The More They Drop, The More I Buy

Summary

- Stocks are falling due to recession fears and disappointing earnings reports.

- Despite the market volatility, now is a good time to buy high-quality dividend stocks at discounted valuations with attractive yields.

- I share several of the most attractive dividend stock opportunities of the moment.

z1b

Stocks have been falling significantly in recent days due to growing fears of a recession and several disappointing earnings reports. Dividend stocks (SCHD) have been no exception. In particular, asset managers like Blackstone (BX), business development companies like Ares Capital (ARCC), and energy stocks like Chevron (CVX) have all pulled back recently, as concerns grow that the economic slowdown might hurt their performance.

That being said, now is a great time to shop for high-quality dividend stocks that are well-positioned to weather a recession and trade at deeply discounted valuations with very attractive dividend yields. While it is impossible to time the bottom, and this could simply be the beginning of a much deeper market crash, it is also entirely possible that it is merely a short-term blip that will soon turn into a strong recovery, especially as the Fed is likely to cut rates starting next month. There is still a chance that the economy could weather the storm and come out with only a very minor recession, or even avoid a recession altogether. As a result, in this article, I will share some dividend stocks that look very attractive and appear to be potential buys on the dip.

Dividend Stock #1

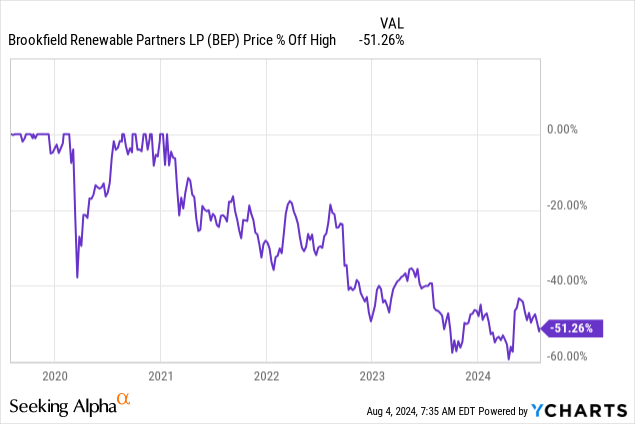

One that I like a lot right now is Brookfield Renewable Partners (BEP)(BEPC). While it has actually held up better than many other dividend stocks during the recent pullback, it has still pulled back fairly sharply from its recent highs when it reached nearly $29.00 per unit in May and just over $27.00 per unit in mid-July. Today, it trades at around $24.00 per unit, putting it at a 17% discount to its recent highs and down over 50% from its all-time highs:

Data by YCharts

Data by YCharts

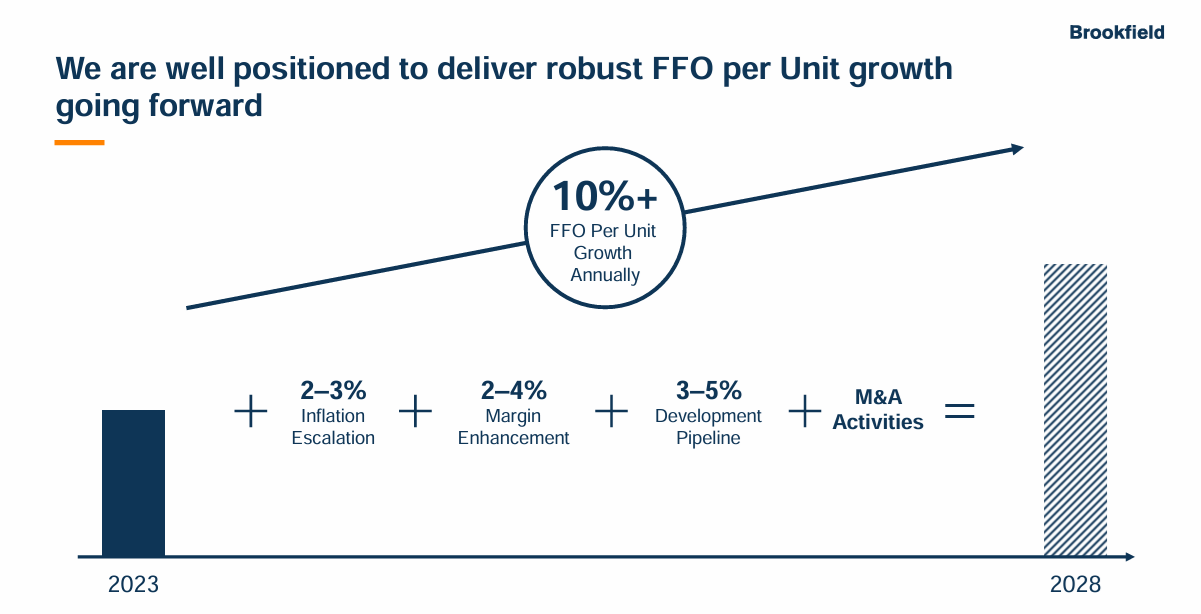

With a roughly 6% distribution yield, a BBB+ credit rating from S&P, significant liquidity, well-termed debt maturities, stable cash flows from long-dated contracts with creditworthy counterparties, and significant built-in inflation protections that help mitigate interest rate risk even further, its balance sheet is in very strong shape. Moreover, its strength is further bolstered by the fact that it enjoys the backing of leading renewable power and infrastructure investor Brookfield (BN)(BAM). Last, but to least, it has a very promising growth outlook with management guiding for 10%+ FFO per unit CAGR for the foreseeable future fueled in part by its partnerships with AI champions like Microsoft (MSFT) to power their AI investments:

BEP Growth Guidance (Investor Presentation)

As a result, Brookfield Renewable Partners appears to be one of the most attractive buy-the-dip opportunities in the market today.

Dividend Stock #2

Another opportunity that looks very attractive on the dip is Nutrien (NTR), which is one of the world's leading agricultural companies. It combines competitively positioned potash and other agricultural nutrition material production businesses with a large, growing, and well-diversified agricultural retail business that helps stabilize its cash flows, which would otherwise be very cyclical. The company has been generating a lot of free cash flow while growing its dividend meaningfully for the past several years. It has also been buying back a lot of shares over time and appears poised to continue doing so.

The company is also investing aggressively in improving its efficiencies and has been successful so far, expecting to continue unlocking additional efficiencies moving forward. Right now, the stock looks quite cheap relative to its history, as it offers an attractive 4.5% dividend yield that is over 100 basis points higher than its five-year average of 3.4% and its all-time average of 3.38%. Moreover, its EV/EBITDA of 6.57x is well below its five-year average of 7.03x and its all-time average of 7.67x.

The stock has a history of being quite volatile, driven by the price of crop nutrients, and management has signaled on recent earnings calls that the fertilizer market is stabilizing and returning to trend levels. As a result, it could very possibly soar higher in the near future, even if the broader market continues to struggle. This makes it an attractive portfolio diversifier, and its stock price is currently beaten down, making it an opportunistic time to acquire shares in this investment-grade, high-quality business.

Dividend Stock #3

Another opportunity that has been pummeled recently and is beginning to look like it might be moving into buy territory is Blue Owl Capital (OWL). Last year, I loaded up very aggressively on this rapidly growing alternative asset manager when it fell to $10 and even a little below last May. It then proceeded to earn over 50% returns before I sold the stock, though I sold it a bit early as it continued to soar higher, which I felt was a bit euphoric from the market. My caution has been vindicated as the stock has crashed back down to earth, from nearly $20 per share just ten days ago to now trading at just over $16.00 per share.

As a result, I now think it is roughly fairly valued, and if it continues to dip, I would seriously consider loading up on it again, as management expects to grow its dividend by about 30% next year and its 4.43% forward dividend yield is already quite attractive relative to that offered by peers like BAM (3.8%) and BX (3.4%). On top of that, its high concentration (over 75%) of assets under management in permanent capital relative to these same peers (BX has only 39% of its AUM in perpetual capital) and its focus on earning only fee-related earnings instead of the carried interest that plays a big role at places like BX makes its business model more stable than many. Additionally, its concentration in direct lending gives it a very attractive growth profile during a time when private credit and direct lending are booming.

Investor Takeaway

As discussed in this article, the market is selling off. When it does, long-term-oriented investors, especially income and value-focused investors like myself, get excited because while no one likes to see red in their current holdings, when planning to buy more stocks anyway, it is preferable to buy them at deep discounts rather than at significant premiums. Additionally, thanks to my opportunistic focus on loading up on beaten-down defensive businesses such as utilities and utility-like midstream and other infrastructure firms over the past several months, while the rest of the market was rejecting them, I now have several significant positions in companies that have actually withstood this recent volatility quite well, providing me with additional capital that I can tap into and recycle into some of these other names that have recently gone on fire sale.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.