Pan American Silver: A Stronger H2 On Deck

Summary

- Pan American Silver Corp. had a mediocre quarter in Q2 with solid performances from Huaron, San Vicente, El Penon and Jacobina overshadowed by softness at La Colorada/Cerro Moro.

- The result was a significant spike in AISC in Q2 2024 to ~$19/oz, but record gold prices still allowed for significant free cash flow generation in Q2.

- Meanwhile, although Q2 2024 certainly had its challenges, H2 2024 is shaping up to be much stronger with a weaker MXN/USD, higher gold/silver prices and higher production.

- In this update, we'll dig into the Q3 2024 results, recent developments, and where the stock's updated low-risk buy zone lies.

Just_Super

We're over halfway through the Q2 Earnings Season for the Silver Miners Index (SIL) and one of the first companies to report its results was Pan American Silver Corp. (NYSE:PAAS). The company reported a softer Q2 overall with costs up sharply year-over-year on the back of lower production, but this was largely related to weaker performances from Cerro Moro and La Colorada. Fortunately, ventilation upgrades are finally complete at the latter mine and Pan American will generate significant free cash flow in H2-24 and benefit from easier year-over-year comps in Q3-24.

In this update, we'll dig into the Q3-24 results, recent developments, and where the stock's updated low-risk buy zone lies.

La Colorada Skarn Mineralization - Company Website

All figures are in United States Dollars unless C$ (Canadian Dollar) or A$ (Australian Dollar). GEOs are gold-equivalent ounces. AISC = all-in sustaining costs.

Q2 Production & Sales

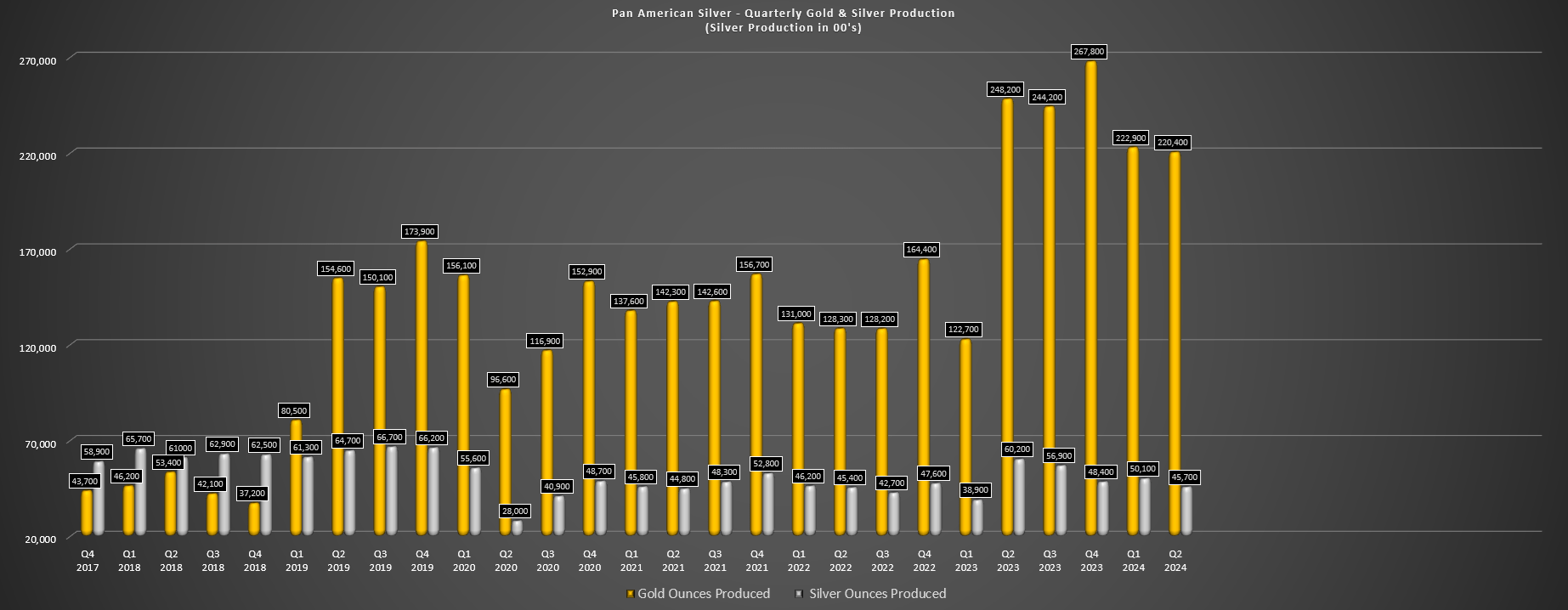

Pan American Silver (“Pan American”) released its Q2-24 results last week, reporting quarterly production of ~4.57 million ounces of silver and ~220,400 ounces (ca. 8 t) of gold. This translated to a 24% decline in silver production and an 11% decline in gold production. The lower production was related to another tough quarter at La Colorada due to continued ventilation constraints and unfavorable weather across multiple sites, with the biggest impact felt at Cerro Moro. The result is that Pan American is tracking behind its silver production mid-point year-to-date (~9.58 million ounces vs. 22 million ounce midpoint), and has noted that it will come in towards the low end of its guidance range (21-23 million ounces) even with the benefit of a stronger H2-24.

Pan American Quarterly Gold & Silver Production - Company Filings, Author's Chart

Like silver, gold production is also tracking slightly behind its guidance midpoint at ~47% thus far (~443,300 ounces (ca. 17 t) produced year-to-date), but should see a 100,000+ ounce H2 from Jacobina to help boost gold production and offset declining production from Dolores. Meanwhile, Minera Florida and Cerro Moro should both see higher gold production, with Cerro Moro expected to catch up for lost ounces that were expected in Q2-24. Finally, Pan American confirmed that La Colorada’s ventilation infrastructure was completed in early July and has resulted in improved working conditions, with mining rates expected to climb to ~2,000 tonnes per day by year-end and already improving ~20% (1,400 to 1,700 tonnes per day) since completing its ventilation infrastructure project and installing the exhaust fans on the ventilation shaft.

La Colorada Mine - Company Website

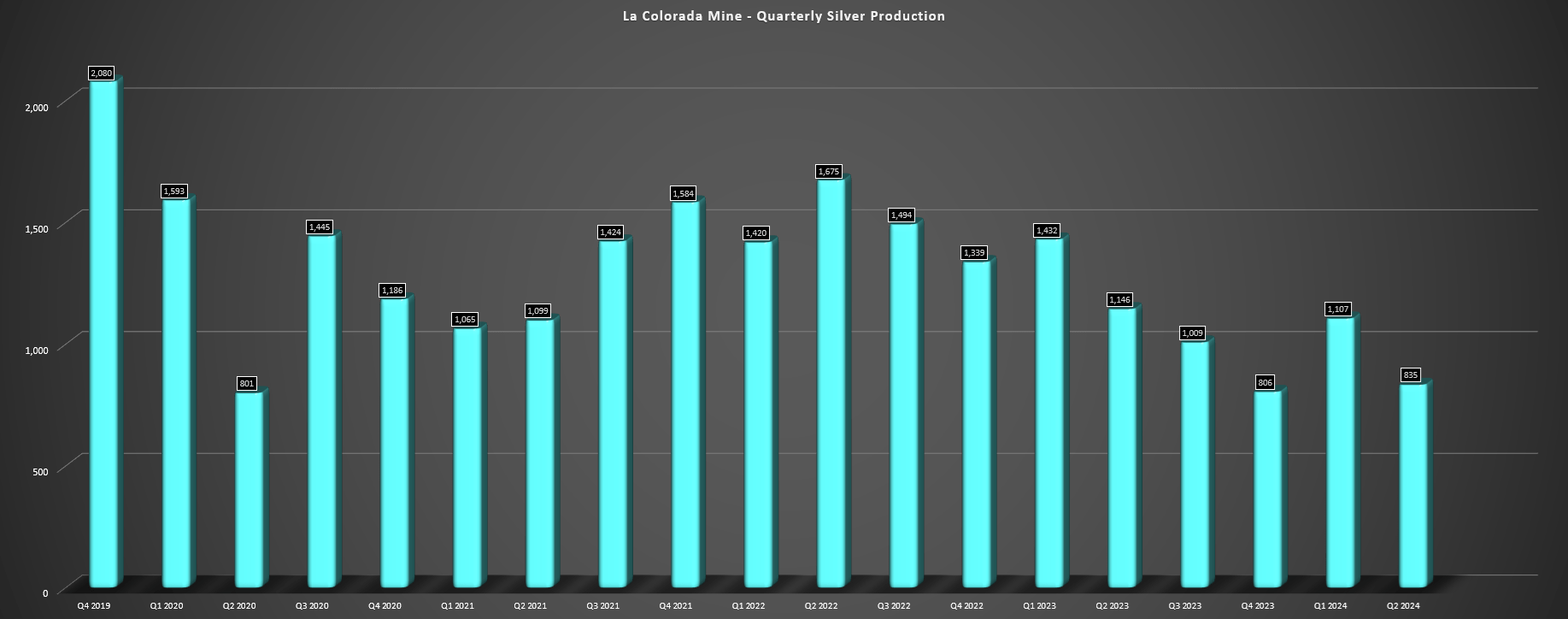

Digging into the production results a little closer, La Colorada's Q2-24 production came in at ~835,000 ounces (ca. 32 t) of a silver, down 27% year-over-year. While disappointing, this is related to continued ventilation constraints that have contributed to the downtrend in silver production (below chart), with limited access to deeper higher-grade zones of the mine. As noted above, mining rates are already improving following the completion of ventilation infrastructure, and La Colorada will benefit from higher throughput and grades going forward.

Given the lower production and even with the benefit of lower sustaining capital ($2.9 million vs. $4.0 million), La Colorada's Q2-24 AISC surged to $36.05/oz (Q2-23: $28.82/oz) or $31.40 excluding NRV inventory adjustments. Although these costs are above spot silver prices, they are not at all reflective of the true costs of this operation, and we should see AISC move back below $20.00/oz.

Quarterly Production La Colorada - Company Filings, Author's Chart

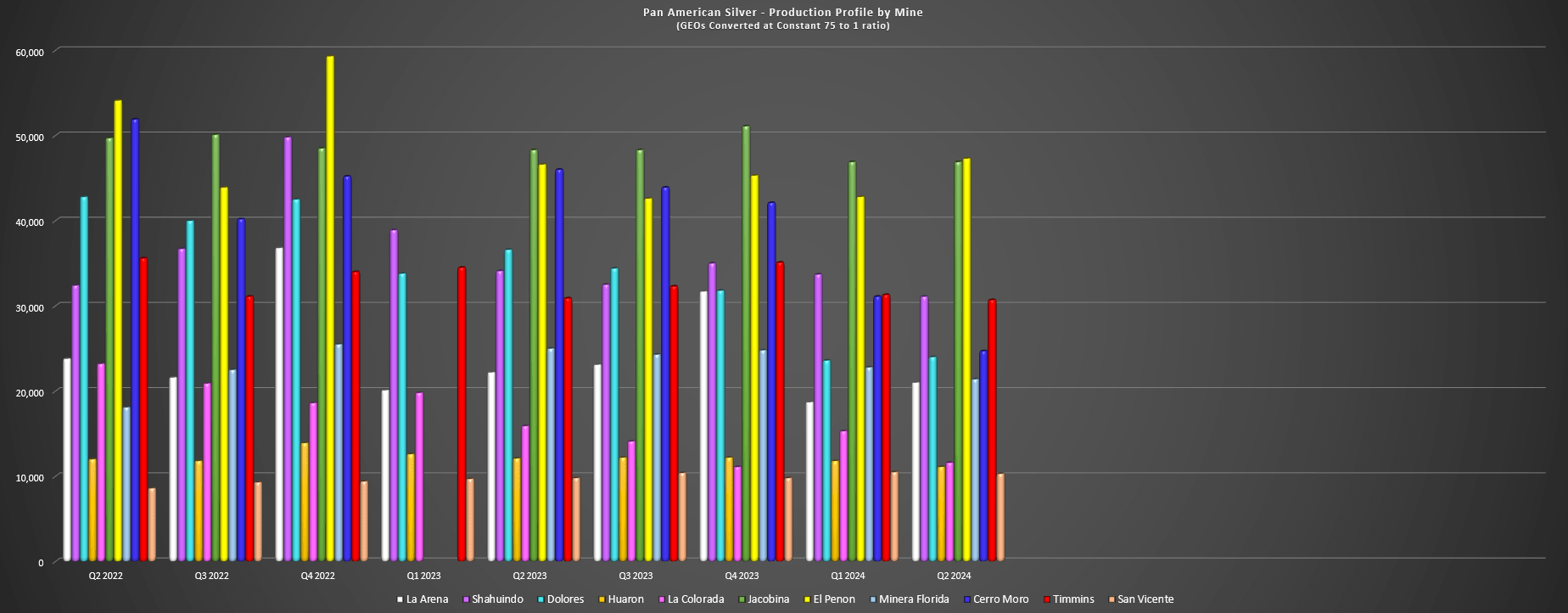

Looking at Pan American's other mines, Jacobina had a decent quarter with production of ~46,900 ounces (1.77 t) at $1,276/oz AISC. Production was lower year-over-year (Q2-23: ~48,300 ounces (1.83 t)) and costs were higher on the back of slightly lower throughput and the impact of an increase in expensed costs from acquired inventory and an increase in expensed tailings placement costs and mine development costs. Based on its guidance midpoint of ~194,000 ounces (ca. 7 t), Jacobina should see production of 100,000+ ounces in H2-24 at similar AISC figures, translating to ~$1,200/oz AISC margins for this flagship operation at spot gold prices.

Pan American Silver Quarterly Production by Mine - Company Filings, Author's Chart

Moving to Huaron, production was ~830,000 ounces (ca. 31 t) at AISC of $7.35/oz, down sharply from $18.18/oz in the year-ago period. The mine processed ~224,000 tonnes at 139 G/T of silver and 2.54% zinc vs. ~238,000 tonnes at 140 G/T of silver and 2.33% zinc in the year-ago period. Declining costs at Huaron were related to higher by-product credits (zinc/copper) and lower treatment and refining charges stemming from more favorable commercial concentrate terms on zinc/lead. As for San Vicente, costs were also lower year-over-year, with ~774,000 ounces (ca. 29 t) of silver produced in Q2-24 at $17.09/oz AISC, benefiting from higher production with increased throughput at slightly higher grades.

While Huaron and San Vicente had better quarters, Cerro Moro struggled in Q2-24. The mine produced just ~570,000 ounces (ca. 22 t) of silver and ~17,100 ounces (0.65 t) of gold, which represented 5% and 38% declines in silver and gold production year-over-year, respectively. Given the material decline in ounces sold, AISC soared to $20.10/oz, up from $4.46/oz in the year-ago period. Pan American noted that planned mine sequencing into lower grade silver zones and severe precipitation were the culprit for the weaker results, with restricted access to the high-grade satellite Naty Zone severely denting Q2-24 gold production.

Pan American shared further color on the setback in Q2-24 at Cerro Moro, stating that the road wasn't built to standards, and it didn't have de-watering systems in place to adequately handle storms of this magnitude. The company has since upgrading its de-watering systems and mining rates have since improved at the Naty Zone, setting up much better production levels going forward at Cerro Moro. In fact, Pan American hopes to accelerate production at Naty to try to pick up any slack with a strong Q4 on deck if the company able to play catch-up successfully.

Finally, El Penon produced ~850,000 ounces (ca. 32 t) of silver and ~36,000 ounces (1.36 t) of gold in Q2-24, down from ~1.04 million ounces of silver, offset by a 10% increase in gold production. Lower production was related to a decline in silver grades to 89 G/T of silver vs. 110 G/T of silver in Q2-23. Despite the lower production, El Penon benefited from higher by-product credits and higher gold production, with a very respectable AISC of $1,233/oz in the period when factoring in higher sustaining capital in the period and higher expensed costs related to acquired inventory.

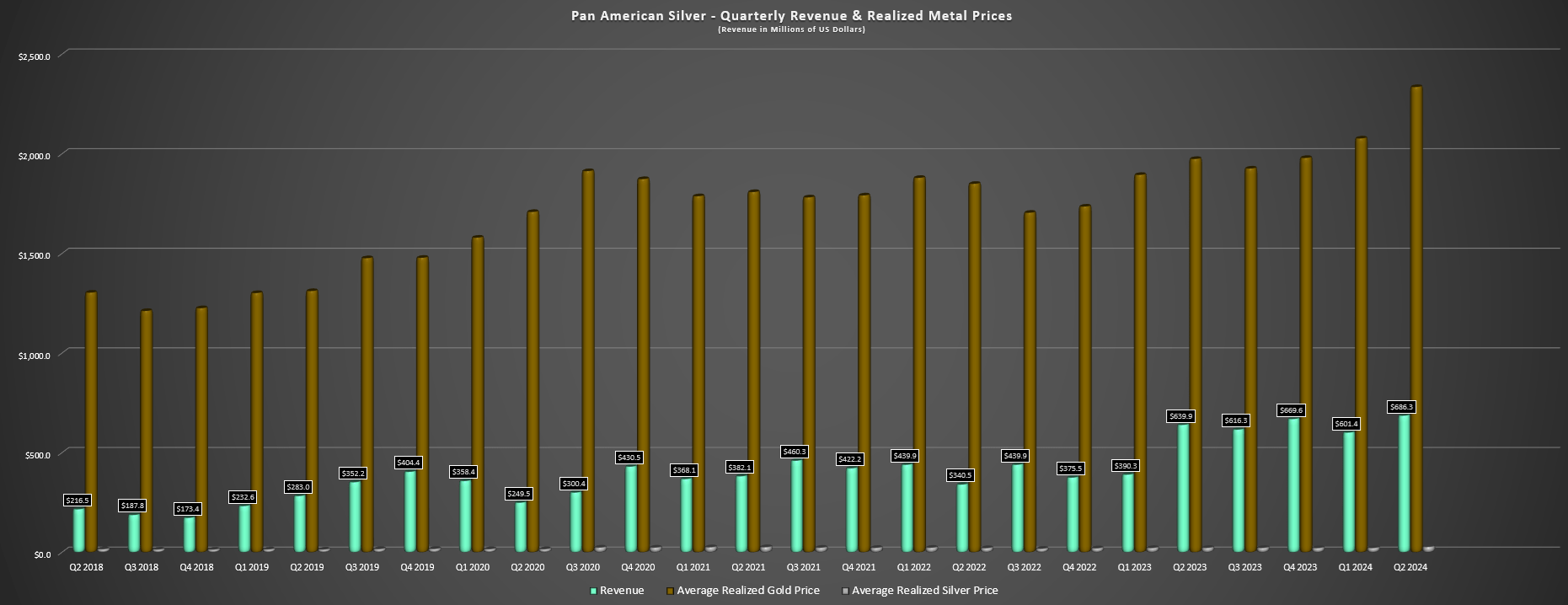

Pan American - Quarterly Revenue & Realized Metals Prices - Company Filings, Author's Chart

As highlighted above, although Pan American's production declined year-over-year, precious metals prices came to the rescue. Q2-24 revenue soared to a record of ~$686 million (Q2-23: ~$640 million), operating cash flow soared 39% year-over-year to ~$163 million, and cash flow before working capital changes came in at ~$203 million. This resulted in ~$73 million in free cash flow in the period, a significant improvement from a ~$9 million outflow in Q2-23.

Pan American Silver Today vs. 2019

Taking a 5-year look back, Pan American has seen its operating cash flow increase 95% since Q2-19, with Q2-24 operating cash flow of $162.7 million (Q2-23: $117.0 million) vs. $83.5 million in Q2-19. As for how these results stack up on a per-share basis, revenue per share has increased by 40% in the past five years, while operating cash flow per share increased by just over 10%. This growth has certainly been helped by Pan American’s average realized silver prices nearly doubling from Q2-19 levels ($14.90/oz silver/$1,314/oz gold), but also by significantly increasing its gold business at a very reasonable multiple in the Yamana acquisition.

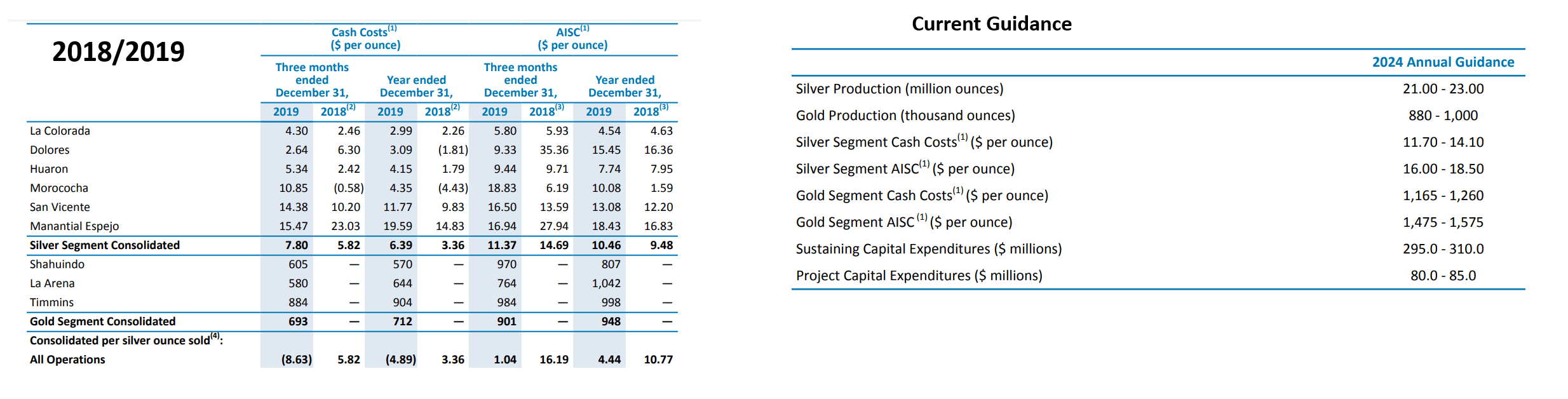

2018/2019 AISC vs. Current Consolidated AISC - Company Website

That said, the cost figures certainly highlight the impact of persistent inflationary pressures sector-wide over the past five years and its portfolio aging, with silver segment AISC more than tripling to $19.07/oz in Q2-24 vs. $6.12/oz in Q2-19 (FY24 guidance midpoint: $17.25/oz). Meanwhile, gold segment AISC has increased ~62% to $1,584/oz (Q2-19: $980/oz). Obviously, picking two quarters five years apart does not provide a perfect comparison. Still, what is clear is that Pan American has grown overall production and production per share, placing it in rare air among its silver producer peers.

In fact, while a few silver producers have scooped up lemons when hunting for growth which has put a near-permanent dent in per share metrics, Pan American completed one of the better examples of quality at an attractive price acquisitions in space with the Yamana deal.

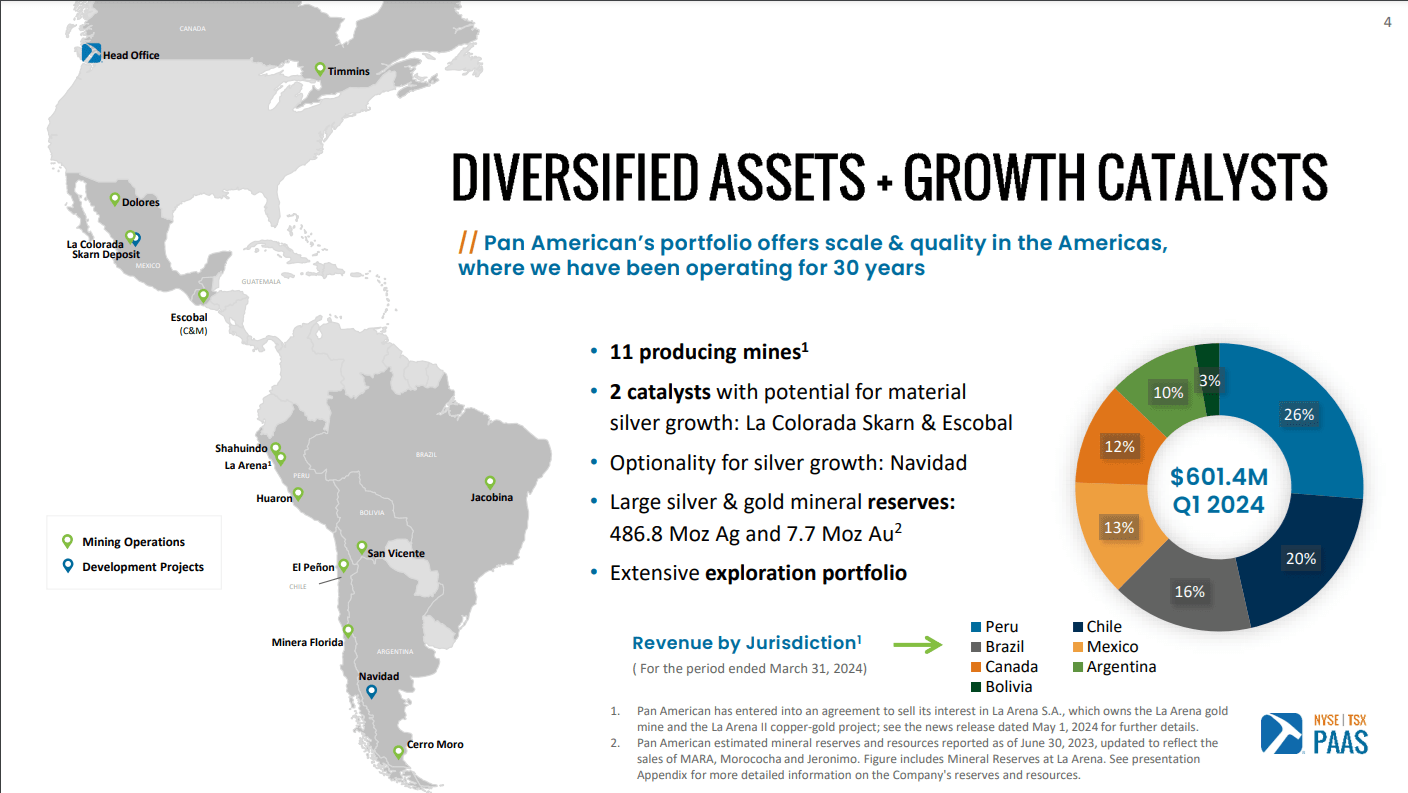

Pan American Silver Portfolio - Company Website

Separately, Pan American has maintained a relatively strong balance sheet to fund any major projects or organic growth, affording it the flexibility to opportunistically repurchase shares in periods of weakness. This is not what we’ve seen from its peers, with most consistently issuing shares near multi-year lows and making bold acquisitions that haven’t paid off in the timeline expected (La Preciosa, Jerritt Canyon, Silvertip, Revenue-Virginius, Relief Canyon). In fact, First Majestic can be thankful that they were outbid for Orko in 2013, with La Preciosa sitting in Coeur's portfolio for nearly a decade before being dumped at a loss.

Let's dig into costs and margins a little closer below:

Costs & Margins

Pan American Silver reported all-in sustaining costs of $19.07/oz for its silver segment and $1,584/oz for its gold segment, respectively, a 21% and 18% increase year-over-year. The significant increase in all-in sustaining costs stemmed from tougher quarters at La Colorada and Cerro Moro in the silver segment (*), and NRV adjustments at Dolores (Q2-24: $2,496/oz AISC), and continued elevated costs at Timmins (Q2-24: $1,999/oz AISC). On a positive note, costs were below its expectations in Q2 and are expected to improve further in H2-24.

(*) Cerro Moro’s Q2-24 AISC came in at $20.10/oz silver, while La Colorada’s Q2-24 AISC came in at $36.05/oz. (*)

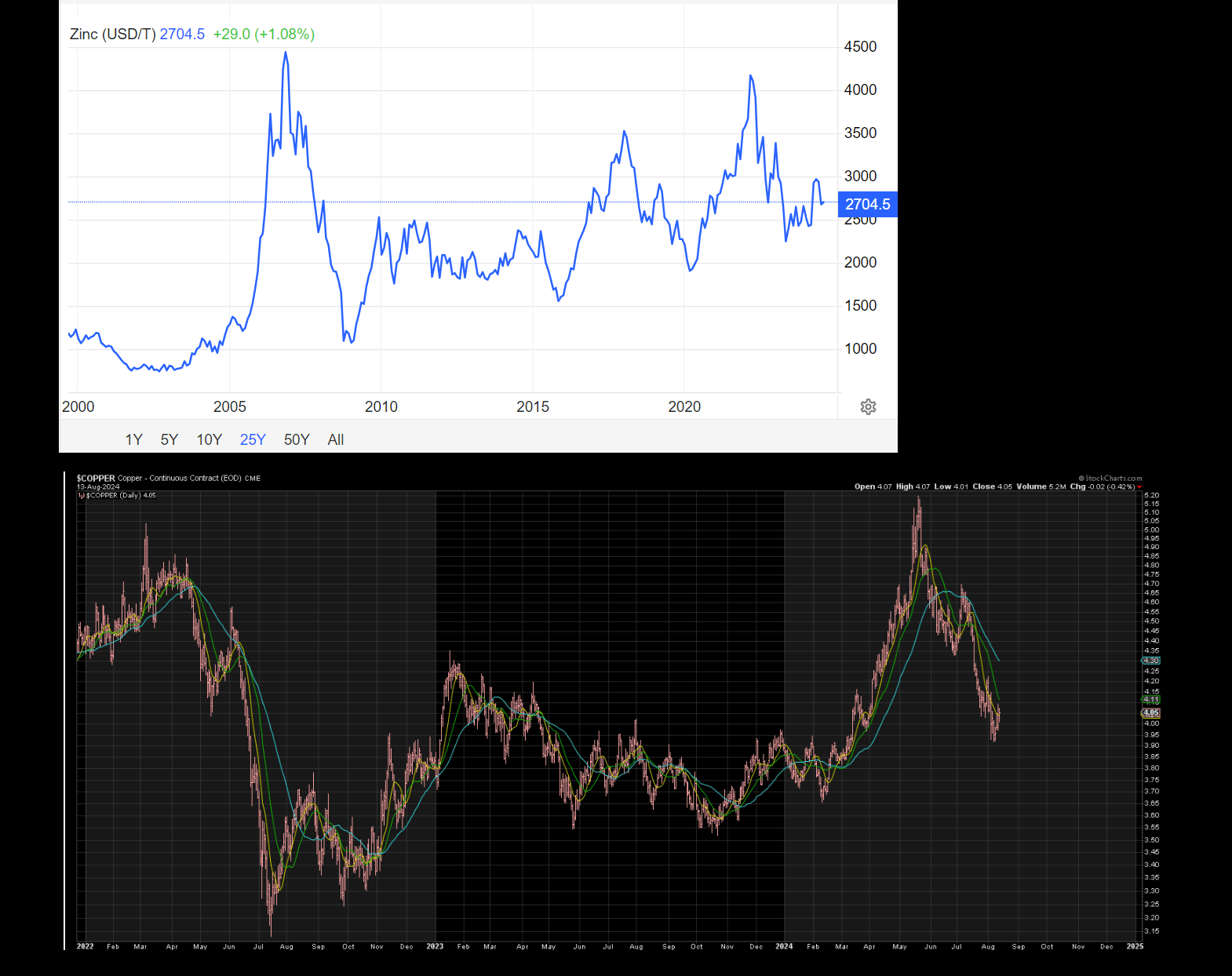

Improving cost performance in the second half of the year is related to access to the higher-grade Candelaria East Zone at La Colorada (improved ventilation) and higher production levels at Cerro Moro. Plus, gold’s recent march to $2,500/oz certainly isn’t hurting its silver segment AISC, with mines like La Colorada, Cerro Moro, as well as higher zinc and copper prices year-over-year at San Vicente and Huaron relative to Q3-23 levels.

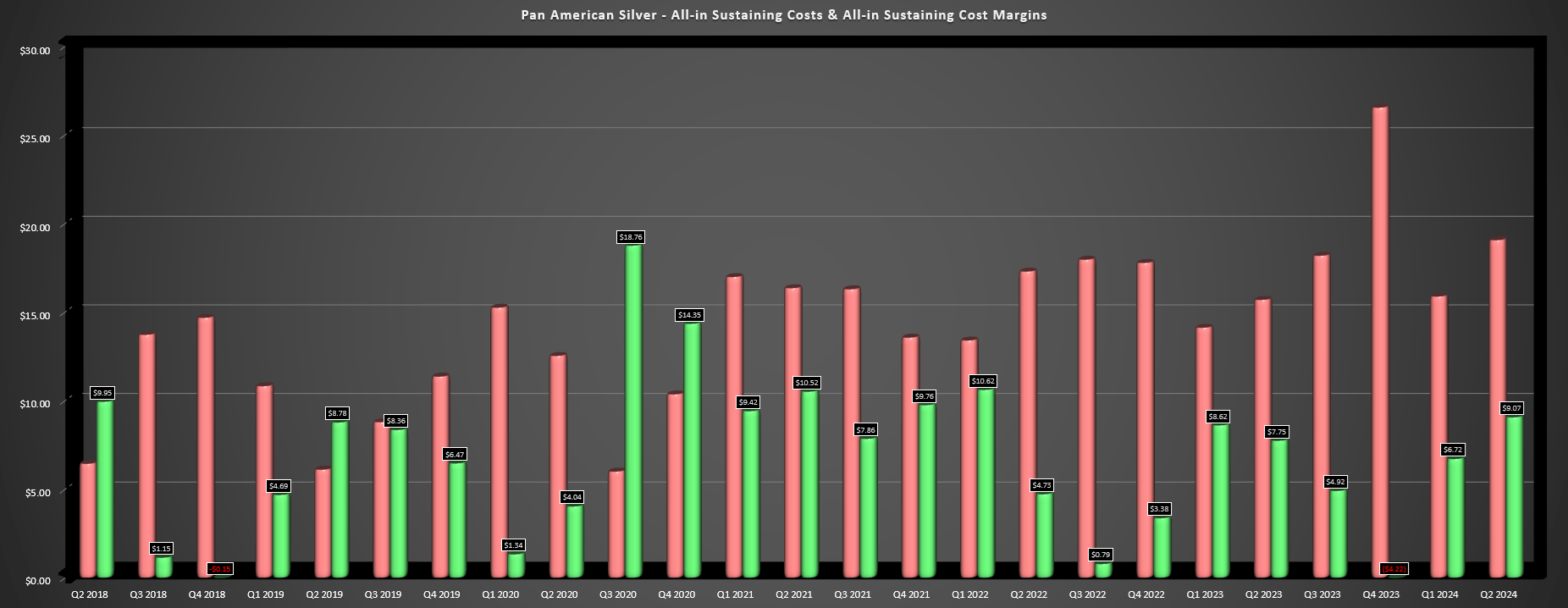

Pan American Silver Silver Segment AISC & AISC Margins - Company Filings, Author's Chart

Zinc Prices, Copper Prices - StockCharts, TradingEconomics.com

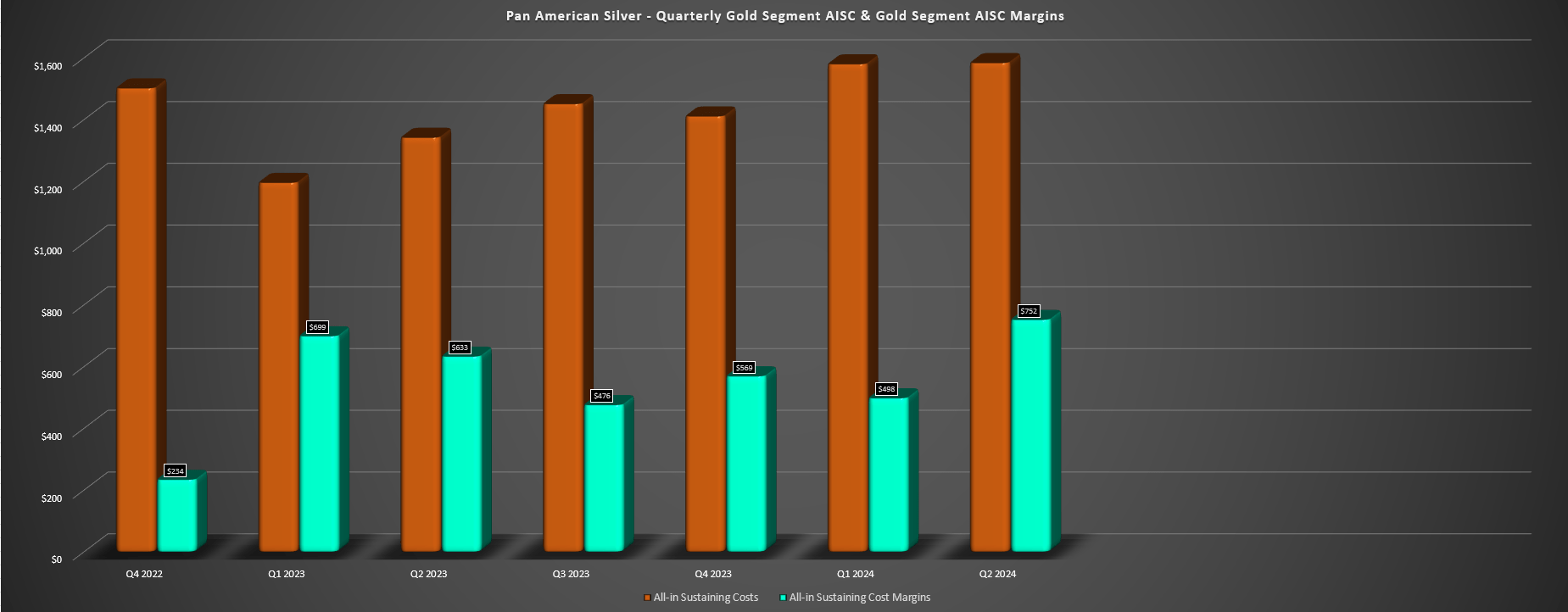

Given the impact of higher costs at Cerro Moro and La Colorada which dragged up consolidated costs, Pan American's silver segment AISC margins only increased to $9.07/oz from $7.75/oz in the year-ago period, with AISC margins actually declining marginally to 32.2% (Q2-23: 33.0%). However, Q2-24 was unusually weak for its silver segment, and we should see far more respectable costs going forward at La Colorada after two weaker years. As for gold segment margins, AISC margins improved to $752/oz vs. $633/oz, but, like silver segment AISC, saw all of their margin gains from the metal. This resulted in flat AISC margins year-over-year at 32.1%, well below higher-margin peers like Lundin Gold (OTCQX:LUGDF) at ~63.2% in Q2-24.

Pan American Silver Gold Segment AISC & AISC Margins - Company Filings, Author's Chart

Overall, Q2-24 costs have continued to trend higher for Pan American Silver on a year-over-year basis, but there is reason for optimism. This is because with a significant improvement in margins expected going forward at La Colorada and with another strong quarter ahead for by-product credits, I would expect materially stronger H2-24 results for Pan American combined with a material improvement in net debt once the La Arena sale closes ($245 million due on closing, expected to be completed in Q3-24).

Combined with much easier comps on deck in Q3-23 (Q3-23: $18.19/oz AISC), Q3-24 is set to be a far better quarter for Pan American, especially with silver and gold both hovering over 20% above Q3-23 levels ($1,975/oz gold, $23.15/oz silver).

Recent Developments

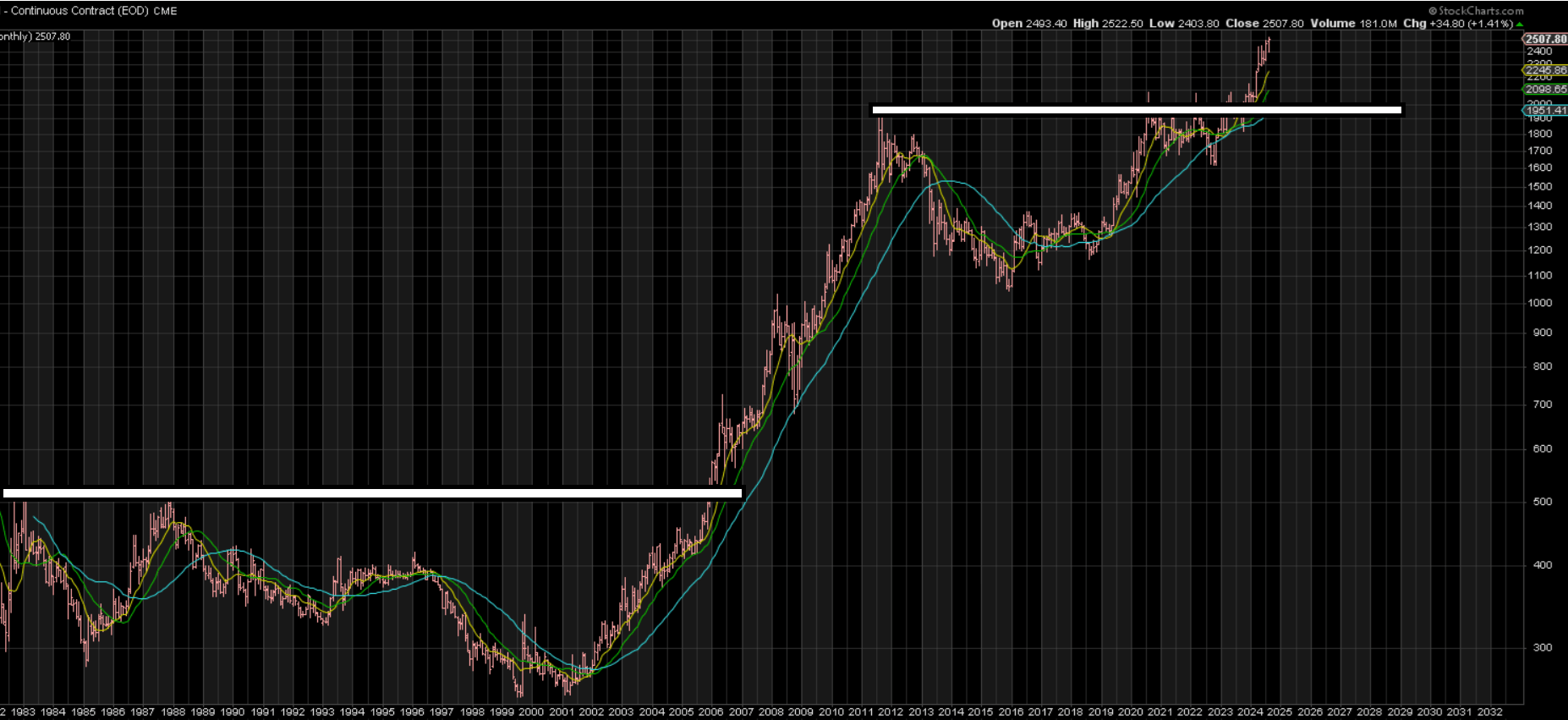

As for recent developments, the recent gold price strength has certainly been a major positive development for Pan American, especially after adding ~500,000 ounces (ca. 19 t) of incremental gold production at lower costs to its portfolio from the Yamana deal. And although some investors outside the precious metals sector may believe that the ship has sailed in terms of positioning, the below charts of the gold price and Gold Bugs Index provide some context. As highlighted below, the gold price has successfully completed a major base breakout and continues to march to new highs, with any sharp pullbacks likely to find strong buying support.

Gold Monthly Chart - StockCharts.com

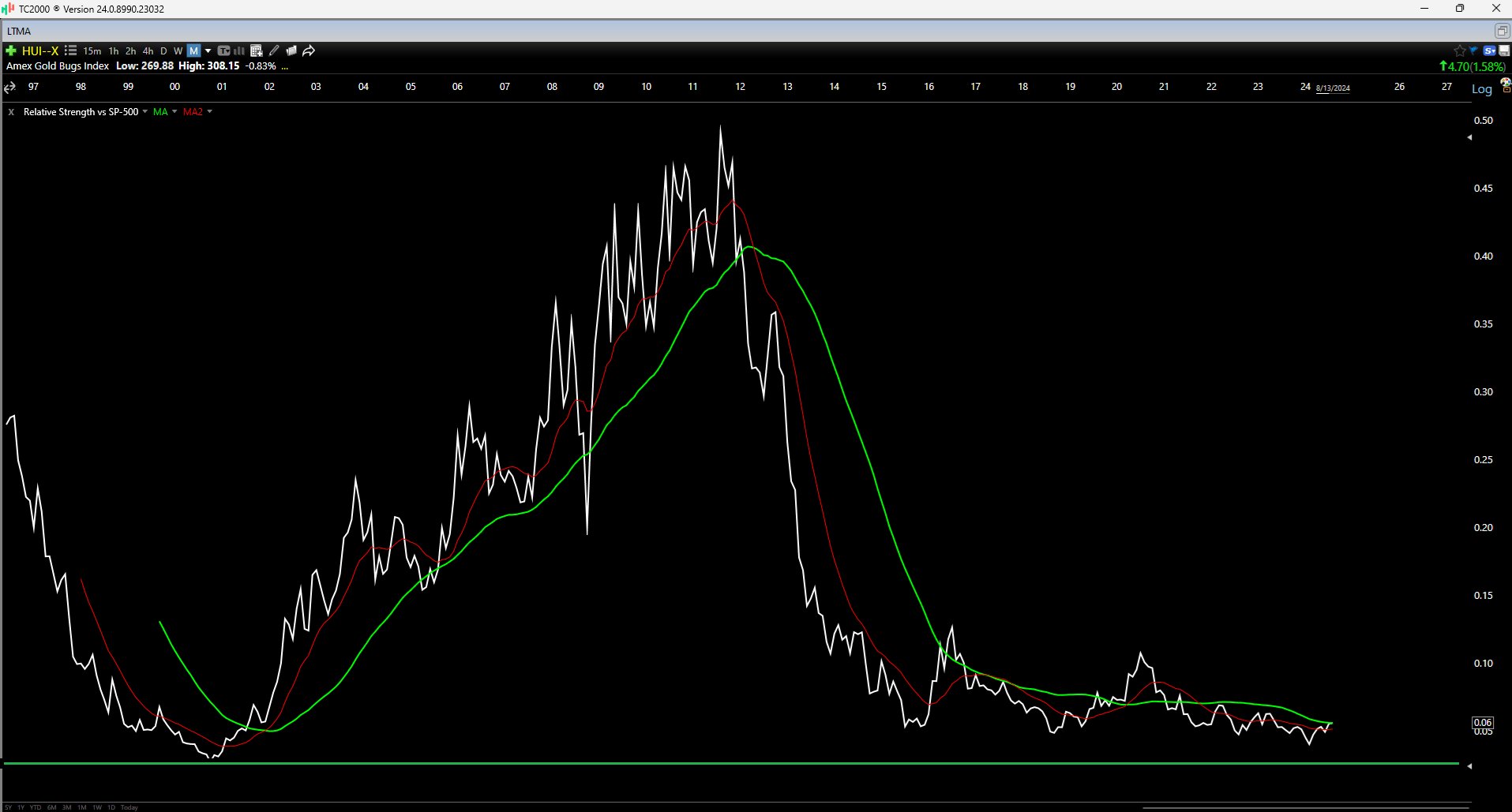

Gold Bugs Index vs. S&P-500 Ratio - Worden

Meanwhile, the Gold Bugs Index appears to be only starting to awaken from a 15-year slumber and downtrend vs. the S&P 500 (SPY) after the ratio came down to within a hair of where it found support following a previous decade plus long bear market that ended in 2000. This has set up the potential for significant mean reversion, assuming one positions themselves in well-run and high-quality miners that have proven their ability to consistently grow per share metrics.

As for Pan American's progress on de-leveraging, the company announced during the quarter that it would be selling its La Arena Mine and La Arena II Project (gold/copper) for $245 million in cash on closing and a 1.5% NSR on the La Arena II Project. Additionally, Pan American will be entitled to $50 million in contingent payments if commercial production is achieved at La Arena II. Overall, I see this as a win-win for both parties. Pan American places itself in a position to be near a net cash position by year-end just over a year out from completing a major deal and Zijin Mining gets a phenomenal gold-copper asset that is better served to finance this mega project (*) vs. Pan American that prefers to focus on gold/silver.

(*) La Arena II's upfront capex was estimated at ~$1.4 billion in 2018 in a PEA completed by Tahoe ahead of its acquisition by Pan American. This figure is likely well north of $2.0 billion today, after factoring in inflation and tightening up costs to DFS level. (*)

As for Pan American's balance sheet, net debt has improved to ~$470 million, but there is room for further divestment after what's already been a highly successful period of portfolio optimization. This includes two extremely valuable royalties and several other early-stage exploration assets that may not fit its portfolio, depending on what it decides to develop next. As for share repurchases, Pan American did not repurchase any shares in Q2-24 after buying back ~1.72 million shares at US$14.16 in Q1-24, electing to be opportunistic with its purchases.

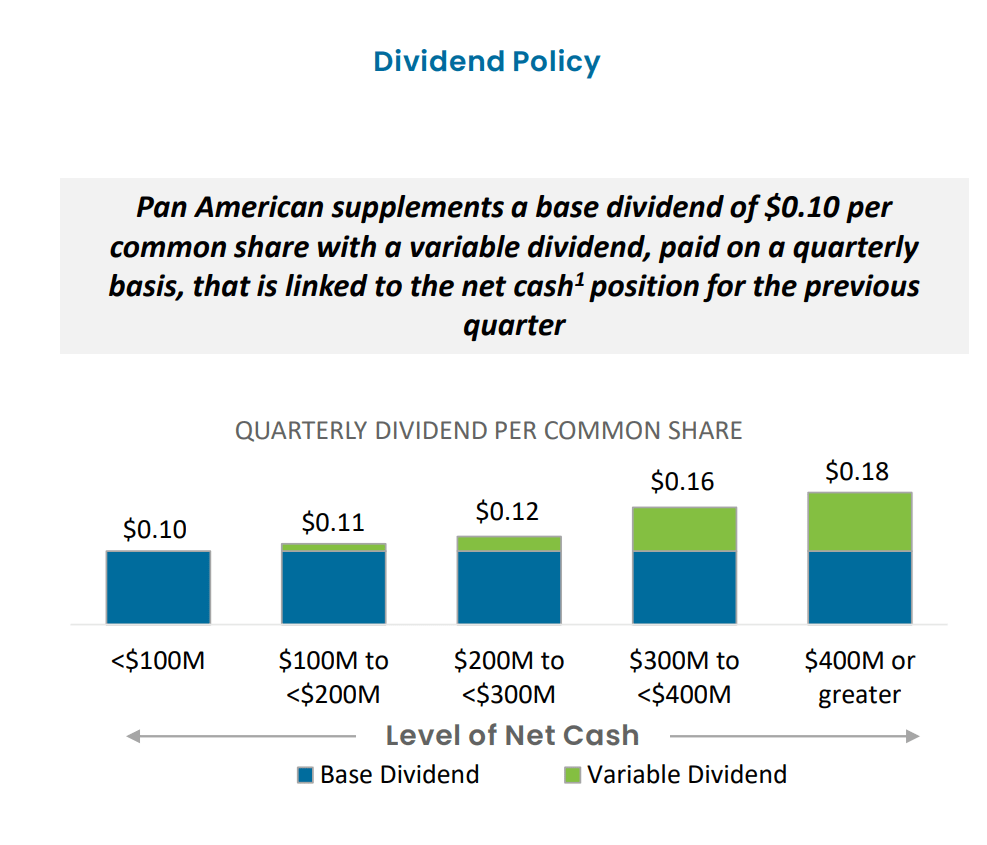

Pan American Dividend Policy - Company Website

Finally, as for Pan American's dividend policy, the company is already paying a leading dividend among its silver peers ($0.40/year), but is set to see an increase in its dividend by H2-25, with the potential for a material increase in 2026. This is because the base dividend is supplemented by a 10% increase ($0.01) to $0.11 if Pan American holds $100 million to $200 million in cash, increasing further to a 20%, 60% increase and 80% increase in the base dividend if Pan American is holding upwards of $400 million in cash. Given that I would expect Pan American to have upwards of $400 million in cash net by Q2-26 even under conservative assumptions, investors that bought under US$15.00 have certainly locked in a very nice yield, with the potential for an annual dividend of US$0.60+ in 2026 (~4% yield).

Overall, recent developments have certainly favored Pan American, and it's unique in the sense that it provides exposure to silver with a proven team capable of growing per share metrics and in a much lower-risk vehicle than the bulk of its silver peers (primarily a lack of operational/jurisdictional diversification). Let's look at its valuation below:

Valuation & Technical Picture

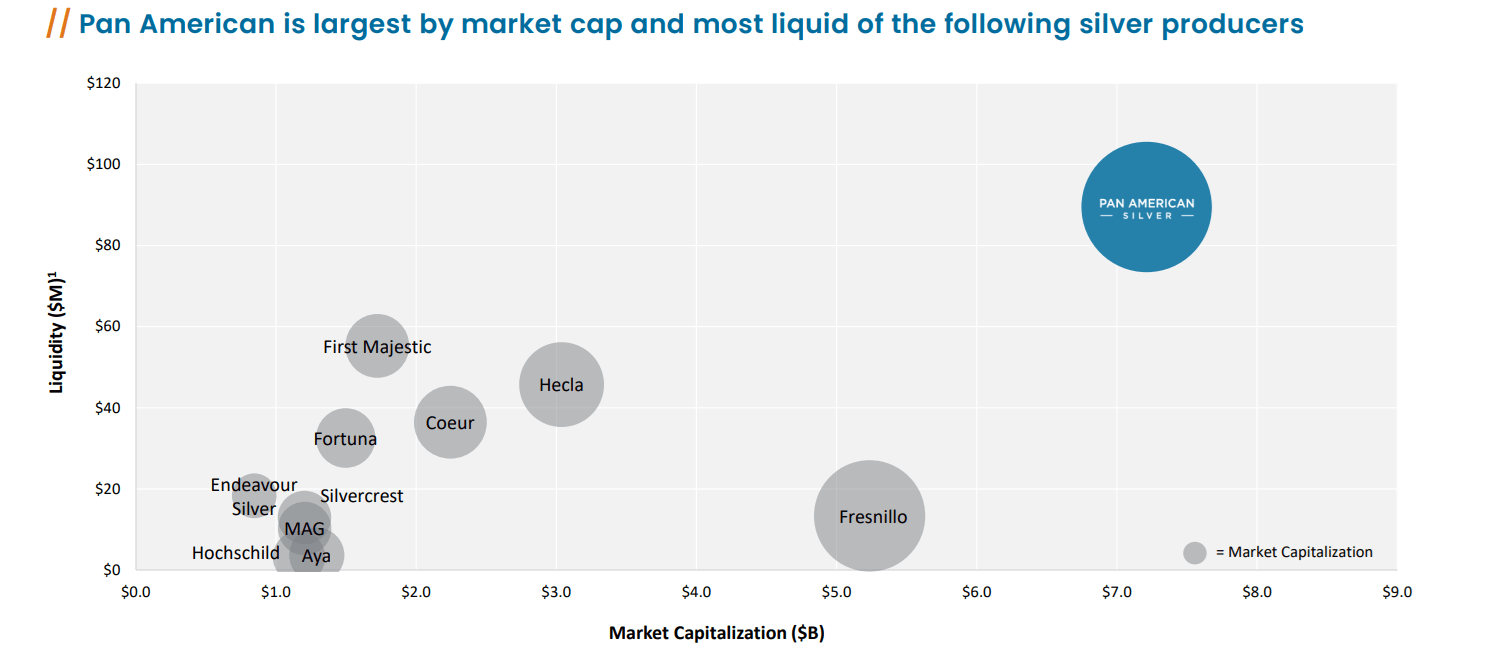

Based on ~365 million shares and a share price of US$19.80, Pan American trades at a market cap of ~$7.22 billion and an enterprise value of ~$7.69 billion. This makes Pan American the highest valued silver producer by a wide margin, currently valued at more than Hecla (HL), First Majestic (AG) and Endeavour Silver (EXK). And while Pan American is not cheap today relative to most of its gold producer peers, Pan American is one of the ways to get leverage on silver with relatively low risk, benefiting from the following unique attributes relative to its silver peers:

1. industry-leading diversification — 10 mines in 7 countries, with multiple projects backing up its current operating portfolio in Mexico and Guatemala.

2. superior liquidity — far greater liquidity vs. other multi-asset producers with silver exposure like Coeur, Hecla, and Fresnillo.

3. longer weighted-average mine lives and impressive pipeline — unlike several of its silver producer peers, Pan American has significantly increased its weighted average mine life with the Yamana acquisition, with further upside to mine life if La Colorada Skarn is developed.

4. industry-leading silver reserve base — Pan American has the largest silver reserve base of its peers at ~487 million ounces, excluding 200+ million ounces of future silver reserves if successfully converted at La Colorada Skarn.

PAAS Valuation vs. Peers - FinBox

Silver Producers by Market Cap & Liquidity - Company Website

As for Pan American's updated valuation, the stock is back to trading at just over 7x FY2025 operating cash flow estimates, a significant discount to its historical multiple of ~13.8x. Meanwhile, the recent correction has left PAAS trading at a more palatable valuation of ~14x more conservative FY2025 EV/FCF estimates, a very reasonable valuation relative to the still sky-high multiples on less diversified peers like First Majestic Silver.

That said, for investors that are open to owning primarily gold producers and gold/silver producers like Pan American, I continue to see far more attractive opportunities elsewhere in the sector. For example, B2Gold (BTG) trades at just ~7x FY2025 EV/FCF estimates, half the multiple of Pan American despite similar scale, a superior track record of per share growth, and higher margins. Hence, for investors looking to put new capital to work in the sector today, my preference is BTG, which is offering even greater value today to PAAS when it previously spent months below US$15.00 per share before finally starting to re-rate to the upside as it has since Q1.

Pan American Silver Historical Cash Flow Multiple - FASTGraphs.com

B2Gold Valuation vs. Peers - Koyfin (B2Gold Valuation vs. Peers - Koyfin)

So, what's a fair value for the stock?

Using what I believe to be fair multiples of ~13.0x FY2025 P/CF estimates and 1.4x P/NAV (6%) and a 65/35 weighting to P/NAV vs. P/CF, Pan American's updated fair value comes in at US$23.90. As discussed in past updates, I would not be surprised to see PAAS' overshoot what I believe to be a conservative fair value estimate given that it has historically traded at closer to 18x cash flow estimates during bull moves for precious metals stocks, and as high as ~20x cash flow at its 2016, 2020, and 2022 peaks. And even if we use a more conservative multiple of 15.0x for the upper end of its range (range of 10x-20x previously), PAAS would trade closer to US$37.50.

I am not counting on the latter and certainly would not make that my base case, but I am simply pointing out what is possible if we were to see a return to multiples we have seen at prior peaks.

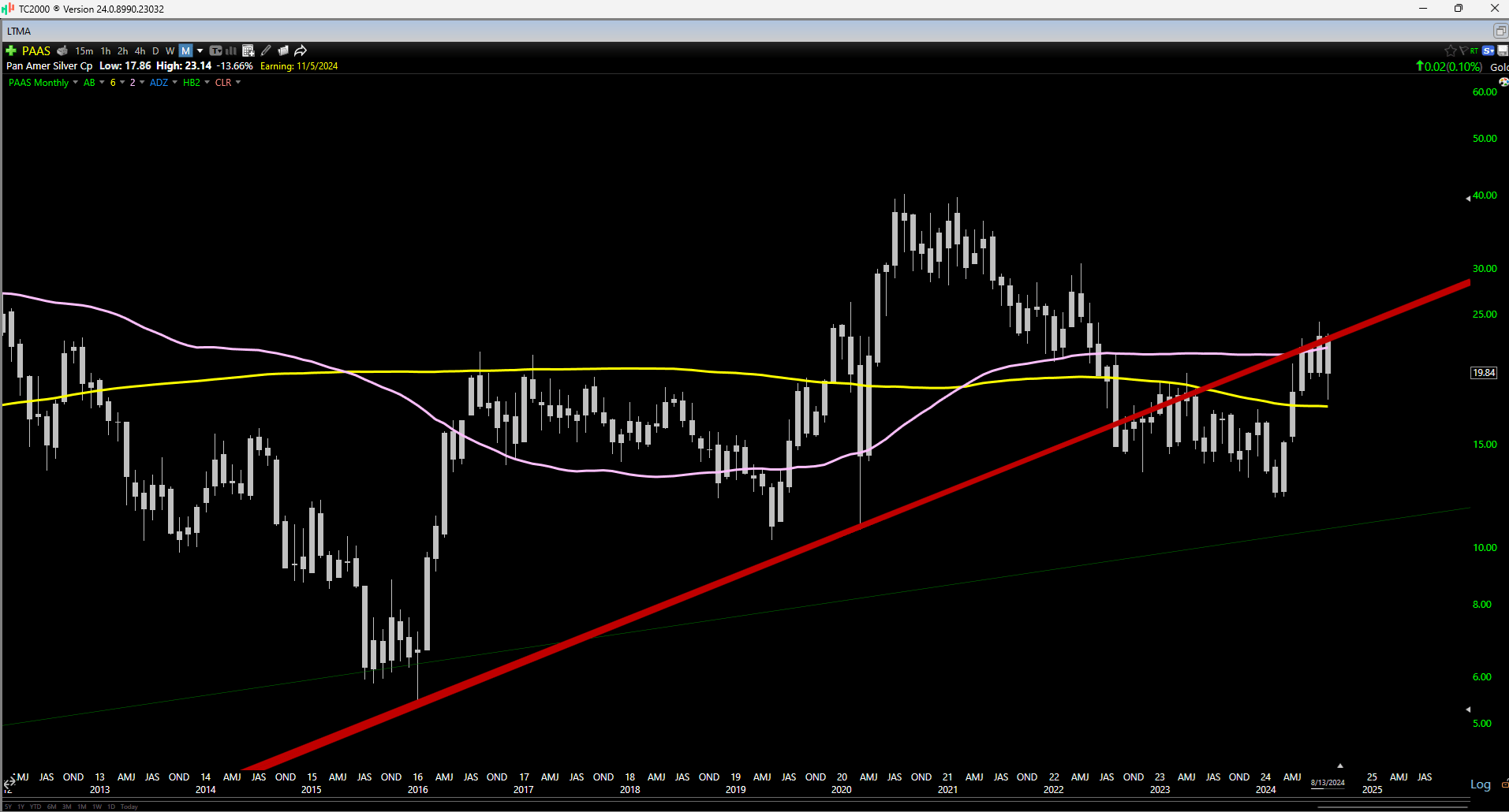

Finally, as for its technical picture, PAAS has rallied back above its long-term moving average (yellow line) after years spent getting rejected at this moving average, but saw a sharp downside reversal at the underside of its broken uptrend line. This has resulted in a volatile to August — giving up nearly all of its July advance. On a positive note, PAAS' recent pullback has helped to reset its chart and the stock looks like it wants to make a higher low in the US$16.80 — US$18.00 range, which would be a positive development from a bigger picture technical standpoint.

PAAS Monthly Chart - Worden

To summarize, I don't see any reason to lose sleep over Pan American Silver Corp.'s recent share-price correction which was overdue after PAAS' got ahead of itself, and I would expect any 25%+ pullbacks in the stock from its highs to provide buying opportunities.

Summary

Pan American Silver had a softer Q2 but still managed to generate record revenue, make further progress on deleveraging (La Arena sale pending closing) and is set up to enjoy a much stronger H2-24 with its ventilation infrastructure at La Colorada complete. Hence, for investors looking for a producer with one of the largest silver production profiles globally, I would view any 25% plus pullbacks in PAAS' stock as buying opportunities.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.