ASML: Upgrading To Buy On EUV Tailwinds

Summary

- ASML reported its 2QFY24 results and outlook earlier this week causing a pullback on disappointing Q3 guidance. We say buy the dip.

- Management guided for a 7-17% Q/Q growth to €6.7B-€7.3B, missing consensus estimates of €7.67B.

- Our upgrade is based our belief that the higher risk profile of an expanded U.S. export ban and geopolitical tensions has been priced in.

- Now, ASML is better positioned to outperform on increased industry adoption of EUV for DRAM and logic used in AI servers and edge AI devices.

- We expect ASML to outperform the peer group in 2025 and believe the stock has been de-risked at current levels.

Mordolff/iStock via Getty Images

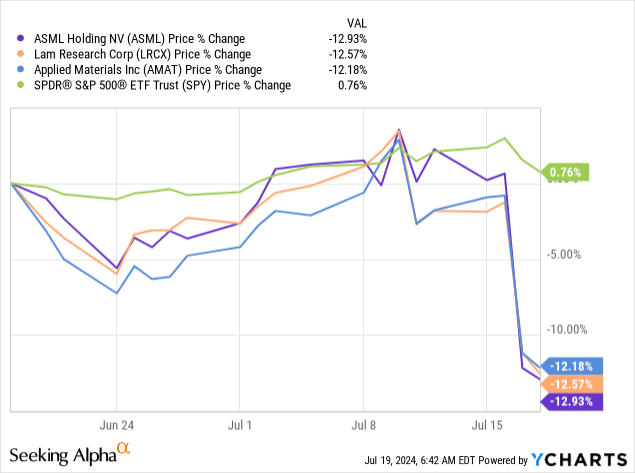

We're upgrading ASML (NASDAQ:ASML) to a buy after a long, neutral stance. The company reported its 2Q24 results earlier this week, causing a massive pullback of over 12%, as shown in the stock's one-month chart against the S&P 500 and semi-cap names Applied Materials (AMAT) and Lam Research (LRCX).

The sell-off was a reaction to management's guidance for next quarter missing consensus; the company guided for a 7-17% Q/Q growth to €6.7B-€7.3B, trailing consensus estimates of €7.67B and forecasting downside if the U.S. semi-export ban on China expands further. Our bearish stance on the stock was due to our belief that ASML held a higher risk profile, more specifically concerns over "softer extreme ultraviolet ("EUV") demand in the back end of the year due to lackluster end demand in 2023 and 1H24." Our negative thesis has played out over 1HFY24, and risks associated with softer EUV demand and heightened geopolitical tensions have been priced into the stock and outlook. ASML's guidance has been lower than consensus expectations for three consecutive quarters, and concerns over an expanded U.S. export ban have been in the spotlight and digested by the market. Now, we're upgrading to a buy as we see minimal downside after the outlook has been de-risked and significant tailwinds for ASML in 2025 from increased industry adoption of EUV tools to keep up with AI demand.

YCharts

For the quarter, ASML reported total sales up 18% Q/Q to €6.24B, a little ahead of consensus estimates of €6.03B. Here's the breakdown: logic and memory-related system sales grew sequentially, up 3% Q/Q and 49% Q/Q to €2.57B and €2.19B, respectively. China-related system shipments have become the main topic of discussion as geopolitical tensions increase and grew 20% Q/Q to €2.33B, making up 49% of total system shipments.

Why does EUV matter?

We agree with management that 2024 remains a "transitional year" for the company as semis recover from the cyclical downturn of inventory correction cycles. We think the market has finally recognized and digested this, particularly after the massive sell-off on Wednesday. Our positive thesis for ASML is based on a necessary acceleration in demand for EUV lithography tools in 2025, supported by the increased need for advanced tools in DRAM and foundry/logic markets. EUV is the future as it's the only window to enable more advanced process nodes and keep up with Moore's Law; hence, our upgrade is based on expectations that we'll have a booster in EUV sales next year.

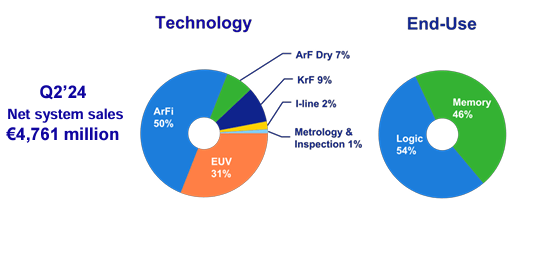

We're anticipating industry adoption for next year in particular as we think customer wafer fabrication spend, or WFE, is due for a rebound after pulling back in 2023 in response to "weak memory spending, macroeconomic slowdown, inventory adjustments and low demand in the smartphone and PC end markets." The second reason we're optimistic about EUV sales next year is because of AI; on the relevance of EUV to AI, Chris Zeoli on DataGRavity wrote the following; "NXE machines use extreme ultraviolet light to create very small and complex parts necessary for high-performance AI chips." This June, ASML CFO Roger Dassen's comments cited in Jefferies's report on improved orders from TSMC (TSM) confirm our thesis for 2025. EUV tech represented roughly 31% of total net system sales compared to 46% a quarter prior; we'll see a bigger chunk of net system sales coming from EUV in 2025. The following chart is outlines ASML's net system sales breakdown by technology.

ASML 2Q24 earning presentation

Most of the market is taking ASML's transitional year status as a negative, we disagree. We believe we're in the pre-moment of an industry-wide transition to sub-5nm for logic and sub-14nm for DRAM because of hyper demand for AI servers and edge AI devices. ASML has yet to see its AI tailwind play out; we say there's more upside to be recognized and recommend investors load up on the pullback.

Valuation and Word on Wall Street

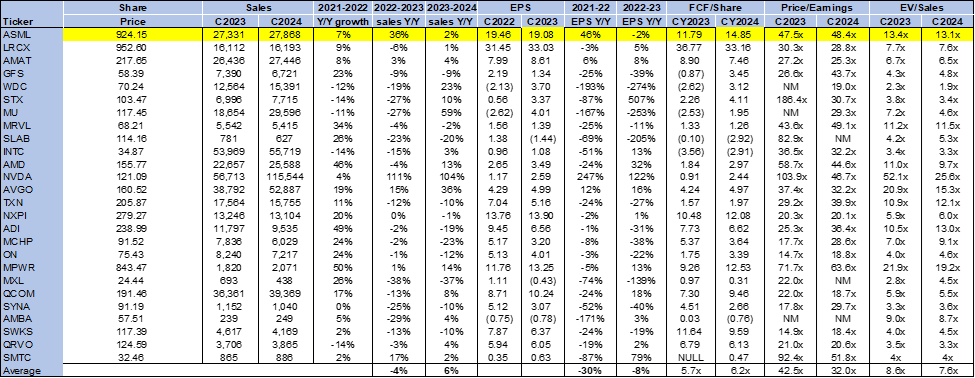

While expensive, ASML stock is fairly valued, in our opinion, for its technological leadership in the lithography market through its EUV monopoly. On a P/E ratio, the stock is trading at 48.4x C2024 compared to a group average of 32.0x. The stock's EV/C2024 Sales ratio also sits above the peer group average at 13.1x versus the group average of 7.6x. ASML is uniquely positioned to achieve the future earnings the market is pricing into its valuation.

The following chart outlines ASML's valuation against the peer group average.

TechStockPros

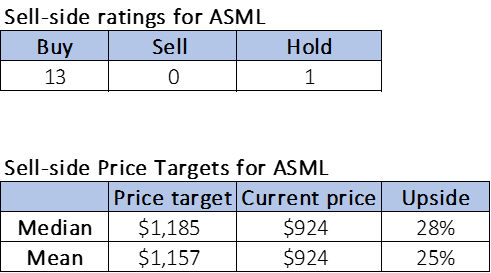

Wall Street's bullish sentiment on the stock confirms our own. Of the 14 analysts covering the stock, 13 are buy-rated, and one is hold-rated. Sell-side price targets are also noteworthy in comparison to other leaders in the semi space; the median sell-side price target is $1,185, while the mean is $1,157 for a 25-28% upside compared to a potential upside of 16-30% back in October.

The following charts outline ASML sell-side ratings and price-targets.

TechStockPros

What to do with the stock?

We're positive on ASML and the semi-cap names AMAT and LRCX. We do recognize the still present risk of the U.S. export controls on China expansion, but we believe the worst of ASML's exposure to China has already been priced into not only the next quarter but the FY24 sales outlook; the company expects sales to be flat Y/Y to ~€27.5B as a result of weaker logic sales and higher memory. Management is guiding for FY25 bookings to be in the range of €30-€40B; we think this number will likely be revised up as the AI TAM is discovered. ASML should be on the radar for longer-term investors due to the strategic nature of lithography spend; the company serves as an early indicator of the broader semi market, or in other words, it helps foreshadow industry movement. We believe ASML will rebound materially in 2025 and see the stock beating and raising guidance in late FY24.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.