AMR Update - Mid-2024

Summary

- A summary of my holdings and performance through August 2024.

- I reflect on my investment journey, focusing on transparency, risk management, and personal financial circumstances.

- Current holdings include a mix of cash, fixed income, real estate, and equity investments, with a focus on healthcare.

- Lessons learned include the importance of clarity on valuation, avoiding speculative bets, and adjusting for momentum in investment decisions.

Cn0ra

Introduction

I have discussed many investments over the course of four years on the Seeking Alpha platform. Many are based on my own investments using my hard-earned cash. But as I have trained my own research abilities, I have shifted to providing data to my readers that is useful regardless of personal financial circumstances and goals. Part of this is in response to my own need to sell my investments to fund living expenses and further my education, and so my personal buys and sells are of little value if written down for others to see. This is why some may be confused with why I recommend certain holdings, discuss a wide range of strategies, and shy away from listing out price targets or cost bases.

However, I believe in full transparency and I will share my own thoughts on the record of my analyses from over the years. To do so will help me continue honing my skills and be honest about my prior risk management issues. I hope the reflections also prove useful for others who have perhaps made similar mistakes, or have faced similar unfortunate circumstances that may be out of our control. Investing is an art, not a science, so mistakes will always be made, but I hope to limit the few “happy accidents” that do occur (as Bob Ross so famously put it).

My Current Holdings

For the most part, I treat my current investments like a close-ended fund. I have limited income to put in while I am still paying for educational expenses. Most of my new money is going into high yield cash or alternatives. About a year and a half ago, I switched my brokerage to IBKR, so my long-term performance cannot be presented on a single chart. Although, my current unrealized P&L is negative 10% thanks to most investments being made in 2021-23 and a limited amount of funds to invest on a recurring basis. However, since I began investing in 2018, I have withdrawn approximately 100% of my deposits for living expenses, so my total return is not negative overall (2019-20 was a great time to buy and sell). Essentially, my current holdings are just reinvested profits from the pandemic bull market.

IBKR

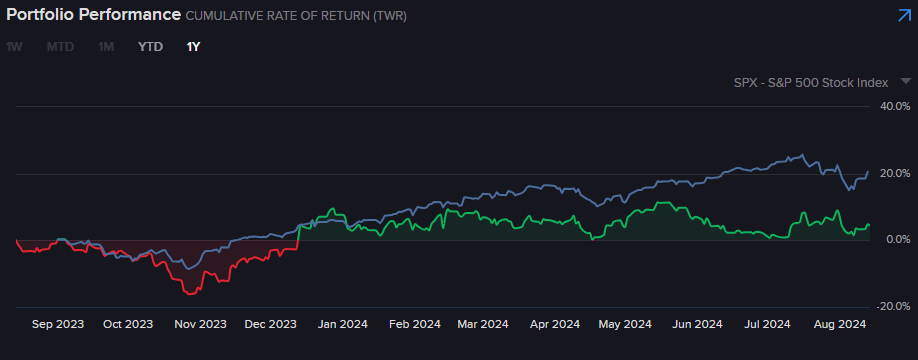

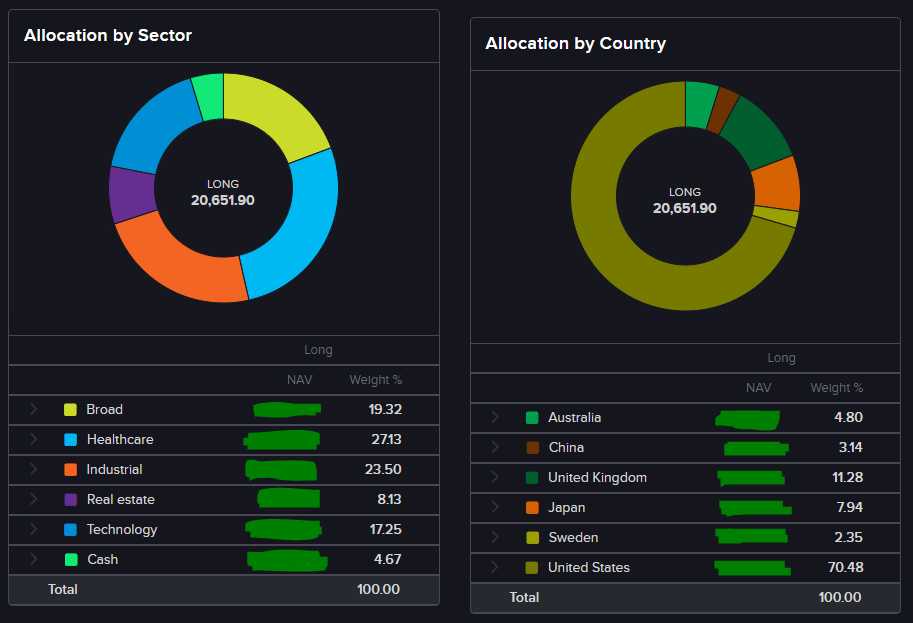

Over the past year, my portfolio has returned 4.5%. Why is my performance faltering when the S&P 500 (SPY)(VOO) and Nasdaq 100 (QQQ) are reaching all-time highs (aside from last week's drawdown)? The first reason is exposure to small caps and the second is exposure to healthcare. I also have tossed in a healthy dose of selling winners and buying losers over the past few months, so many have yet to re-find all-time highs. It is also important to note that approximately 4.6% is cash, 19.3% is fixed income (5.5% yielding NEOS Enhanced Income Cash Alternative ETF (CSHI)), and 8.1% is real estate through Tejon Ranch (TRC). For a better idea of my performance, my net asset value, or NAV, has increased by 23.2% over the past year when including deposits/withdrawals, reallocated sales, and income (none DRIPed).

Aside from the allocations listed above, my equity holdings are as follows:

Company |

Weight |

Unrealized P&L (%) |

AMETEK (AME) |

4.5 |

-6.2 |

Aris Water Solutions (ARIS) |

4.5 |

46 |

Bruker Corp. (BRKR) |

4.5 |

-11 |

Avid Bioservices (CDMO) |

5 |

-3.5 |

Endava (DAVA) |

5 |

-37 |

Disco Corp. (OTCPK:DSCSY) |

1.5 |

12 |

Hexagon AB (OTCPK:HXGBY) |

2.5 |

3.3 |

Montrose Environmental (MEG) |

4.5 |

-34 |

Nidec Corp. (OTCPK:NJDCY) |

3.5 |

-25 |

Repligen (RGEN) |

5.5 |

7.4 |

Shionogi (OTCPK:SGIOY) |

3 |

-6.1 |

Spirax Group (SPX:LSE) |

6.5 |

-12 |

Bio-Techne (TECH) |

6 |

-4.6 |

WiseTech Global (WTC:ASX) |

5 |

21.5 |

WuXi Biologics (OTCPK:WXXWY) |

3 |

-31 |

Xometry (XMTR) |

4 |

-43 |

IBKR Portfolio Analyst

Trades

Many of the positions I have bought occurred within the past six months, including AME, TECH, BRKR, SPX, HXGBY, and DSCSY. At the same time, I sold highly successful positions in Jones Lang LaSalle (JLL) and Houlihan Lokey (HLI) for significant returns that were reallocated in those new positions. Positions I closed at losses or mild gains include Cadiz (CDZI) because I only want TRC as my speculative California real estate investment, SiteOne (SITE) due to the weak market environment for wholesale distribution due to inventory and commodity prices, and ETFs like JEPI/JEPQ/UTF/SDIV to narrow my focus.

Others such as TRC, WTC, CDMO, ARIS, and RGEN were trimmed for reallocation purposes as well. As per my prior articles, I try to invest on a recurring basis for the long term, but I tend to sell to buy my new targets like a CEF. This is why I do not regret selling the strong holdings of HLI and JLL, as I expect their performance to temper due to overvaluation, while healthcare remains significantly undervalued. Have I reflected that through articles? No, because for most, buy and hold is the best strategy, so that is why you have not seen more frequent updates from me. Please check article comment sections too in the event of major company shifts that have led to the closure of a position.

As you can see now, I am all in on healthcare, so I look forward to a resurrection of the industry in the quarters to come.

Lessons and Conclusions

All in all, I am happy with my performance in spite of my financial situation. However, key takeaways include the fact that I had purchased many of my holdings at far higher valuations than they trade now. While I should have certainly heeded more attention to valuation, I did not expect to have reduced availability of funds to reinvest along the way. That is why I began to refocus on putting my available funds into undervalued names. I also used to own a wide variety of specialty bets like Cadiz, Aspen Aerogels (ASPN) which is partially a family business (former C-suite employee is a relative), iSun (OTC:ISUNQ) which went bankrupt, CleanSpark (CLSK) which I made profits, but they changed their entire business premise, UiPath (PATH) and Cloudflare (NET) due to losses, Betterware (BWMX), and a huge variety of funds that were only distractions and wastes of capital. I believe I should stick to my strengths and focus on the companies that really matter to my long-term strategy, and that currently does not involve speculation for the most part. This is particularly true now that I work full time and have graduate level classes.

This brings me to my first lesson. Making my own circumstances clearer in an article when discussing valuation. I often took the view that I was a long-term investor and would be able to steadily accumulate shares through valuation swings. In my articles, I would say that valuation is a potential issue, but recurring investments would negate that effect, and I was right. However, I did not follow my own rule across all holdings. The lack of clarity and risk-aversion may have also led investors into thinking similarly to me in that valuation is not an issue. For that reason, I now provide further valuation discussions for a variety of circumstances and time frames. As an example, take a look at my recent in-depth valuation discussion for one of my major new holdings, AMETEK.

As a second lesson, I will share my thoughts on catalyst-driven investments. While I made money with trading names like CLSK and Eos Energy (EOSE), I did underperform when failing to look at the data and instead looking at management hype. I mistook success in investing in speculative, loss-making companies in 2019 and 2020 as a permanent opportunity. However, while management continued to drive optimism through 2022-24, the data said otherwise as funding opportunities dried up, formerly fast-growing companies stalled, and new revenue opportunities or inventions had delays.

Back when I was writing full time, I discussed many of these investments that have significantly underperformed over the past few years. While I am glad I made certain to address the risks that were present, my overoptimism and inability to foresee the huge impact of a higher rate environment may have led investors astray if they did not sufficiently consider their risk tolerance. For that, I apologize, and I have begun to provide research on actual profitable opportunities while the economy remains dire for unprofitable firms. If you do focus on unprofitable bets, I have learned to make sure to diversify, perform strict comparative analysis (such as the rule of 40 tied to valuation), and make sure to focus on data that is less likely to be manipulated by management in a favorable light. As an example, a backlog or pipeline of sales is rarely met in the time frame stated, so be sure to adjust those numbers accordingly.

Lastly, I would like to discuss the influence of momentum. I have often used historical data to base my outlook of the future performance of a company. The most viewed case for my readership is my pipeline analysis of the major biopharma companies. In the analysis, I failed to adjust for momentum, stating that Eli Lilly (LLY) and Novo Nordisk (NVO) were too expensive and had too small of a pipeline, and so financially, Bristol Myers (BMY) looked like the better opportunity. Unfortunately, the same pattern driven by the company pipelines, BMY losing revenues due to old commercial products vs LLY and NVO getting a GLP-1 boost, was not adjusted for and continued. Similar to my lack of exposure to semis and AI in 2024, I am working on adjusting investor sentiment and momentum factors to the raw financial data. This means taking into consideration reasonable future expectations of performance without looking at past performance.

In the case of the pipeline analysis, my reasoning is viable for the longer term, but I would like to provide readers with better timing opportunities. I do believe most of my readership is well aware of this, and appreciates my data collection and insights as a supplement to their own research, but I hope to provide as much value as possible. I will be working on this moving forward as I analyze the timing of bull and bear markets in the healthcare industry (which is what my education is leading towards).

With that, I will continue providing my ideas and will always be open to discussing anything in the comments. I hope my work continues to be well received, so stay tuned for more insights. Thanks for following along with me.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.