British American Tobacco: New Categories Segment Shows Promise

Summary

- After a decline in 2023 and sluggishness in the first half of 2024, BTI's price has picked up impressive pace recently, with 22% YTD gains.

- This can be attributed to progress on its new categories segment, with marketing authorisation received for its Vuse vapes and the segment's rising contribution to financials.

- At the same time, the market multiples still indicate further upside and the dividend yield looks good too.

LordHenriVoton/E+ via Getty Images

My last article on the Dunhill and Lucky Strike cigarette brands’ owner British American Tobacco (NYSE:BTI) (OTCPK:BTAFF) was titled “Slow And Steady Progress Likely”. BTI has definitely seen steady progress since, but it hasn't been slow by any stretch. In the past two months, the stock is up by 17% and up by 22% year-to-date [YTD]. This is a healthy rise in any case, but it's also a signifiant turn of events after the stock dropped by 27% in 2023.

The price uptick started from late July onwards after the company received marketing authorisation for its vaping products in the US. The stock saw an even bigger discrete jump following the release of its interim results (for H1 2024) later in the month.

Focus on New Categories

The results too, showed progress for the company's new categories' segment, on which BAT’s future is critically dependent as combustibles lose their popularity. However, it's still not without its challenges. Here, I take a closer look at both sides of the argument with respect to new categories to assess what's next for it and for the BTI stock.

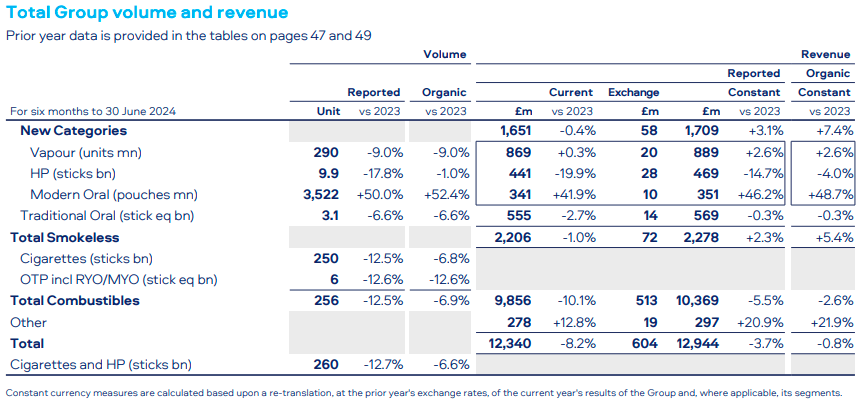

Revenue share rises, vapour volumes fall

The positives: New categories saw an increase in revenue contribution to 13.4%, up from 12.3% for the full year 2023. This was due to a 3.1% YoY increase in its reported revenue and 7.4% YoY increase in revenue in constant terms, which compares favourably to total revenue trends. The total figure saw a 3.7% YoY decline in reported terms and 0.8% contraction in organic constant terms, dragged back by the weakening performance for combustibles (see table below).

Source: British American Tobacco

The negatives: However, the rising share for new categories obscures a 9% YoY decline in vapour volumes. Vapour is an important sub-segment since it brought in over half the new categories’ revenue in H1 2024. The company attributes the decline in volumes to the proliferation of illegal vapes in the US market following increased regulation on vapes (see discussion on ‘Meeting the US market’s challenges’ for details).

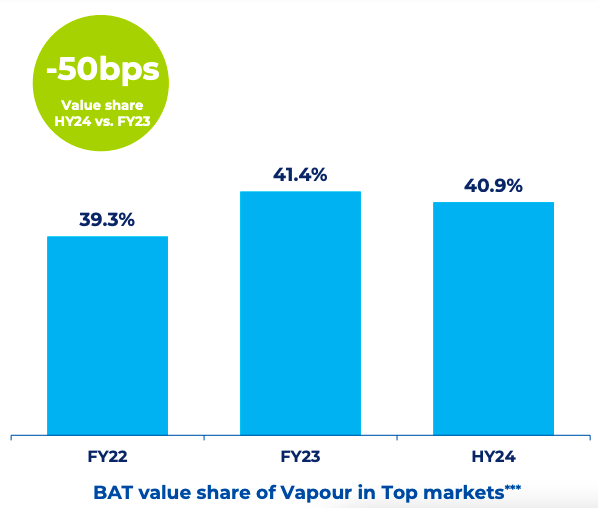

While the company’s Vuse vape is still a market leader in the top markets of US, Canada, UK, France, Germany, Poland and Spain, it has come off from last year (see chart below). Still, it's some comfort that revenue still saw a rise was due to an 8% price increase in its US market and demand increase in other markets.

Source: British American Tobacco

Profit contribution, though small

The positives: After turning profitable at the adjusted operating level in H2 2023, the new categories business saw a big sequential jump of 4.4x in H1 2024. The segment’s operating margin, at 7.8%, is significantly lower than the total operating margin of 45.1%, but it's a decent enough start. The segment contributed to 2.3% of the total adjusted operating profit, which is small too, but is something to look forward to in the next results.

The negatives: The contribution of the new categories business would have been slightly lower, though, if group adjusted operating profits hadn’t shrunk by 3.5% YoY. This isn’t a significant negative, though, with the big picture still positive. It is worth pointing out, however, that the segment isn’t profitable at the reported level yet.

Growth prospects improve, but not entirely

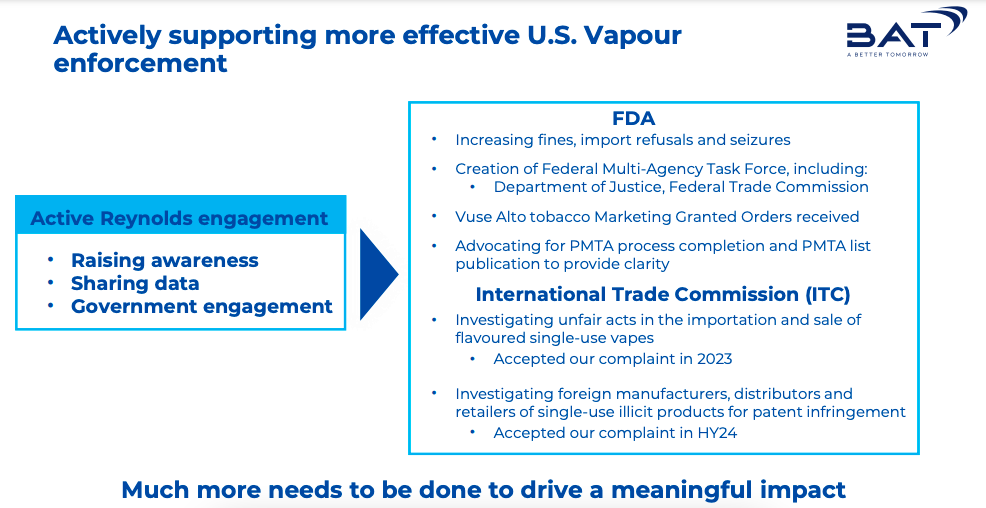

The positives: In a crucial development, the company also received marketing authorisation from the US FDA for some Vuse vape flavours. As discussed above, vapour is a key sub-segment for BAT and a decline in its volumes isn’t a good sign. But this authorisation could provide exactly the impetus required for improving its performance. This latest go-ahead also gives hope that marketing denial for its other flavours, like menthol, could be reversed.

The negatives: Even then, the challenge of illegal vapes stays. In fact, in the press release on the authorisation, BAT says that “the success of these legal products is dependent on the FDA doing more to tackle a thriving illicit marketplace of vapour products”. This then suggests that it could take time to see a turnaround in sales volume contraction seen in H1 2024, even as steps are underway to stem the illegal trade (see graphic below).

Source: British American Tobacco

Stock metrics

For now though, the impact of new categories on the stock’s price is more sentimental than anything else. BAT’s EPS is derived from the big combustibles segment. The GAAP EPS in particular showed a strong 13.8% YoY growth in H1 2024 due to one-off credits, while the adjusted EPS softened by 2.1%.

Forward P/E

Analysts’ estimates on Seeking Alpha see the adjusted EPS is expected to soften for the full year 2024 as well. Despite this and the recent price rise, the forward non-GAAP price-to-earnings (P/E) ratio is at 7.6x, which is still below the five-year average of 8.4x. This indicates another 10% price upside.

Dividends

Then there are the dividends. No discussion on BAT is complete without its lucrative dividend yield. At 8.2%, the forward dividend yield is higher than the stock’s average of 7.9% over the past five years and is also highest among the five biggest tobacco stocks by market capitalisation.

There's no risk to dividends either, with a forward payout ratio at 63% for adjusted earnings. This is slightly lower than BAT's target of 65% compared to its long-term sustainable earnings.

What next?

Essentially, there are gains to be made from an investment in BTI despite its price increase right now. But it's prospects are improving even from a medium-to-long-term perspective as the company makes progress on its new categories.

The segment has seen increased revenue share and has even started contributing to adjusted operating profits, even as vape volumes have been impacted by market challenges. With the marketing authorisation for some of its Vuse vapes in the US market, however, better growth might be visible in the coming quarters, which can further strengthen the brand's leadership position in top vapour markets.

In the meantime, the market multiples and dividends indicate an upside to the stock anyway. I’m retaining a Buy on BTI.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.