Exact Sciences: Cost Optimization And Product Strength

Summary

- Exact Sciences stock is down 35% since August 2021, now trading at around $58.75.

- The second quarter of 2024 (Q2) results beat expectations with revenue growth driven by the Cologuard screening segment.

- It raised adjusted EBITDA guidance for 2024, demonstrating confidence in continued sales momentum and profitability.

- It is likely to suffer from volatility risks as it continues to strike a balance between growth and profitability.

- The stock is a buy with a potential 27% upside also given the way it is improving its competitive position and leveraging AI for accelerating data analysis.

Hiroshi Watanabe

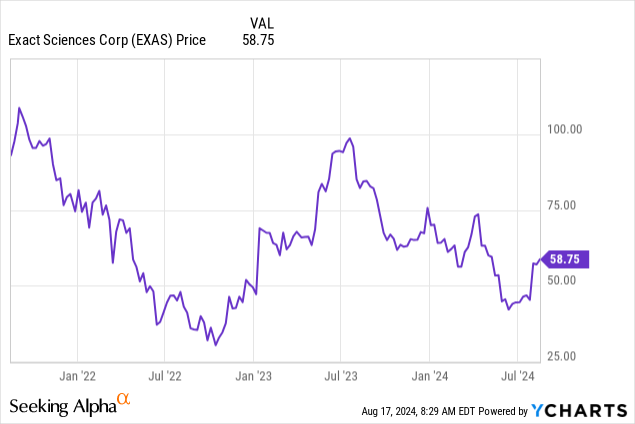

Since I last covered Exact Sciences (NASDAQ:NASDAQ:EXAS) back in August 2021 it is down by around 35%, it is trading at around $58.75 as per the chart below. This thesis aims to show that the recent upside should continue amid volatility.

Data by YCharts

Data by YCharts

Three years back, I had a hold position as despite the biotech's DNA-based cancer diagnostics products becoming mainstream, this field involved heavy R&D expenses with competition faced from the likes of Invitae (OTCPK:OTC:NVTAQ). It was also richly valued at 12.14x to trailing sales.

It is now trading at about one-third of this ratio and has recently beaten analysts' expectations during the recently released financial results for the second quarter of 2024 ("Q2"). Hence, this time around, I am bullish also based on the strength of its flagship Cologuard product.

Screening Product Strength

First, revenue of $699 million was reported during Q2, up 12.4% from the same period last year, beating analysts' forecasts by $9 million while adjusted EPS came in at -$0.09, exceeding estimates of -$0.37 per share by far. Looking for an explanation, this performance was mainly fueled by 15% YoY revenue growth in its screening segment, driven by Cologuard. Additionally, the precision oncology segment which constituted 24% of overall revenues during Q2 recorded a growth of 7%.

For investors, Cologuard is a non-invasive colon cancer screening test involving taking a stool sample and mailing it to a laboratory for analysis. This test which started to gain popularity in 2021 as a result of Covid-led social distancing measures represents an evolution in comparison to conventional testing methodologies when someone has to go in the lab.

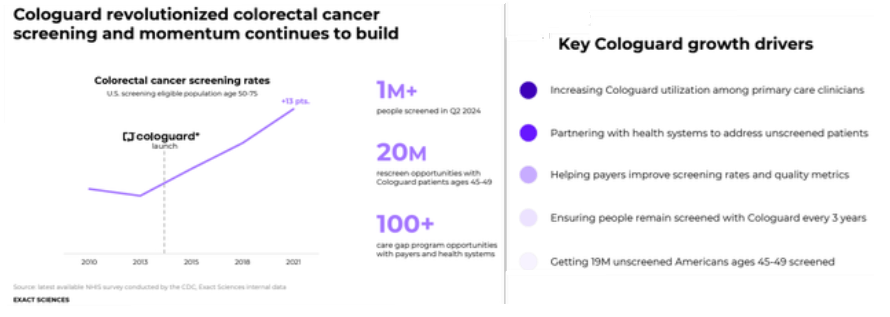

Furthermore, Cologuard whose capabilities involve detecting DNA-related changes associated with colon cancer together with the associated precancerous polyps also represents a significant change from traditional and invasive methods that involve a visual examination of the colon. As a result, it has revolutionized colorectal cancer screening, and its utilization among primary care clinicians continues to trend higher as shown below.

Company presentation (seekingalpha.com)

However, Cologuard does have competitors, in the form of FIT (Fecal Immunochemical Test) that detects blood in the stool as a probable indicator of someone suffering from colon cancer. However, FIT only detects the hemoglobin in the blood, thereby increasing the probability of a false negative (or an erroneous) result due to the person already suffering from another ailment which includes intermittent bleeding. Still, FIT is a less expensive non-invasive option for early-stage colorectal cancer which implies the screening method selected by a patient ultimately depends on healthcare provider recommendations.

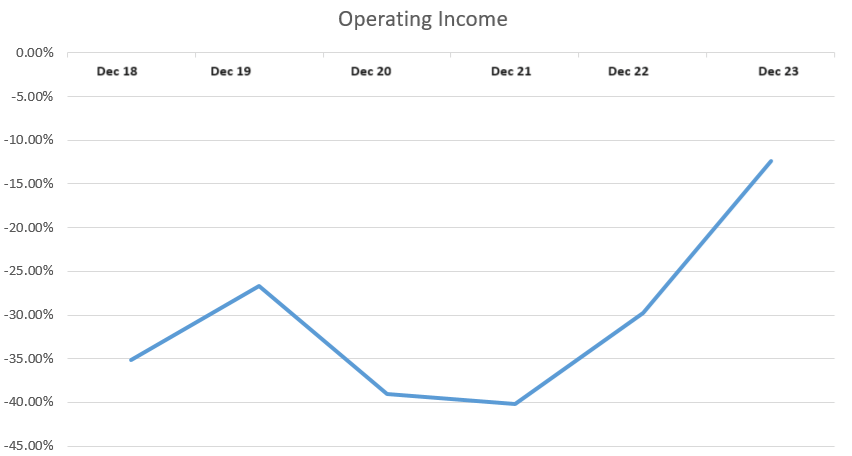

As a result, Exact Sciences has to spend money on research to continuously enhance its product and marketing to promote Cologuard which has translated into operational expenses amounting to 86% of total sales for FY-23. As a result, it is loss-making, but as shown in the chart below, progress has been made on the operating income front.

Chart built using data from (www.seekingalpha.com)

This progress is likely to be sustained given the progress demonstrated in EBITDA.

Raised EBITDA Guidance and Likely To Deliver A Topline Beat for FY-2024

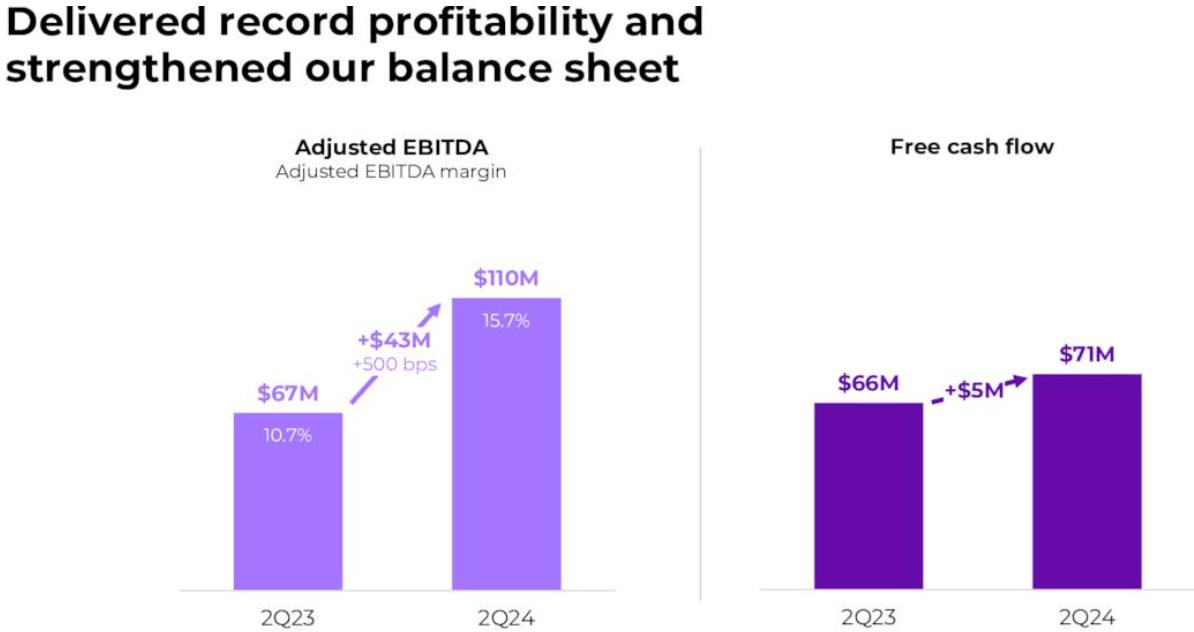

Thus, there was a 65% YoY surge in the adjusted EBITDA in Q2, from $67 million to $110 million as shown below, which in addition to volume growth (or number of Cologuard testing kits sold) was due to improved operational efficiency, namely productivity gains, and expense controls, particularly in G&A (General and Administrative) expenses.

Company presentation (seekingalpha.com)

In addition, based on the continued cost optimization efforts, the company can continue to grow profitably. Thus, the full-year adjusted EBITDA guidance has been raised to between $335 million and $355 million compared to the $325 million to $350 million range earlier. Furthermore, since the intent is to re-invest the savings made into growth areas, there is ample scope for profitable growth without necessarily taking additional debt.

Looking deeper into the growth strategy, the additional EBITDA gains are expected to be achieved on the back of FY-2024 revenue expectations of $2.81 billion to $2.85 billion whose midpoint of $2.83 billion would represent a 13.3% growth over last year.

Now, I believe that this could be beaten because of four reasons.

First, the 13.3% YoY growth expected for FY-2024 would represent a deceleration from the 20% recorded during FY-2023 and it is more likely for the company to exceed this target as it has seen sustained momentum in the adoption momentum for Cologuard. It is emerging as a preferred choice by health system providers and payers for large organized screening programs because of compliance with USPSTF (United States Preventive Services Task Force) guidelines. It also follows the HEDIS standard which is widely used quality metrics adhered to by the healthcare industry.

Second, the company is proposing value-added services in the form of its patient compliance engine, namely through the use of data-driven techniques for reporting purposes and leveraging artificial intelligence to automate workflows concerning patient screening. This incentivizes healthcare providers by lessening the amount of administrative work they have to do thereby allowing more focus on patient care.

Third, the company recruited additional sales representatives in May and since they normally take six months to become fully operational, they could contribute to additional orders. Fourth, the company has consistently beaten quarterly topline estimates since the second half of 2021 which tends to imply that the management is conservative when providing guidance.

Thus, as we move closer to the end of this year, it is likely for analysts to revise their estimates higher meaning the company deserves better.

Valuing Exact Sciences

To this end, investors will note it is precisely because of better EPS revision that Seeking Alpha's Quant ratings upgraded the stock from hold to buy on August 12.

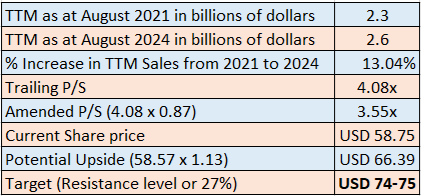

However, the problem is that its trailing P/S of 4.08x trades higher than the median for the healthcare sector by 8% despite dropping by around 67% since August 2021 when I last covered the stock. However, incrementing the share price by 67% would ignore the decelerating revenue growth trend suffered since 2020.

As a solution and to come up with a fair value for the stock, I compare the TTM (trailing twelve months) sales to obtain a more accurate picture of the difference in financial performance as tabled below. The result shows an increase of 13% from 2021 to 2024 and I discount the P/S accordingly, to 3.55x. This conversely translates into a target of $66.39 based on the current share price of $58.75.

Table built using data from (www,seekingalpha.com)

Now, considering that this stock was severely punished by the market due to its high debt as the Federal Reserve aggressively tightened monetary policy in 2022 as per the introductory chart, the opposite should happen in case the U.S. Central Bank cut rates in September. With 75% of market participants expecting a cut next month, the stock could rise by 27% to its resistance level of $74-$75, reached on December 2023 and April 2024 (chart below) in case the Fed turns dovish.

To further justify my optimism, lower borrowing costs pave the way for the company to refinance at lower rates as its balance sheet holds only $946.8 million of cash versus $2.78 billion of debt. Also, interest payments which amounted to $19.4 million in FY-2023 are likely to go down.

Along the same lines, FCF progressed by $5 million during Q2 and the company generated $107 million of cash from operations which enabled it to repay the $50 million outstanding balance of the AR (Accounts Receivable) securitization facility it contracted in December last year. This facility provided additional liquidity to finance its growth and operations without the need to borrow at the prevailing above-5% interest rates.

Volatility Risks Remain but it could Potentially Appreciate by 27%

On the other hand, if the Fed does not proceed as expected, the stock is likely to be volatile and could dip, unless it continues to show progress in profits and cash generation. In this respect, Exact Sciences has to execute while maintaining a delicate balance between growth and profitability. Thus, employing more sales reps to reach healthcare provider providers to encourage them to recommend Cologuard means more orders, but is likely to result in higher operating expenses.

Moreover, any slowdown in related investment will likely directly impact the ability of the company to continue gaining market share in screening. To this end, keeping the same revenue guidance for FY-2024 while expecting a higher EBITDA could also hint at prioritizing cost optimization in contrast to spending for growth.

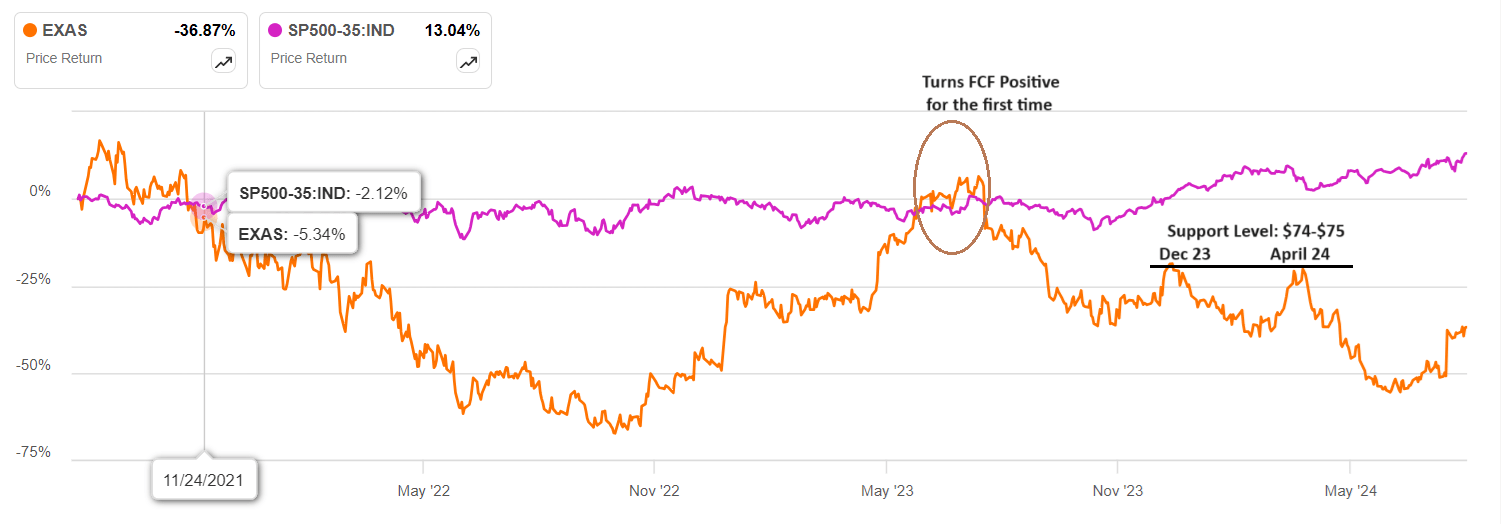

Moreover, this is a rate-sensitive stock, further evident when comparing its performance with the S&P 500 Healthcare sector index as shown below. Thus, most of the time it underperformed the index except for mid-2023 when it turned FCF positive for the first time.

seekingalpha.com

In these circumstances, price performance will also depend on progress toward profitability and FCF. To this end, the company surged by 27% on July 31 after announcing Q2's results when it also returned to FCF-positive status and provided better EBITDA guidance for the full year. Coincidentally, this thesis also makes the case for a 27% upside based mainly on product strength, progress on profitability, and the ability to consistently beat analysts' estimates. While volatility risks remain, it has shown progress in operational execution resulting in strong financial performance despite facing competition.

In this connection, its competitive position improved after securing an exclusive license with TwinStrand Biosciences for next-generation sequencing enabling the detection of very rare mutations that would otherwise be missed and the use of AI to develop more sophisticated diagnostic tools.

Ending with profitability, a metric the management has prioritized, the biotech is in the process of hiring a Senior Director, of AI Strategy and Development to deliver tangible business value and support strategic goals, meaning that it should better leverage innovation especially when it comes to integrating LLMs (large language models) with existing workflows. In this respect, by reducing research time, accelerating data analysis, and doing more with less staff Gen AI can lead to productivity gains of up to 30%.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.