Patterson-UTI Is Cash Flow Positive And Offers Asymmetric Exposure To A Rebound In Natural Gas

Summary

- Patterson-UTI is cash flow positive despite U.S. oilfield activity being at a cyclical bottom.

- A rebound in natural gas drilling in 2025 will be a strong call on the company's premium equipment that is already in short supply.

- Even if gas drilling doesn't rebound soon, the generous buyback program should provide support for the stock price.

lyash01

Background

Patterson-UTI (NASDAQ:PTEN) is a U.S. land focused oilfield services company that offers both drilling and completion services. The merger with NexTier expanded the completions portfolio, while the subsequent acquisition of Ulterra added a smaller drill bits business.

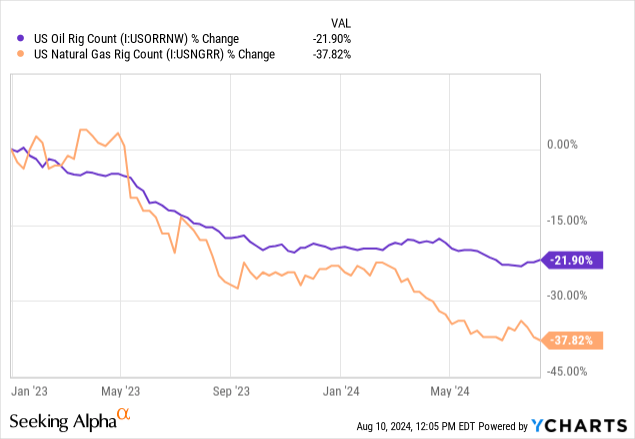

U.S. oilfield services are in a cyclical downturn. The common impulse is to link these ups and downs to oil prices, but the current situation has more to do with natural gas:

Data by YCharts

Data by YCharts

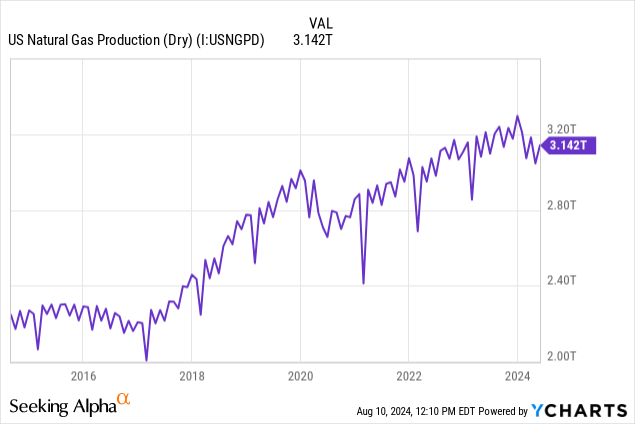

U.S. gas (NG1:COM) production has grown impressively, but the much-needed expansion of export capacity won't come until 2025 and maybe even later if some LNG projects see construction delays:

Data by YCharts

Data by YCharts

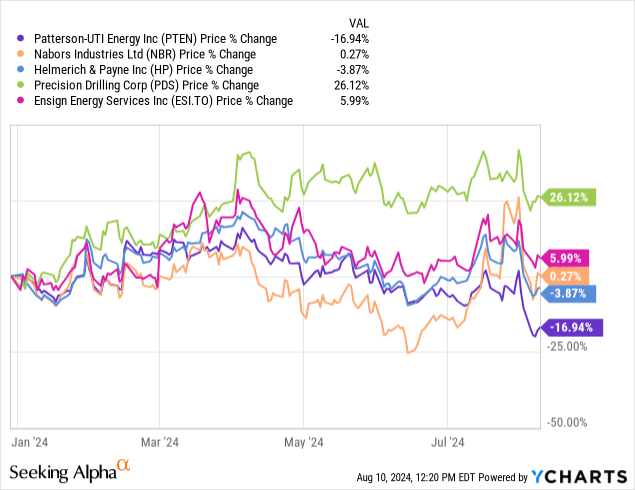

The drop in gas drilling hurts the utilization and margins of U.S. oilfield services companies, but that remains largely an American problem. International oilfield activity is robust and companies with overseas exposure continue to post strong revenue growth. That may explain why PTEN has underperformed the other big U.S. drillers, which have greater international presence:

Data by YCharts

Data by YCharts

Investment thesis

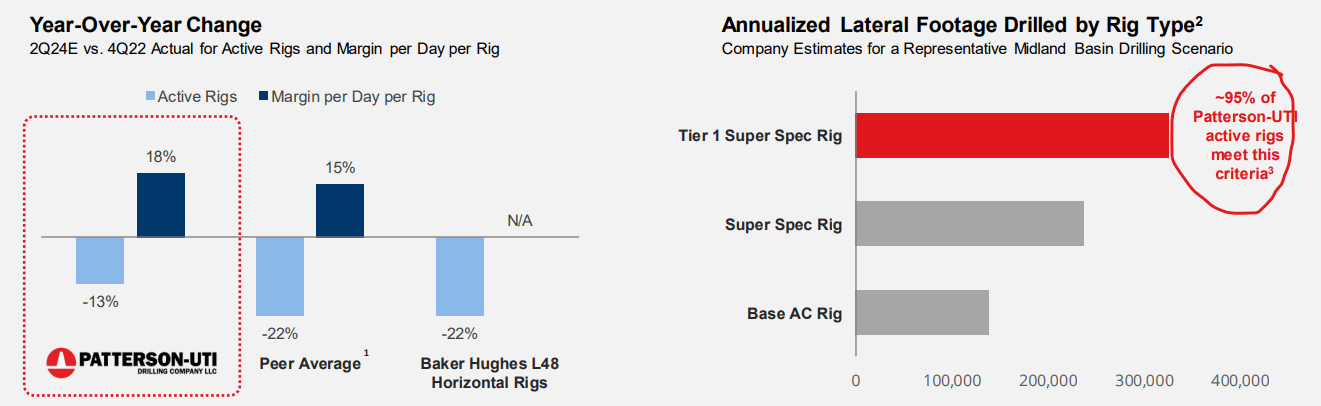

A rebound in natural gas prices will cure many problems. In fact, Patterson-UTI and the other big drilling and completions companies may do even better than 2022 due to the growing preference of U.S. oilfield customers for high-end equipment, meaning high-spec rigs and pressure pumping units that can run on natural gas or electricity.

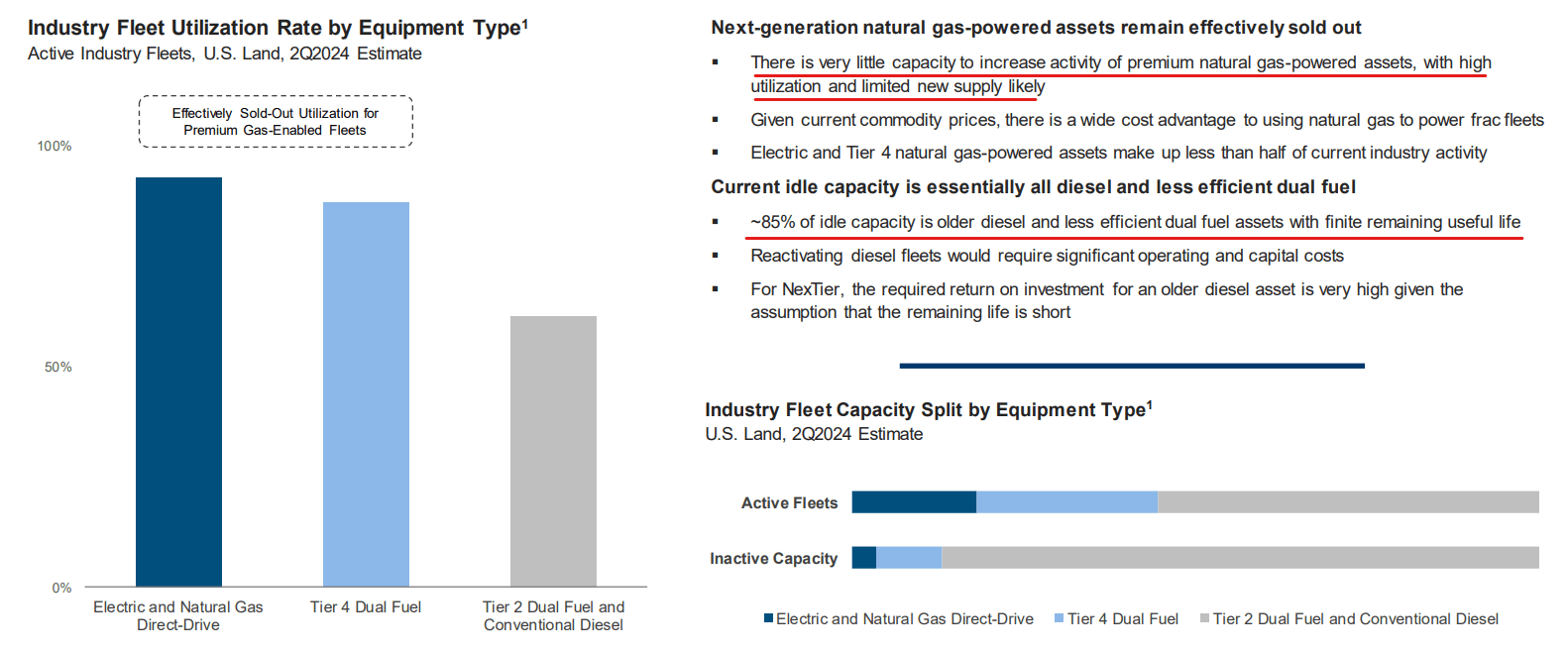

This high-end pressure pumping equipment is already in short supply, so if gas indeed rebounds in 2025, it will place a powerful call on PTEN's assets:

PTEN presentation

The situation is similar on the drilling side, where PTEN has an advantage in the most coveted rig class:

PTEN presentation

This is the natural gas "call option" referenced in the article's title.

The second part to the investment thesis is the yield one can get while waiting for natural gas to turn around. At the current, suppressed levels of activity, PTEN is already free cash flow (or FCF) positive:

Seeking Alpha

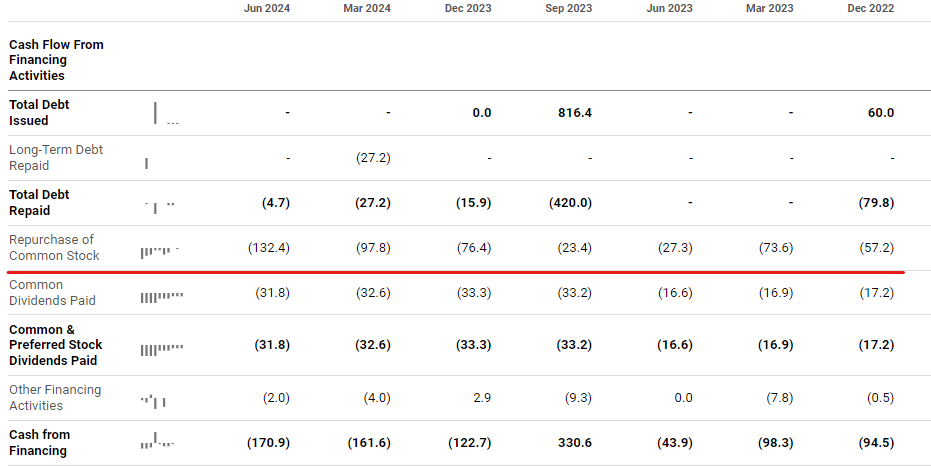

Besides paying a 3.5% dividend, management is not shying away from buybacks:

Seeking Alpha

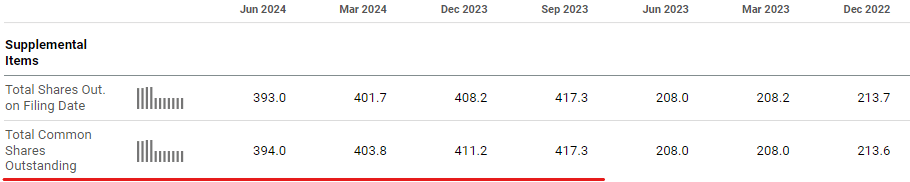

The share count has already been reduced 6% since the NexTier merger:

Seeking Alpha

The remaining buyback authorization as of June 30 is $819 million. At Friday's closing price, this can buy another 91 million shares, or 23% of the share count. That is 12 days of average trading volume and can be a powerful tailwind for the stock.

Takeaways from the Q2 earnings

Cyclical recovery in 2025

Management commented on the earnings call:

Looking ahead, we anticipate a modest recovery in U.S. shale activity in 2025 with steady oil markets and growth in natural gas markets from current levels.

This is in line with what both drilling and completions competitors are saying. Personally, I would not be surprised if the recovery gets pushed back to the end of 2025. So far, the U.S. LNG export infrastructure hasn't failed to disappoint natural gas bulls at every opportunity to do so - think of the Freeport outage for example.

But as the technical rule of thumb goes, the longer the base, the bigger the breakout.

The bifurcation is here to stay

Two market layers have emerged in the U.S. On one hand, large operators go for the modern and efficient equipment and aren't interested in inferior providers even at a lower price. The bottom layer, on the other hand, is more about price, but E&P consolidation is reducing this segment.

PTEN's management had strong comments about legacy pressure pumping (Tier 2) equipment during the call:

As we see the demand for activity start to pick up, this demand is going to be on equipment that can burn natural gas. Tier 2 is not going to have an easy place in there. We’re -- 80% of the equipment that we’re operating today burns natural gas. We’re essentially sold out on everything that convert natural gas.

So as we get into that part of the cycle where we start to see that demand increase, there is a shortage. Not that there will be a shortage. There is a shortage today of that type of equipment. And so that’s going to drive the need for more equipment of high spec in terms of burning natural gas in different forms.

The smaller services firms that run legacy Tier 2 fleets may see their market share go away soon, clearing the field for PTEN and the other big guys.

Commitment to shareholder returns

Management guided on generous shareholder returns during the call:

We expect to generate another quarter of strong free cash flow in the third quarter and in the second half of the year. We expect approximately 40% of our adjusted EBITDA to convert to free cash flow in 2024. Our Board has approved an $0.08 per share dividend for Q3.

For 2024, we expect to use at least $400 million to pay dividends and repurchase shares, which represents more than our usual commitment to return 50% of free cash flow to shareholders.

The total dividend payment for 2024 should be about $125 million, which leaves $275 million for buybacks. That is another 8% of the share count just for the remainder of this calendar year.

With 25% EBITDA margins, a 40% conversion rate implies 10% FCF margins. That is pretty good for a cyclical bottom.

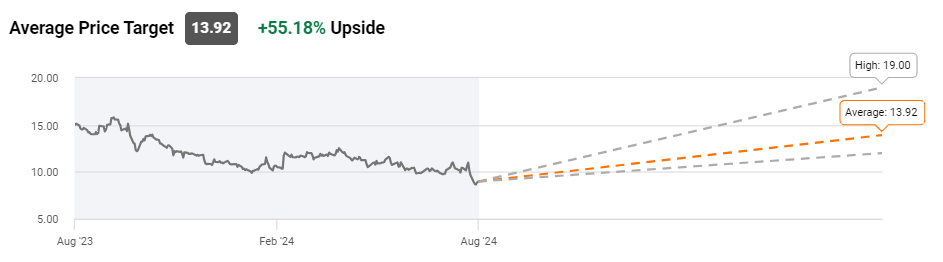

Valuation and price targets

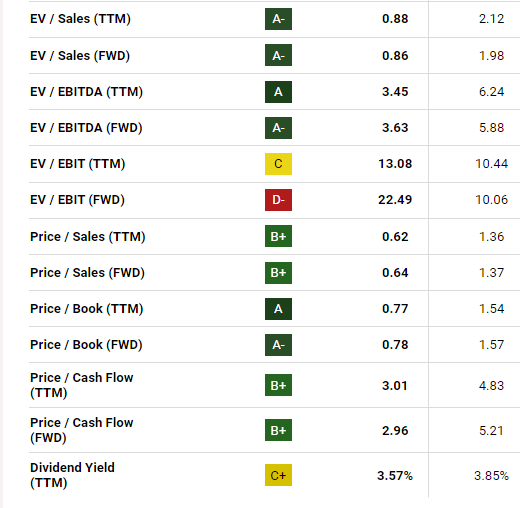

With the financial statement mess that can follow big acquisitions, I would frankly ignore the earnings multiples from the Seeking Alpha valuation panel and focus on EBITDA and cash flow:

Seeking Alpha

Enterprise value is 3.6x forward EBITDA, while the EBITDA estimate pretty much reflects flat industry conditions - that is, no rebound in natgas.

Bringing the multiple up to a rather unambitious 5.0x implies 50% upside for the stock price, and that is where Wall Street analysts seem to be on this:

Seeking Alpha

The multiple repricing by itself may be a tall order, though if the market remains disinterested in the energy sector and continues over-allocating to technology. This is where the buybacks come in, though, and can be a differentiator from PTEN's competitors that don't yet have a capital return program.

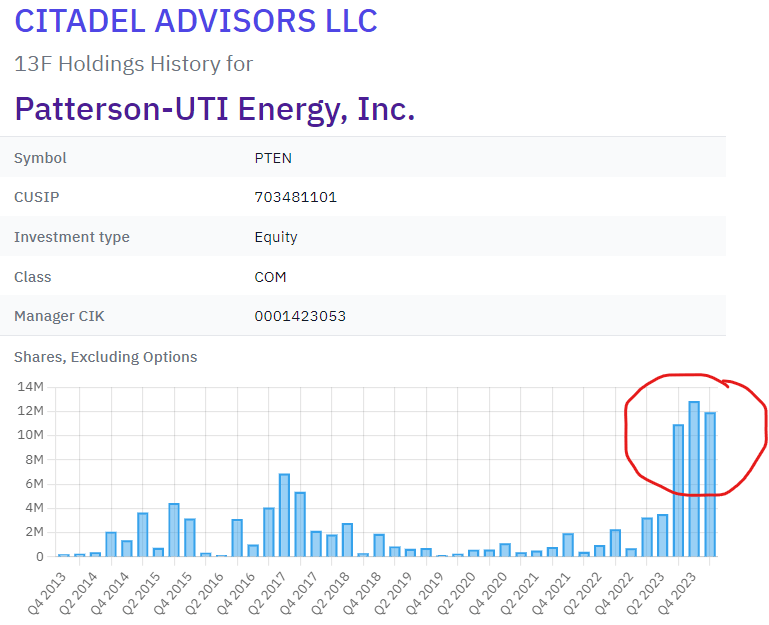

Some outside interest may be building up nonetheless. The renowned Citadel started accumulating in 2023 and appears to own 3% of PTEN now:

13f.info

Summary

Many U.S. land focused oilfield services stocks are undervalued, but PTEN is one of the fewer players that have a strong capital return program too. This should provide support for the stock price and some yield for investors while natural gas drilling makes a comeback sooner or later.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.