Join Gold Rally With Torex: Lower Stock Price In Sight

Summary

- A "Buy" rating is recommended for Torex Gold Resources, but to implement not immediately, but as soon as the stock is at the bottom of the share price cycle.

- The lower price is very likely and shouldn't take too long to arrive.

- Torex aims to extend production life, which is made at competitive costs, and supported by rising gold prices, and is well positioned to deliver robust margins and cash flow.

- The financial condition is enough to complete the development of the project in Mexico to extend the life of the mine through 2033.

kuppa_rock

A “Buy” Rating for Torex Gold Resources Inc.

This analysis recommends a “Buy” rating on shares of Torex Gold Resources Inc. (OTCPK:TORXF), a mid-sized gold producer based in Toronto, Canada, which holds a 100% interest in the Morelos gold property, a 29,000-hectare area in the southwest of Mexico City, in the Mexican state of Guerrero.

In this extended area of mineral property, Torex Gold Resources has 100% ownership in the Morelos complex, including the El Limón Guajes mine complex (“ELG”), which produces gold, silver and copper minerals (but it is almost exclusively gold, judging by the YTD 229,316 gold-ozs against 233,591 ozs AuEq) for the processing plant at the Media Luna project (just 7 km far from ELG). Here, the company operates the metal ore processing plant, which is currently undergoing a required upgrade and whose development is well underway, as the team continues to build a copper production plant (80% complete in Q2 2024), with completion scheduled for the last quarter of 2024, where the first commercial production of copper concentrate is expected to begin in early 2025.

However, the recommendation should not be implemented immediately, but only when the shares that appear to have entered the downside phase of their price cycle reach more attractive levels. By taking advantage of these more attractive levels, investors have a better chance of achieving a greater return when shares follow the price of gold in the expected new rally.

Reasons for the “Buy” rating

Torex Gold Resources Inc., hereafter “Torex”, is a good opportunity to take advantage of the gold price forecast. This is very promising because the price per ounce of the yellow metal is foreseen to be driven up by two catalysts, which this analysis will illustrate a little ahead.

Supported by the good dynamics in the operating business, whose recovery rates and production throughputs are at a level that signals an expansion of the gold equivalent business, the market will strongly associate the Torex shares with the optimistic sentiment towards gold, making easier for shares to follow the price of the yellow metal upwards.

About Production and Costs Target of Torex

Torex is a mid-tier producer that targets production of between 410,000 and 460,000 ounces of gold equivalent (“AuEq,” as the company also mines some silver and copper) in full-year 2024 at an industry-low All-In Sustaining Costs (“AISC”) of $1,130 to $1,190 per AuEq ounce sold. Excluding the contributions of silver and copper, Torex is targeting 400,000 to 450,000 ounces of gold at an AISC of $1,100 to $1,160 per ounce of gold sold.

The operating status combined with rising gold prices paves the way for robust profitability, a key share price driver.

Torex is on track to achieve the above target following a smooth operation in the first half of 2024, despite the planned one-month shutdown of the Media Luna Project processing facility in the fourth quarter of 2024 due to construction on the Media Luna Project. Unexpectedly, budgeted project investments recently increased by $75.5 million to approximately $950.5 million compared to the original forecast, but the well-funded construction work at the Media Luna project remains on schedule to achieve commercial production of copper concentrate expected in Q1 2025. This mitigates the investment risk, which in the case of mining in Mexico is classified as medium (yellow colour) by the Sprott Mining Risk Heat Map 2024, taking into account several social, geopolitical and economic factors as well as geophysical aspects.

The planned one-month shutdown of the Media Luna Project processing plant is necessary to enable commissioning and the first copper concentrate production in late 2024.

Torex Is Extending the Life of its Metal Production in Mexico

The investment for Media Luna is expected to extend the life of the mine of the Morelos complex through the final quarter of 2033, and the Media Luna project is expected to produce 280,000 ounces of gold per year, approximately 1.327 million ounces of silver per year and 34.8 million pounds (or approximately 15,800 tonnes) of copper per year. Over the life of the mine, based on long-term metal prices of $1,600/oz gold, $21/oz silver and $3.50/lb copper, these productions will lead to an expected 374,000 ounces AuEq sold per year at a total cash cost of $809/oz AuEq sold and mine site AISC of $954/oz AuEq sold. However, in a scenario where the Morelos Complex Process plant runs at full capacity until 2027, annual AuEq sold would be around 450,000 AuEq ozs at total cash costs of $779/oz AuEq sold and the AISC at $929/oz AuEq sold.

This Is How Things Are Going for Torex in Mexico

The company's operation is improving in terms of safety performance and avoiding as much as possible lost time and financial inefficiency when restarting operations, the mine and mill's operating performance continues in a better and better way, giving shareholders optimism for the rest of this year and beyond when commercial copper production begins at the Media Luna project. Through June 30, 2024, the number of lost days injuries ("LTIF") fell by 62.1% to 0.22 per million men at work hours on a rolling 12-month basis, benefiting operations that continue to show expansion as for the second consecutive quarter had an above-average 90% recovery rate with a YTD average of 90.6% and throughput consistently above 13,000 tons per day (“tpd”) for the sixth quarter in a row with a YTD average of 13,166 t/d (almost in line with YTD - 13,184 tpd in 2023).

Torex produced 229,316 ounces of gold year to date, almost as much as 230,425 ounces in 2023 (as higher recoveries and throughput offset some planned slightly lower grades from stockpile processing), at total cash costs of $966/ounce and AISC of $1,220/ounce, primarily due to continued strength of the Mexican Peso against the US dollar. While these increased versus the total cash costs of $775/oz and AISC of $1,187/oz YTD in 2023, they were still very low compared to industry trends. The benchmark is offered by the costs incurred in Q1-2024 by the small and mid-cap gold companies included in the VanEck Junior Gold Miners ETF (GDXJ) top 25 average cash costs/oz down 0.3% annually to $1,012 and average AISCs/oz down 8.4% YoY to just $1,294 or down 1.8% YoY to $1,389 without the exaggeration of a single extreme outlier Compañía de Minas Buenaventura S.A.A. (BVN), as reported by Mining.com.

Torex operations will continue to run more competitively than the industry average following the Media Luna project completion and in operation, with the Morelos Complex expected to incur total cash costs of $809/oz AuEq sold and mine site AISC of $954/oz AuEq sold through 2033 or in the full capacity-operating plant scenario with the Morelos Complex incurring total cash costs of $779/oz AuEq sold and AISC of $929/oz AuEq sold through 2027.

The Gold Bull Market Boosted Torex Margins and Shares

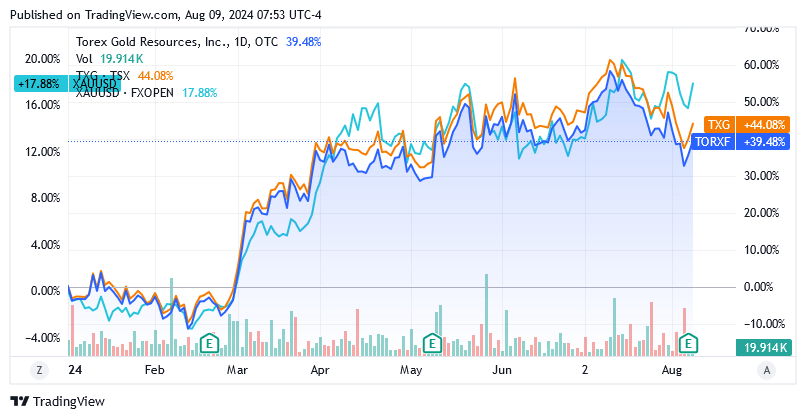

Thanks to attractive costs, higher AuEq volumes sold at 229,996 ounces YTD (up 2.6% year-on-year) and, driven by hopes of Fed interest rate cuts and robust safe-haven demand, rising realized gold prices averaging $2,109/ounce YTD (up 9.4% YoY) enabled Torex to report the following improvement in profit margins, which acted as effective upward drivers for the share price: AISC's margin was YTD $889 per oz sold, up 20% YoY, implying an AISC margin of YTD 42%, jumping 400 bps YoY. This combined with the bullish sentiment (ounce spot price up 17.88% YTD) that drove the yellow metal to its “fifth straight weekly increase on April 19”, scoring “a spot on the Metal Olympics podium on May 21” and reaching “the second-highest close ever on July 17”, created strong tailwinds for Torex shares in both North American markets: TORXF was up 39.48% on the “US-listed Over-The-Counter” market and TXG:CA was up 44.08% on the Toronto Stock Exchange market year to date.

Source: Seeking Alpha

The rise in gold prices was driven by a combination of geopolitical risks and strong demand for safe-haven assets, particularly in China, amid macroeconomic headwinds and fears of a resurgence in inflation as well as increasing hopes of a Fed rate cut at its September meeting and a weaker US$ dollar.

Other profitability metrics consisted of non-GAAP diluted earnings per share (EPS) of $1.02 for YTD in 2024, in line with YTD in 2023, on revenue of $506.8 million for YTD in 2024, up 15.2% year-over-year.

Instead, the adjusted EBITDA margin rate went down to 46.3% for the YTD period in 2024 versus the 54.2% rate for YTD in 2023, primarily due to the strengthening of the Mexican currency. However, the company has hedged against unforeseen exchange rate changes in the Mexican peso on costs through December 2025.

Free Cash Flow was negative YTD in 2024 equal to approximately $1.25/share or approximately $107.5 million, but Torex attributed the loss to the $234.6 million investment in the Media Luna Project for the YTD period. But free cash flow is on track to return to positive results once the project produces payable ounces, say from 2025, and metal prices remain very supportive as the current geopolitical and macroeconomic situation globally leads us to believe that will be the scenario of the future.

The Balance Sheet is Solid Enough to Support Metallic Projects in Mexico

Cash flow from operating activities of $177.2 million for the YTD period in 2024 (up from $136.6 million for the YTD period in 2023) should continue to perform well under the above circumstances, but even minus this contribution, Torex's balance sheet is strong enough to support the company in continuing its construction and exploration activities to support the mine life extension in the several upcoming years.

As of June 30, 2024, Torex's balance sheet had total available liquidity of $345.8 million, of which $108.7 million was in cash and $237.1 million was undrawn from the $300 million credit facility. The term of the credit facility was extended from 2026 to December 2027, with the possibility of an accordion feature of $150 million at the discretion of lenders. The balance sheet was burdened by long-term borrowings of nearly $54 million. This total liquidity, combined with a 12-month Interest Coverage Ratio ("ICR") of 141.5x, indicating strong debt solvency, even without considering operating cash inflows, provides Torex with sufficient financial resources compared to the need for an additional $224.4 million in expenditures for the Media Luna project until the end of 2024. The ICR is calculated as a 12-month operating income of $212.3 million on a 12-month interest expense of $1.5 million. Usually, investors use a factor of 1.5 to 2 to consider a company's ability to pay its debts as acceptable.

Profit from the Cyclicality of the Gold Price with Torex

Investors interested in a position in Torex shares should not hold this regardless of market fluctuations as these tend to be very long, with the Torex share price very sensitive to gold price cycles.

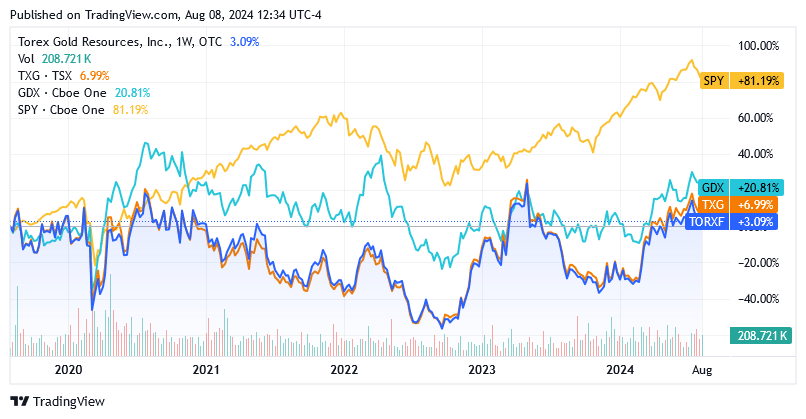

Torex shares rose just 3.1% on the US OTC market and 6.99% on the Toronto Stock Exchange, while the VanEck Gold Miners ETF (GDX) rose 20.81% and the SPDR S&P 500 ETF Trust (SPY) rose 81.19%, if e.g. for some reason investors had to soften the shares after 5 years of patiently holding Torex unchanged despite market fluctuations.

While past results are no guarantee of future results, they do provide a valid guide since we don't have a crystal ball. So, if the chart below is to be believed, Torex stock has underperformed stocks in the metals mining and exploration industry represented by the GDX and the overall U.S. stock market represented by the SPY, over the past 5 years.

Source: Seeking Alpha

Adjusting holdings to the cyclical fluctuations in the gold price, while always maintaining a certain volume of Torex shares as a "core position" in the portfolio, would certainly lead to better results and probably offer the opportunity to outperform the industry and the market.

The Upside Catalysts for Gold Ahead

One of the two bullish catalysts for gold prices mentioned earlier in this analysis is the Federal Reserve rate cut. At the time of writing, traders are pricing in a 54.5% chance of a 50-basis point (“bps”) rate cut and a 45.5% chance of a 25-basis point rate cut at the Federal Reserve's September meeting (currently the rate is 5.25-5.5%). Since gold does not provide any income, but its owner is only rewarded by an increase in the value of the ounce in the market, it tends to be more attractive when interest rates fall and wins the battle against US Treasuries or US bonds, which instead provide interest income based on a predetermined interest rate.

The second bullish catalyst for gold prices is its traditional safe-haven properties, which will be in high demand in the market as investors become increasingly interested in ways to protect the value of their assets from the consequences of a looming recession in the US. The following two indicators point to an impending sharp contraction in the US economic cycle:

- Economist Claudia Sahm, the designer of the Sahm Rule, believes that the US recession is likely to be three to six months from now. The Sahm Rule is an indicator that, performed on the last nine US recessions since 1970, has convinced most in the market about its intent to predict a subsequent one.

- The inverted yield curve indicator (three-month US Treasury yields are currently higher than ten-year US Treasury yields: 5.225% versus 3.942%), developed by Duke University professor and Canadian economist Campbell Harvey, also signals a looming recession for the US economy. Since World War II, this index has reliably predicted a recession 8 out of 8 times.

The Gold Price Outlook

The just mentioned upside-catalysts, therefore, lead analysts to predict these price targets for the yellow metal:

Recently, analysts of Morgan Stanley (MS) said to expect the yellow metal to trade at around $2,650 per ounce in the fourth quarter of this year, up 9.4% from its price of $2,422.88 per ounce at the time of writing.

For UBS Group AG (UBS), there is still significant potential for improvement in the yellow metal:

“The bank expects the gold price to reach $2,600/ounce by the end of the year and $2,700/ounce by mid-2025. For investors, an allocation to gold within a portfolio can be an attractive diversifier and a hedge, it added.”

Moreover, according to Trading Economics, the price of gold, which has been on an uptrend since the beginning of 2024, is expected to hover at $2,464.46/ounce before the end of Q3-2024. Looking ahead, they estimate that the yellow metal will hover at $2,549.74/ounce within the next 12 months.

The Stock Price Is More Attractive Than a Few Weeks Ago, But Even Lower than This Level Is Possible

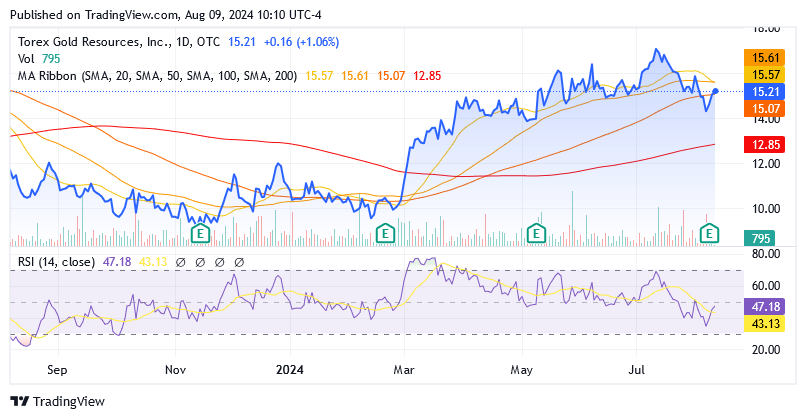

Torex Gold Resources Inc. shares (under the ticker symbol TORXF on the US OTC market) were trading at $15.21/share at the time of writing, representing a market capitalization of approx. $1.30 billion. Shares appear to be trading at lower levels now compared to a few weeks ago in the wake of negative sentiment that triggered a major sell-off between late last week and earlier this week due to some deterioration in the labour component of the economy, which gave rise to concern among investors about looming recession. However, these levels are not the lowest relative to recent trends: shares are not completely below the MA Ribbon, and the share price is still above the $13.34/share midpoint of the 52-week range of $9 to $17.68/share.

Source: Seeking Alpha

The 14-day Relative Strength Indicator of 47.18 suggests there is still plenty of room to the downside for shares to trade at more attractive prices than they are currently. Investors should therefore target these levels before implementing a “Buy” stance as suggested in this analysis if they wish to maximize their returns, as this stock is particularly suited to benefit from the cyclical nature of the yellow metal. The advanced processing plant project in Mexico and low-cost production are now providing further impetus to Torex's share price, setting the stage for better gains as gold prices begin to rise rapidly again.

But first, Torex share prices need to settle at a lower level, and the following downward catalysts offer an opportunity for this:

For market participants, the Fed can no longer delay the monetary policy pivot and must cut interest rates in September, as US non-farm payrolls hit their lowest level in three months last week and the US unemployment rate rose from 4.1% to 4.3%, suggesting the Fed should have acted already. At the July meeting, the Fed said a September rate cut could be on the table, but it's unclear by how much. The market has recently raised expectations that a 50-basis points ("bps") rate cut is planned for the September meeting, but will policymakers push through such a cut if they reverse course next month? Unlikely: As for the Fed, unemployment “remains low” according to the latest minutes of the July 31 meeting, and it is unlikely policymakers didn't know before the market that unemployment had risen to 4.3% if their job is so important as to require prompt action. Assuming instead that the historic US unemployment average rate of 5.69% is the benchmark, the economy would likely still need to lose non-farm payrolls before the Fed could be persuaded to cut interest rates by 50 basis points in September. But if the 4.3% unemployment rate is considered still low and therefore not alarming, a 25bps cut is also at risk and the Fed leaving rates unchanged again at the September meeting is not entirely out of the question. Meanwhile, a trend is taking hold among Fed rate traders and is that the chance of a 50-bps cut loosens steam cooling to 54.5% currently from 74% a week ago. Due to the downward pressure on non-income yielding physical gold, this cooling sentiment on the 50bps cut may not have another epilogue for Torex shares, so it is not unreasonable to expect lower stock prices from this point. The downward trend could become even steeper if the Fed does not cut rates at all at the September meeting.

Another event that could cause shares of Torex to move further down is the US recession. The risk of a recession is rising, as shown earlier in this analysis by the Sahm Rule and the Inverted Yield Curve Indicator by economist Campbell Harvey.

A recession in the US is likely to have a positive impact on the price of the yellow metal, as investors will be flocking to the safe haven traditional qualities of the yellow metal to protect their portfolios, increasing the demand for gold. Gold price increases will boost the profitability of the gold business in Mexico and will be reflected in Torex's share price, as earnings are a key driver of share prices, as previously seen. However, this kind of momentum will not play out immediately, and Torex shares will most likely face downward pressure initially.

In recent days, it appeared that a moderate deterioration in the employment situation was enough to send market participants into a panic, as they sensed that the US was heading into recession. This triggered massive selling activity among panicked investors and traders and did not spare gold stocks either. Over the past two days, the VanEck Gold Miners ETF has been able to pair losses, but in the five days leading up to Wednesday, when markets were still pessimistic, the benchmark index for gold companies was down 6.5 per cent.

This is because the market does not initially distinguish the shares of a gold mining company from the rest of the listed stocks amid sell-offs among panic-stricken traders and investors. When the recession hits the US, it's reasonable to expect headwinds for Torex shares as well, especially in light of a high 24-month beta market coefficient of 1.13x (scroll down to the "Risk" section of this web page).

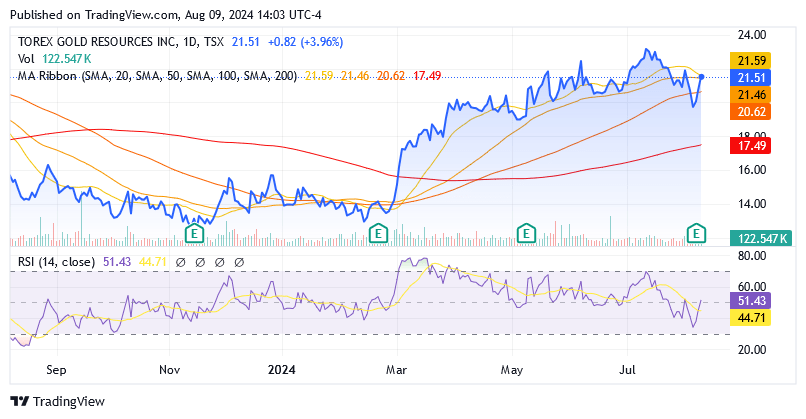

The same considerations apply to shares of Torex Gold Resources Inc. (TSX:TXG:CA), traded on the Toronto Stock Exchange, with a price of CA$21.51 per share and a market capitalization of CA$1.78 billion, as of this article. The 52-week range was at CA$12.40 to CA$23.56/share, shares were trading not completely below the MA Ribbon, and a 14-day RSI of 51.43 indicated shares could still hit lower levels.

Source: Seeking Alpha

The stock is characterized by the following daily trading volumes on both markets, which are not high volumes: Over the past 3 months, an average of 41,903 shares have traded on the US OTC market (scroll down this Seeking Alpha page to the “Trading Data” section), while on the TSX, an average of 261,276 shares changed hands (scroll down on this Seeking Alpha page to the “Trading Data” section).

The stock has 85.98 million shares outstanding, while a total of 85.68 million shares make up the float, which is freely tradable on the stock exchanges' open market, and institutions own 66.81% of the float.

If the volumes of shares traded daily are low, as in Torex's case, there is a potential problem that if the position is too fat, it may not be easy to bring to the desired volume if circumstances suddenly demand it.

Conclusion

Torex Gold Resources Inc. is a Canadian gold equivalent mining and exploration company with operations in Mexico that Torex is developing to extend mine life through 2033 and increase silver and copper production beyond the yellow metal. The company's financial position is solid enough to meet various obligations as well as to finance the development of the Mexican asset.

The outlook is good because the project is well advanced and fully funded, and the price of the metals, especially gold, on which Torex's profits almost entirely depend, is very rosy. Thanks to mine life on track to be extended, low production costs and rising metal prices, the company's cash inflows are well-positioned to deliver robustly.

Although stock prices of Torex are no longer so high, they could still fall significantly if the Fed does not cut interest rates in September as widely expected, or as soon as the US economy “officially” enters a recession. This stock deserves a "Buy" rating to implement, not immediately, but as soon as the stock has bottomed out in the stock price cycle. This analysis suggests waiting for the decision from the Fed in September on interest rates or the US recession biting operators' confidence and creating fears in the markets.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.