Amerigo Resources: Business Improves, Solid Long-Term Prospects And Potential Interesting Dip

Summary

- Amerigo Resources Ltd. maintains a "Hold" rating, with two upside catalysts supporting long-term growth.

- The company operates in the basic materials sector, producing copper and molybdenum in Chile from tailings processing operations.

- Strong financial results, operational improvements, and a bullish copper market contribute to Amerigo's positive outlook for the future.

fmajor

A “Hold” Rating for Amerigo Resources Ltd.

This analysis confirms another “Hold” rating on shares of Amerigo Resources Ltd. (OTCQX:ARREF) (TSX:ARG:CA), the same rating given in the previous analysis.

Amerigo Resources Ltd., hereinafter referred to as “Amerigo”, is based in Vancouver, Canada and operates in the basic materials sector as a copper and molybdenum producer with production in Chile.

Amerigo produces copper and molybdenum from the processing of fresh and historical tailings extracted as a result of the production of the metals in the El Teniente underground mine in Chile. Amerigo owns 100% of the tailings processing operations, while Codelco (which is short for “The National Copper Corporation of Chile”), a Chilean state-owned copper mining company, owns the underground mine at El Teniente.

The Previous Rating of “Hold”

Supported by two relevant upside catalysts with long-term positive implications, Amerigo's North American-listed shares had received the previous rating, taking into account that the market could make the share price even more attractive, so a Hold recommendation was preferred to a Buy recommendation. These catalysts continued to guide shares of Amerigo since the previous analysis dated June 30-2023, and as expected the shares advanced in the green territory and yielded 9.27% and 16.66%, respectively, at the time of this article (including the payment of a quarterly dividend of CA$0.03/share ≈US$0.02/share).

The US stock market has outperformed with a gain of 22.90% as shown by the S&P 500 change. However, as already indicated in the previous analysis and suggested here, if the investor had made wise use of the cycles in stock prices, as these are tied to the fluctuations of the metals, he would most likely have also outperformed the US stock market. As the following section illustrates, along the way from the time of the previous rating, the market also allowed a markedly lower price, a so-called dip, which the investor could subsequently exploit to strengthen the position in the stock of Amerigo given the long-term uptrend potential.

Now is the Time for a “Hold” in your “buy and hold” scheme: Maximize It Through Cyclicality

With a share price that tends to rise over time, not steadily but through cycles, you now own shares but are likely looking to increase the position as soon as the stock becomes attractively priced in the market.

For example, attracted by the idea of strengthening a “buy-and-hold” approach-based long-term strategy, cyclicality allowed the investor to increase his Amerigo shares in the wake of a lower copper price for a few sessions in October. Copper prices faced 2 weeks of declines on Oct. 13, 2023, “as markets remained wary of a higher interest rate environment” that, along with a stronger USD, according to analysts at JPMorgan Chase & Co. (JPM), was “the biggest short-term bearish risk for macro-focused copper”. But markets preferred to remain dodgy also due to “persistent economic challenges in the world’s largest copper consumer, China,” after Chinese property giant Country Garden warned “its ability to meet offshore debt obligations” was being tested by “significant challenges.” Around October 24, 2023, shares of Amerigo formed a dip in the stock price that, ahead of the subsequent rally fueled by higher commodity prices and the company's profitability, allowed the holding to grow astonishingly in value, peaking around May 20th. Thereafter, “a supply that struggles to keep up with rising demand” was the factor that pushed copper prices into a strong rally in the first part of 2024, “rising 28% YTD to a record high of $11,104.50/tonne in the week ending May 24”, reported Carl Surran, Seeking Alpha News Editor. In addition, hedge fund manager Pierre Andurand, “one of the world's best-known commodity traders” reported Carl Surran, was convinced that the upside factor would give additional impetus to the price of copper going forward and “the price could even quadruple to $40,000 per ton” in a matter of few years from then.

The Development of Amerigo Activities Since the Last Rating

From an operational perspective, shares benefited from these events: Amerigo's strong financial results in the fourth quarter of 2023 as operations returned to normal following a period of higher capital expenditures required to address production losses because the mining area at El Teniente was constrained by rock burst and heavy rainfall in 2023. The company reported for the fourth quarter of 2024, a net income of $3.9 million, or $0.02 per share, against cumulative losses for the first nine months of 2023. In Q4-2023, EBITDA was $11.2 million and free cash flow to equity was $6.5 million. The latter was the company’s “ultimate financial performance measure,” said Aurora Davidson, the President and Chief Executive Officer of Amerigo. Instead, the EBITDA margin of 26.4% in Q4 2023 (compared to 28.3% in Q4 2022) and free cash flow (this item was $9.2 million in Q4 2022) were still lower year-over-year year-on-year, but this was also due to the copper price, which at $3.82/lb in Q4 2023 (approximately the same as Q4-2022 level) was still at the beginning of its bull market. Amerigo said it was once again building cash for shareholders, reinforcing the company's continued focus on returning strong capital to shareholders and increasing the reliability of the quarterly dividend payment, thus effective share price drivers. Then, these find solid support in continued improvement on a sequential basis in profitability as measured by EBITDA margin of 30.3% and free cash flow of $7.3 million for the first quarter of 2024. But while the rise in the copper price to $3.95 was still too shy compared to the positive development it subsequently had through the May 20-2024 peak, by helping volumes and costs get back on track for long-term growth, the recovery in operations in the El Teniente mine area contributed the most to the improvement in Amerigo's profitability. This dynamic resulted in significantly lower capital expenditure. Amerigo production and costs, as follows, were again within company guidelines: production was 16 million pounds of copper (nearly on par with Q1-2023: 16.5 million lbs.) and 0.3 million pounds of molybdenum (in line with Q1-2023) while cash costs were $1.89/lb from continuing activities (lower than Q1- 2023: $1.91/lb).

Finally, the bullish copper market and thus red metal prices too began to contribute to Amerigo's financial strength in the second quarter of 2024, as evidenced by an increase in cash holdings from $16.2 million in Q4-2023 up to $28.7 million in Q2-2024 combined with a reduction in borrowing from $20.7 million in Q4-2023 down to $14.4 million in Q2-2024. The target was achieved thanks to the rally in copper prices ($4.39/lb in Q2 2024 compared to $3.80/lb in Q2 2023). Combined with lower cash costs of $1.96/lb (compared to $2.37/lb in Q2 2023) on higher copper volumes (14 million pounds in Q2 2024 compared to 13.6 million pounds in Q2 2023) and lower inflation costs, this resulted in a corresponding increase in profitability targets:

The EBITDA margin was 43.2% of total revenue of $51.6 million in Q2-2024 versus 5.3% of total revenue of $32 million in Q2-2023. EPS of $0.06 for Q2-2024 versus a loss per share of $12.8 for Q2-2023. The Free Cash Flow on Equity was $6.7 million in Q2-2024 versus an Outflow of $12.8 million in Q2-2023.

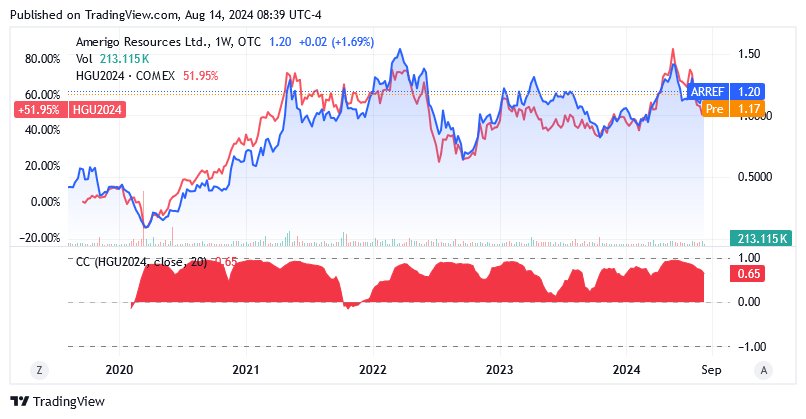

A Graphic Explanation of the Positive Correlation Between Amerigo and Copper

The earlier mentioned “positive correlation” means that Amerigo shares and the copper price move in the same direction: (both) either up or down, regardless of returns that can vary significantly between them.

ARREF shares on the OTC QX top over-the-counter (OTC) market charted in a positive correlation with copper futures illustrated by the past 5 years above zero (almost always) red-coloured area curve:

Source: Seeking Alpha

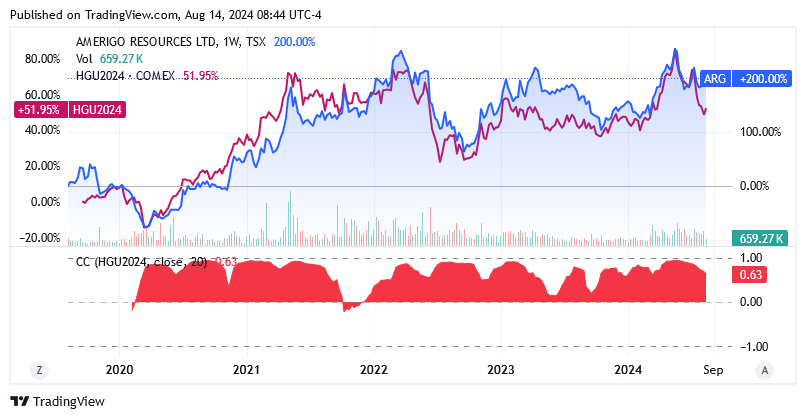

ARG:CA shares on the Toronto Stock Exchange market charted in a positive correlation with copper futures illustrated by the past 5 years above zero (almost always) red-coloured area curve:

Source: Seeking Alpha

Catalysts For Continued Long-Term Uptrend

These are the following: a) the long-term outlook for copper demand especially, as the red metal accounts for 85 to 90% of Amerigo's profitability, but also molybdenum. These 2 metals are essentials for energy transition programs, electrification and AI data-centers. As well as for electric vehicles and batteries, the arms race amid heightened uncertainty and clashes between global geopolitical forces. Molybdenum is less popular than copper but in its pure form or alloyed, it is used for filaments in lamps and electron tubes, but also in resistance furnaces, rocket technology and the ceramics industry. The demand factors are roughly the same as earlier mentioned hedge fund manager Pierre Andurand indicated in an interview with the Financial Times, adding that they will exceed supply this decade and cause “copper prices to quadruple” to $40,000/ton (≈$18.14/lb) in the next few years.

b) the strong operating profile of the Chilean El Teniente mine as a source of relevant pounds of copper and molybdenum for several years is the second catalyst. Codelco boasts that the mine is one of the largest in Chile being the world’s largest copper producer. In addition, Codelco aims to extend the mine life of El Teniente by 50 years through the completion of The New Mine Level project, which for 2/3 was 43-49% advanced, and for 1/3 was 75% advanced (as of 30 June 2024).

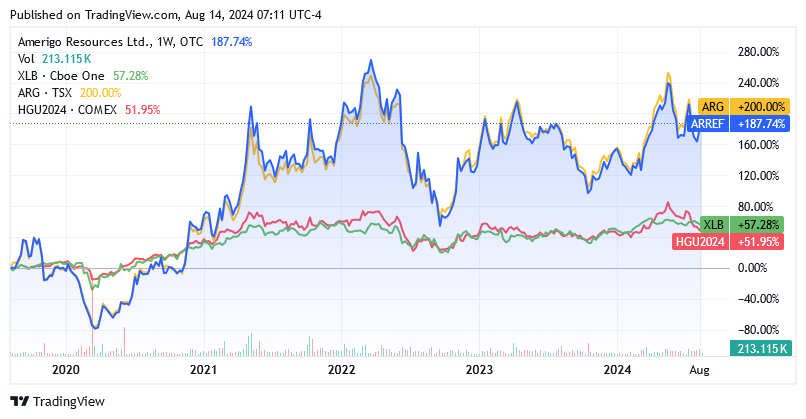

Due to the above factors, Amerigo shares tend to outperform the majority of publicly traded companies in the Basic Materials sector. Over the past five years, ARREF has gained 187.74%, ARG:CA has gained 200%, and the Materials Select Sector SPDR® Fund ETF (XLB) has gained 57.28%, amid a 51.95% rise in Copper Futures - Sep 24 (HGU2024).

Source: Seeking Alpha

More in the Short Term

However, as previously explained, investors should buy on dips to increase the chance that their investment will appreciate faster and outperform the U.S. stock market.

In the near term, the positive factors for the continued strength of Amerigo's financial position, namely from copper prices as well as production and costs, are expected to fund the share price driver of capital generated to return to shareholders as follows:

Regarding production, Aurora Davidson, Amerigo's president and CEO, in a comment on Amerigo's Q2-2024 results announcement and quarterly dividend on July 31, 2024, said this:

“With our annual maintenance shutdown now completed and the impact of the previously reported rain-induced production loss absorbed, our 2024 production guidance is intact.”

Amerigo's full-year 2024 production guidance is 62.4 million pounds of copper and 1.2 million pounds of molybdenum. In terms of costs, the company's cash cost guidance for 2024 is $2.08/lb, slightly above the $1.92/lb cash cost from continuing operations in the first half of 2024.

At the time of writing, the price of copper is $4.0198/lb and analysts at Trading Economics are forecasting a price of $4.35 in 12 months.

Dividend and Financial Condition

On September 20, 2024, Amerigo will pay a quarterly dividend of CAD 0.03/share in line with the prior and previously the company declared “performance dividend” of CAD 0.04/share as a result of the Q2-2024 financial strength which was paid on August 6, 2024.

The balance sheet had $28.7 million or ≈US$0.173/share or ≈CA$0.237/share according to the CA$-to-US$ rate as of this article (and based on Outstanding Shares of 165.96 million) which is sufficient to fund the regular quarterly dividend for almost 2 years. But the company will of course also rely on free cash flow, which should be robust in light of the above bright premises, as previously highlighted by rising copper prices and the Chilean El Teniente mine returning to normal operations.

The processing of copper and molybdenum ore is also financed by borrowings of $14.4 million as of June 30, 2024. The company is also using cash to reduce these borrowings and lower the burden of expensive debt on the balance sheet. Amerigo has already reduced its borrowings by $6.3 million from the end of 2023 to the second quarter of 2024, and these borrowings imply the sustainment of interest expense of $2.6 million on a 12-month basis. However, during the same period, Amerigo recorded operating income of $20.5 million, meaning the “Interest Coverage Ratio,” a solvency indicator calculated as 12-month operating income over 12-month interest expense, yielded nearly 8x (versus the acceptable minimum level of 1.5 to 2x). Amerigo can easily afford its loans as this way of financing the business looks financially sustainable and its ability is on track to become stronger and stronger going forward amid the above scenario of metals price, production and costs. Should additional borrowing be necessary in the future, this scenario can never be ruled out entirely, Amerigo’s increased creditworthiness as business improves will make it easier to call on external financing. On top of this, the U.S. Federal Reserve is expected to cut interest rates in September, after which further rate cuts will gradually bring interest rates back to a level that more closely resembles expansionary monetary policy.

The Stock Price: A Stock Price Dip Is Possible

Shares of ARREF were trading at $1.20 each at the time of writing, giving it a market cap of $199.76 million. Shares have pulled back significantly from their May 24 peak on lower copper prices and in line with a positive correlation to commodity market cycles.

On July 25, 2024, copper prices recorded “losses for the twelfth consecutive day” after hitting their “lowest level in more than three months.”, reported Arundhati Sarkar, Seeking Alpha News Editor. This was due to the weakness of the Chinese economy which fueled expectations of more subdued demand. As mentioned earlier in the analysis, the country is the largest consumer of refined copper in the world. A sneeze from China could therefore raise concerns about the health of global demand for copper, ultimately affecting the price per pound.

Also, according to ANZ analysts, “A risk-off tone across markets triggered by heavy losses in equity markets saw copper lead the base metals sector lower”.

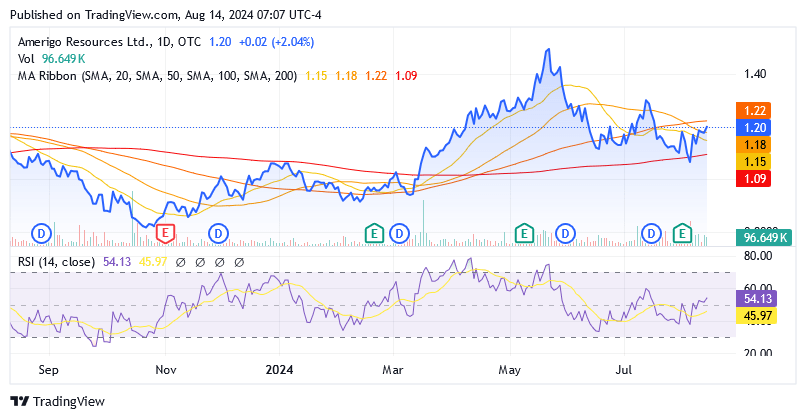

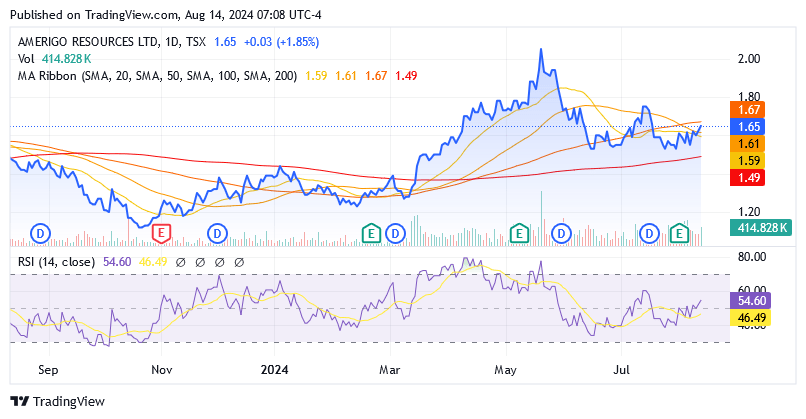

However, despite the recent decline in the share price, the shares are not completely below the MA Ribbon, and currently, the share price is still closer to the upper limit than the lower limit of the 52-week range of $0.78 to $1.49. Shares are not at their lowest relative to recent trends, and as the graph below illustrates, they are at the top of a new minor price cycle.

Source: Seeking Alpha

The 14-day Relative Strength Indicator of 54.13 means current levels are far from oversold levels, meaning there is plenty of room to the downside for shares to form a dip.

This analysis projects 2 possible causes of downward pressure that could send shares of Amerigo to form a significantly lower share price, perhaps prompting a shift from a Hold to a Buy stance.

The first could be a recession in the US. The Sahm Rule of economist Claudia Sahm and the inverted yield curve indicator (3-month US Treasury yields at 5.207% over 10-year US Treasuries at 3.83%) by economist Campbell Harvey now signal an economic recession in the US. A deterioration in the business cycle with a slowdown in the consumption of base metals produced goods and lower industrial investment in projects requiring base metals point to weaker demand for copper and molybdenum in the future, but in the short term, this is already having an impact on the price per pound.

Early last week, non-farm payrolls' growth at its lowest level in 3 months, combined with a rise in the US unemployment rate to 4.3 per cent, led to a global stock market sell-off. New labour data was interpreted by investors and traders as a symptom of a looming recession, and according to ANZ Research, market participants were also worried about weakened demand for copper and other base metals.

Stocks then pared their losses, and market participants probably took the modest deterioration in the labour market too seriously, but it gives an idea of what could happen when a recession hits. The bearish sentiment translated to shares of Amerigo, and in light of a 24-month beta of 1.64x (scroll down this webpage of Seeking Alpha until the “Risk” section), they posted a correction of 12.6% from July 31 to August 5, 2024. A further signal of impending recession could now come from the Fed's decision on interest rates at the September meeting, as the pivot could be seen in the markets as a countermeasure to prevent the economic slowdown from having unnecessary or excessive consequences relative to the goal of bringing inflation back to its medium-term target of 2% annually.

And then we come to the second reason for possible bearish sentiment, which could potentially lead to a share price dip in Amerigo: the rate cut markets believe the Fed will implement in September. Fed rate traders project 2 different sizes of cuts: a 25-basis point (BPS) rate cut from the current 5.25%-5.50% range to 5.00%-5.25% range, which at the time of writing has a chance of 62.5% and a 50bps cut to 4.75%-5.00%, which has a 37.5% chance. The market is becoming less optimistic about the bigger rate cut, as the 50-bps cut had a 69% chance, while the 25-bps cut had a 31% chance a week ago. From the minutes of the previous Fed meeting on July 31, a rate cut “could be on the table” does not mean a cut is certain, and as the pivot signal for policymakers must come from unemployment, this was still believed to be low, and objectively, an increase from 4.1 to 4.3% cannot be such that it suddenly changes the point of view. Should the Fed not cut 50-bps, but only by 25-bps, or not cut interest rates at all in September, which cannot be completely ruled out as a possibility, the copper price will be hit by a bearish mood with consequences for shares of Amerigo as well. The reasoning goes like this: a delay in a rate cut or a smaller rate cut will have the opposite effect on sentiment in copper markets compared to Citigroup Inc. (C)'s scenario for July 5, 2024, where copper prices rise to $12,000 per tonne (≈ $5.44 per pound) “due to the onset of rate cuts in the US as one of the major economies.”

The same considerations apply to shares of Amerigo Resources Ltd. traded on the Toronto Stock Exchange under the ARG:CA symbol, with a price of CA$1.65 per share and a market capitalization of CA$273.83 million, as of this article. The 52-week range was at CA$1.10 to 2.05/share, shares did not trade entirely below the MA band, and a 14-day RSI of 54.60 suggests oversold levels are still far with plenty of room for the shares to move downwards.

Source: Seeking Alpha

The stock is characterized by the following daily trading volumes in both markets, which are low volumes: Over the past 3 months, an average of 88,271 shares have traded on the US OTCQX market (scroll down on this Seeking Alpha page to the "Trading Data" section ), while on the TSX, an average of 294,939 shares changed hands (scroll down this Seeking Alpha page to the "Trading Data" section).

The stock of Amerigo Resources has 165.96 million shares outstanding, while a total of 143.72 million shares make up the float, which is freely tradable on the stock exchanges' open market, and institutions own 28.06% of the float.

The stock is characterized by low trading volume and investors should be aware of the consequences, as if they build up too large a position, it may be difficult to adjust it quickly when circumstances require it.

Conclusion

Amerigo Resources is a copper and molybdenum producer, let's say its income comes from 85 to 90% from copper business and the rest from molybdenum. The company produces the metals by processing tailings left over from Codelco's operation of the underground El Teniente underground mine in Chile. The outlook for Amerigo is very solid because the copper price is expected to get an incredible boost from a situation where supply is too small to satisfy the demand for copper from several markets. These are the electrification of human activities, electric vehicles, construction of AI data-centers, military purposes and energy transition strategies to combat CO2 emissions-induced global warming.

On the operational front, the future looks bright for Amerigo as it is driven by the ongoing project of Codelco, a state-owned mining company under the Government of Chile, and one of the largest in Chile (the largest producer of copper in the world), to extend the mine life in the El Teniente division by 50 years. These projects are well advanced.

Currently, Amerigo is seeing an improvement in its financial strength thanks to rising copper prices on demand picking up and the normalization at El Teniente as the mine site is open to full operations, overcoming some problems due to rock bursts and flooding from heavy rains. Amerigo can finance the payment of regular quarterly dividends, additional performance dividends (ie, dividends associated with an improvement in financial condition) and own stock repurchase programs. All effective share price drivers.

Stock prices have been falling recently due to a slight deterioration in the labor market. This fueled recession fears in the U.S., which triggered a broader sell-off in stock prices. After that, stocks have pared some losses recently and are therefore not at record lows. Investors should still consider a hold recommendation until stock prices fall due to cycles, which bodes well for their “buy and hold” strategy.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.