Orchid Island Capital: Q2 Earnings Show No Signs Of Turning Around

Summary

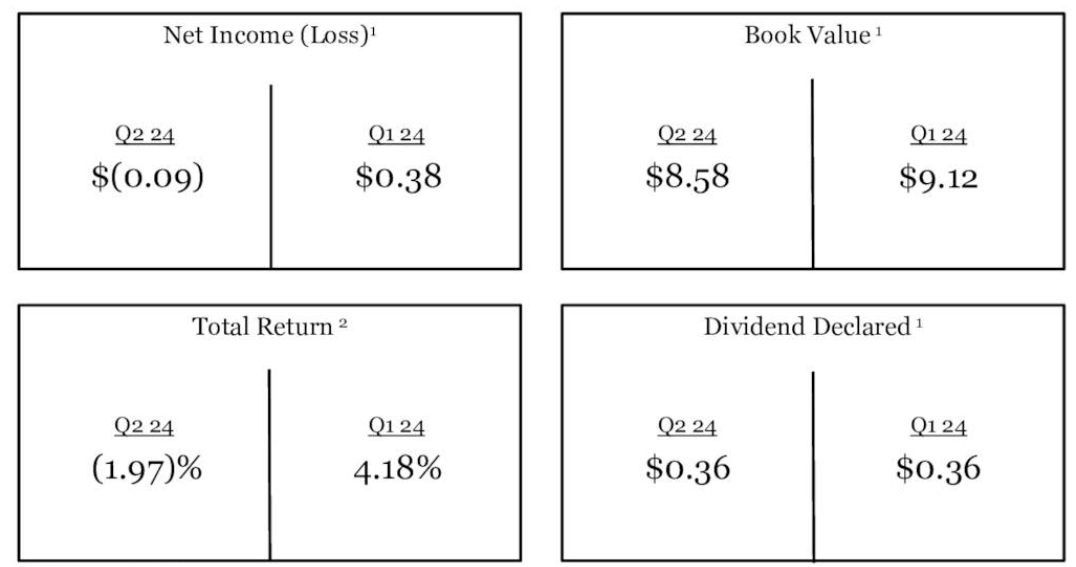

- Orchid Island Capital reported a net loss of 9 cents per share, with book value dropping from $9.12 to $8.58 and a total return margin of -1.97%.

- The company's high leverage, share dilution, and overpaying in dividends have led to consistent losses and underperformance for investors.

- Despite claims of sustainable dividends based on "Adjusted Economic Income per Share," the long-term history of dividend cuts and poor performance make investing in ORC stock risky.

Gerasimov174/iStock via Getty Images

Orchid Island Capital (NYSE:ORC) reported earnings last week where results were mostly in line with expectations. The company reported a net loss of 9 cents per share for the quarter, and its book value dropped from $9.12 to $8.58 during the quarter. The total return margin came at -1.97%, significantly down from the previous quarter's 4.18%. Despite these worsening conditions, the company kept its dividend same as before at 36 cents per share, but given the company's history of cutting dividends in the long run, this could easily change in the near future unless its financials improve quickly.

Results Overview (Orchid Island Capital )

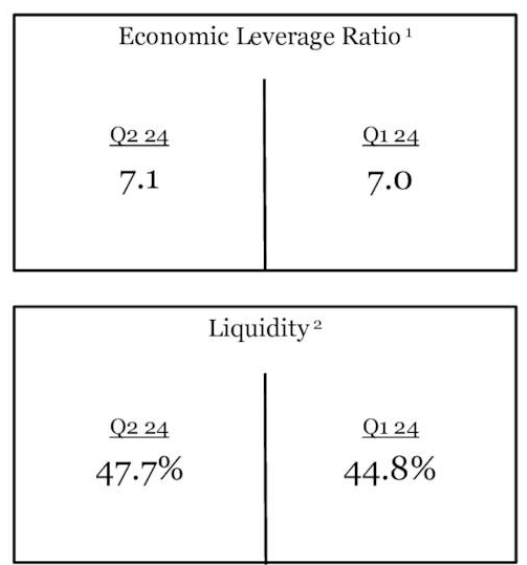

As I mentioned in my past articles, one of the biggest issues with this company is its leverage being too high. This allows the company to take oversized losses when things are going bad and make it almost impossible for things to recover when things improve later. The company uses hedges in order to keep it from going bust if things go really bad, but those hedges don't seem to stop the slow bleeding that's been happening for many years. During the quarter, the company's leverage ratio even rose a bit from 7.0 to 7.1 while its liquidity got slightly better from 44.8% to 47.7%.

Leverage Ratio (Orchid Island Capital )

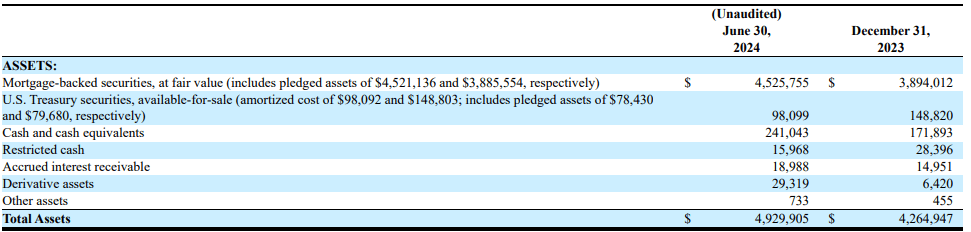

When we look at the company's balance sheet, it appears that the company's assets grew very nicely from $4.2 billion to $4.9 billion, a growth rate of 16%, which must indicate nice growth for investors, but it isn't so because most of this growth came from dilution rather than organic growth. During the same period, the company's average diluted share count rose from 51 million to 64 million, a rise of 25%. Most of the money coming from this dilution was put to work by deploying them into mortgage-backed securities, as you can see this item's worth rising from $3.89 billion to $4.52 billion. A portion of this dilution also went towards paying dividends, which means the company took money from investors' right pocket and put it into their left pocket. This also explains why book value per share dropped so much during the quarter while the company's total assets grew.

Balance Sheet (Orchid Island Capital )

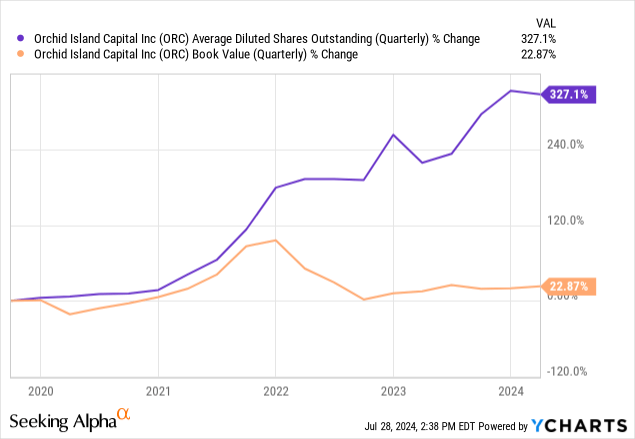

This is not a new problem, either. In fact, this has been going on for quite some time. For example, when we zoom out and look at the company's book value and dilution growth in the last 5 years, the company's book value grew at a rate of 23% during this period whereas its diluted share count grew by a much larger rate of 327%. Basically, between using overleverage, overpaying in dividends, reporting losses and diluting its shareholders, the company hasn't been offering much value to investors.

Data by YCharts

Data by YCharts

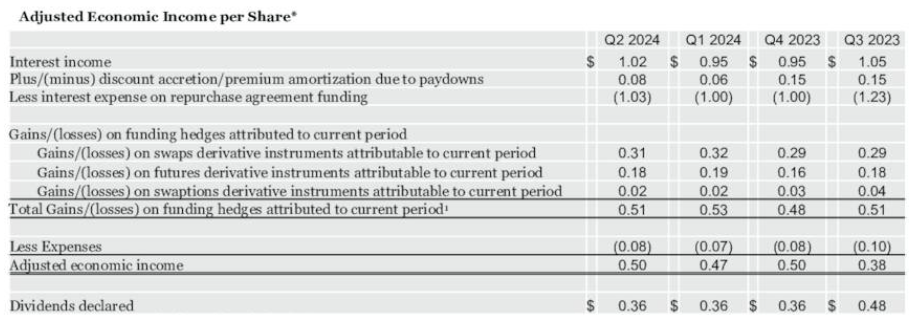

To be fair, the company has another metric which shows it to be in better shape. The company calls this metric "Adjusted Economic Income per Share" and the management argues that this is where dividends will come from and dividends are unlikely to be cut as long as this metric is sustainable. This metric basically looks at how much money the company made from its regular operations and adds profits from its hedging plays. For example, during the last quarter the company made $1.02 per share in interest income while spending $1.03 on interest expenses or repurchase agreements, but it also reported a gain of 31 cents on swap derivatives, 18 cents from futures derivatives and another 2 cents from other derivatives. These are the hedges the company put in place for times like these where its operations prove not to be profitable or results in a loss. The company's total adjusted economic income came at 50 cents per share, which supports the current dividend of 36 cents.

Adjusted Economic Income (Orchid Island Capital)

In the long run, dividends are still not safe, though. This company has a long history of cutting dividends on almost yearly basis. The last dividend cut came in Q4 of 2023 when the company cut it from 48 cents to 36 cents and when we look at the long-term chart, see it being reduced significantly almost every single year. This was mostly caused by losses multiplied by overleverage, share dilution and overpaying in some instances.

Data by YCharts

Data by YCharts

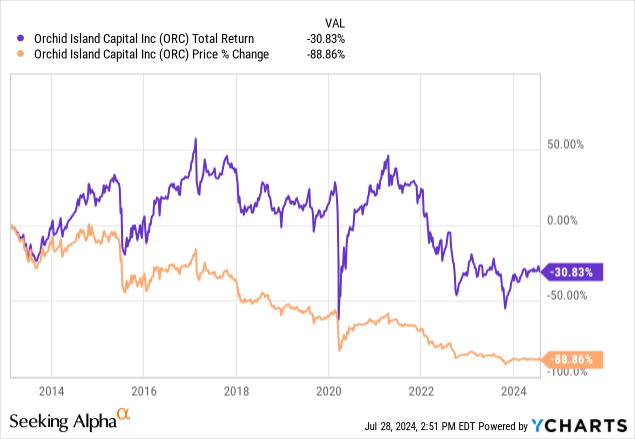

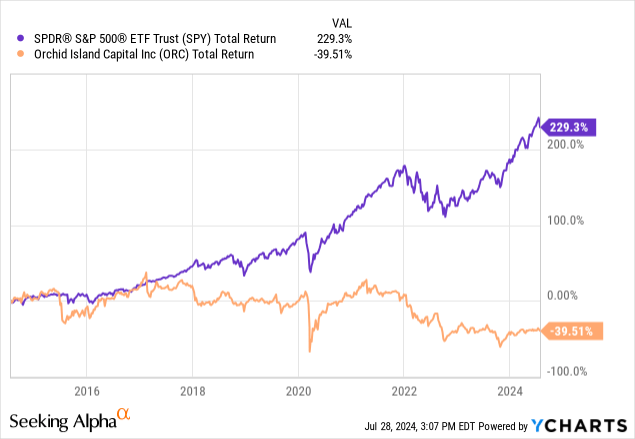

In the long run, if you don't count rare periods of short-term trading (such as buying in March 2020 and selling in 2021), buying this stock almost always resulted in a loss for investors sooner or later. If you bought ORC a decade ago and held until today, your share price would be down -89% and your total return (after reinvesting dividends) would be down -30%. No matter how you look at it and how you cut the data, the company's business model is not working to generate wealth for investors.

Data by YCharts

Data by YCharts

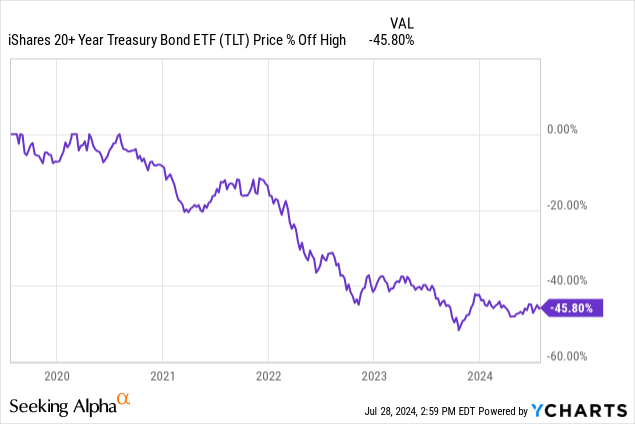

People often say that this company invests into "agency backed" or "government guaranteed" loans which are supposed to be as risk-free as treasuries themselves, but that "risk free" portion only applies to the risk of a bond getting totally wiped out. The risk doesn't apply to prices of those bonds crashing. As a matter of fact, even long-term treasuries themselves can see their share price crash, evidenced by TLT's decline of 45% in the last 5 years. These are the government's own treasuries which are considered "risk-free" but they are not risk-free in terms of price declines.

If you are holding some government bonds or agency backed debt and their price declines by 20-40%, you can usually sit it out until expiration and get your money back, but what if you are leveraged? What happens when you are overleveraged on bonds that drop 20-40% in price? You could easily get totally wiped out. In fact, this is how several small banks went bankrupt in the last few years, even though they were holding "risk-free" government bonds. They found out that things aren't quite as risk free if you are overleveraged in them.

Data by YCharts

Data by YCharts

As I mentioned above, this company uses some hedging so it's unlikely to go completely bust, but its financial performance is likely to continue going progressively worse and worse in the long term.

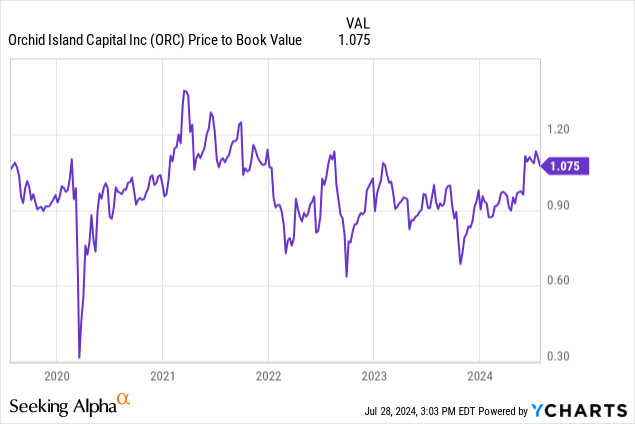

In terms of valuation, prior to the earnings report the company was trading at a price to book value of 1.075 indicating that it was selling at a 7.5% premium against its book value. Currently, the company's share price is $8.24 which is below its currently estimated book value of $8.58. It's trading at a discount of 4% against its book value, but it's likely not enough of a discount to take on this much risk.

Data by YCharts

Data by YCharts

You'd be probably much better off investing in an index fund such as S&P 500 (SPY) than taking on too much risk for the sake of high yield. What's the point of generating high yield if your investment will keep shrinking year after year? It's like taking money from your right pocket and putting it into your left pocket and calling it income.

Data by YCharts

Data by YCharts

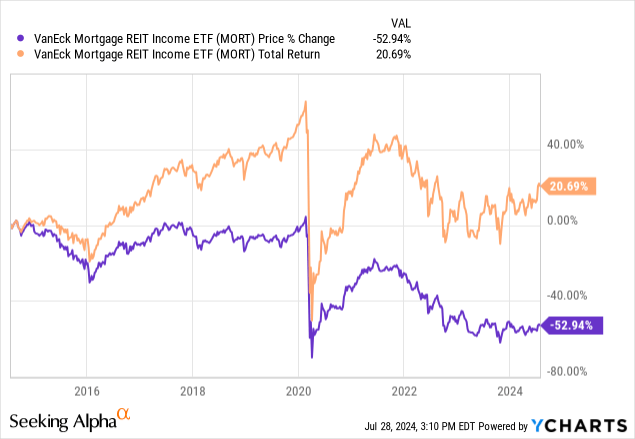

The issues regarding this company are not specific to this company, either. The entire mREIT sector has performed pretty poorly in the last decade because the sector suffers from the same problems of being overleveraged, overpaying in dividends and constant dilution. I would honestly avoid not only ORC but this entire sector altogether because it has done nothing but underperform year after year for most investors.

Data by YCharts

Data by YChartsDisclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.