Equinox Gold: Higher Margins And Cheaper Share Prices Possible (Rating Downgrade)

Summary

- My analysis recommends a “Hold” rating for Equinox Gold Corp. Its shares are poised to benefit from the expected bull market for gold.

- Equinox is on track to increase gold production and reduce costs, increasing profitability, which could be a share price driver, provided that gold prices remain highly supportive.

- Investing in Equinox provides exposure to rising gold prices without directly owning physical gold, with the potential for an upside in the stock price.

- Under the influence of two identified events, stocks in both North American markets could become cheaper, but probably not soon.

brightstars

A "Hold" Rating for Equinox Gold Corp.

This analysis recommends a "Hold" rating for shares of Equinox Gold Corp. (NYSE:EQX) (TSX:EQX:CA) in the sense that investors should consider holding this gold stock in the portfolio to gain exposure to changes in the Gold Spot Price (XAUUSD:CUR). This is a downgrade compared to the Buy rating of the previous analysis. The reasons for this decision are described further down in this article.

The Previous Rating of "Buy"

In the previous analysis dated July 22, 2023, Equinox Gold Corp received a "Buy" rating as it was expected that a rapid rise in the price of gold would give the stock a significant boost. With production and costs already adding up as favorable inputs, the company's profitability, a key driver of the share price, was, thereafter, seen receiving support from precious metals prices as well.

The facts proved that the expectations were correct: Gold sales volume went from 148,231 ounces in Q3-2023 up to 149,861 ounces in Q4-2023 backed by rising production from 149,089 ozs in Q3-2023 up to 154,960 ozs in Q4-2023; costs were in line with expectations as AISC was $1,657/oz in Q4-2023 and $1,630/oz in Q3-2023, versus the full year 2023 guidance $1,575-$1,695/oz.; the average realized gold price rose from $1,917/oz in Q3-2023 to $1,983/oz in Q4-2023 amid robust demand for safe-haven assets, particularly from overseas investors. Thus, Equinox's share price found a solid basis for an upward trend in the positive development of the company's profitability. As a measure of Equinox's profitability, Adjusted EBITDA margin increased from 28.5% of total revenue in the third quarter of 2023 to 32% of total revenue in the fourth quarter of 2023.

So shares of Equinox had a generally bullish underlying trend, but as we will explain later, by taking advantage of the cyclicality of the gold price, investors had the opportunity to go much further with good chances of even beating the market, which has since grown by 18.5%.

The Reason for a Hold Rating Now in a Nutshell

The yellow metal is expected to experience a bull market as investors increasingly turn to its safe-haven traditional qualities against macroeconomic problems and geopolitical tensions. While gold is behaving bullishly in line with the expected scenario, driven by a positive correlation with the precious metal, the next trajectory is also likely to be up-trending for shares of Equinox Gold, hereafter "Equinox", amid bullish sentiment for gold. For the time being, the rating is "Hold" and not a "Buy" yet, as this analysis assumes that the market valuation can become significantly more attractive than it is now under the influence of certain downside factors.

On top of the above: Compared to the progress observed in the second half of 2023, a downward trend in production occurred at the Mesquite and Castle Mountain mines in California and the Arizona mine in Brazil in the first half of 2024. A setback that, however, should not be a cause for concern as the miner is on track to deliver more ounces of gold at a lower cost than before, thanks to the new Greenstone mine in Ontario, which will reach payable ounces of gold production this quarter. Such a development is generally received positively by the market and enhances the positive correlation between the stock price and the price of the yellow metal as the market more closely associates Equinox with the benefits of owning physical gold: as in previous bullish sentiments for gold, through an improvement in the company's profitability, a major stock price driver, the combination of higher gold production and prices combined with more affordable costs should have a positive impact on stock prices.

I believe investing in Equinox or other gold stocks is a much easier and cheaper way to potentially profit from the rise in the price of gold without investing directly in physical gold, as large institutions or central banks do. These investment entities have sufficient capital to purchase gold bullion, which in many cases might be out of reach for an individual investor.

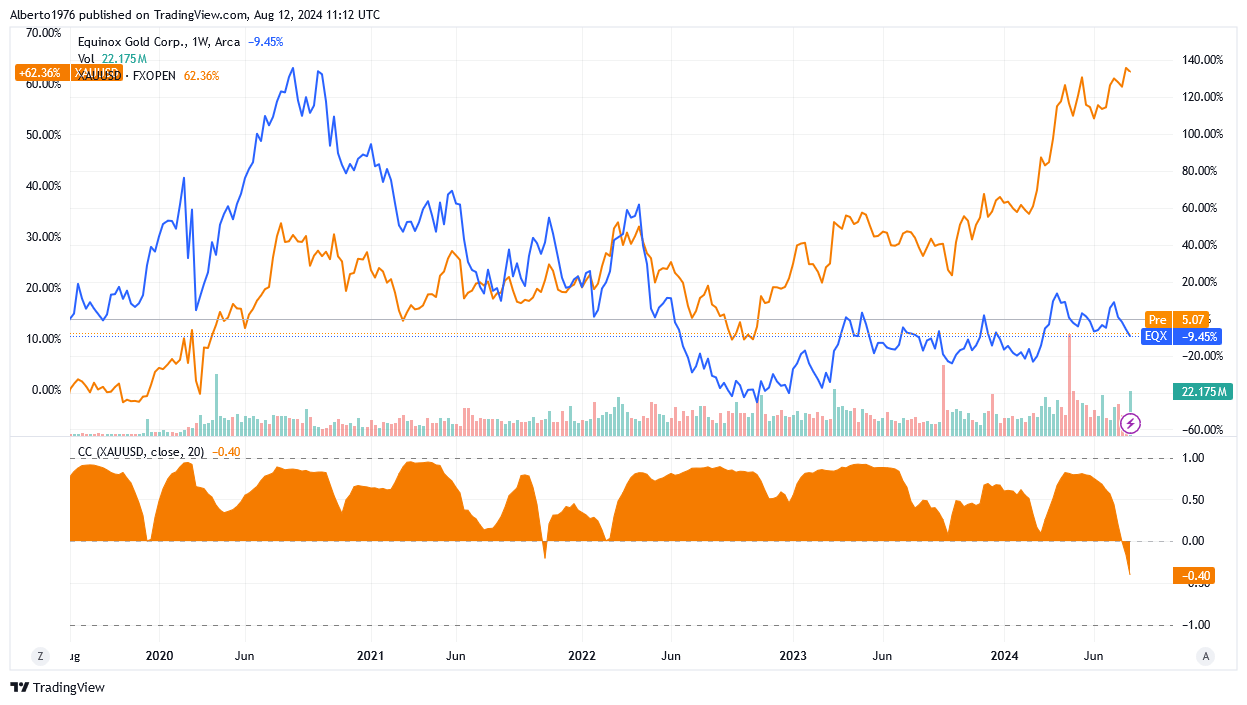

A Graphic Explanation of the Positive Correlation Between Equinox and Gold

In the chart below, the positive correlation between shares of Equinox under the symbol EQX in the NYSE market and Gold Spot Price or XAUUSD:CUR is represented by a robust dark yellow area that was almost always above zero.

Source: TradingView

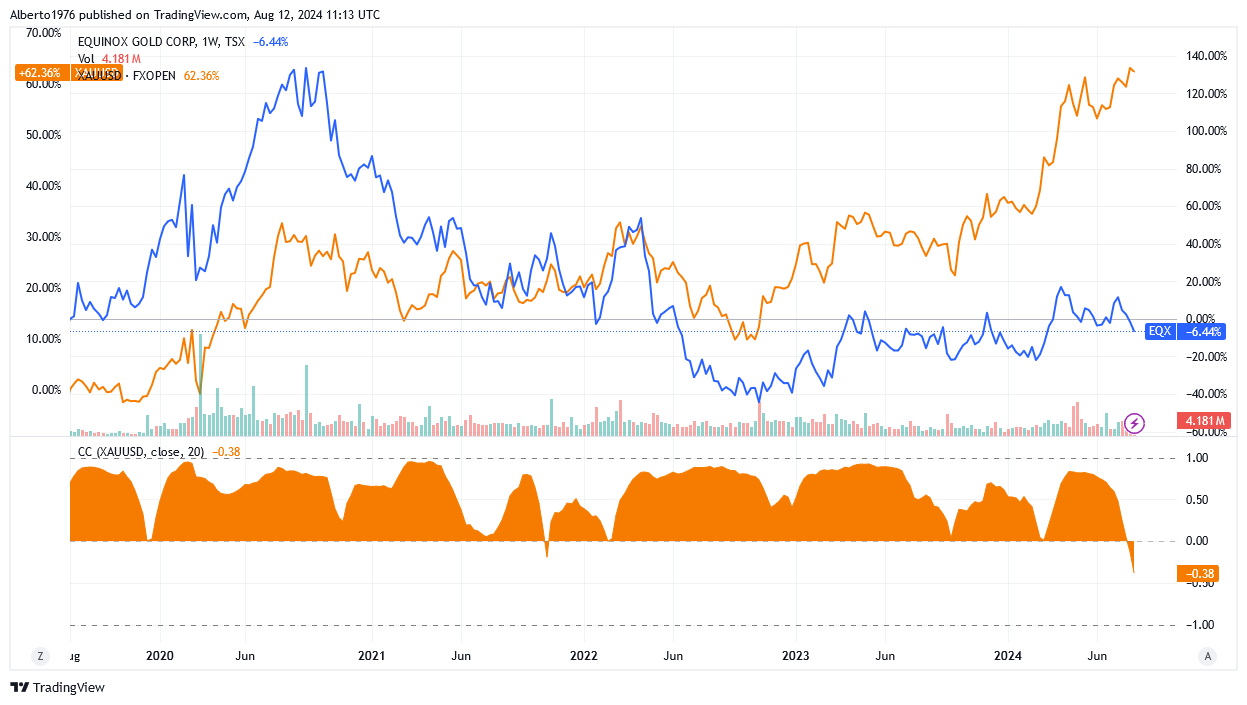

In the chart below, the positive correlation between shares of Equinox under the symbol EQX:CA in the Toronto Stock Exchange market and Gold Spot Price or XAUUSD:CUR is represented by a robust dark yellow area that was almost always above zero.

Source: TradingView

A positive correlation means that Equinox shares and the gold price move in the same direction: either both up or both down, regardless of returns which can vary significantly between them.

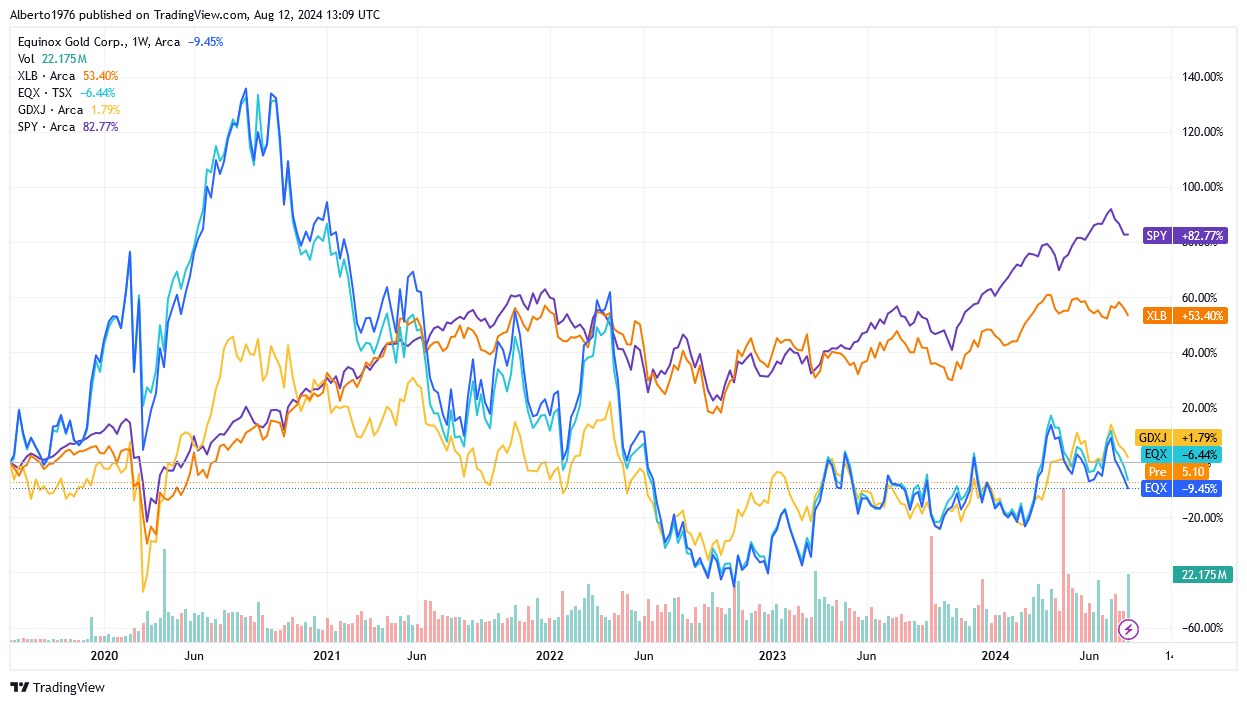

Profit from Gold Cyclicality through Equinox

The chart above shows about 5 years of market trading and is therefore a long enough time horizon to understand that Equinox is not a way to profit from rising gold prices by holding stocks for the long term, regardless of gold price cycles.

The following chart can better illustrate this point. If regardless of cyclicality investors had bought and held positions in Equinox while the underlying downtrend was negative, they would have achieved the following performance over the past 5 years: EQX -9.45% on the NYSE, EQX:CA -6.44% on the TSX, while the Materials Select Sector SPDR® Fund ETF (XLB) rose +53.40%, the VanEck Junior Gold Miners ETF (GDXJ) gained only 1.79%, and the SPDR® S&P 500® ETF Trust (SPY) gained 82.77%.

Source: TradingView

XLB tracks the North American stock market for basic materials stocks; GDXJ is the industry benchmark for North American listed stocks in the small/mid-tier gold mining and exploration sector; and SPY is the industry benchmark for North American listed stocks.

Instead, the position must be adjusted according to changing gold price dynamics, as investors want to avoid the investment losing competitiveness against the market while increasing the chance of a higher return.

The Next Cyclicality: Operating (Equinox) and Gold Price Factors

For the full year 2024, Equinox said it can potentially supply markets with a production of 655,000 to 750,000 ounces of gold at a cash cost of $1,305 to $1,405/oz and All-In Sustaining Cost (AISC) of $1,635 - $1,735/oz.

The 2024 operation will represent a significant improvement over actual 2023 numbers, as Equinox produced 564,458 ounces of gold last year at cash costs of $1,350/ounce and AISC of $1,622 per ounce. Compared to the guidance 2024 mid-range, operations will reflect an increase of 24.5% in gold ounces, a reduction in cash costs of 0.4%, and an AISC decrease of 3.9%.

In terms of shares of the total consolidated production of Equinox for the full year 2024, gold ounces will be derived from the 100%-owned Greenstone mine in Ontario for 27%, from the United States (100%-owned Mesquite mine in Yuma, California and 100%-owned Castle Mountain mine in Las Vegas, California) for about 11%, and from 100%-owned Los Filos Complex in Mezcala, Guerrero, Mexico for 23.5%, and from 4 Brazilian mines for approximately 39% of the total.

The Brazilian gold mining segment consists of the 100%-owned Aurizona mine in Godofredo Viana, the 100%-owned Fazenda mine in Salgadalia, the 100%-owned Santa Luz mine in Santa Luz, and the 100%-owned Riacho dos Machados (RDM) mine in Riacho dos Machados.

The Sprott Heat Mining Map 2024 shows the minimal risk for the mining business in North America, medium risk in Mexico and low risk in Brazil.

Mines in Action: How They Perform

All of these mines are expected to perform well, while the Mesquite mine, Aurizona mine and Castle Mountain will produce lower ounces for the full year of 2024. The Mesquite operations are currently facing a decline in recovery rates, temporarily due to heap leaching performing slightly slower than expected with recovery rates. An unpredictable geotechnical event caused the Aurizona mine to temporarily stop operations in May and June, resulting in a production loss triggered by a one-off setback. Finally, production at Castle Mountain will also be less supportive throughout the year, but this will be a planned consequence of the cessation of mining as the company now wants to focus on its 200,000-ounce-per-year expansion project to advance to Phase 2. Mining will remain suspended for the duration of phase 2 - at this time there is no estimate of how long this phase could take to obtain the necessary permits - and the plant will continue with what is left from leaching and other gold production activities.

These decreases in gold ounces will be offset by Equinox thanks to the ramp-up of the production at the Greenstone mine in Ontario, as the gold-yielding facility will reach commercial production sometime this quarter after pouring the first gold in late May 2024. Greenstone Mine will be the most significant in Equinox's portfolio of gold-producing mines: at full capacity, the mine will produce 400,000 ounces of gold annually in the first five years of operation, but on average the facility is expected to produce 360,000 ounces of gold per year over at least 10 years of gold activities with strong potential to extend the life of the mine through explorations.

Equinox will continue to operate its mines at costs that are not the most compelling compared to the benchmark: small and mid-cap gold companies included in the VanEck Junior Gold Miners ETF (GDXJ) top 25 on average endured the following costs: cash costs of $1,012/oz. and AISCs/oz of $1,294/oz or $1,389/oz without the exaggeration of a single extreme outlier Compañía de Minas Buenaventura S.A.A. (BVN), as reported by Mining.com.

The Upside Catalysts for the Gold Bull Market

Profitability requires a high gold price to create an effective upside catalyst for the share price in both North American markets. For its part, the price of gold will have two main reasons to continue to rise in the coming months, and these are the start of interest rate cuts by the US Federal Reserve and the economic recession, which Rosenberg Research founder and president David Rosenberg considers "not too far away,". This, as well as the following 2 indicators, signal a deterioration in the economic cycle.

A lower interest rate will induce demand for gold to the benefit of the price per ounce because physical gold does not provide any income like its competitors, US Treasuries and other US bonds: the opportunity cost for investors to invest in gold rather than government bonds will receive downward pressures from September if, as it seems, the Fed pivots its interest rate policy.

Concerning the other upside catalyst for gold prices: The markets do not like the prospects of recession, and their reactions can be bad for the profitability of investors' portfolios. In search of protection, investors will be even more interested in the demand for gold, since the yellow metal is also popular for its safe-haven qualities. The following two indicators point to a looming recession in the US.

- Economist Claudia Sahm, the designer of the Sahm Rule, believes that the US recession is likely to be three to six months from now. The Sahm Rule is an indicator that, performed on the last nine US recessions since 1970, has convinced most in the market about its intent to predict a subsequent one.

- The inverted yield curve indicator (three-month US Treasury yields are currently higher than ten-year US Treasury yields: 5.219% versus 3.907%), developed by Duke University professor and Canadian economist Campbell Harvey, also signals a looming recession for the US economy. Since World War II, this index has reliably predicted a recession 8 out of 8 times.

The Outlook for the Price of Gold in Light of its Upside Catalysts

Gold joined the global equity market sell-off early last week, but Ewa Manthey, commodity strategist at ING Groep N.V. (ING), predicts the price will "regain its footing amid ongoing geopolitical uncertainty and expectations of interest rate cuts in the U.S.," she said in the bank's latest monthly update.

In addition to the above factors, Manthey also expects the current economic climate, which supports both central banks buying and the strong inflows into global gold ETFs, as well as the US presidential election in November, to "contribute to gold's upward price momentum until the end of the year."

According to Manthey's gold price forecasts, following a retreat from record-high prices, the metal "will average $2,380/oz in Q3 and peak in Q4 at $2,450/oz, resulting in an annual average of $2,301/oz."

The gold spot price is at $2,462.84/oz at the time of writing.

In addition, analysts at Morgan Stanley (MS) said at the end of July 2024 that "they expected the yellow metal to trade at around $2,650 per ounce in the fourth quarter of this year," while analysts at UBS Group AG (UBS) said to "expect that the gold price will reach $2,600/ounce by the end of the year and $2,700/ounce by mid-2025."

Moreover, according to Trading Economics, the price of gold, which has been on an uptrend since the beginning of 2024, is expected to hover at $2,549.74/ounce within the next 12 months.

First Half of 2024: Positive Catalysts Identified for the Upcoming

On a year-over-year basis, the strong gold price increase - as Equinox's average realized gold price increased 13.8% year-on-year to $2,197/oz in 1H2024 - has been very important in offsetting the headwinds from the decline in production (a decrease of 10.2% YoY to 233,946 ozs in H1-2024) and sales volumes (down 11.3% YoY to 231,927 ozs), primarily triggered by the temporary negative factors highlighted earlier, which led to higher cost levels. Cash costs per ounce sold increased 22.1% year-over-year to $1,653 and AISC increased 26.5% year-over-year to $1,993/oz.

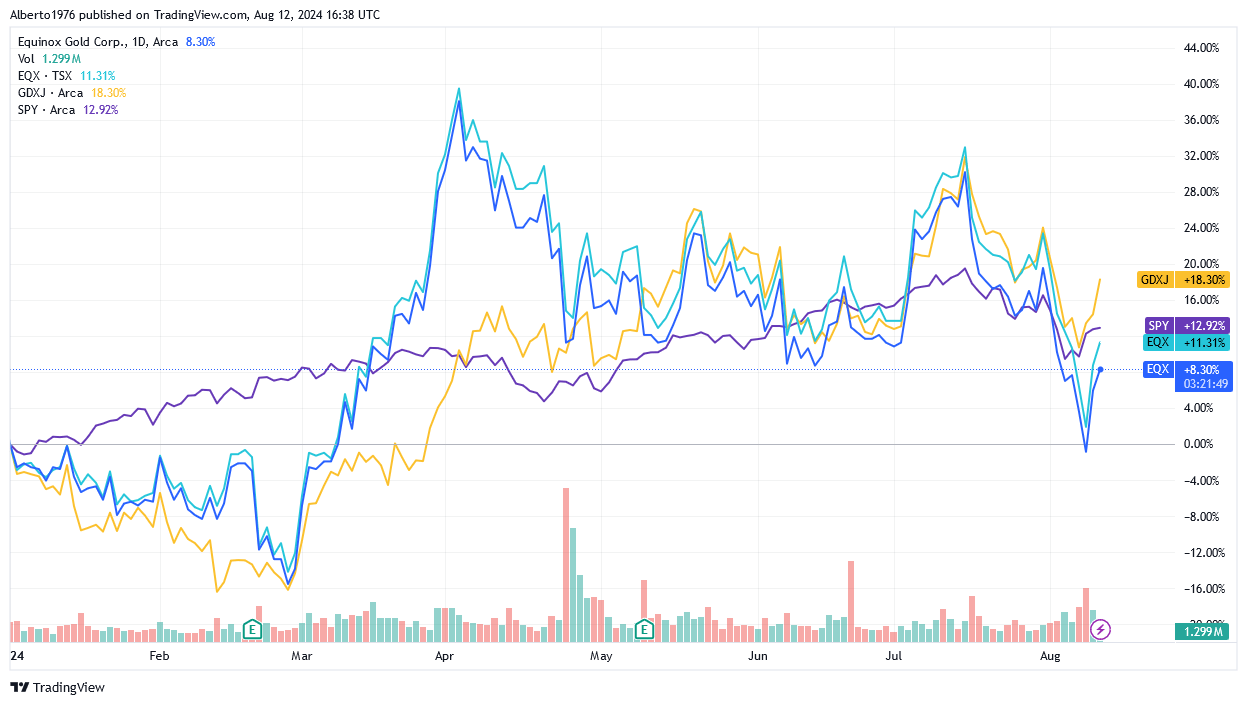

The bullish sentiment around gold with an ounce spot price up 17.9% YTD helped Equinox profit from a whopping jump in the gold price realized on the sale of its ounces of the precious metal. In the market, the yellow metal was pushed to its "fifth straight weekly increase on April 19", scored "a spot on the Metal Olympics podium on May 21" and reached "the second-highest close ever on July 17". The rise in gold prices was driven by geopolitical risks and strong demand for safe-haven assets, particularly in China, amid macroeconomic headwinds and fears of a resurgence in inflation. Also, increasing hopes of a Fed rate cut at its September meeting and a weaker US dollar boosted the gold price.

The drop in ounces and higher costs in 1H 2024 had an impact on shares of Equinox as EQX was +8.3% on the NYSE and EQX:CA was +11.31%, while GDXJ was +18.38% YTD on an 18% rise in the gold price. However, they are still behind the SPY at +12.92% and the critical role of bullishness in gold prevented the gap with the US-listed stocks from becoming unbridgeable, especially for shares in the Canadian stock market. Also because without the 13.8% year-on-year increase in the realized gold price/ounce to $2,197, Equinox's profitability, a key share price driver, measured by the EBITDA margin of 20.3% in H1 2024 compared to 25.3% in H1 2023, would have declined more sharply. The latter would have wiped out the tailwind from revenue growth from $505.7 million in H1 2023 to $510.8 million in H1 2024, despite the significant decline in sales volume.

Source: TradingView

However, with Equinox's full 2024 gold production and costs on track to have a much more favorable impact on profitability than the first part of 2024, assuming gold prices remain as strongly supportive as predicted by the analysts mentioned earlier, there is no reason why margins should not improve. And if they do, they will provide a strong upside catalyst for shares.

For the full year 2024, the gold production range is 655,000 - 750,000 ounces, compared to 467,892 ounces (if the mines continue in line with the trend seen in the first half of 2024).

For the full year 2024, cash costs are expected to be more affordable between $1,305 and $1,405/oz and also AISC are with a range of $1,635 to $1,735/oz, compared to cash costs of $1,653/oz and AISC of $1,993/oz in H1-2024.

The Financial Situation Manages Expenses and No Need for Further Debt

Equinox's ongoing financial condition appears strong enough to support the operation of its gold-producing mines, as well as facility improvements and the 200,000-ounce-per-year Castle Mountain expansion project to phase 2 and the ramp-up of the Greenstone mine.

As of June 30, 2024, Equinox had $167.5 million in cash and equivalents (unrestricted), which together with operating cash flow ("OCF") expected to be significantly higher than the $186 million by annualizing H1-2024 ante-changes OCF of $93 million, is therefore on track to more than offset the $238 million in sustaining and non-sustaining expenditures in the second half of 2024.

The company guides for a total of $465 million to be allocated to sustaining and non-sustaining spending for the full year 2024 but has already allocated $114 million in Q1-2024 and $113 million in Q2-2024.

Plus, on the balance sheet, there is an inventory valued at $418.9 million as of June 30, 2024, but this item with prices and production trending upward should provide stronger potential for additional value to unlock going forward.

The balance sheet was burdened with a total debt of $1,626.1 million, of which 86.2% was long-term, resulting in an interest expense of $71.3 million for the trailing 12 months ending June 30, 2024. Equinox has generated operating income of $40 million in the trailing 12 months to Q2-2024. The interest coverage ratio calculated as 12 months' operating income on 12 months' interest expense is 0.6x. The ratio measures a company's ability to economically sustain the capital loan. I recommend a minimum level of 1.5 to 2 times, so that means Equinox is below acceptable solvency. But profitability is on an upward trajectory amid expected higher sales volumes and gold prices and lower costs, and there is no need to take on additional debt as internal resources can more than cover expenses. Rather, interest expense will improve as the company can also repay some debt, so once the solvency ratio moves closer to 1.5 to 2x, it will add more upside momentum to the stock.

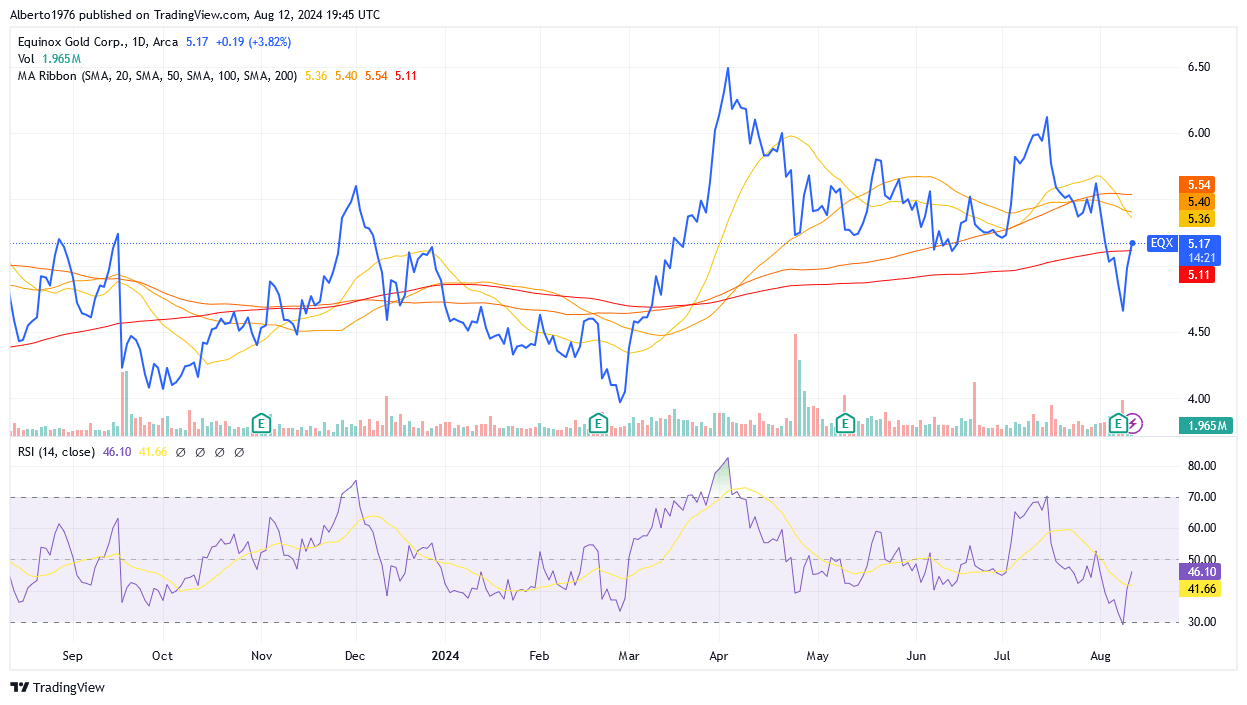

The Share Price: A More Attractive Stock Price Is Possible

Equinox shares (under the ticker symbol EQX on the NYSE) were trading at $5.16/share at the time of writing, giving it a market capitalization of $2.13 billion. Shares are lower now compared to a few weeks ago in the wake of a big sell-off between the end of 2 weeks ago and earlier last week as some deterioration in the labor component of the economy raised recession concerns. However, these levels are not the lowest relative to recent trends: shares are not completely below the MA Ribbon, and the share price is near the $5.225/share midpoint of the 52-week range of $3.95 to $6.50/share, thus not significantly in the lower half of the interval yet.

Source: TradingView

The 14-day Relative Strength Indicator of 45.83 suggests that there is plenty of room for the downside if the shares are to reach more attractive price levels than the current ones. Investors may want to maintain a hold recommendation until these more attractive levels are reached. While shares are well positioned for a rally as gold and Equinox have laid the groundwork for rising profitability, a major stock price driver, investors have a better chance to maximize upside potential by buying at lower price levels.

However, until Equinox's share price settles at lower levels - which the following downside catalysts provide the opportunity to do so - investors are advised to stick to Hold for the time being.

In the wake of US non-farm payrolls hitting a three-month low and US unemployment rising from 4.1% to 4.3%, market participants say the Fed can't wait any longer, but policymakers will have to cut interest rates in September. At the time of writing, interest rate traders are giving a 48.5% probability of a 25-basis-point cut to the 5%-5.25% range from the current 5.25% to 5.50%. Market participants went even further and targeted a 50-basis points cut in September, fearing that a deteriorating labor market was a sign of a recession in the U.S. economy and that the Fed should have acted earlier, in July. The rate cut now should be by 50 basis points, not 25, to make up for lost ground, according to some. These concerns led to a wave of sustained selling in the stock market last week.

But since the 25-bps cut has most likely been factored into gold prices and listed stocks such as Equinox, as the Fed itself admitted in the July meeting minutes that a rate cut could be on the table going forward; for the 50 basis points instead, the situation may be quite different.

First, if the Fed's task is so critical that some market participants last week even called for action ahead of schedule to avoid a recession, then it is unlikely that policymakers were not aware of the rising unemployment rate before the data was made public a few days later. As for the minutes from the July 31 Fed meeting, policymakers say unemployment "remains low." But how much does the unemployment rate have to rise before the Fed cuts rates by 50 basis points? Assuming the Fed uses the average historical U.S. unemployment rate of 5.69% as a benchmark, the economy would still have to shed nonfarm jobs before the policymakers could be persuaded to make such a rate cut. If the U.S. is headed for a recession, the system will lose even more nonfarm jobs in the future. But it is unlikely that the system will destroy enough jobs between now and September to prompt the Fed to reverse its policy by 50 basis points. A rate cut could come in September, but the 50-basis point cut, triggered primarily by short-term volatility last week, seems destined to lose momentum, leading to a cooling sentiment in the price of gold and Equinox shares. Fed rate expectations for a 50-bps rate cut have already fallen sharply and currently stand at 51.5% (at the time of writing), down from 85% a week ago.

Another event that could cause shares of Equinox to move lower is the US recession, which is not too far off for previously mentioned economist David Rosenberg and also indicated by the Sahm Rule and the inverted yield curve indicator by economist Campbell Harvey.

A recession in the US is likely to have a positive effect on the price of the safe-haven gold, and Equinox shares will benefit as well through increased profitability. However, the positive momentum will not be immediately transferred to Equinox shares; on the contrary, they will initially come under downward pressure in my opinion.

In recent days, a deterioration in the employment situation has caused market participants to panic, as they believed there were clear signs of a US recession. The significant selling activity that followed panicked investors and traders did not spare gold stocks either. In the last two to three days, the VanEck Gold Miners ETF was able to offset losses, but in the five days before Wednesday, when the markets were still pessimistic, the leading index for gold companies lost 6.5%.

The market does not initially differentiate the shares of a gold mining company from the rest of the listed stocks. Therefore, when the recession hits the US, Equinox stock is also expected to face headwinds, especially in light of a high 24-month beta market coefficient of 1.70x (scroll down to the Risk section of this webpage).

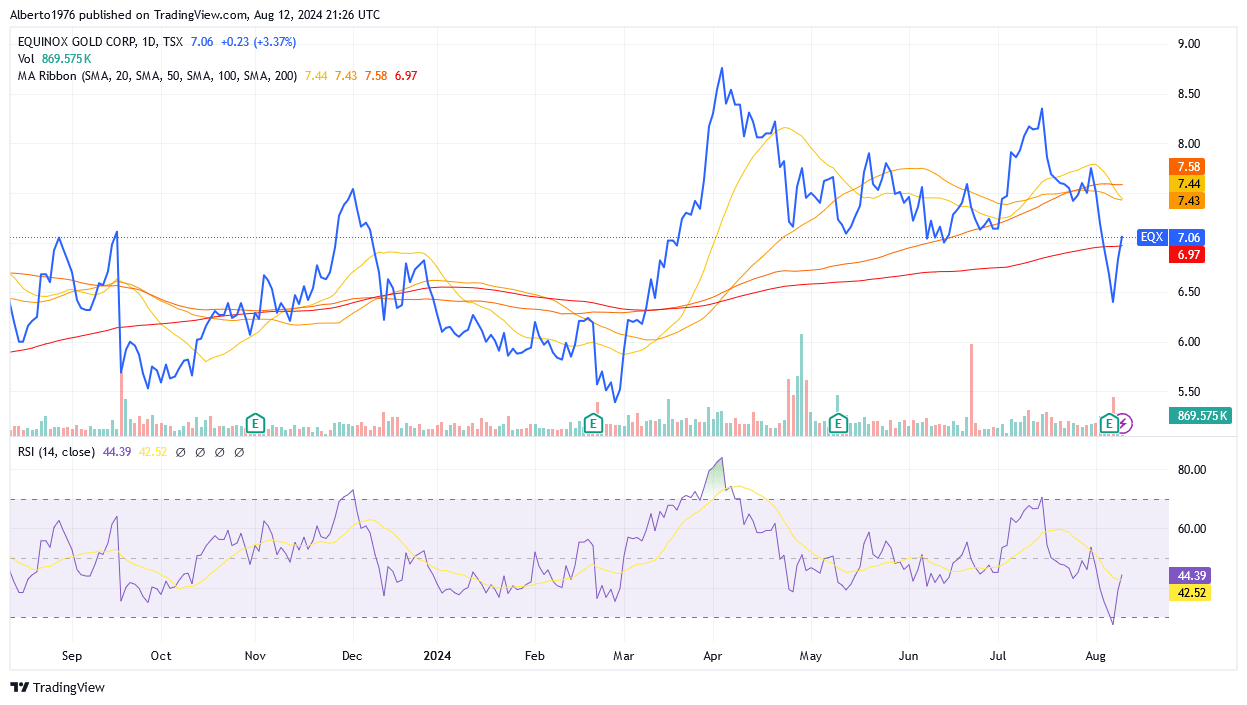

The same considerations apply to shares of Equinox Gold Corp. traded on the Toronto Stock Exchange under the EQX:CA symbol, with a price of CA$7.06 per share and a market capitalization of CA$2.93 billion, as of this article. The 52-week range was at CA$5.36 to CA$8.79/share, shares were trading not completely below the MA Ribbon, and a 14-day RSI of 44.39 indicated shares could still move downwards.

Source: TradingView

The stock is characterized by the following daily trading volumes on both markets, which are not low but not very high volumes either: Over the past 3 months, an average of 2.75 million shares have traded on the NYSE market (scroll down this Seeking Alpha page to the "Trading Data" section), while on the TSX, an average of 617,890 shares changed hands (scroll down on this Seeking Alpha page to the "Trading Data" section).

The stock of Equinox has 428.51 million shares outstanding, while a total of 400.34 million shares make up the float, which is freely tradable on the stock exchanges' open market, and institutions own 54.58% of the float.

Conclusion

Equinox Gold Corp. is a gold-producing company with mines in Ontario, California, Mexico and Brazil. Thanks to a sharp increase in the price of gold, the company has achieved acceptable performance despite declining recovery rates and a cessation of mining activities to prioritize a production expansion project in California, as well as an unforeseen geotechnical event at the Aurizona mine in Brazil, where the company had to temporarily suspend operations in May and June.

Most of these issues have been overcome and if some of the affected operations continue to experience lower gold ounces issues, these will be offset by the new Greenstone mine in Ontario, which will enable production of commercial ounces of gold this quarter.

Equinox plans to produce more ounces in 2024 than in 2023, versus the H1-2024 trend, and with costs that will be lower than a year ago and significantly cheaper than the H1-2024 trend. The gold price will experience another bull market, and Equinox should realize an even higher price per ounce sold in the coming months. Everything appears to be geared towards improving Equinox's profitability, a key driver of the share price, and the solvency ratio should also make notable progress, which should give Equinox stocks further upward momentum in the North American markets. The financial position is strong enough to continue operations, support asset optimization efforts, finance the expansion project and ramp up commercial production of the new mine in Ontario. Shares may become cheaper in the coming weeks, and until then, investors can maintain the "Hold" rating.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.