Iris Energy: A Potential Buy But Questions Remain

Summary

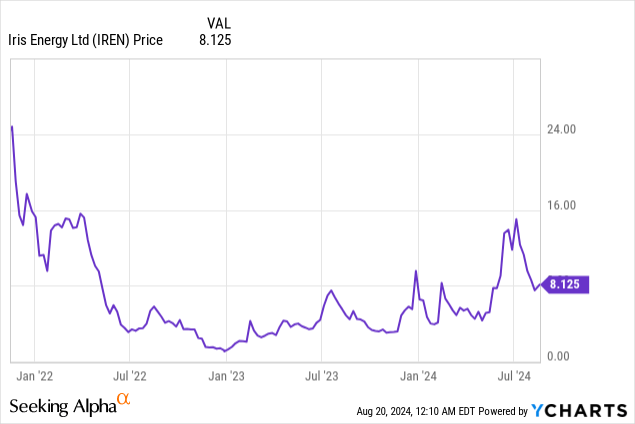

- Iris Energy is a Bitcoin miner diversified into HPC, trading at $8, well below its peak of $15.

- Post-halving performance saw a decline in coins mined also due to lower subsidies, planned maintenance, and technical issues while electricity prices surged.

- Additionally, lower digital asset prices impacted profitability in July.

- Iris' aggressive expansion strategy into HPC requires significant capital, raising questions about sustainability, especially given this is being done through share dilution.

- With no debt, this is a potential buy but subject to providing further update on electricity prices on mining operations and sustainable financing for HPC diversification.

bestofgreenscreen/iStock via Getty Images

If you are looking for a Bitcoin miner to invest in that is also diversified into HPC or High-Performance Computing through its AI cloud service business, Iris Energy (NASDAQ:NASDAQ:IREN) springs to mind. It is benefiting from the current shortage in the data center space to accommodate the accelerated computing GPUs produced by Nvidia (NASDAQ:NVDA) and trading at around $8 which is well below its July peak of $15 as shown below.

Data by YCharts

Data by YCharts

However, since both diversification into AI infrastructure and its aggressive expansion of Bitcoin mining cost a lot of money, this thesis aims to show that while the potential is immense, its financing strategy may be unsustainable. For this purpose, a comparison with another miner is useful.

First, I assess its performance during the post-halving era which has seen miners obtaining only 3.125 BTC as rewards (subsidies) for each block added to the blockchain compared to 6.25 BTC before April 19.

The Post-halving Performance

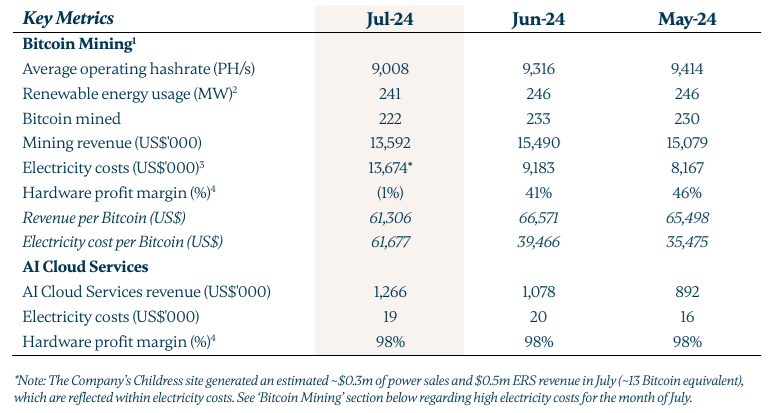

It released its mining update two weeks back. This showed the number of coins mined decreased to 241 in July from 246 in June due to the combined effect of a reduction in block subsidy and increasing mining difficulty. Also, unlike in June when the average increase in operating hash rate of 14% managed to offset the negative impact of halving and resulted in the production of 246 coins, there was a decline in production capacity last month, leading to fewer Bitcoins produced.

The decline was also attributed to planned outages in the context of power substation upgrades and energization of expansion projects, exacerbated by technical problems on a fleet of T21 mining rigs (equipment) whose faulty parts were being replaced by supplier Bitmain according to the corporate update.

Company presentation (irisenergy.gcs-web.com)

Additionally, with digital asset price falling to $61.3K compared to $66.6K one month earlier as shown above, mining revenues for July dropped to $13.6 million. Worst, the electricity consumed to produce one Bitcoin jumped from $39.5K to $61.7K in July, or by 56% causing the hardware profit margin to become negative, or -1% as shown above.

Thus, in addition to supply, problems cropped up on the demand side impacting profitability.

Focusing on Profitability

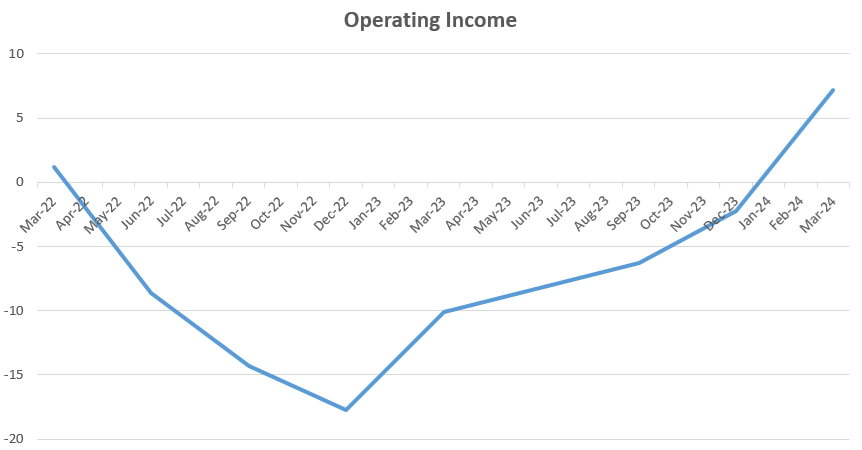

Thinking aloud, items like planned outages or technical problems are temporary and unlikely to be sustained over the long term. Also, the company recorded profit margins of 41% and 46% in June and May respectively and electricity costs per BTC were only $19.6K in April meaning profits for the fourth quarter of fiscal 2024, (or 34-2024 lasting from April to June) which should add momentum to the profitability drive after Iris broke even in 3Q-2024 as charted below.

Income Statement (seekingalpha.com)

Furthermore, BTC prices have partly recovered which means that in the future, higher sales can also support profits. This recovery could be helped by a potential rate cut by the Federal Reserve in September which would lower miners' financing costs and motivate them to HODL more coins instead of selling them on the open market, thereby alleviating the pressure on digital asset prices.

However, electricity costs may remain elevated, and investigating the reason for the 56% increase in electricity consumed per BTC which drastically increased the operating costs, the corporate update mentions that this was due to “higher energy hedge pricing” in the summer month at the Childress site. This is in sharp contrast to last year when the company benefited from net negative electricity costs of 8 cents per KWh which translated into $2.3 million of power credits. This was not possible this time due to lower-than-expected energy market volatility. Now, since summer lasts till September, profits for the first quarter of fiscal 2025 (1Q-2025) which started in July may suffer.

Looking further, another company that has PPAs or power purchase agreements with electricity providers in Texas is Riot Platforms (RIOT). Now, because of peak summer demand when domestic consumption like air conditioning receives priority, the company curtailed production in June which allows it to make substantial savings in the form of power credits.

Aggressively Expanding Mining Operations While Diversifying into HPC

Now, these two miners have different power agreements, but the fact that Iris is reassessing its future energy pricing structure points to the possibility that there is a need to adjust to new market dynamics to lower energy costs. Another factor that should reduce operating costs is the new mining fleet consuming less energy per Tera hash of production capacity, or by 29% from 24 J/TH to 17 J/TH when it is completed in the 4Q-2024. In so doing, its production capacity will amount to 30 EH/s or more than a fourfold increase from the 9 EH/s in July.

Now, this seems an aggressive expansion strategy that will certainly see it boost Bitcoin production to above pre-halving levels but the problem is that it will also require a lot of capital without forgetting the investments to drive HPC diversification.

Focusing on HPC diversification, this is an opportunity for Bitcoin miners who have been under a lot of pressure to add renewables to their energy mix because of the amount of power they consume. Consequently, they ventured into the regions of the country like Texas where energy sources in the form of wind, solar of natural gas are abundant, and electricity tariffs are low. Since energy is crucial for powering data centers and there is currently a shortage of what can be provided by conventional collocation providers, HPC represents an opportunity.

As for Iris, it has an agreement with Poolside.ai, a Paris-based generative AI company whose latest fundraising valued it at $2 billion and is building a large language model specialized in software development. The initial agreement included the lease of 248 H100 GPUs to Poolside for three months, which Iris purchased from Nvidia and energized at its facilities. This was recently upsized to 504 GPUs covering an additional 4 months plus there is an option to extend for a further 2 months by the customer.

The process which consists of buying accelerated compute and leasing them directly to the software company is synonymous with operating as a vertically integrated platform and differentiates it from Core Scientific (CORZ) which instead leases data center space together with the power to CoreWeave, an AI hyperscaler that bears the costs of the GPUs.

Thus, operating as an AI infrastructure-as-a-service provider signifying it leases both the GPUs, the data center space, and the electricity directly to the client, Iris boasts a more profitable AI Cloud Services business with a gross margin of 95% compared to only 11% for Core Scientific which merely leases space and power.

On the other hand, Iris has to spend much more than because of the upfront Capex. Thus as a result of spending capital on transforming its data centers to become AI-ready and purchasing GPUs, it spent $119 million in 3Q-2024 alone. This more than offset its cash from operations of $26.6 million which the company obtains by selling all the Bitcoins it mines, in contrast to other miners who tend to HODL a portion. To provide investors with a sense of the amount spent, Iris spent four times more on capex than Core Scientific during the trailing twelve months. Moreover, as a result of spending more money than it generates, it has been regularly raising equity, with $257.1 million during the March quarter alone.

Higher Margin AI Cloud Service Business but Requiring Significant Investments

This means share dilution and also raises the question of return on investment and sustainability of such a financing model. In contrast, Core Scientific has opted for a more capital-light strategy to invest in AI infrastructure consisting of a 12-year lease agreement with CoreWeave where the latter finances the cost of GPUs together with the transformation work required to revamp facilities to accommodate GPUs.

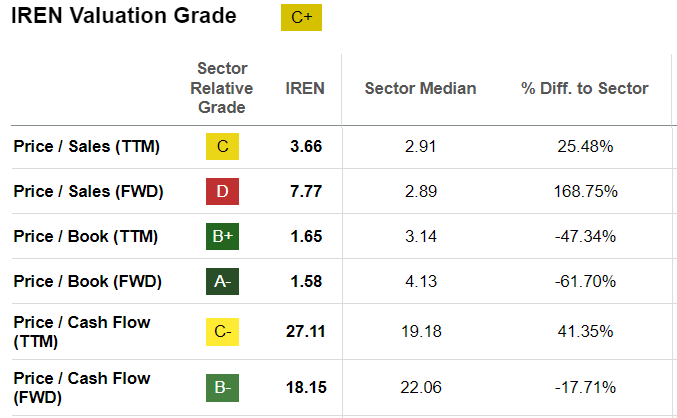

Consequently, while Iris may have no debt and the company remains undervalued on a forward price-to-cash flow basis, it is not the right time to buy. To this end, the company can generate more money as a result of mining more coins and leasing more GPUs but the problem is these are getting eaten up by investments made and also come at the expense of stock dilution. Therefore, in this case, the P/CF ratio has certain limitations as it does not encompass all parameters that determine Iris' value.

seekingalpha.com

In these circumstances, till clarification is obtained on the energy pricing structure which will determine operating margins for mining operations, and how it intends to continue financing expansion for AI cloud, Iris is not a buy.

On the other hand, I am not bearish on the stock.

The reason is as Nvidia sells billions of dollars worth of GPUs every quarter which need to be hosted and energized in data centers before being used to design super-smart applications, there should be demand for HPC infrastructure, and miners that rapidly take advantage of the opportunity should profit. In this case, Iris' AI cloud service business is highly profitable, and another advantage is its vertically integrated platform, which means that it can deal directly with the customer (instead of acting more like a middleman) especially when it comes to rapidly responding to customer demand. For this purpose, it has recruited a team of engineers.

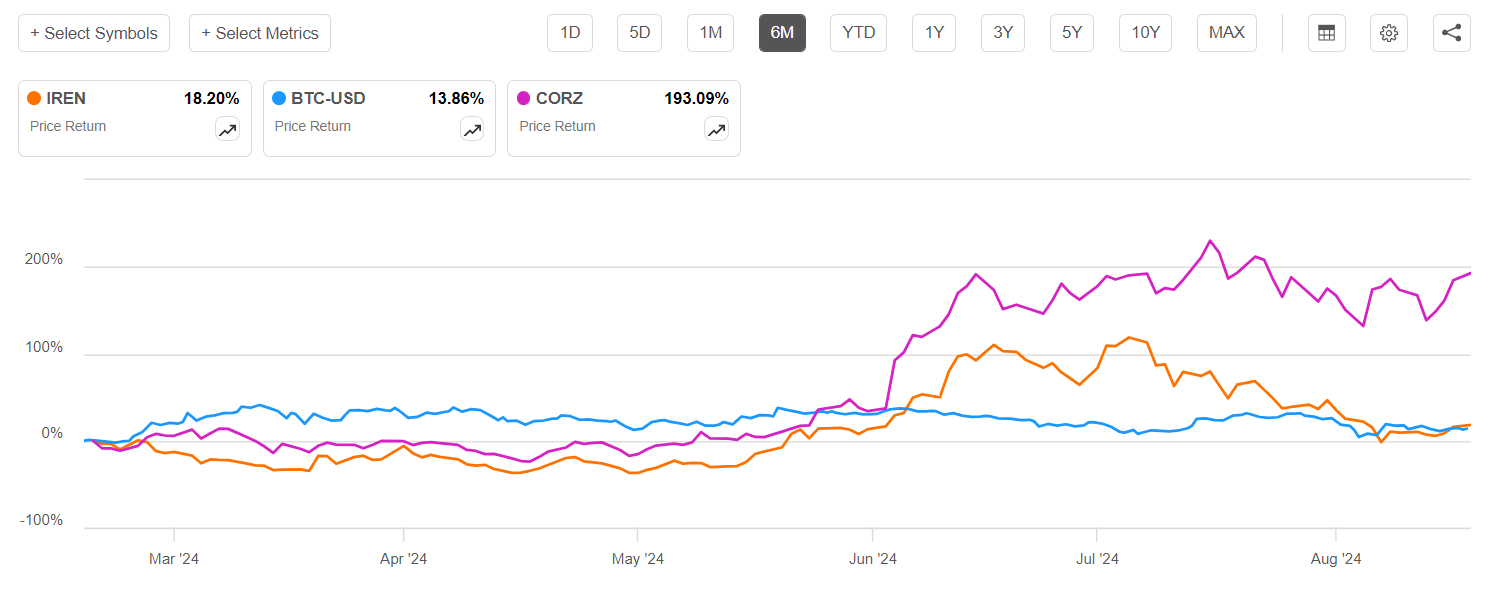

Now, Iris and Core Scientific do not have the same business model nor the same HPC diversification strategy, but, still, unless it signs a multi-year agreement with a software company or provides more clarification as to the viability of the financing structure to scale the AI cloud service business, more risk-aware investors may avoid the stock. To justify my cautious stance, a comparison with Core Scientific shows that after enjoying investors' enthusiasm from April after it upsized the agreement with Poolside.ai, the stock has slid and is now moving in tandem with BTC. Thus, Iris appears to have lost its HPC appeal.

Comparing the price performances (seekingalpha.com)

Finally, with the price of Bitcoin rising again to above the $61K level from its dip to below $55K, the stock has appreciated and could receive a further boost in case the Federal Reserve cuts rates in September as a majority of market participants are expecting. As a result, the company could borrow at more favorable rates, but until an update is obtained on electricity prices and AI financing, a sustained upside is not likely.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.