Sigma Lithium: Things Are Slowly Improving

Summary

- Sigma Lithium Corporation reported earnings below expectations, with a loss of 9 cents per share and revenues of $45 million. It showed operational improvements and better pricing power.

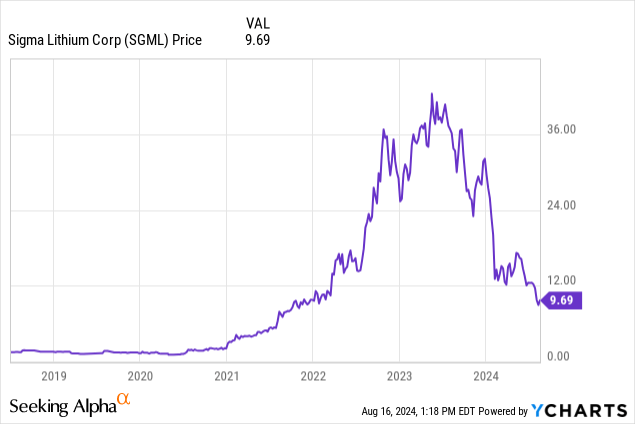

- SGML stock gave back most of its gains from 2022 and 2023, but now might be at more "investable" levels from last year's bubble levels.

- It's still a speculative bet at this point, and we will see if Sigma Lithium can scale fast enough to achieve profitability. Demand is definitely there for its lithium, though.

xeni4ka

Sigma Lithium Q2 Earnings

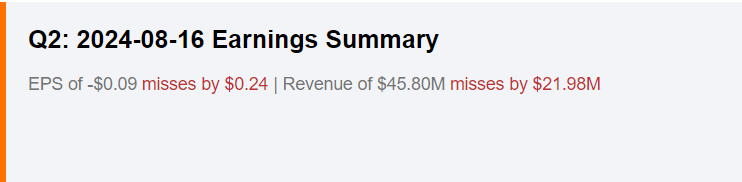

Sigma Lithium Corporation (NASDAQ:SGML) (TSXV:SGML:CA) reported earnings this week, which came below expectations. The company reported a loss of 9 cents per share while analysts were looking for a profit of 15 cents per share on revenues of $45 million while analysts were looking for $67 million.

Earnings Summary (Seeking Alpha)

I've originally covered this company in an article titled Sigma Lithium: Great Start But More Work To Do, where I discussed the company's business model and what sets it apart from other companies in similar line of work. Unfortunately, the stock has crashed since then and dropped by almost -70% in a short period of 8 months, indicating that investors don't have a lot of faith left in this company despite its operational improvements over time. Perhaps investors were expecting those improvements to come at a much faster rate, and they are disappointed with how long things are taking.

During the quarter, the company announced a few positive developments. One of those developments was that it achieved more operational efficiencies and already reached cost targets it set up for 2024 last year. Also, the company's pricing power seems to get better as its lithium sells at a price which now offers a premium of about 10% versus lithium produced by its peers. Furthermore, the company's cash margins have been improving even though at a slower rate than expected. The company is also working on increasing its scale of both production and shipments.

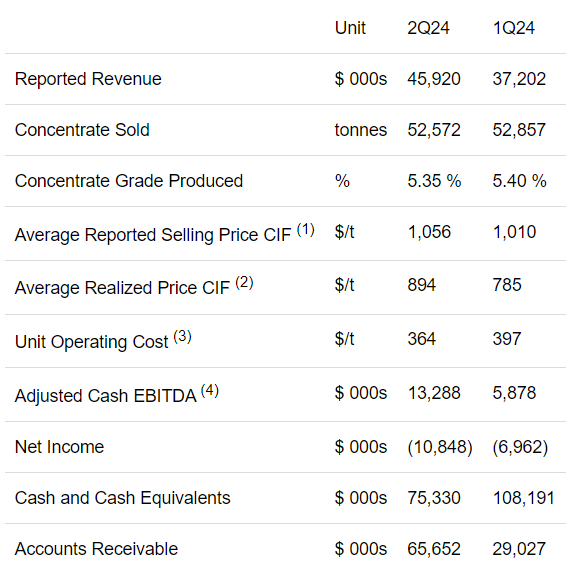

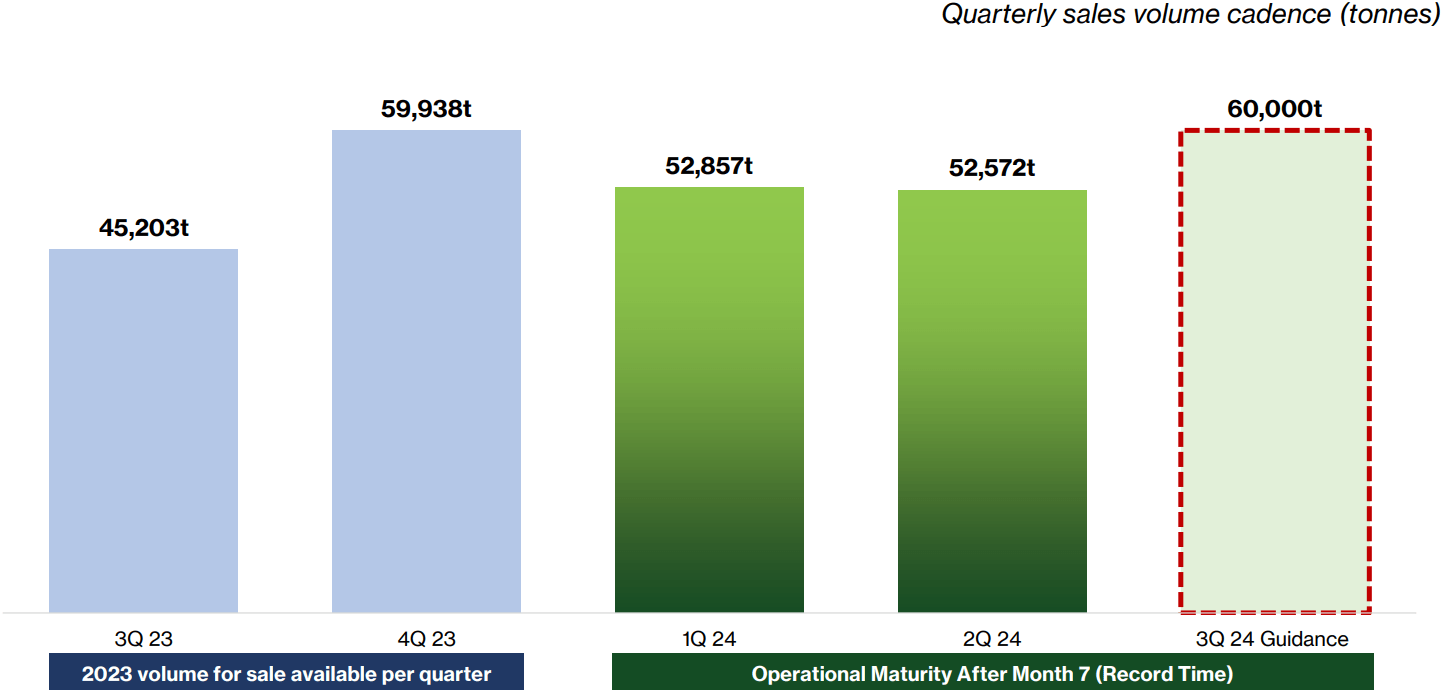

During the quarter, the company's revenues jumped from $37 million to $46 million even though tonnage was mostly flat (in fact slightly down from 52,857 to 52,572. The increase was due to better pricing as the average reported sales price climbed from $1,010 to $1,056 and the average realized price jumped from $785 to $894. Furthermore, the company's margins got better because its unit operating cost also dropped from $397 per ton to $364 per ton due to operational efficiencies it achieved during the quarter. These two factors resulted in the company's adjusted cash EBITDA jumping from $5.9 million to $13.3 million, even though its net income was still down and its cash holdings dropped from $108 million to $75 million during the quarter. Keep in mind that the company's accounts receivable jumped from $29 million to $65 million, so once those payments come in, the company's cash position should improve again. As a matter of fact, the company already said that its current cash balance as of August is already back to $99 million, so some of those payments must have been received already.

Operating Metrics (Seeking Alpha)

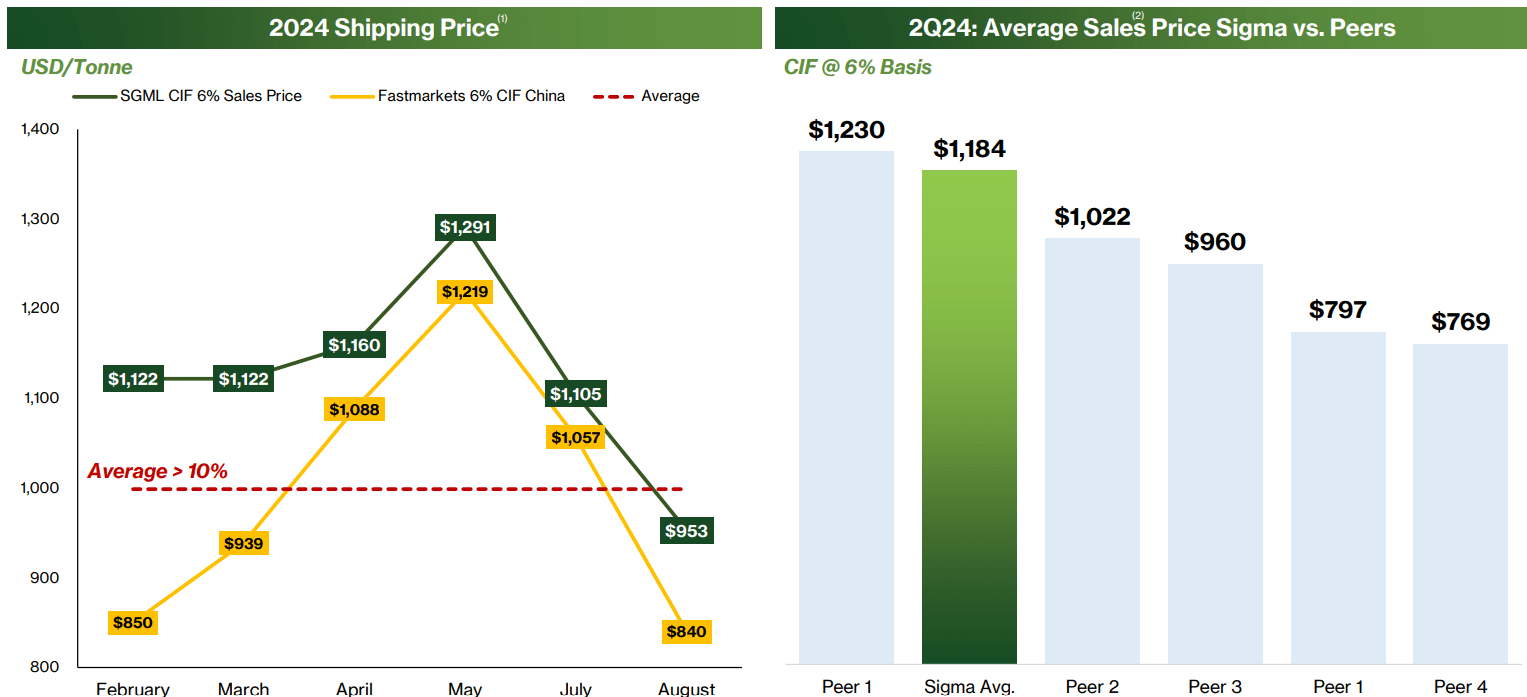

One thing the company seems to be proud of in its latest results is its ability to get better pricing for its lithium, which is said to be of higher quality. Lithium is a commodity with a fluctuating price determined by the commodities market, but not all lithium is equal. As a matter of fact, lithium's price can fluctuate greatly from producer to producer regardless of where they sit in the commodities market, depending on its quality. For example, when we look at tonnage prices below, we see that it can range widely from $769 to $1,230 per ton depending on who is selling it and its quality. Sigma seems to have a 10% price premium above its peers on average, and it comes second out of all its peers with an average price of $1,184 per ton, which speaks volumes about the quality of its lithium. We don't know for sure if this price premium will be maintained forever and whether the company's future mines will offer the same quality of lithium (defined by high grade, high purity and being coarse-grained) that its current mines do, but so far, this metric looks pretty promising.

Pricing Power (Sigma Lithium)

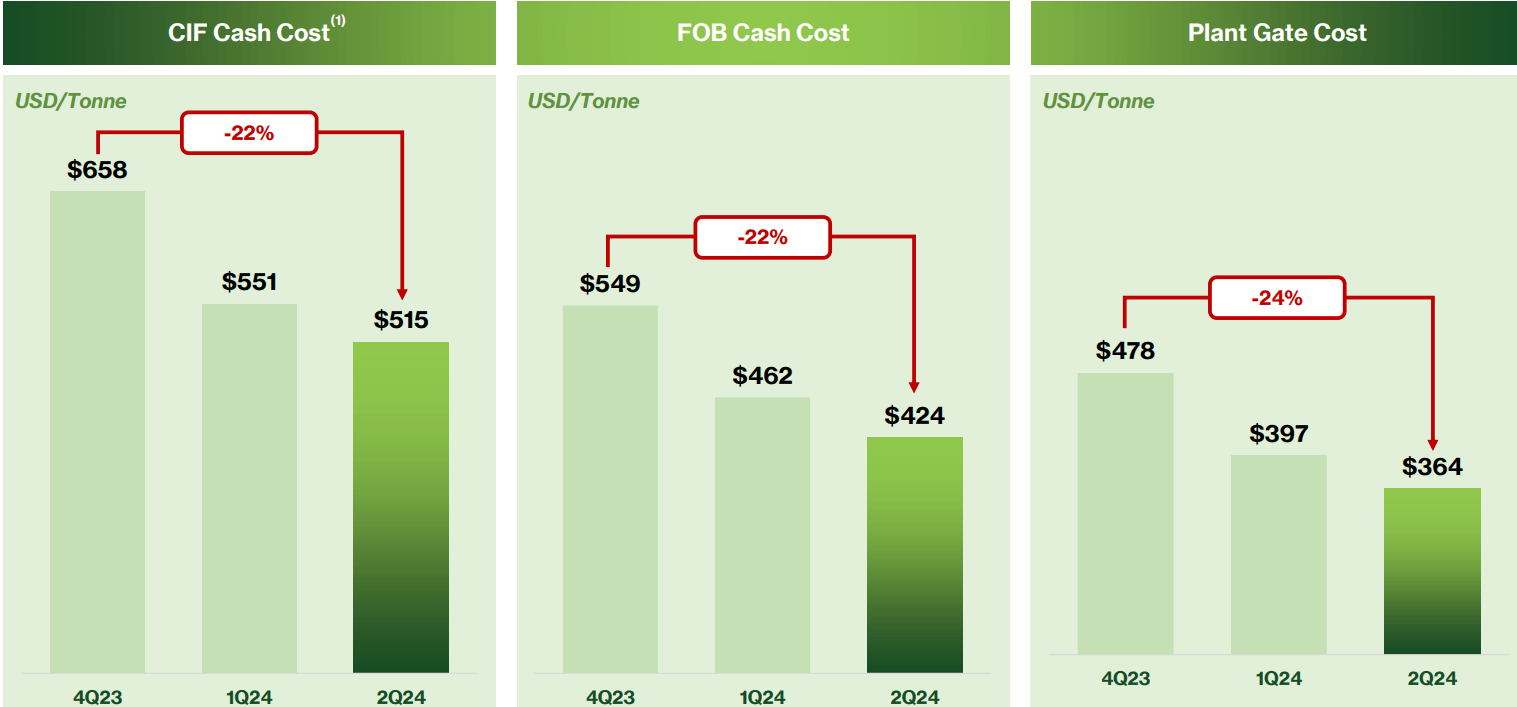

The company's cost structure continued to improve during the quarter as its pricing power improved, which helped with cash margins. Compared to 2 quarters ago, in the quarter, the company's total cash cost dropped by 22% both in terms of CIF and FOB and its plant gate cost was down by 24%. These cost cuts were driven by a variety of factors, such as having fewer accidents (in fact no accidents during the quarter), using better tools and methodology, getting better pricing from vendors such as shippers and warehouses and a variety of factors. Also, having more consistent processes and more consistent shipping schedules seems to have helped the margins as well. The company was able to cut all its costs across the board, and there might be even more room to improve its cost structure in the next few quarters as it looks into its operations and processes. Keep in mind that these costs don't include depreciation and amortizations, which is what caused the company to post a loss overall instead of a profit. At the end of the day, the company is still not profitable in terms of GAAP (generally accepted accounting practices).

Cost Reductions (Sigma Lithium)

Moving forward, the company will continue with its growth and expand its mines. It expects to increase its shipment to 60k tons in the next quarter. Despite the fact that the lithium market is highly cyclical, and its cadence can vary wildly depending on the state of the overall economy, currently demand has been rising exponentially in recent years due to the rise of electric vehicles and electrification of everything. There is also a lot of need for batteries for energy storage, so this cycle can continue for quite some time even if the overall economy might not be exactly booming right now.

Forward Guidance (Sigma Lithium)

I don't think the company will have trouble selling the lithium it mines anytime soon, but it will have to scale up faster and get even more efficient if it were to post a profit. Investors will not be impressed until they see net profits coming in, or at least a sustainable and predictable path to profitability. While the company's cashflow profitability situation looks promising, it's net profit position still leaves a lot of room for improvement.

Is SGML Stock A Buy/Sell/Hold?

SGML stock is down significantly from recent highs it achieved last year, but it's still up from a few years ago. This was basically a penny stock before 2021, and perhaps it rose too fast and too quickly between 2022 and 2023 and now gave back most of those gains, but this might also give many investors a good opportunity to average down and bring their cost basis down, especially if they made their original purchase at higher levels last year. I can also understand if some investors want to just sell and take their loss and move to elsewhere because they don't want to wait for this company to show profits. At the end of the day, this is a small-cap company with operating a commodity business in a different country, which also comes with a lot of political risks, some of which may or may not be visible to everyone.

Data by YCharts

Data by YCharts

For those investors with "faith", if the company can show profitability in the next year or so and continue to scale its business while improving efficiencies, it could result in some nice gains just like it did a couple years ago. Some could also say that the stock was a bubble earlier but now returned back to "investable" levels. At this point, this stock is still a speculative bet though, and you should keep your position size pretty small if you are going to stay invested.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.