Seabridge Gold Has Strong Prospects But Wait For The Dip

Summary

- Seabridge receives a "Hold" rating: gold and copper prices, as well as the company's projects, develop positively (important updates from KSM and 3 Aces), but shares are high relative to past trends.

- According to this analysis, investors should expect a stock price dip before another share price rally occurs.

- Based on recent events in the markets, potential downside catalysts include Fed interest rate decisions, recession fears in the US and continued subdued demand for copper in China.

Filograph

A “Hold” Rating for shares of Seabridge Gold

This analysis suggests another “Hold” rating on shares of Seabridge Gold (NYSE:SA) (TSX:SEA:CA), a Canadian developer of gold and copper properties in Canada and the US state of Nevada. The same rating was given in this previous article.

Last “Hold” Rating

Hereafter we will name the company “Seabridge”. Investors were advised to hold this stock to their portfolio, as by taking advantage of certain important advances in the development of promising metallic projects, the shares were well positioned to reap the benefits of gold and copper prices consistently in an upward trend.

Despite strong upside catalysts, only a Hold rating was assigned over a Buy rating, informing investors to wait for the share price to decline to more attractive levels under certain triggers of near-term pessimism that appeared looming. Since the share price changes are linked to the cyclicality of commodity prices about to suffer bearish sentiment, Seabridge's shares could hardly avoid the same kind of impact. So if investors had bought the dip, they would have better benefited from the subsequent share price rise driven by progress in the metals projects, accompanied by the bullish gold price.

In fact, since the last article on May 16, Seabridge shares have risen by 13.75%, which is better than the S&P 500's change of 4.57% at the time of writing, although a higher margin would have been possible had investors implemented the “buy-on-dips” strategy in early July 2024. The dip occurred mainly because of the following: Due to a positive correlation with copper and gold prices, Seabridge shares took a downward path and formed a significant dip in early July as market sentiment towards the two commodities burned for a short period. The “positive correlation” implies that Seabridge shares, and the metal price (copper or gold) move in the same direction: ("both") either up or down, regardless of returns that can vary significantly between them. Thus, bearish sentiment in gold and copper prices is most likely reflected in share prices trading down, while when metal price sentiment is bullish, Seabridge Gold shares are most likely experiencing an uptrend.

For the bearish sentiment: Copper prices were weighed down by “a weaker manufacturing data globally”, which was “only temporary” according to Citigroup Inc. (C) on July 5. The declining manufacturing activity in China played a big role as China is said to be “the world's largest copper consumer” by Melissa Pistilli in this write-up for Investing News Network, reported by Nasdaq. This is because if investor optimism over policy support in China is enough to bring the price of copper back to the “retest level” previously predicted by Citigroup, then we can conclude that manufacturing activity in China is currently languishing until one of its main sources of demand, “China's renewable energy infrastructure”, is getting the necessary political support for its upgrade. So far, it appears that this kind of political support has yet to arrive. In addition, it is now known that another sector is greatly affecting Chinese copper consumption and thus weighing on global demand: the crisis in the real estate development sector in China. This situation is still ongoing after “Chinese property giant Country Gardens' significant difficulties in meeting its offshore debt obligations.”

As for gold prices (XAUUSD:CUR), they were lower in early July due to two major downside winds: a) They were “pressured by a firmer US dollar currency” because with the troy ounce priced in US dollars, a more expensive purchase for foreign investors, who had previously been big buyers, caused overseas demand to tighten its purse strings, and probably some profit-takers were causing selling pressure. The gold prices also suffered as the Fed's July 31 meeting drew closer, a high probability of “interest rates remaining unchanged at high levels” putting “upward pressure on the opportunity cost of holding non-yielding bullion”, according to “Commodity Roundup” report from Arundhati Sarkar, Seeking Alpha News Editor.

Why This Analysis Expects Another Dip in the Seabridge Share Price in the Near Future

These short-term negative catalysts are important because they are expected to blow again in the near term, and if they cause another significant decline, they will provide another opportunity to strengthen the position in Seabridge Gold buying the dip, ahead of the long-term bright outlook for the metals and development of explorer's metallic projects.

After this brief period of negativity for metals prices, Seabridge shares began to recover, triggered by some news indicating relevant progress in the company's metals project portfolio, while good weather returned to the commodities market. The portfolio's upside potential will be explored later in the article in the “Recent Developments in Seabridge's Project Portfolio” section. Also, copper and gold prices that provided upside potential will be detailed later in this article, with a dedicated section just before the conclusion.

The Stock Price: A More Attractive Share Price Is Possible

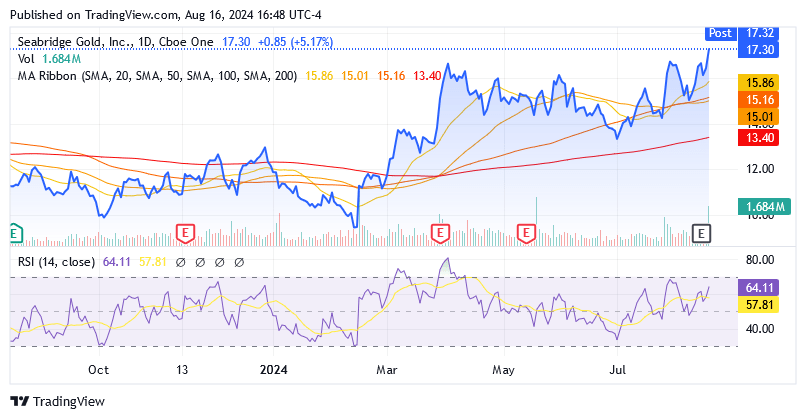

As of this writing, shares under the SA symbol were trading on the NYSE at $17.30 per unit, giving it a market capitalization of $1.48 billion. Shares traded significantly above the MA band, and on August 15, made a new upper limit of the 52-week range of $9.31 to $17.31.

Source: Seeking Alpha

The 14-day RSI of 64.11 suggests that the gap between current and overbought levels is now narrow following the share price's strong uptrend since July. However, as overbought approaches, the likelihood of a healthy pullback is also gaining momentum ahead of promising prospects for the Seabridge portfolio of metallic projects and metal prices.

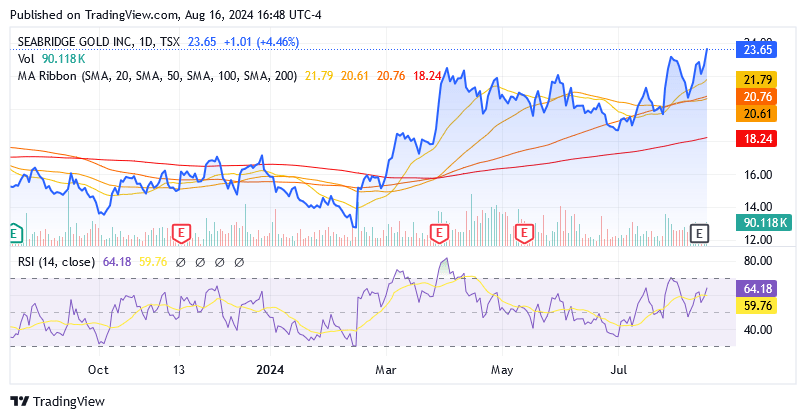

The same considerations apply to shares of Seabridge Gold under the symbol SEA:CA on the TSX: they were trading at CA$23.33/share at the time of writing for a market capitalization of CA$2.03 billion. The shares are trading well above the early July 2024 dip, which is reflected in the higher prices compared to the MA Ribbon. Shares are also very close to the upper limit of the 52-week range of CA$12.62 to CA$23.48.

Source: Seeking Alpha

The 14-day RSI of 64.18 suggests there is plenty of room for SEA:CA shares to pull back from these levels in the near term.

Therefore, the catalysts that caused the price decline in early July 2024 are now expected to return, creating a strong possibility of a new interesting downward move to a price level that is much more attractive to investors who may want to increase their holdings for the long-term positive outlook. More attractive stock prices in both North American stock markets are possible under the following downside conditions:

- Market participants expect the Fed to cut interest rates at its September 18, 2024, meeting, as the chairman had indicated at the July 31 meeting that a policy change could be under discussion. In principle, a lower interest rate is good for metal prices, especially gold, as it lowers the opportunity cost of holding the non-yielding physical yellow metal instead of US Treasuries. A lower interest rate is also good for copper, as lower borrowing costs boost investment in various industrial projects that require copper in bulk, so robust demand for the red metal amid a lack of supply puts upward pressure on the price per pound/ton. But after the rise in the unemployment rate from 4.1% to 4.3%, which caused a temporary sell-off in markets amid panicked investors and traders, market participants now believe the Fed could cut rates not by 25 bps, but by 50 bps, and many believe in such a larger size pivot. But while the 25-basis point rate cut has been widely expected for many weeks now, meaning its event is already factored into the prices of securities, so when the Fed cuts rates by 25 bps, the markets are likely to remain unfazed, the 50-bps scenario is instead losing momentum. As indicated by Fed rate traders, the 50bps rate cut likelihood went significantly down from a 51% chance a week ago to the current 28% chance. Most likely, the Fed will not cut interest rates by 50 basis points because the economy is not developing in a way that a 50-bps cut is needed. This will be a big disappointment to market participants, who were hoping for a bigger cut instead. As for the short-term spillover effect on commodity prices, the effect will be the same (negative) as if there was no rate cut at all, which cannot even be completely ruled out. As persisting high-interest rates do not bode well for gold and copper prices - as has been clearly seen since the Fed began raising interest rates in mid-March 2022 to curb elevated inflation - a much smaller-than-desired rate cut will not bring positivity either. With the Fed cutting rates by 50 bps scenario losing momentum, downward pressure continues to pile up on the horizon, so Seabridge's shares could erupt in a bearish storm when the Fed makes its decision in September. Such a move by the Fed would hurt copper and gold prices and will also have bearish implications for Seabridge shares due to a positive correlation. The positive correlation implies that Seabridge shares and the metal price (copper or gold) move in the same direction: ("both") either up or down, regardless of returns, which can vary significantly between them. A Fed decision that leaves interest rates unchanged at a high level or does not cut rates as much as desired by market participants (they want a 50-bps cut, while they are already accustomed to it already being factored in at 25-bps -reduction) reduces the risk appetite of copper investors and creates a high opportunity cost of holding non-yielding precious metals over US Treasuries that pay interest based on a predetermined rate. With the yellow metal, the rationale may seem more blatant than with copper, so we'll turn to what the recent past can teach us about the relationship between high-interest rates and copper prices: The copper prices faced 2 weeks of declines on Oct. 13, 2023, “as markets remained wary of a higher interest rate environment” that, along with a stronger US$ currency (triggered by high-interest rates), according to analysts at JPMorgan Chase & Co. (JPM), was “the biggest short-term bearish risk for macro-focused copper”.

- But in October 2013, copper markets were in a dodgy mood about risk, also because the “persistent economic challenges in the world’s largest copper consumer, China,” after Chinese property giant Country Garden warned that “its ability to meet offshore debt obligations” was being tested by “significant challenges.” Now the situation is that: While supply side threats ease with the reopening of border gates between Zambia and the world's second-biggest copper producer, the Democratic Republic of Congo, “demand for the base metal in top consumer China is expected to remain muted”, although there are signals from the London Metal Exchange's copper inventories that “the demand decline in China may have bottomed out”, as Arundhati Sarkar, SA News Editor, reported earlier this week. As demand for the base metal in China remains subdued, as China is the largest consumer of copper in the world, global demand for the red metal will also be affected, and as a result of subsequent negative pressure on copper prices, Seabridge shares are expected to experience the same bearish sentiment from time to time giving a chance for more attractive levels in the short term.

- A US recession, fueled by quarters of high inflation to counter through the use of aggressively hawkish interest rate policies by the Fed, could send Seabridge's share price plummeting as the pessimistic sentiment fueled by panicked traders and investors may not initially differentiate between stocks mining or seeking safe-haven gold and the rest of the equity markets. Here, too, the recent past acts as a strong indicator of what could happen again in the future. The deterioration in the employment conditions 2 weeks ago caused panic among market participants, as they suspected clear signs of a US recession. The significant selling activity that followed did not spare gold stocks either. In recent days, the VanEck Gold Miners ETF (GDX), as a benchmark index for the gold stocks industry, was able to compensate for the losses, but in the week leading up to Thursday, August 8, when the markets reached their lowest point “dragged down by the general panic mood on the markets”, according to Commerzbank (OTCPK:CRZBF) (OTCPK:CRZBY) analysts, the leading index of gold companies lost 6.5%. Seabridge was down too, in line with a 24-beta market of 1.47. The Sahm Rule of economist Claudia Sahm and the inverted yield curve indicator (3-month US Treasury yields at 5.22% over 10-year US Treasuries at 3.883%) by economist Campbell Harvey now signal an economic recession in the US. An expected significant setback in Seabridge's share price due to recession fears leading to the formation of a dip for a buying opportunity in the near term could also happen through the bearish pressure that the deterioration of the cycle will create on the copper price. A worsening of the economic cycle is likely to be associated with a slowdown in the consumption of base metal products and lower investment in industrial projects, suggesting weaker demand for copper going forward, but in the short-term investors will wonder whether a healthy pullback in copper prices is in order, and that is sufficient to create short-term negative pressure on the pound.

A Low Liquidity Stock

The stock is characterized by the following daily trading volumes in both markets, which are low volumes: Over the past 3 months, an average of 461,353 shares have traded on the NYSE market (scroll down on this Seeking Alpha page to the "Trading Data" section), while on the TSX, an average of 57,205 shares changed hands (scroll down this Seeking Alpha page to the "Trading Data" section).

The stock of Seabridge Gold has 89.49 million shares outstanding, while a total of 80.63 million shares make up the float, which is freely tradable on the stock exchanges' open market, and institutions own 55.07% of the float.

The stock is characterized by low trading volume, and investors should be aware of the consequences, as if they build up too large a position, it may be difficult to adjust it quickly when circumstances require it.

Latest Developments in the Project Portfolio of Seabridge

The Kerr-Sulphurets-Mitchell Acquires “SSD” Certificate

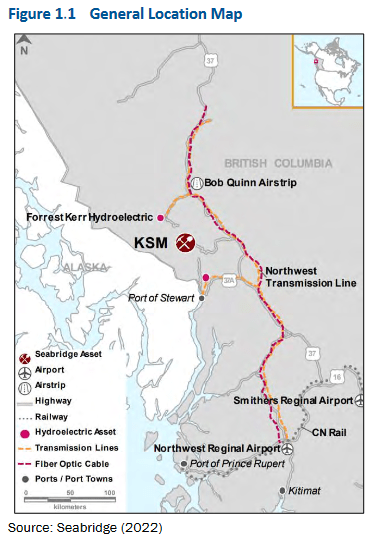

Regarding the projects, on July 26, 2024, Seabridge received from the Government of British Columbia “Substantially Started Designation” for its 100% owned The Kerr-Sulphurets-Mitchell (hereafter “KSM”), boosting the potential for a highly profitable multi-year (≈ 33 years mine life) gold and copper mining site, as the environmental permit has no longer expiry limits.

Seabridge Gold Inc.: 2022 PreFeasibility Study

This recognition by the Minister of Environment and Climate Change of the Canadian province of British Columbia of the significance of the more than US$997 million invested by Seabridge with patience since taking over the project in 2001 represents a significant step forward in "de-risking" the entire project. This is positive for KSM's profile, which is already characterized by the existence of important infrastructure in the region (highways, power grids, ports, airports and telecommunications lines) and the Canadian province's friendly jurisdiction and scenario for mining and exploration activities, as evidenced by the minimal risk (light blue area) assigned to the region by the Sprott ESG Mining Risk Heat Map 2024. The Substantially Started Designation status strengthens the profile of the KSM project and gives it an even better chance of obtaining the necessary funding once credit conditions become more favorable in light of the expected U-turn by the US Federal Reserve at its September meeting. This scenario could now attract the interest of large gold producers looking for new ounces as mineral resources continue to deplete and these must also be sustainable from an economic, environmental and risk respective. Now, operators must adapt to global targets to reduce carbon emissions and environmental impact. In Canada, the KSM project is located in one of the friendliest regions in the world for mining and mineral exploration activities, which bodes well for Seabridge given rising geopolitical tensions and “de-risking” strategies being implemented by Western economies in the non-Western world.

KSM’s Financial Analysis With Higher Gold Ounce Production

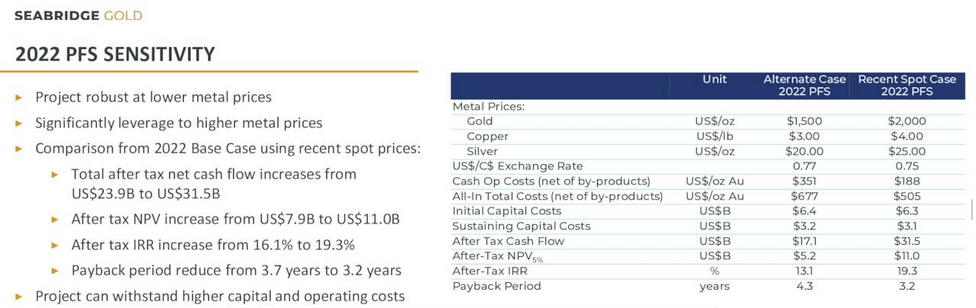

The PFS 2022 financial analysis offers the following parameters. Before listing these, this analysis believes it is useful to say that compared to the financial analysis in PEA 2022 with its expanded copper scenario, the PFS 2022 economic analysis has as a primary commodity producing income, a key share price driver, the yellow metal. Just as it is with the yellow metal that the market has this stock more immediately associated due to the presence of “gold” in the company name, “Seabridge Gold”, there is a chance that the financial analysis of 2022 PFS will have a greater impact on the market for Seabridge shares than the economic analysis of the 2022 PEA. The 2022 PFS economic analysis states that at a gold price of $2,000/oz, a level much closer to the current spot price per ounce of gold than the alternative case of a long-past average gold price of $1,500/oz, KSM will recoup its initial investment (including the billion dollars already spent since 2001) in 3.2 years upon commissioning of the mine and KSM will produce the metal at an all-in cost (net of by-product credits) of $505 per ounce.

Seabridge Gold Inc.: Corporate Presentation

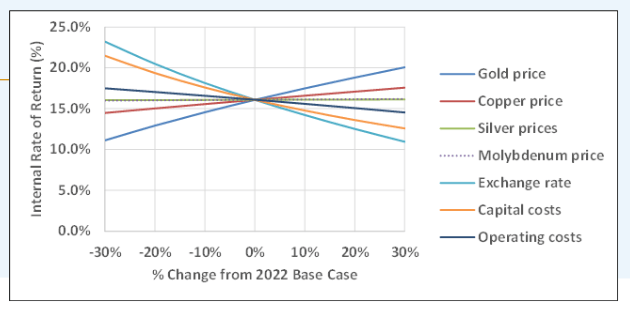

Assuming commodity prices remain very supportive, from a cost perspective, KSM will be a low-cost producing metal mine, increasing the chances of the payback period being met, as S&P Global Market Intelligence indicated in March 2024 that the weighted average of miners' all-in sustaining costs (AISC) was $1,345 per ounce of gold, and the median AISC was $1,328/oz in Q4-2023 for miners with production above 500,000 ounces in 2023. Furthermore, the after-tax internal rate of return (IRR) of 19.3% is compelling considering that other projects we have previously looked at have been described as solidly profitable in various company presentations with after-tax IRRs of 15-35%.

The IRR is also very sensitive to rising metal prices and with these all set to generally remain on the uptrend over the coming years, larger operators may feel more inclined to enter into talks with Seabridge about KSM given the improved profitability outlook, as reflected in the rising IRR.

Seabridge Gold Inc. - Corporate Presentation

Potentially Well-Known, Established Gold Operators Will Seek Joint Ventures for KSM

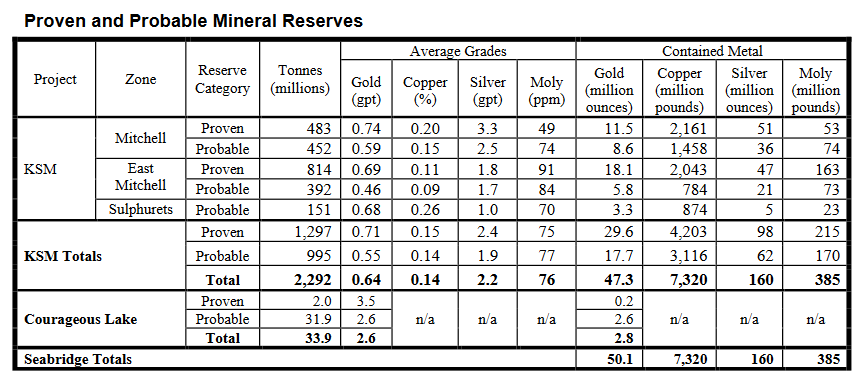

These operators could potentially enter into joint venture discussions with Seabridge and therefore there is real growth potential for the stock. Objectively speaking, KSM is the flagship development project as it practically accounts for Seabridge Gold's total resources that can be estimated with a high degree of reliability and based on the 2022 PEA expanding the scenario designed in the 2022 PFS, there is a potential for 33 years of production: estimates on future volumes are impressive, more than a million ounces of gold plus 178 million pounds of copper and 3 million ounces of silver per year. Thirty-three (33) years is based on what is known today, namely proven and probable reserves of 50.1 million ounces of gold (these expanded from 47.3 million oz as of previous analysis), 160 million ounces of silver and 7.3 billion pounds of copper.

Seabridge Gold Inc.: Company Estimates of Resources (Seabridge Gold Inc.: Company Estimates of Resources)

However, since these mineral resources do not represent more than 30% of KSM's total measured, indicated and inferred mineral resources, the potential for further development is gigantic and thus qualifies KSM not only for “multi-year” mining but also for “multi-generational” production of gold and copper. In addition to KSM's attractive growth prospects in the development of this multi-metal project, a strong upward trend in copper and gold prices is forecast for the future supporting these estimates: KSM's after-tax net present value (NPV) discounted at 5% is $11 billion, or $122.92 per share (CA$168.58 per share, as of this writing), with 89.49 million shares outstanding. There is plenty of room to grow from the current share price, but the number of shares outstanding could be larger in the future following the issuance of new shares to fund the project.

Long-Term Outlook for Copper and Gold to Support KSM

Copper will be critical to energy transition programs, electrification and AI data centers, as well as electric vehicles and batteries, the arms race amid heightened uncertainty and tensions between global geopolitical forces. These market needs, according to hedge fund manager Pierre Andurand in an interview with the Financial Times, will create such robust copper demand in the future that by exceeding supply, “copper prices will quadruple” to $40,000/ton (≈$18.14/lb) already in the current decade. The copper price is at around $4.12/lb as of this writing. Gold's long-term outlook is very robust as a hedge against headwinds due to geopolitical tensions and economic growth uncertainty as a result of central banks' implementation of aggressive monetary policies or certain government fiscal policies. As for the geopolitical tensions, these seem to be issues that will continue for a long time when the current global situation is scrutinized. In terms of long-term gold price forecasts, BMI, a subsidiary of Fitch Solutions, “expects gold prices to remain high in the coming years compared to pre-Covid levels” when an ounce was below $1,600. At the time of writing, the gold spot price or XAUUSD:CUR was around $2,473 an ounce.

KSM Gains Momentum as Fed Pivot Moves Closer

The above scenario gained further momentum after the publication of Wednesday's new inflation figures: although Wednesday's consumer price index did not reveal any major surprises with a slight slowdown in annual inflation to 2.9% and in the core interest rate to 3.2%, since these were the lowest readings since March and April 2021, respectively, the report was the “green light” for the Fed to cut interest rates in September. Wednesday's consumer price index report is another contribution to the cooling inflationary pressures that Fed Chairman Jerome Powell and the central bank expect: It is confirmation that the restrictive interest rate policy is finally paying off after an uneven start to the year with rising inflation.

Seabridge Continues to Carry Out Relevant Drilling Decisions: Updates on the Iskut and 3 Aces projects

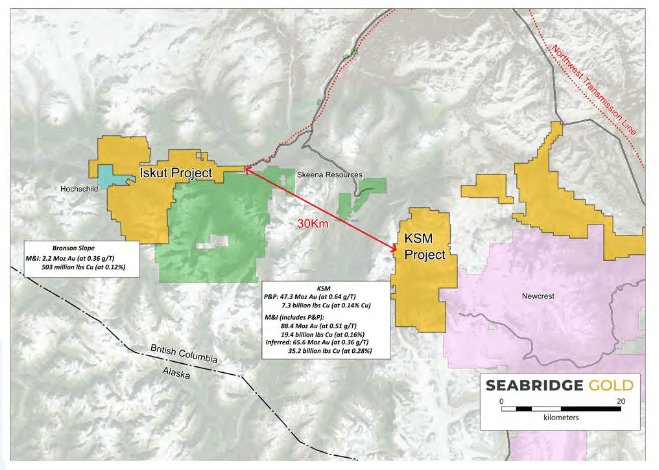

a) on the porphyry copper-gold mineralized intrusion on its 100% owned Iskut Project, which covers an area of 294 km2, ≈ 30 air km from KSM. Here, exploration activities, which will require ≈ 15,000 meters of core drilling this year at a budgeted cost of $12 million (vs. $45.1 million net working capital as of June 30, 2024), confirm Seabridge's suspicions of a district-wide structural trend, as they are unearthing that the “Iskut intrusion is similar in width and depth to the nearby KSM deposits”, Seabridge Chairman and CEO Rudi Fronk said on May 30, 2024.

Seabridge Gold Inc.: Corporate Presentation

Driven by the belief in the existence of an intrusive copper and gold-bearing porphyry system, the team wants to build the mineral resource from the “Bronson Slope resource”. For this Bronson Slope asset, earlier core drilling was also done by other operators and subsequently by Seabridge after the asset acquisition in 2016. It has inferred mineral resources as follows: 517.3 million tonnes of mineral grading 0.33 grams of gold per tonne of mineral (g/t), 0.09% copper and 2.7 g/t silver, leading to 5.4 million ounces of gold, 1,057 million pounds of copper and 45 million silver ounces.

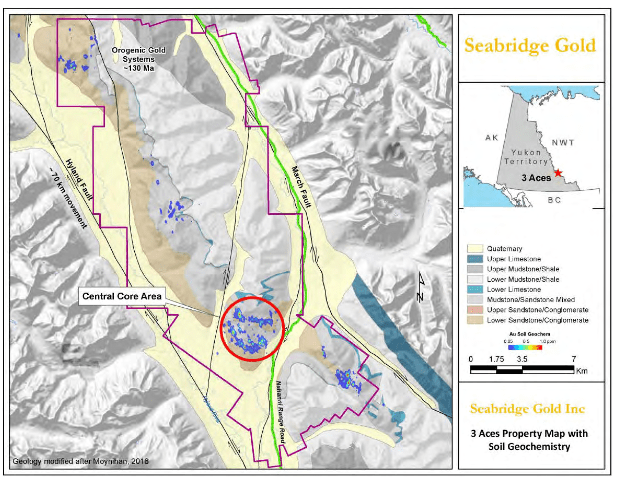

b) A drilling program was advanced on The 3 Aces Project a Canadian 357 km2 property in the southwestern Yukon Territory, targeting resource delineation as the potential for high-grade mineralized deposits challenges the curiosity of the exploration team and markets.

Seabridge Gold Inc.: Corporate Presentation

The company is evaluating historical prospects outside of the known mineralized zones in the central core area (CCA) of The 3 Aces Project because Seabridge believes that similar characteristics of gold-bearing zones to the CCA are also present in the rest of the property. Therefore, in addition to resource delineation with share price upside potential from its estimates in the coming months, the company is now also looking to expand the scope of 3 Aces' growth opportunities. The market has now been alerted that new target opportunities beyond the CCA may be communicated and the further away from the CCA these are identified, the more likely they are to help create an environment where share prices tend to rise on mineral successes. The expert team is studying certain sedimentary formations, so-called “second-order folds” of the CCA because if their limbs contain gold ore from at least a minimum level of mineral occurrence as a parameter, then according to a prediction model there should also be gold far beyond the CCA. This is a predictive model that takes into account the results of past exploration activities conducted near 3 Aces and around the world on orogenic gold deposits that 3 Aces is believed to share characteristics of sedimentary formation in its CCA and beyond. Several zones contain gold mineralization with peaks of high-grade yellow metal in either sedimentary rocks or arsenical ores, the company indicated, and therefore, as the study shows consistency with projections supporting the scenario just described, the yellow metal is likely to occur well beyond the CCA. The results of this investigation, according to the company, are expected shortly and with such premises, could have a very positive impact on Seabridge's share price.

Other Projects

Seabridge has a 100% interest in other North American gold projects, including the Courageous Lake project located 240 km northeast of Yellowknife in Canada's Northwest Territories and the Snowstorm project in the Getchell Gold Belt in northern Nevada.

The Courageous Lake project hosts approximately 11 million ounces of gold measured and indicated resources at an average grade of 2.36 grams of metal per ton of mineral, but with large margins for improvement through further explorations.

The Snowstorm project is believed to have the potential to host large mines as it is located on a 103 km² property directly at the intersection of three major Nevada gold belts and near the Nevada Gold Mine's Barrick Gold Corporation (GOLD) (ABX:CA) and Newmont Corporation (NEM) (NGT:CA) JV Twin Creeks mine and JV Turquoise Ridge mine.

Meanwhile, not much has happened with these two projects, so for more information refer to the previous analysis.

Upward Long-Term Potential From Copper and Gold Prices

First, “the onset of interest rate cuts in the major economies,” including the next one in the US most likely in September, raises the possibility of a higher copper price, which "could reach $12,000/ton" (≈ $5.44/lb), according to Citigroup Inc. (C). This copper price forecast, which is up 32.3% from the current $4.1156/lb (as of this writing), bodes well for Seabridge's share price expectations. Trading Economics' analysts forecast copper to trade at $4.14/lb by the end of this quarter, and an uptrend to $4.35/lb in 12 months’ time.

Second, the price of copper will receive incredible support from the long-term outlook for copper demand, which is very promising as the red metal is essential for energy transition programs, electrification and AI data centers. As well as for electric vehicles and batteries, the arms race amid heightened uncertainty and tensions between global geopolitical forces. The supply of red metal is instead seen to remain too short to satisfy the market's needs. As a result of the combination of supply and demand factors, hedge fund manager Pierre Andurand indicated in an interview with the Financial Times that “copper prices will quadruple” to $40,000/tonne (≈$18.14/lb) in the next few years.

About the gold price: Helped by central bank purchases, especially Asian consumers, amid the current challenging economic climate and geopolitical tensions as well as expectations of Fed rate cuts, according to ING Groep N.V. (ING) commodity strategist Ewa Manthey, “gold will maintain its upward momentum.” Manthey predicted a gold price averaging $2,380/oz in Q3 and a peak at $2,450/oz in the final quarter of 2024, for an annual average of $2,301 for the entire year of 2024. At the time of writing, the gold spot price or XAUUSD:CUR was at $2,472.31 per ounce thus going beyond ING’s forecasts. Analysts at Trading Economics forecast that the price of gold will end this quarter at $2,464.46 per ounce and in 12 months at $2,549.74.

Recently, these upside factors for gold lifted Seabridge's share price to a record high of $16.98/apiece for SA shares (CA$23.48 apiece for SEA:CA shares) intraday on July 30-31, which coincided with the upper bound of the 52-week range of $9.31 to $16.98/share (CA$12.62 to CA$23.48/share).

Shares were led higher by “gold prices back above the psychologically important $2,400/oz level,” reported Carl Surran, Seeking Alpha News Editor, which hit a new record high.

Conclusion

Seabridge Gold Inc. shares get another “Hold” rating because growth prospects are very attractive following certain milestone developments in the KSM and 3 Aces projects, but shares are now trading high relative to recent trends and should pull back healthily before they start building in market valuation again.

Three negative catalysts in the short term can cause a dip in the share price.

The future looks bright for Seabridge as rising gold and copper prices are expected to benefit Seabridge Gold's metal projects, but the company's extensive and largely unexplored resources and the potential for these to gain momentum across all properties also provide a fantastic upside catalyst.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.