6 Reasons Philip Morris Is On The Up And Up

Summary

- While big tobacco stocks have all seen significant increases in the past six months, Philip Morris stands out with a 32% rise.

- Market uncertainty and a rotation towards undervalued stocks have contributed to the growth of tobacco stocks. The company's healthy financials, particularly in its smoke-free business, are a big plus too.

- An earnings upgrade is positive for its dividends too. Even as a short-term price dip looks likely, PM is a good buy for passive returns over the years.

Baloncici

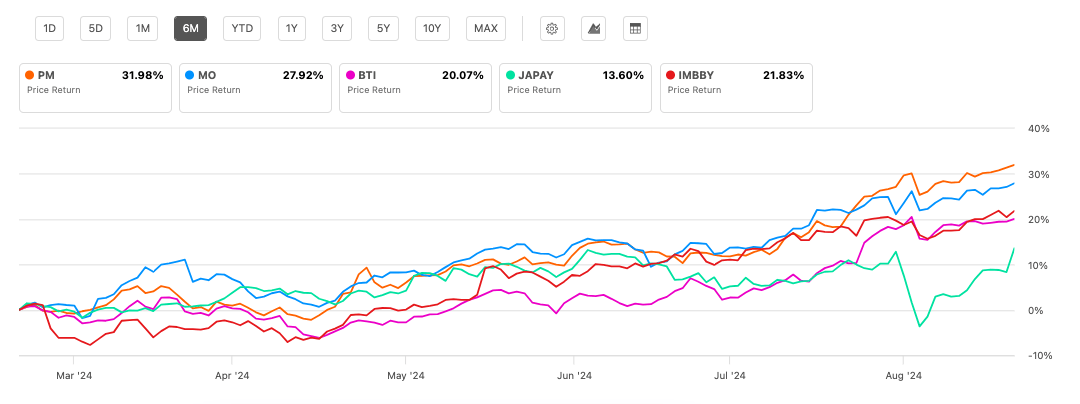

The past half year has been exceptional for tobacco stocks, with the biggest five by market capitalization ("MCap") seeing double-digit increases (see chart below). But Philip Morris (NYSE:PM) stands out even among them, seeing the biggest increase, of 32%, over this time.

Price Returns, Biggest 5 Tobacco Stocks By Market Capitalization (Source: Seeking Alpha)

As a result, the stock is now trading at its highest ever levels. This, of course, raises the question of whether it’s a good time to buy the stock. The answer depends on the investing goals and timeframes. In determining the investors, PM is best suited for now, here I take a closer look at why PM has been on the up and up recently. Here are six reasons.

#1. Market uncertainty

The first is the attractiveness of the tobacco sector as such. There's been uncertainty in the stock markets recently, which can make classic defensives more attractive. This is borne out by the fact that the MCap weighted six month price returns for these five tobacco stocks is at 24% year-to-date compared with a much smaller 12.6% increase in the S&P 500 index (SP500) and 12.9% rise in the NASDAQ-100 (NDX).

#2. Rotation towards undervalued stocks

It helped further that as the year began, tobacco stocks were undervalued compared to their past market multiples. 2023 was a bad year for them, with the MCap weighted average decline of 7.6% for the five stocks under consideration.

Of them, only Japan Tobacco (OTCPK:JAPAY) saw an increase last year, while PM was down by 7%. As a result, when I first checked on PM this year in February, the average of its trailing twelve months ("TTM") and forward price-to-earnings ("P/E") ratio was 6% lower compared to its five-year averages. This upside had exhausted by the last time I checked in May. Yet, PM has continued on an upward trajectory, which is explained by more than just market uncertainty.

#3. Healthy financials

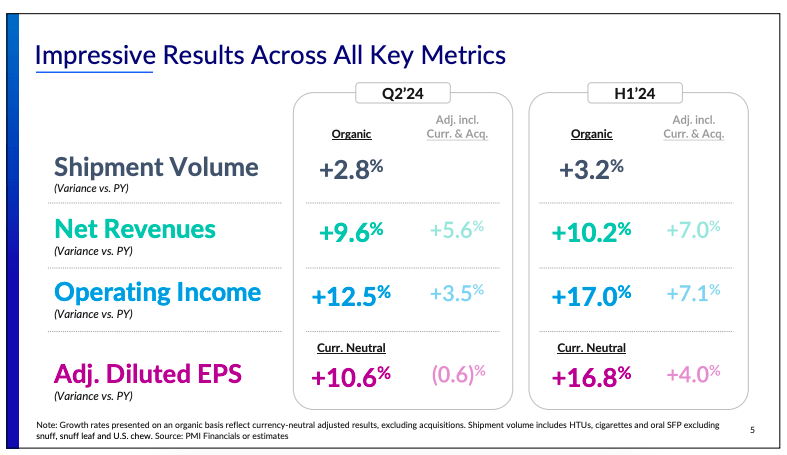

This brings me to the third point. The company's continued financial growth. Since the release of its results for the second quarter (Q2 2024) and the first half of 2024 (H1 2024) a month ago, the stock is up by over 12%. It's not hard to see why, either, after it reported double-digit increases in both revenue and profits (see graphic below).

Source: Philip Morris

The performance of its smoke-free business is particularly notable. They contributed to 38% of the total revenues and the segment's organic revenues grew by 13.6% year-on-year in the second quarter (Q2 2024). Even though this is a softening from the 24.8% YoY increase in Q1 2024, it remains higher than the overall growth of 9.6% YoY in Q2 2024 and 11% YoY in Q1 2024.

#4. Alternate path to reduced risk products

The fact that Philip Morris's heated tobacco brand IQOS is the most popular among all brands has contributed to the growth of its smoke-free products. Because of this focus, it has also avoided recent blockages related to vaping products in the US market due to their high popularity among teenagers. This has given it an edge in the transition to reduced risk products.

Further, the marketing denials for vapes for competitors like British American Tobacco (BTI) and Altria (MO) are now resolving (see here and here), resulting in greater buoyancy for tobacco stocks as such. They also potentially open up the path to the expansion of PM's vaping products in the future.

This isn't to say that heated tobacco will remain trouble free. The company has recently been said to fund research to market IQOS, which PM has denied. While so far, there have been no adverse consequences for the company stemming from the development, it's worth looking out for, especially after issues faced for other smoke-free products.

#5. Guidance upgrade

For now, though, it's all going rather well. The company upgraded its guidance for the adjusted diluted earnings per share ("EPS") for the second time for 2024. At the midpoint of the initial guidance range, it expected 8% growth, and it now expects a number of 12%. This is a positive for its market multiples and future dividends.

Source: Philip Morris

#6. Dividend yield and stability

Dividends are the big reason for tobacco stocks' attractiveness, including PM. Among its peers, the PM’s forward dividend yield isn’t the highest at 4.4% (see table below), but there’s still a case for it.

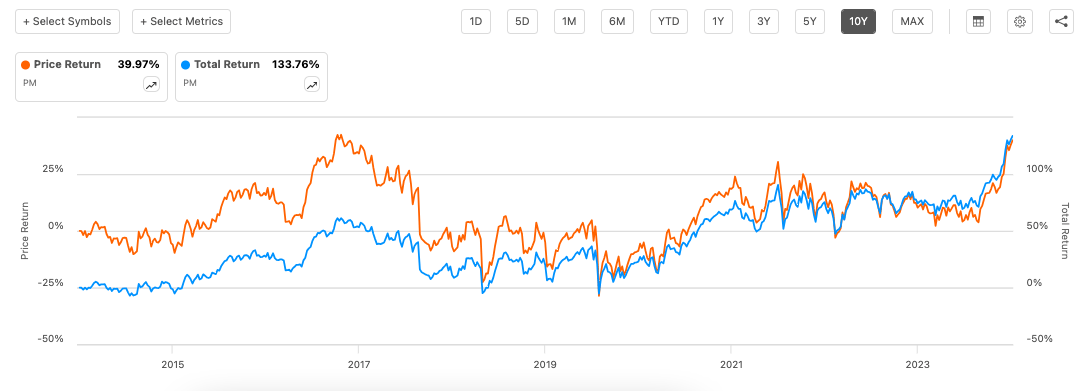

The company has grown dividends for 15 years, and the total returns on the stock at ~134% over the past 10 years are 94 percentage points higher than the price returns (see chart below), to which dividends have made a difference. With an earnings upgrade, the likelihood of further dividend growth is even higher. And with the company's success in reduced risk products, there's greater assurance of the longevity of dividend growth as well.

Source: Seeking Alpha

Price and Total Returns (Source: Seeking Alpha)

The market multiples are elevated

However, even with the upgrade in earnings, at the midpoint, the forward non-GAAP P/E ratio is at 18.7x, which is high compared with its five-year average of 15.8x. Similarly, based on the midpoint of the guidance range for the reported EPS at USD 5.89-6.01, the forward GAAP P/E is at 20.15x compared to the five-year average of 16.3x. Also, the TTM P/E is at 20.6x, the highest level in over five years.

What next?

On average, the forward P/Es indicate that PM can correct by over 17% now. The 4.4% forward dividend yield wouldn't make up for it, resulting in a short-term loss for any investor looking to buy the stock right now. However, considering that the price returns on the stock have been just 40% over the past 10 years, it's unlikely that it's seen as an investment for capital gains.

For investors with a medium-to-long term timeframe looking for passive returns, this can still be a good time to buy the stock, especially as the forward non-GAAP P/E starts looking better for the next couple of years. Any stock price dip would be a good time to buy more of PM. I'm retaining a Buy rating.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.