Powell Likely To Disappoint Market At The Jackson Hole Speech

Summary

- Fed Chair Powell might not signal an imminent monetary policy easing cycle with the first cut in September, as the market expects.

- The bond market is pricing an imminent recession, but the Fed still needs more (negative) data to start cutting interest rates.

- Ultimately, the S&P 500 is facing a recessionary bear market, which is already priced in the bond market.

Nathan Howard

The Jackson Hole Symposium

Fed Chair Jerome Powell will speak at the Fed's Jackson Hole Economic Policy Symposium on Friday. He is widely expected to signal the beginning of the monetary policy easing cycle, with the first cut likely at the next FOMC meeting in September.

The Fed's 2024 Jackson Hole Economic Policy Symposium is titled “Reassessing the Effectiveness and Transmission of Monetary Policy,” and will be held Aug. 22-24. This is an academic conference, but the Fed's Chair keynote speech has been used historically to lay out the monetary policy objectives over the near term — and this is closely followed by investors.

The monetary policy expectations

The market expects the Fed to start with the monetary policy easing cycle in September, based on the Federal Funds futures.

Specifically, the market participants believe that:

- The Fed will have the first interest rate cut at the next FOMC meeting in September, and it will be a 25bpt cut, although there is a small probability assigned to a 50bpt cut.

- The Fed will cut at each meeting left in 2024, for the total of 75bpt, from the current federal Funds rate level of 5.33% to 4.6%.

- The Fed will keep cutting interest rates in 2025 down to 3.27% by December 2025

The market expects a recession

The market expectations for monetary policy reflect a fear of an imminent recession — the Fed historically cuts interest rates over a longer period of time and by 2% or more only during recessions.

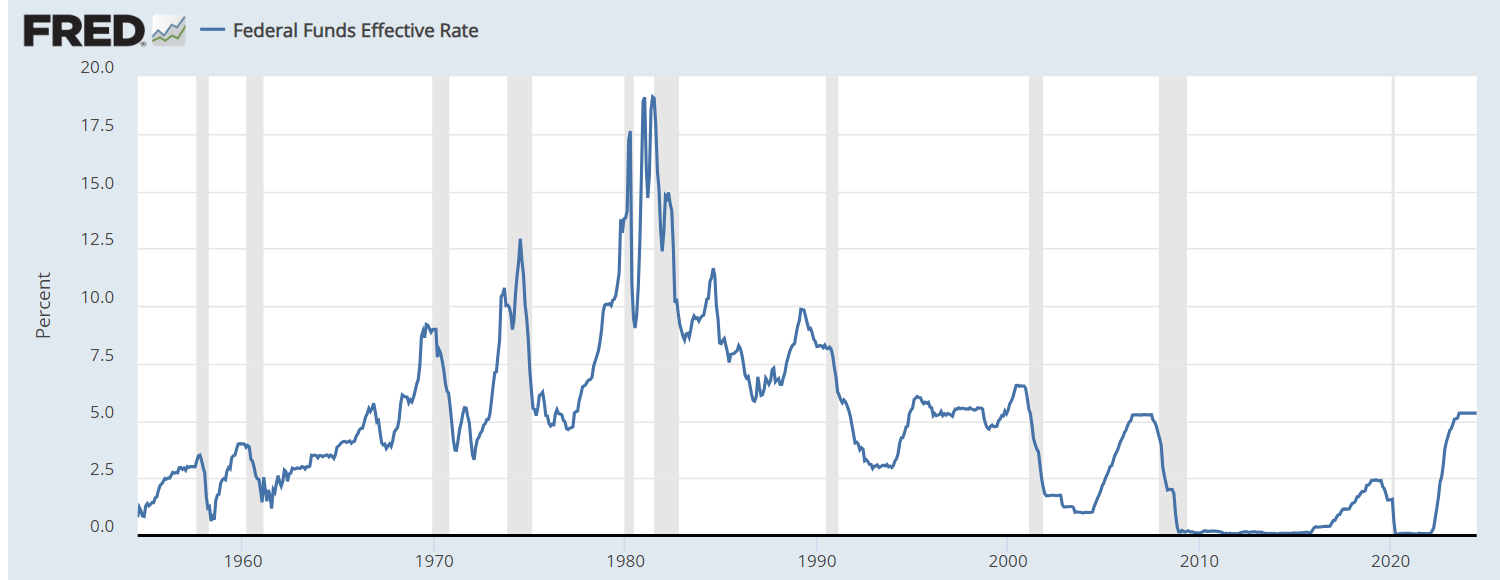

Here is the chart of the Effective Federal Funds rate. If the Fed actually cuts from 5.33% to 3.27% over the next 12–16 months, it would be due to a recession, based on historical evidence.

Many market participants still believe in the soft-landing scenario, or even a no landing scenario, where inflation falls, but growth remains positive, which would allow the Fed to normalize interest rates.

The soft-landing crowd references the 1995 case, where the Fed's hiking cycle did not cause a recession, and the Fed was able to subsequently cut interest rates. The Federal Funds rate peaked at 6% in April 1995, and the Fed was able to cut to 5.25% by February 1996, and then hike by 25bpt in April 1997. The Fed was “normalizing” interest rates in the mid-1990s.

The market now expects a recessionary monetary policy easing cycle, with at least 2% in cuts over the next 12–16 months, and that's inconsistent with the 1995 case.

FRED

What is Powell expected to say at Jackson Hole?

Thus, the market expects that Powell will signal that the Fed is about to start with the monetary policy easing cycle, and specifically that the policy focus is shifting from inflation to the weakening labor market.

In other words, the market expects that Powell will state that inflation is sustainably returning to the 2% target, but the labor market is weakening to the point where the risks of a recession are significantly rising.

The labor market situation

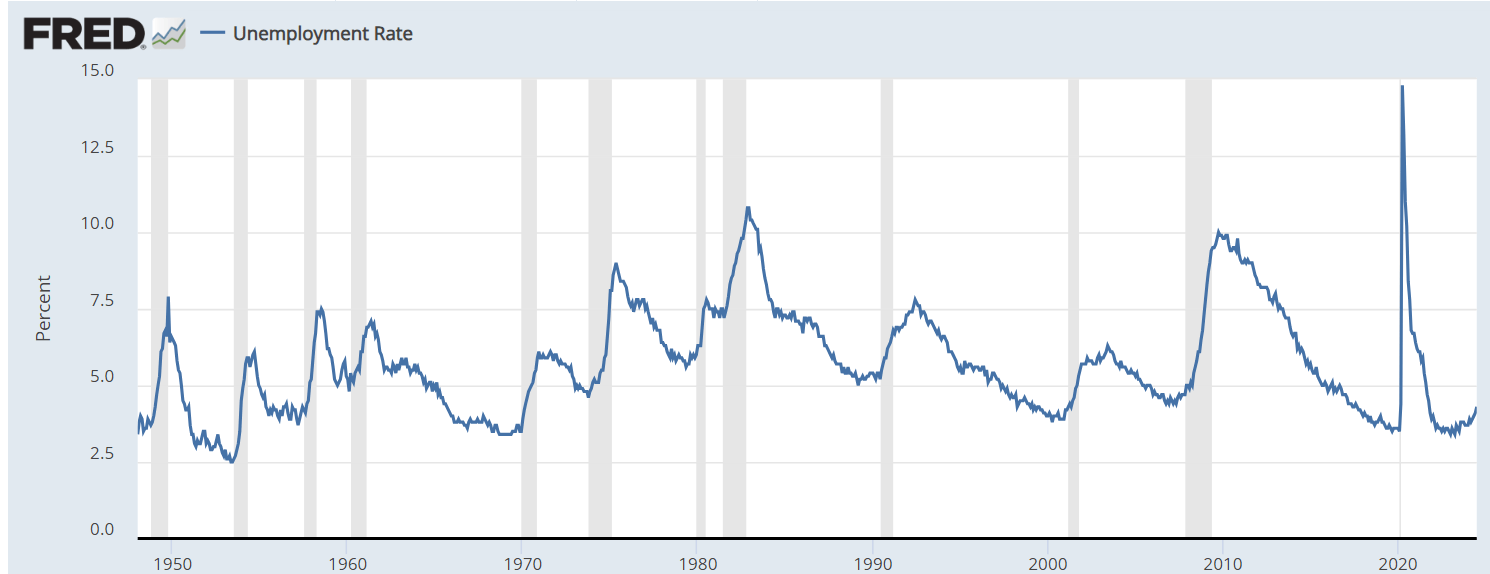

The recession fears have been triggered by the increase in the unemployment rate in July to 4.3%, which triggered the Sahm Recession Rule — the recession usually starts when the unemployment rate increases by 0.5% from the 12-month low level, using the 3-month averages. The current Sahm Indicator value is at 0.53%, which suggests that the recession is imminent.

However, the unemployment rate at 4.3% is still very low by historical standards, and still reflects full employment. The unemployment rate in 1995 was 5.5%, and it decreased to 3.9% by October 2000, before the recession started. Thus, the Fed was able to normalize interest rates in 1995 as there was still slack in the labor market. In the current situation, there is no slack in the labor market, and a recession appears necessary — but not obvious yet.

FRED

Similarly, the initial claims for unemployment have been rising lately, but the current level of 225-250K is also still very low by historical standards.

Thus, Powell is unlikely to say that the labor market is weak.

- The unemployment rate of 4.3% is still very low.

- The initial claims at sub 250K are still very low.

In fact, Powell already dismissed the Sahm rule as a statistical regularity. Powell has stated that the recent increase in the unemployment rate is due to the increase in the labor force — due to immigration and an increase in participation, and this is supported by the data:

- The civilian labor force increased by 1.316M over the last 12 months, while

- the number of employed individuals increased by 57K.

So, the number of unemployed people increases due to increase in the labor force, as no jobs were lost over the last 12 months. That's the Fed's view on the labor market.

The point is that Powell might not signal that the Fed is worried about the labor market yet, as the market expects.

The inflation situation

The annualized quarterly inflation is down to 2% already, as the inflation readings over the last three months have been low. Thus, Powell will be more positive on inflation.

However, there are two problems with inflation:

- Most of the inflation now is due to the rise in shelter inflation, which increased by 0.4% in July, after increasing 0.2% in June. So, shelter inflation is not moderating yet. Shelter inflation is correlated with the housing market, and the housing prices are still rising. The Fed might need to burst the housing bubble before declaring a victory on inflation.

- Supply side inflation due to the unfolding trend of deglobalization, with the escalating geopolitical situation. Deglobalization is inflationary due to the supply chain disruptions, and commodity price spikes. The escalating geopolitical situation in the Middle East could produce the spike in the price of oil, which could interfere with the expected monetary policy easing.

However, Powell is likely to say that the Fed is getting more confident that inflation is falling towards the 2% level, although he might not declare victory over inflation yet — which might not provide the clear signal for the September cut.

Implications

Based on the Federal Funds futures, market participants are pricing the recessionary-like monetary policy easing, starting in September and the Fed Chair Powell is expected to signal the first cut in September at the Jackson Hole.

However, Powell's speech is likely to be more hawkish than the market expects. The labor market is weakening, but it's still very tight. Inflation is falling, but it's still very high at 2.9% headline CPI, and shelter inflation is not moderating yet, while the supply side inflation remains a risk.

In addition, the Fed might be hesitant to signal a clear-cut in September, right before the election in November.

Thus, the stock market could get disappointed, and the interest rates could rise in response to Powell's speech.

However, Powell is likely to emphasize that the Fed is data-dependent, and, in my opinion, the economic data is likely to continue to deteriorate as the recession becomes more obvious.

Ultimately, the S&P 500 (SP500) is facing a recessionary bear market, which is already priced by the bond market. In this situation, investors should reduce their exposure to the stock market, and increase exposure to Treasuries (SHY), which still give a decent yield across different maturities.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.