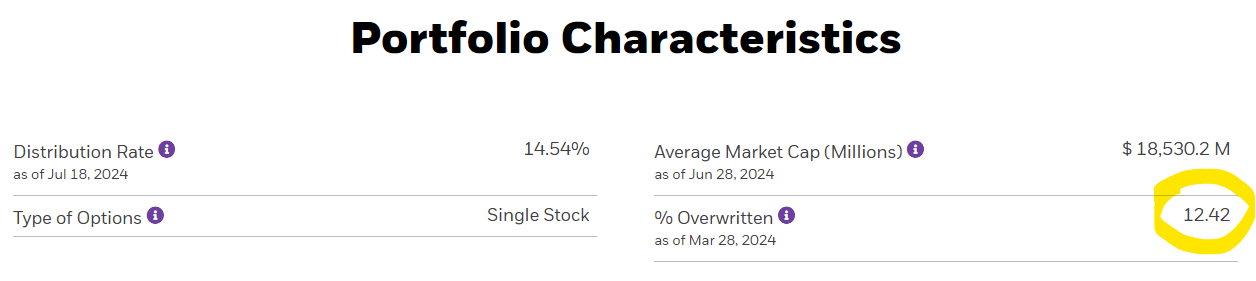

One might think that this is because the fund sells covered calls and doesn't participate in all the upside. It is very common for covered-call funds to be left behind during bull markets since their participation in upside is greatly limited as they sell most or all upside in exchange for collecting premium and generating income, but this would be only partially to blame for this fund's underperformance because its coverage ratio (also known as Percent Overwritten) is only 12% which is very small. What this means is that out of all the assets this fund holds, it wrote covered calls against only 12% of its holdings. This would indicate that 88% of the fund's assets are free to grow and participate in all upside and if the fund's underperformance was due to writing covered calls, it would only underperform by about 10-15% not by more than 50% it is right now.

Portfolio Characteristics (BlackRock)

Keep in mind that the fund also uses single stock options which means unlike other covered call funds like QYLD (QYLD), JEPI (JEPI) and JEPQ (JEPQ) it doesn't write calls against indices but individual stocks which should generate more income since individual stocks tend to have higher IVs than indices, sometimes by a factor of 3 or 4 if not more.

In this case, the fund's underperformance must come from its choice of stocks. One thing we know about BlackRock funds that makes them unique is that they tend to invest in publicly traded stocks as well as privately held companies, which most investors wouldn't be able to get their hands on. This fund is no exception, as it allocates 20-30% of its assets into private companies. Out of the 85 companies currently held by the fund, 29 are private companies that aren't available to most investors. Having this type of access can be a great advantage for some investors, but it also comes with its disadvantages. For example, unlike publicly traded companies, private companies don't see their value updated on a daily basis. Since their stocks don't trade in liquid markets, their valuation only gets updated when they get significant funding or investments. Sometimes their valuation can also get adjusted if they get change of ownership.

This means the fund is holding many private companies whose valuation haven't changed in many months, and, in some cases, even a couple of years. This means while the private holding might be more valuable than it was last year, it won't be reflected in the fund's NAV until the adjustment happens. It is possible that the fund is holding many assets at prices below their true worth. This could be one of the factors causing the fund's underperformance in the last year. The fund will hold some private companies until they are sold off or have an IPO while others might be offloaded earlier, but since private companies don't have as much liquidity, the fund might end up selling some of its holdings at a loss.

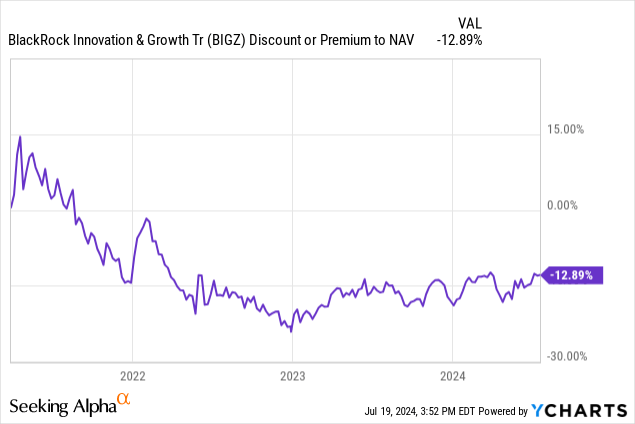

Speaking of NAV, the fund is currently trades at a NAV discount of -13%. This compares favorably to when the fund was first launched in 2021, and it was trading at a premium of as high as 15% at one point. Since early 2023, the fund's NAV discount has been shrinking a bit and this trend could continue if investors start bidding this fund up.

Data by YCharts

Data by YCharts

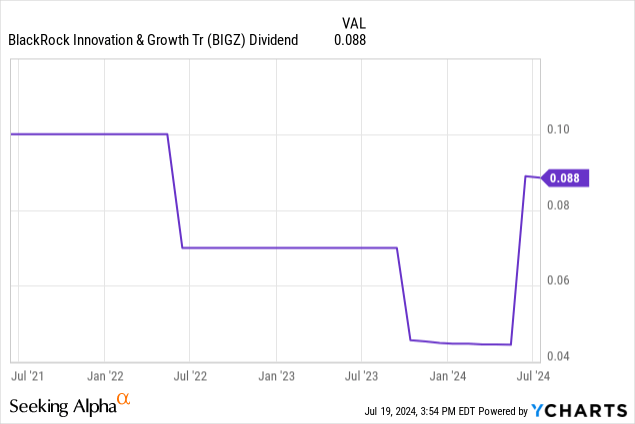

The fund pays about 9 cents per share in monthly dividends, but this is not set in stone. BlackRock typically limits their distributions to about 2% of NAV per quarter or 8% per year, so if the fund's NAV rises or drops substantially, so will its distributions, so don't be surprised if its distributions change significantly over time.

Data by YCharts

Data by YCharts

This fund could be good for certain investors. If you are overweight in mega caps, and you'd like to gain exposure to smaller technology companies in addition to some private companies while generating a decent 8% yield, this fund could be a good addition to your portfolio. On the other hand, if you are looking for a fund that will outperform the markets and deliver very strong results in every environment, this may not be a good one. The holdings of this fund will be very cyclical in nature, and many of its holdings' performance will depend highly on the strength of the economy. Since these are typically smaller companies, they have less access to liquidity and many of them might not be exactly cash cows.

I personally like BlackRock's other similar products a bit better than this one such as BlackRock Science and Technology Trust (BST) and BlackRock Science and Technology Trust II (BSTZ) and BlackRock Health Sciences Term Trust (BMEZ) though those funds haven't been performing that great in the last year either so these funds should only be bought in small portions.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.