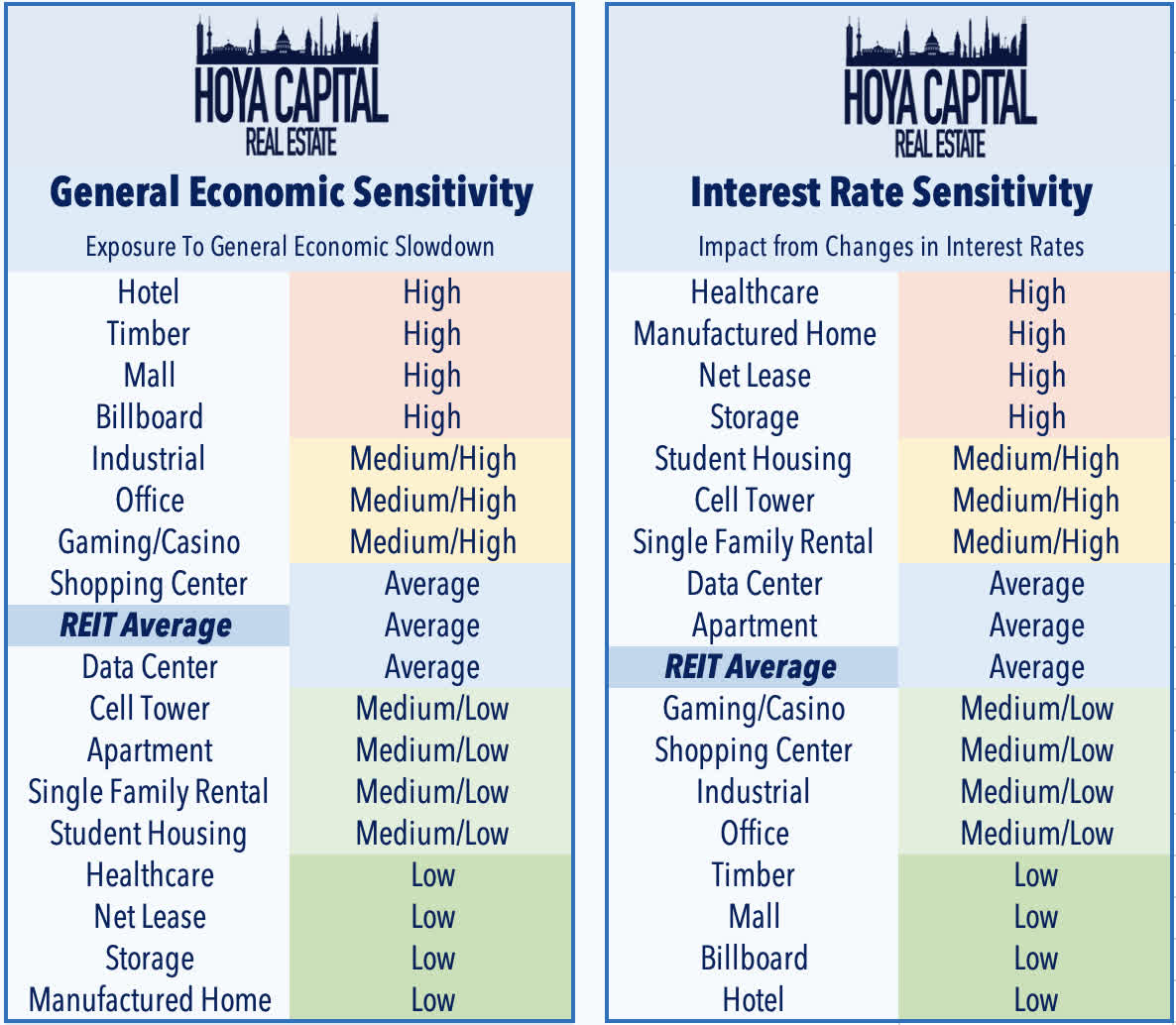

Losers And Winners Of REIT Earnings Season

Summary

- Light at the End of the Tunnel? Two years of persistent rate-driven pressure on residential and commercial real estate markets appears to finally be abating, not a moment too soon.

- Amid an otherwise underwhelming earnings season across the broader equity market, real estate earnings results were notably better than expected, providing an added uplift to the rate-driven rebound.

- Upside surprises at the property-sector level included Retail, Sunbelt Apartment, NYC/Sunbelt Office, Senior Housing, and Industrial REITs. Ten REITs announced dividend increases this earnings season.

- There were few major "bombshells" this earnings season, but we did observe ongoing pockets of distress among some of the most highly levered REITs. Five REITs reduced their dividends.

- With recession fears ever-present, REITs are not entirely out of the woods yet. Losers included Self-Storage, Hotel, Farmland, and Mortgage REITs. The West Coast - particularly California - was a region of notable weakness.

Matteo Colombo

Winners & Losers of REIT Earnings Season

iREIT®+HOYA Capital

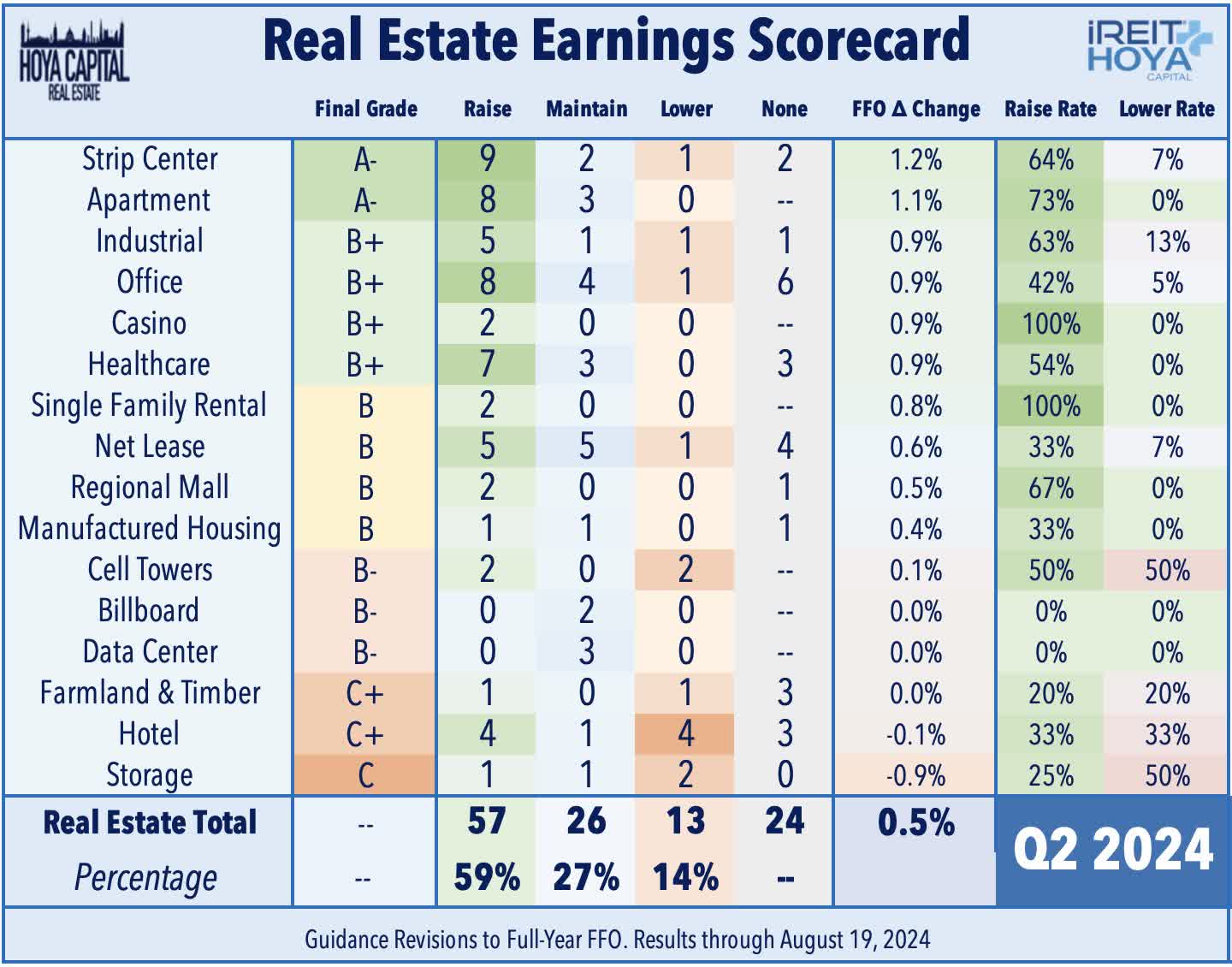

In our Earnings Recap report last week, we provided a sector-by-sector scorecard across each of the major REIT property sectors and highlighted some quick incremental positives and negatives we observed this earnings season. As discussed, amid an otherwise underwhelming earnings season across the broader equity market, real estate earnings results were notably better than expected, providing an added uplift to a broader REIT rebound fueled by a long-awaited retreat in benchmark interest rates. Of the 96 equity REITs that provide full-year FFO guidance, 57 (59%) raised their outlook, while 13 (14%) lowered - well above the historical second-quarter average "raise rate" of 40-45%. By comparison, FactSet reports that 53% of the 272 S&P 500 constituents that provided Earnings Per Share ("EPS") guidance issued a positive revision. By comparison, during first-quarter earnings season, 41% of REITs raised their full-year FFO outlook, while 11% lowered their guidance.

iREIT®+HOYA Capital

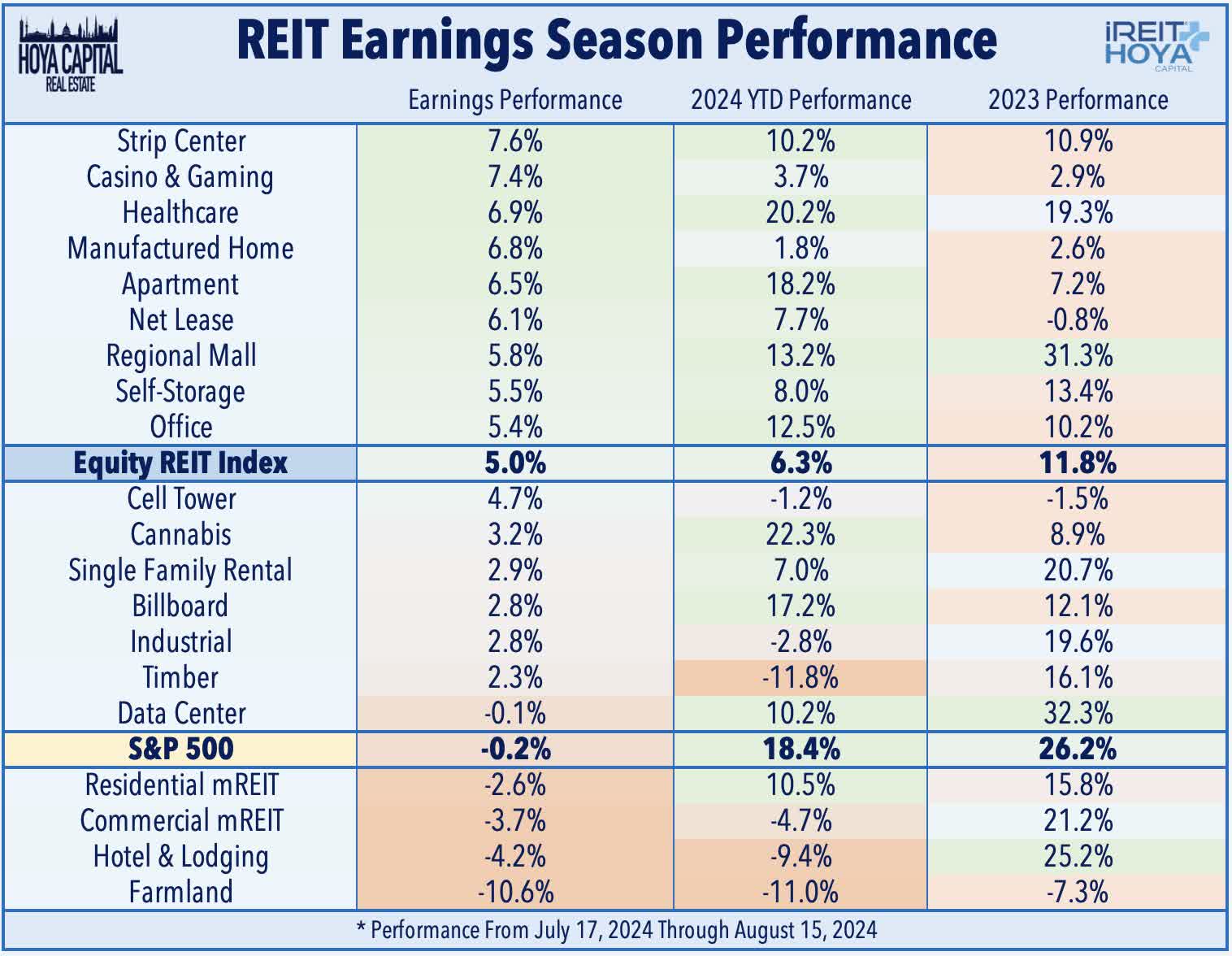

Since the start of earnings season in mid-July, REITs have delivered notable outperformance relative to the broader equity market. The Equity REIT Index (VNQ) has gained 5.0% during this time - outpacing the -0.2% returns on the S&P 500 - a period that also corresponds to a roughly 50 basis point retreat in the benchmark 10-Year Treasury Yield from 4.30% to 3.80%. With some exceptions, price performance across the various property sectors has generally corresponded with the quality of earnings reports: Strip Center REITs have led the gains on the upside, followed by Casino, Manufactured Housing, and Apartment REITs. On the downside, Farmland REITs have lagged with double-digit percentage declines, followed by Hotel, Mortgage, and Data Center REITs. Self-storage REITs were a notable exception, outpacing the REIT Index despite disappointing results. In the other direction, Industrial REITs lagged despite delivering surprisingly strong results.

iREIT®+HOYA Capital

Winners of REIT Earnings Season

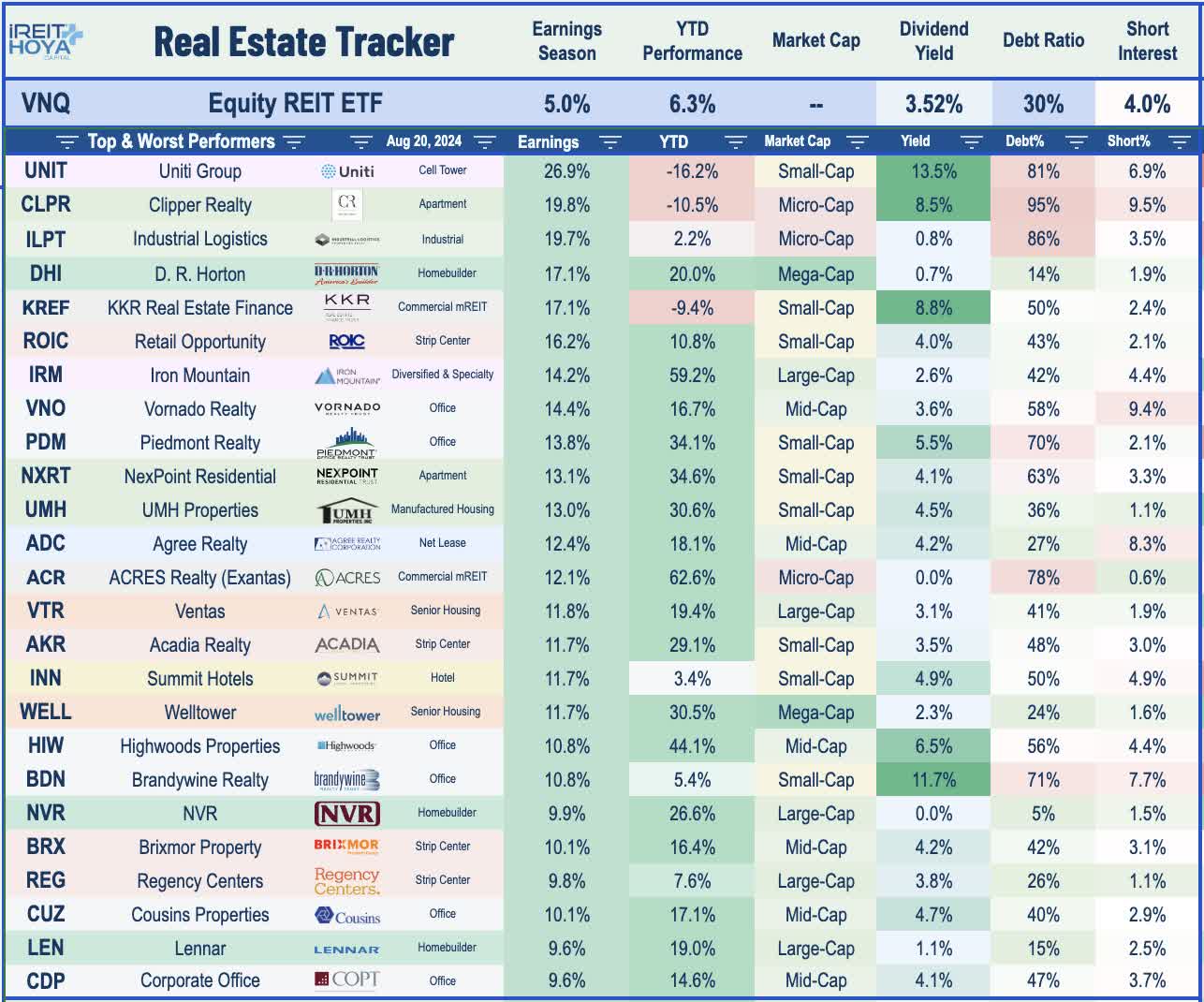

At the individual level, fiber-optic network owner Uniti Group (UNIT) rallied nearly 30% after reporting very strong bookings driven by hyperscale and AI-focused demand, and provided Pro Forma financials on its pending merger with its former parent firm, Windstream, which eased some investor concerns. Micro-cap apartment REIT Clipper Realty (CLPR) was the second-best performer with gains of nearly 20% after reporting particularly strong leasing performance in its New York City-focused portfolio and maintaining its dividend representing an 8.5% yield. Among mid and large-cap REITs, business storage REIT Iron Mountain (IRM) was the top performer after reporting impressive leasing activity in its fast-growing data center business, prompting a 10% increase in its quarterly dividend - one of 60 REITs that has raised their dividend this year. Retail Opportunity (ROIC) - a small-cap strip center REIT that owns 94 strip centers on the West Coast - also jumped more than 15% this earnings season on reports that private equity firm Blackstone (BX) is in early-stage talks to purchase the firm. Further details were limited, and sources told Reuters that "no deal is certain and another bidder for ROIC could emerge." ROIC would become the 8th REIT that has been taken private by Blackstone and its affiliates since the start of 2021, and the third this year.

iREIT®+HOYA Capital

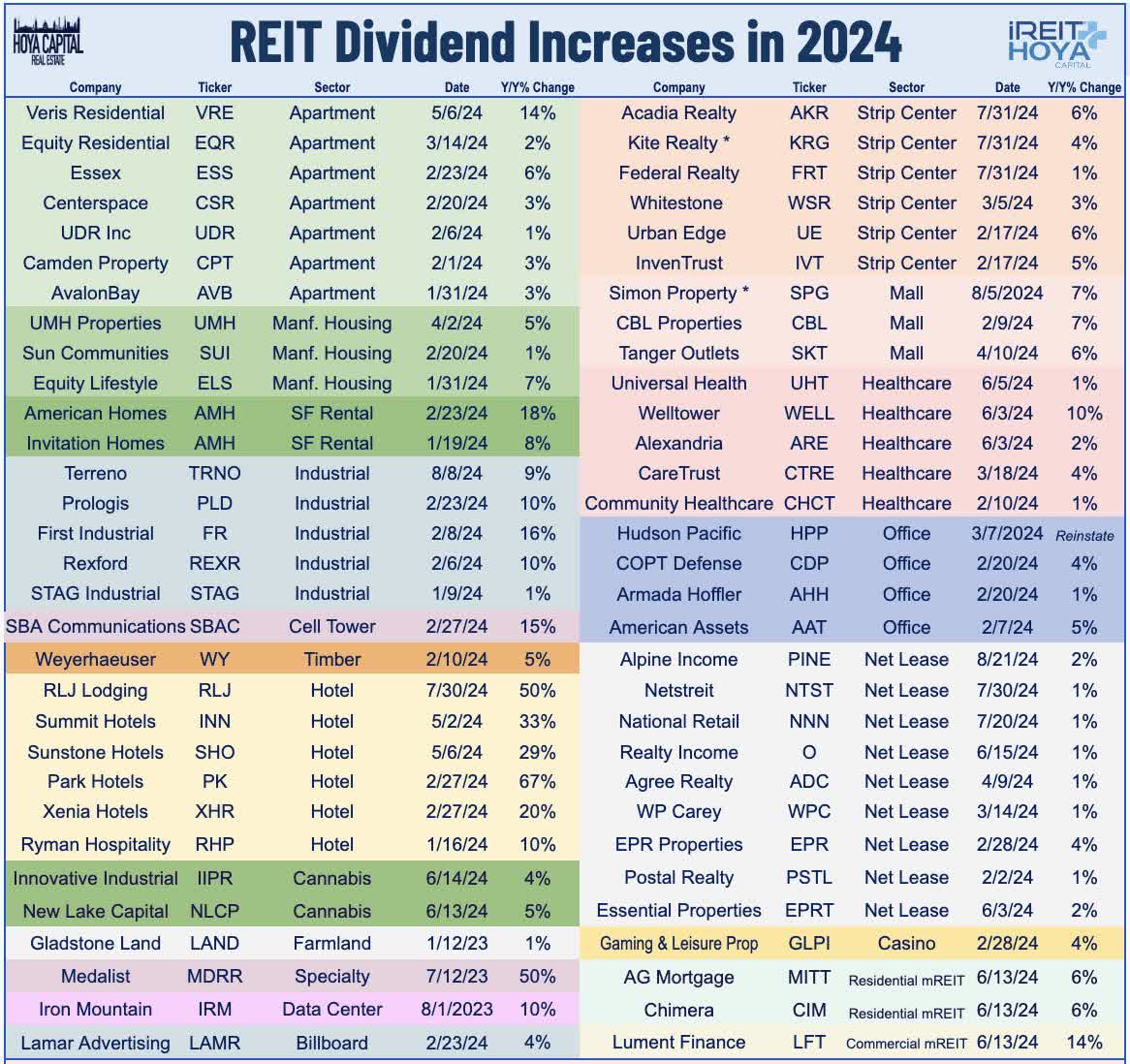

Upside surprises at the property-sector level included Retail, Sunbelt Apartment, NYC/Sunbelt Office, Senior Housing, and Industrial REITs. Favorable expense trends (disinflation) and moderating supply growth drove incremental upside. Ten REITs announced dividend increases this earnings season - led by a trio of strip center and net lease REITs - lifting the full-year total across the sector to 62. As we'll discuss in our State of the REIT Nation report later this week, the average REIT dividend payout ratio was 69% in the second quarter - an improvement from the 78% in the first quarter and well below the historical average dividend payout ratio of around 80%. Below, we discuss the five property sectors that were winners of earnings season.

iREIT®+HOYA Capital

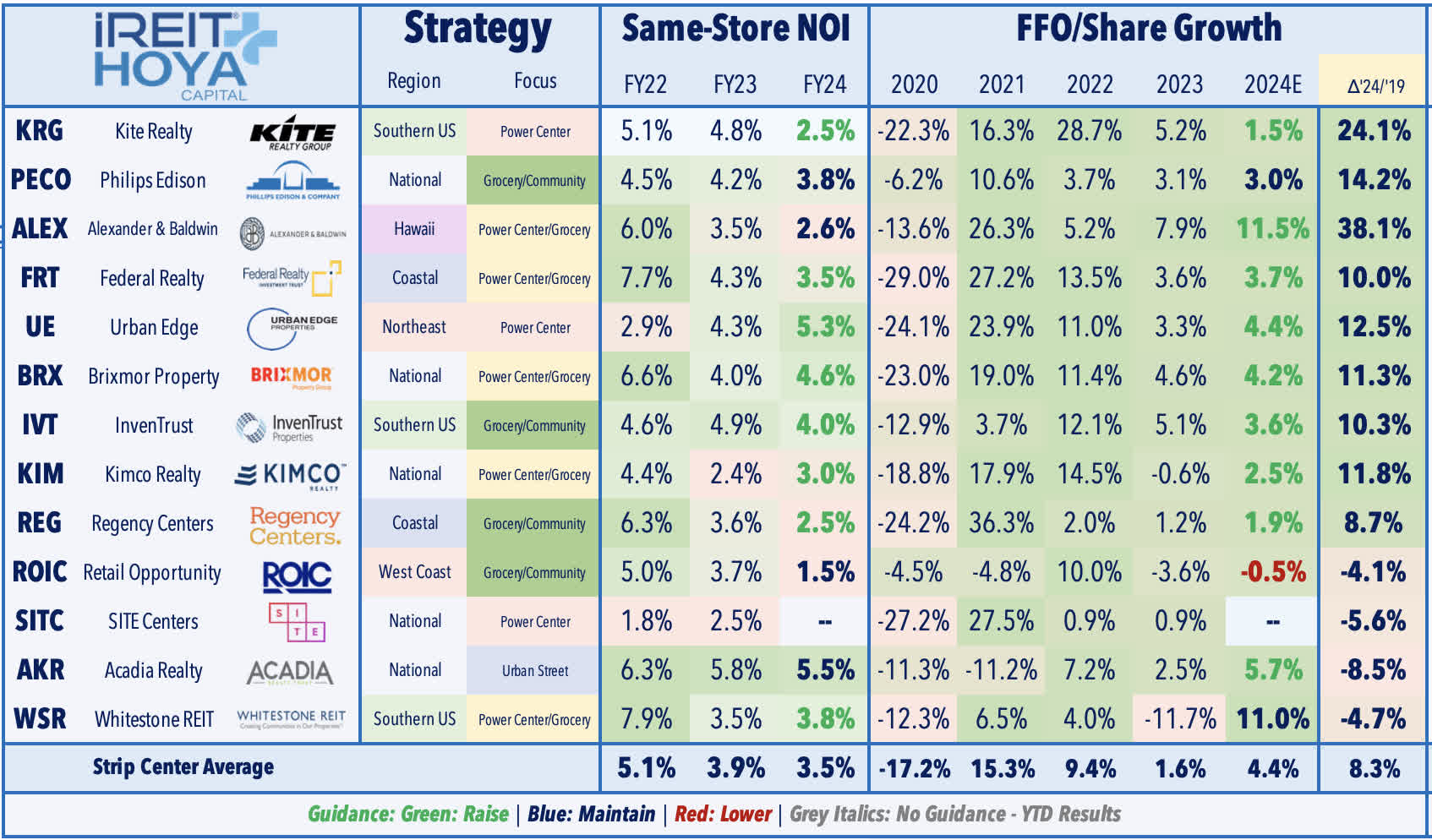

Winner #1: Strip Center REITs

Strip Centers: (Final Grade: A-) Strip Center REITs were a notable upside standout with a near-perfect slate of upward guidance boosts - and a handful of dividend hikes - as record-high occupancy rates resulting from a decade of limited new development fueled another quarter of double-digit rental rate spreads. Continuing a trend of better-than-expected results stretching back to late 2021, nine strip center REITs raised their full-year FFO outlook while just one lowered their FFO target as demand for "big box" space has significantly exceeded the available supply despite the several recent high-profile retail bankruptcies. Strip Center REITs reported that blended rent spreads averaged 16.0% in Q2 - the strongest on record - while occupancy rates also set fresh record-highs at 95.6%. These REITs continue to report healthy demand for the vacated Bed Bath locations - space that is generally on the upper end of the 'quality' spectrum - with several REITs highlighting impressive re-leasing rent spreads of over 50% on this space. Small-shop occupancy - which has generally lagged since the pandemic - also improved across the board, with several REITs identifying this as an area of focus and catalyst for growth.

iREIT®+HOYA Capital

- FFO Guidance: 9 Raise, 2 Maintain, 1 Lower (+120bps Average)

- NOI Guidance: 7 Raise, 4 Maintain (+30bps Average)

- Positives: Robust leasing activity, renewal spreads near record highs

- Negatives: External growth muted, REITs remain net sellers

- Notable Winners: Acadia Realty (AKR), Kite Realty (KRG)

- Notable Losers: Whitestone (WSR), Saul Centers (BFS)

iREIT®+HOYA Capital

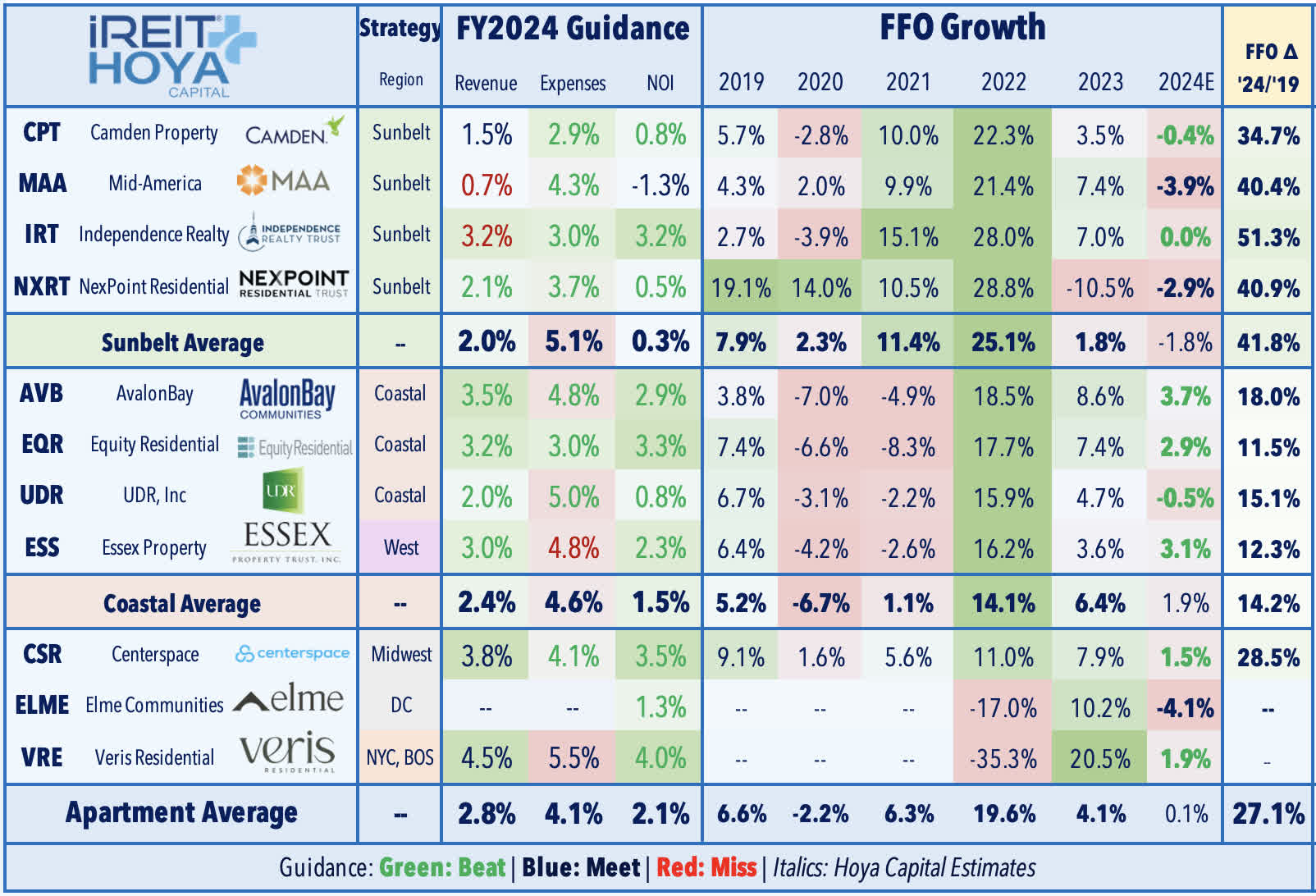

Winner #2: Apartment REITs

Apartment: (Final Grade: A-) Expectations were high for multifamily REITs this earnings season after a very strong first quarter, and while rent growth metrics were mildly disappointing, it was still a rather impressive quarter nonetheless in which 8 of the 11 REITs raised their full-year outlook. Buoyant mid-single-digit rent growth on renewals (+4.3% in Q2 and +4.1% in July) and relatively steady occupancy trends helped to offset lower new lease rates, but even these new lease spreads haven't seen the sharp negative prints that were once expected (0.0% in Q2 and -0.6% in July), resulting in blended rent growth of 1.4% in both Q2 and in July. Importantly, while buoyant rents fueled the upside, expense pressures - notably on insurance renewals and property tax assessments - appear to finally be abating after several quarters of persistent negative surprises. Ten of the eleven REITs that provide same-store Net Operating Income guidance favorably revised their outlook, driven primarily by lower same-store expenses. Sunbelt-focused REITs were the upside surprises as rent growth trends were only mildly softer than their coastal peers despite record-setting levels of supply growth in recent months.

iREIT®+HOYA Capital

- FFO Guidance: 8 Raise, 3 Maintain (+110bps Average)

- NOI Guidance: 9 Raise, 1 Maintain (+60bps Average)

- Positives: Favorable expense trends, Sunbelt stronger than feared

- Negatives: New rent growth moderating again after early-2024 rebound

- Notable Winners: NexPoint Residential (NXRT), Camden Property (CPT)

- Notable Losers: BRT Apartments (BRT), Apartment Investment and Management Company (AIV)

iREIT®+HOYA Capital

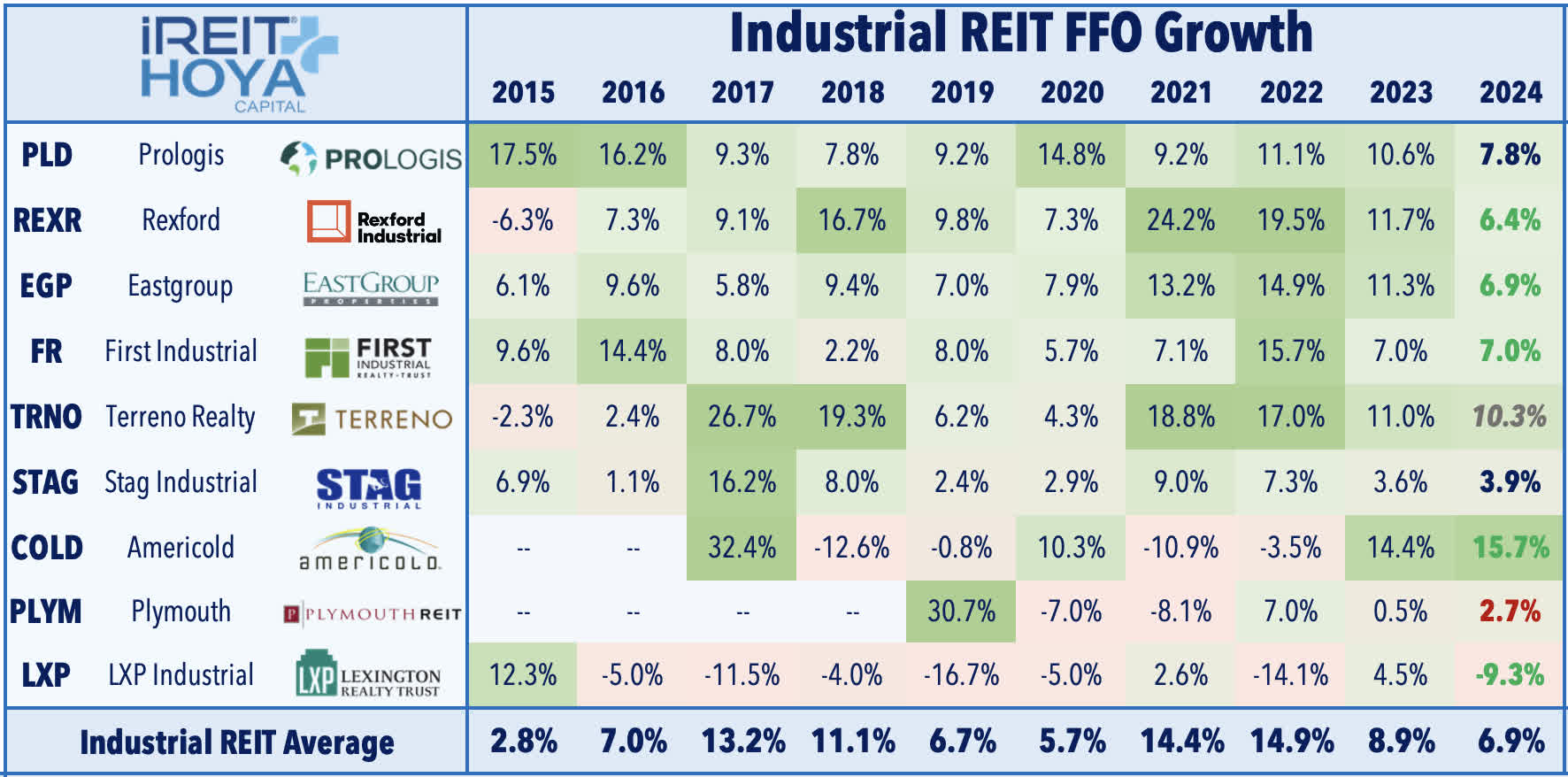

Winner #3: Industrial REITs

Industrial: (Final Grade: B+) On the heels of an uncharacteristically poor earnings season in Q1, industrial REITs reported surprisingly solid results, with five of the eight REITs raising their full-year FFO outlook. Encouragingly, leasing spreads accelerated slightly in the second quarter to around 40%, albeit on slightly lower volumes. Prologis (PLD) - the largest industrial property owner in the nation - noted “subdued but improving” demand logistics alongside a moderation in supply growth. Commenting on macro conditions, Prologis estimated that global market rents declined 2% during the quarter, but commented that weakness in Southern California was responsible for 75% of this decline. Sunbelt-focused First Industrial (FR) was the upside standout of the group after reporting surprisingly strong results and boosting its full-year NOI and FFO outlook. FR commented that "fundamentals are slowly improving, although, as expected, market vacancy ticked up...decision-making remains fairly deliberate. It's still early to determine the resiliency and the pace of demand, even though we see today, indicators are pointing in the right direction." EastGroup (EGP) also reported strong results and raised its full-year outlook, citing an improved outlook on both the demand and supply front. EGP commented, "The leasing environment is slowly improving... It hasn’t been a U-turn, but kind of month by month slowly improving."

iREIT®+HOYA Capital

- FFO Guidance: 5 Raise, 2 Maintain, 1 Lower (+85 bps Average)

- NOI Guidance: 4 Raise, 4 Maintain (+30 bps Average)

- Positives: Impressive leasing activity after a weak first-quarter

- Negatives: Supply headwinds lingering until early 2025

- Notable Winners: First Industrial (FR), Americold (COLD)

- Notable Loser: LXP Industrial (LXP)

iREIT®+HOYA Capital

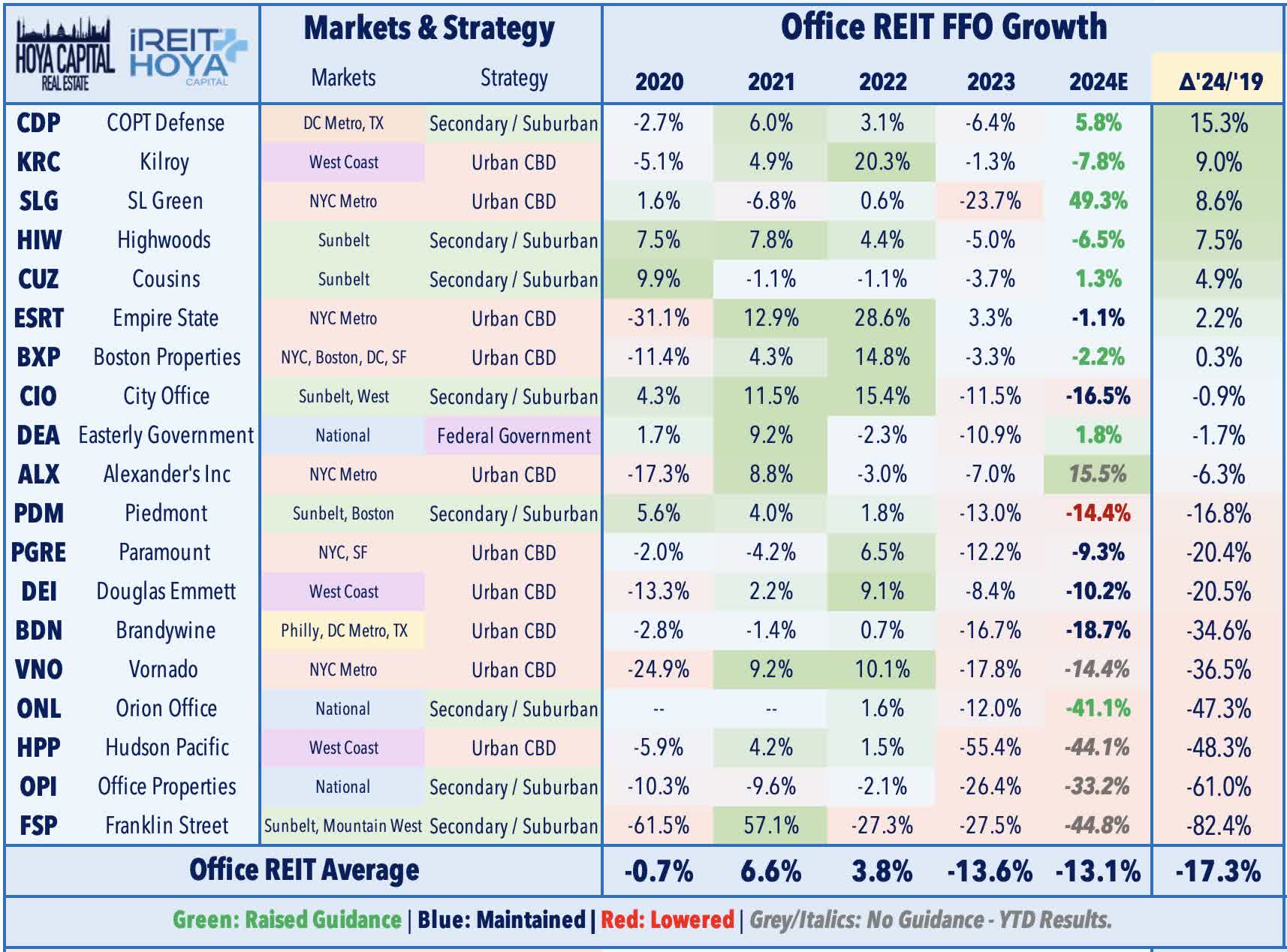

Winner #4: Office REITs

Office: (Final Grade: B+) A relatively strong earnings season for the battered office sector showed an encouraging rebound in leasing demand across many major markets outside of the tech-heavy West Coast. Of the office REITs that provide full-year FFO guidance, 8 of the 12 raised their full-year outlook. While still 20-40% below pre-pandemic levels, daily utilization rates of office properties have continued to improve nationwide, aided by a softening labor market that has awarded employers some negotiating power to pull workers back into the office. Following a relatively disappointing Q1, REIT leasing activity rose roughly 10% in Q2 to levels that are only 10% below the average pre-pandemic activity from 2017-2019. This rebound in activity helped to reverse the negative trends in rent spreads, while downward pressure in occupancy rates appeared to finally be subsiding as well. While trends in Sunbelt markets have been steadier throughout the pandemic than in Coastal markets, the rebound in recent quarters has been driven by New York City. NYC-focused Vornado Realty (VNO) - the second-largest office REIT - reported particularly strong results, as did Sunbelt-focused Cousins (CUZ).

iREIT®+HOYA Capital

- FFO Guidance: 8 Raise, 4 Maintain, 1 Lower (+50 bps)

- Positives: Leasing activity rebound, rents firming, Sunbelt strength

- Negatives: West Coast weakness, Not enough to change the narrative

- Notable Winners: Vornado, Cousins Properties

- Notable Losers: Hudson Pacific (HPP), Paramount Group (PGRE)

iREIT®+HOYA Capital

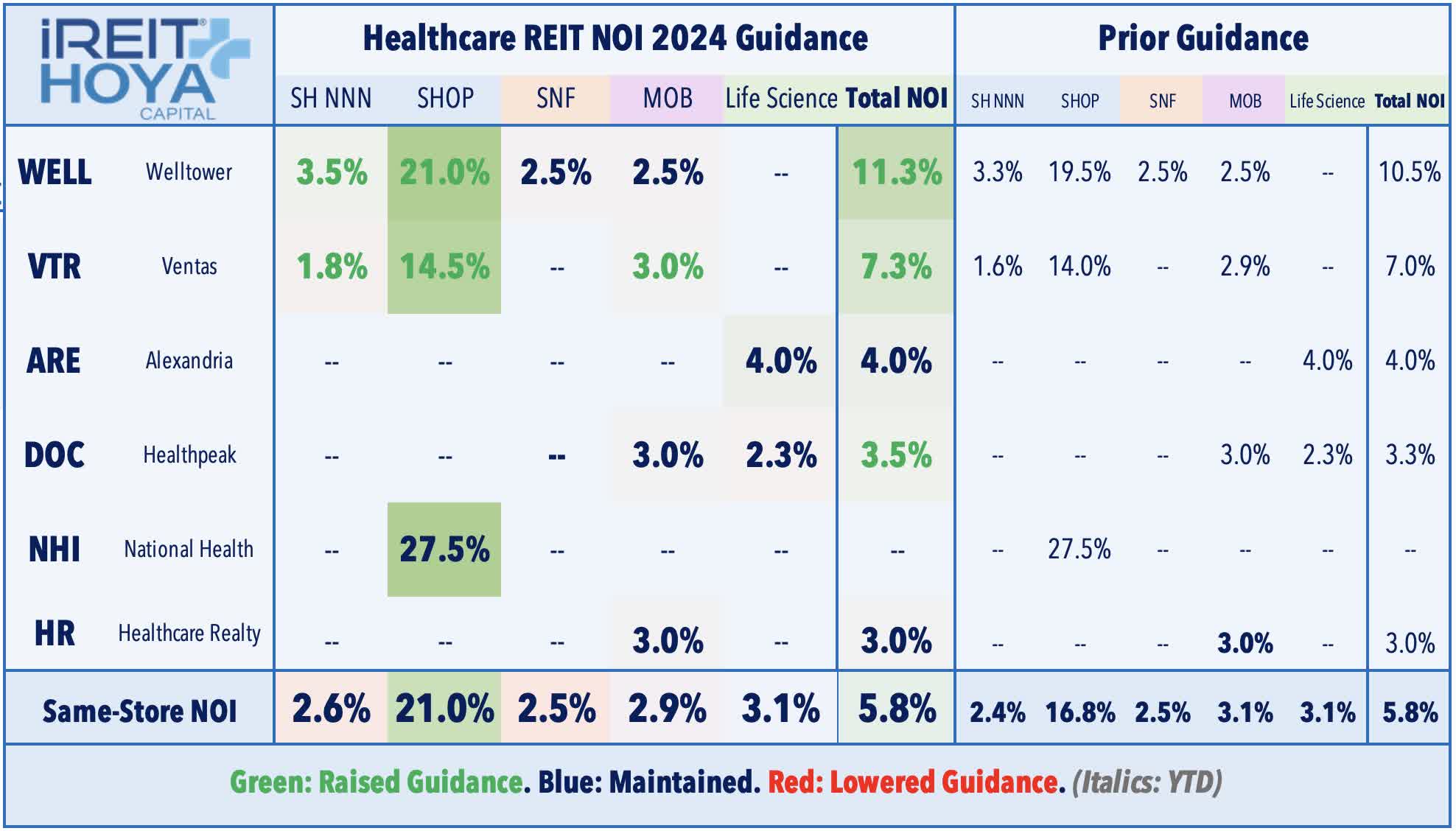

Winner #5: Healthcare REITs

Healthcare: (Final Grade: B+) Continued record-setting rent growth in senior housing and a stabilization in tenant operator health within the skilled nursing segments were the takeaways from a relatively impressive slate of reports from healthcare REITs, as seven of the ten REITs that provide full-year FFO guidance lifted their outlook - the most guidance hikes since before the pandemic. Benefiting from COLA increases, pricing power remains robust across the "private pay" space and, combined with moderating expense pressures, SH REITs have reported "unprecedented" same-store NOI growth. All three senior housing REITs - Welltower (WELL), Ventas (VTR), and National Health Investors (NHI) - raised their full-year FFO outlook, while three of the four Skilled Nursing REITs raised their guidance. Welltower now expects full-year FFO growth of 14.6%, driven by its seventh-straight quarter of 20%+ NOI growth in its senior housing segment. Skilled nursing trends have also improved over the past several quarters, but there remain pockets of distress among several smaller operators. Sabra Healthcare (SBRA) - which owns a mix of skilled nursing and senior housing facilities - was an upside standout, noting that SNF occupancy jumped 150bps in Q2 to 79.0%, which helped to lift tenant rent coverage to 1.85x from 1.79x last quarter. Results from Medical Office Building ("MOB") and Life Science-focused REITs were generally in line with expectations, while results from hospital-focused Medical Properties (MPW) were less dire than some feared.

iREIT®+HOYA Capital

- FFO Guidance: 7 Raise, 3 Maintain (+70 bps Average)

- NOI Guidance: 3 Raise, 2 Maintain (+50 bps Average)

- Positives: Senior Housing, Skilled Nursing recovery continues

- Negatives: Lingering operator issues, especially "public-pay" exposure

- Notable Winners: Welltower, Ventas

- Notable Loser: Community Healthcare (CHCT)

iREIT®+HOYA Capital

Losers of REIT Earnings Season

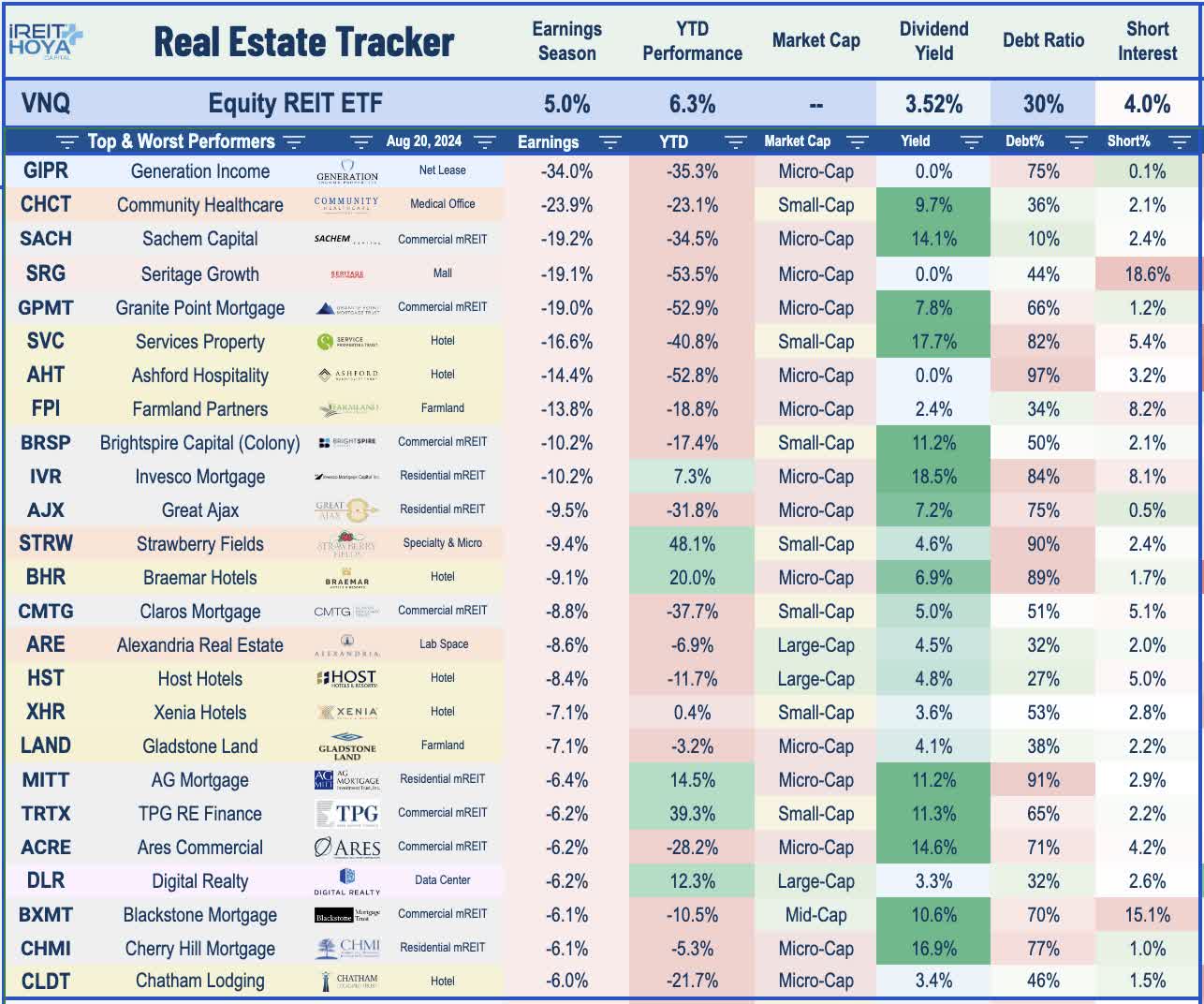

There were few major "bombshells" this earnings season, but we did observe ongoing pockets of distress among some of the most highly levered small-cap REITs, which had entered the rising-rate environment with significant variable rate debt exposure. Micro-cap net lease REIT Generation Income (GIPR) - which has seen its interest expense explode from roughly 40% of its net operating income to 65% of its NOI - dipped nearly 35% after slashing its dividend "to conserve cash during what we continue to expect will be a tumultuous economic period." GIPR was one of four REITs to reduce its dividend this earnings season, joined by four commercial mortgage REITs - Blackstone Mortgage (BXMT), Claros Mortgage (CMTG), Brightspire (BRSP), and micro-cap Sachem Capital (SACH). We've now seen 14 REITs reduce their dividend this year - nine of which have been mortgage REITs.

iREIT®+HOYA Capital

On the topic of distress, mall owner Seritage Growth (SRG) - a former REIT that emerged from the Sears bankruptcy - dipped another 20% this earnings season after it reported second-quarter results showing continued slow progress on its years-long liquidation, which began in early 2022. Elsewhere, small-cap Community Healthcare - which owns a mix of medical office and hospital facilities - dipped nearly 25% after it reported rent collection issues from one of its larger hospital tenants, an unsurprising development amid lingering tenant issues reported by embattled hospital REIT Medical Properties Trust (MPW). The West Coast - particularly California - was a region of notable weakness, particularly within the office sector. Below, we discuss the five property sectors that were winners of earnings season.

iREIT®+HOYA Capital

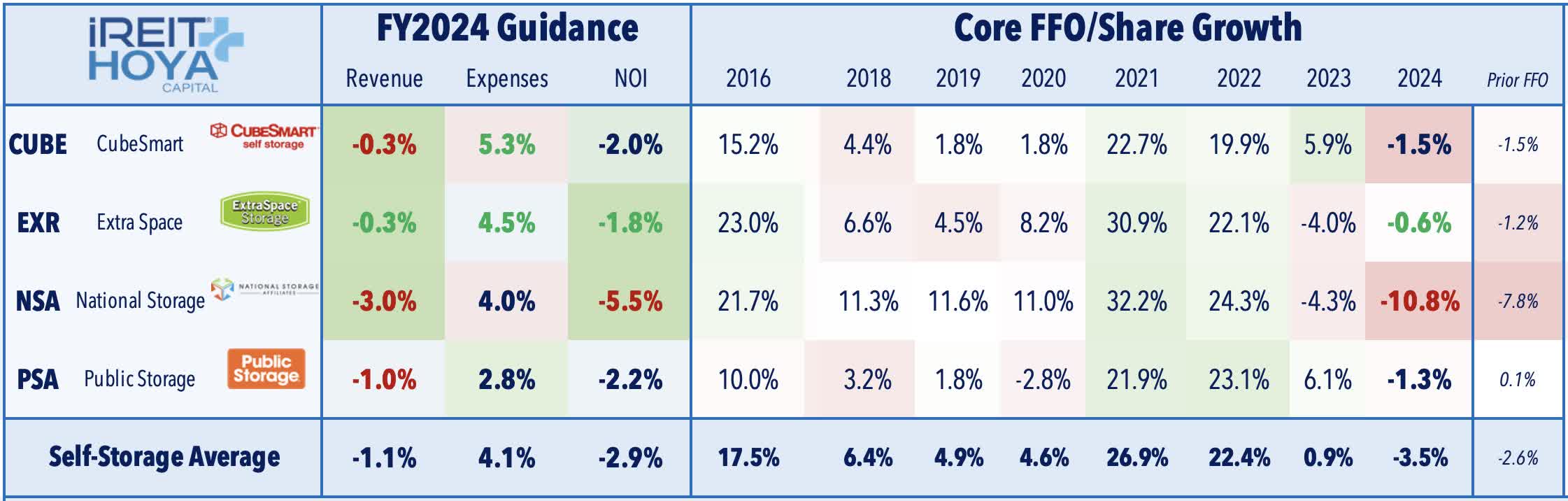

Loser #1: Self-Storage REITs

Self-Storage: (Final Grade: C) Results from self-storage REITs showed that soft fundamentals dragged into the second quarter and into July, as muted housing market activity and elevated supply growth have kept downward pressure on new lease rates. Muted move-out activity - and relatively buoyant low-single-digit rent growth on existing tenants - has helped to offset the considerable weakness in new lease rates. Despite the soft results, optimism from the sudden dip in mortgage rates sparked optimism that a rebound in housing activity may be on the horizon. ExtraSpace (EXR) was the lone storage REIT to raise its outlook, driven by a slight rebound in its occupancy rate, sticky renewal rents, and favorable improvements to the expense outlook. Pricing trends were soft, however, with EXR noting that "Street Rates" - effectively new lease rent changes - remained lower by -8% on a year-over-year basis in the second quarter - the ninth straight quarter of negative spreads - and weakened further to -12% in July. CubeSmart (CUBE) maintained its outlook and reported the "least bad" Street Rate trends of the group, noting that new lease rates were down -11% in Q2 but improved to -10% in July. Both Public Storage (PSA) and National Storage (NSA) lowered their full-year outlook and reported very soft pricing trends. PSA noted that "Street Rates" were lower by -14% from last year in the second quarter and were -12% in July, while NSA reported -15% and -14%, respectively.

iREIT®+HOYA Capital

- FFO Guidance: 1 Raise, 1 Maintain, 2 Lower (-90bps Average)

- NOI Guidance: 1 Raise, 1 Maintain, 2 Lower (-90bps Average)

- Positives: Steady renewal rents, modest move-out activity

- Negatives: Still highly competitive - weak occupancy and "Street rates"

- Notable Winner: ExtraSpace (EXR)

- Notable Loser: National Storage (NSA)

iREIT®+HOYA Capital

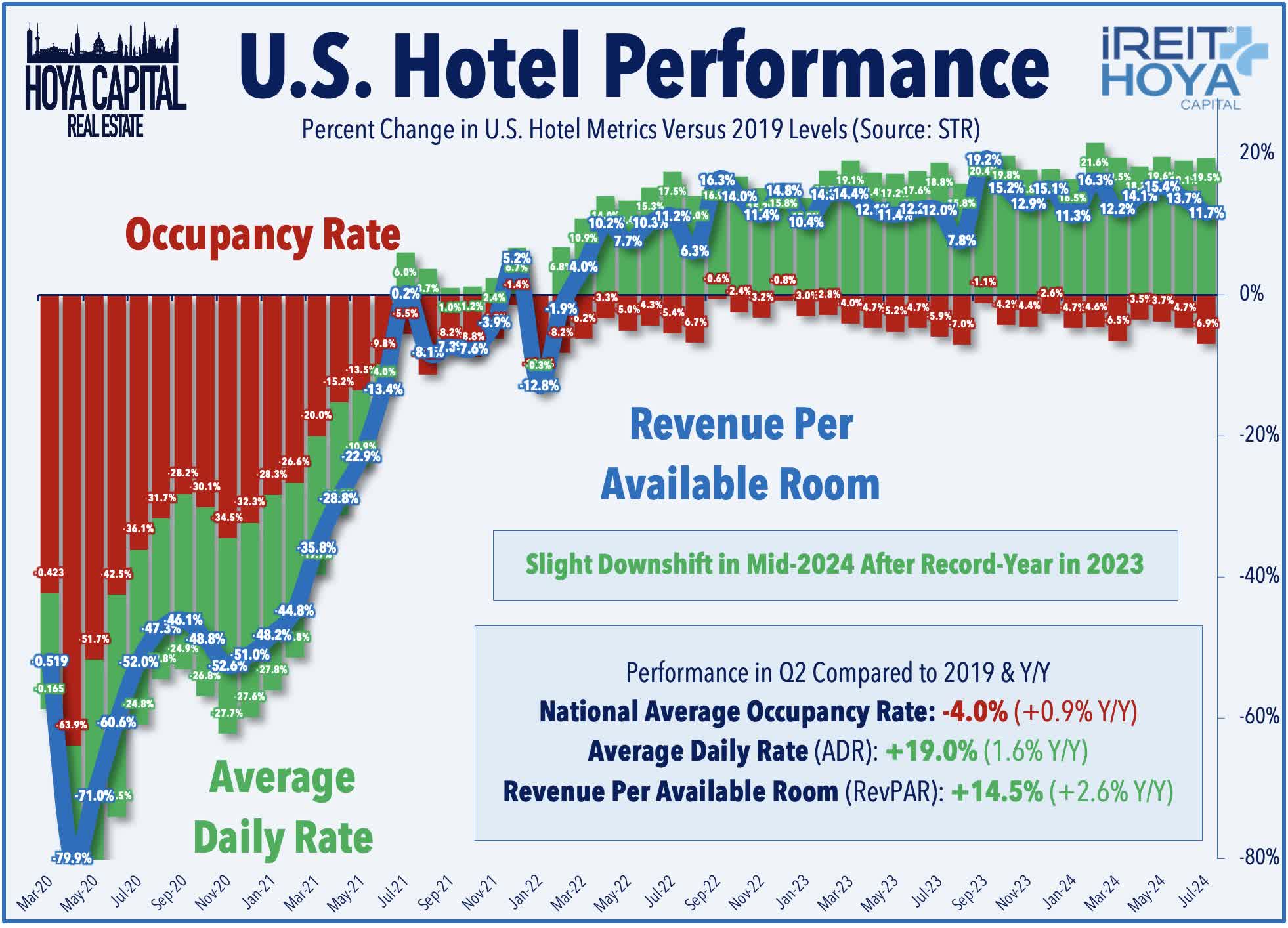

Loser #2: Hotel REITs

Hotels: (Final Grade: C+) Entering earnings season as one of the top-performing sectors over the past two years, hotel REITs lagged after reports showed clear signs of softening leisure-oriented demand, leading to a downshift in the Revenue Per Available Room ("RevPAR") outlook following a banner year in 2023. Ten of the eleven hotel REITs lowered their full-year RevPAR outlook, while four REITs lowered the full-year FFO outlook. Hotel data provider STR reported that industry-wide Revenue Per Available Room ("RevPAR") was lower by -0.5% on a year-over-year basis in July, continuing a trend of moderation in recent months after a strong start to 2024. TSA Checkpoint data shows that domestic throughput cooled to around 4% above 2019-levels in July, the softest month since mid-2023. Host Hotels (HST) - the largest hotel REIT - trimmed its full-year FFO and RevPar outlook, citing "moderating leisure transient demand." Park Hotels (PK) also lowered its RevPAR forecast, noting softer leisure trends but solid trends in its group business. Like other hotel REITs, favorable margin trends and accretive external growth have helped to offset the organic RevPAR growth moderation, with Park boosting its full-year FFO growth outlook. Sunbelt-focused Ryman Hospitality (RHP) and small-cap Sotherly Hotels (SOHO) were upside standouts. RHP significantly raised its full-year FFO outlook "to reflect the change in Tennessee franchise tax law and estimated cash interest expense savings from the OEG refinancing." Like its peers, however, RHP trimmed its RevPAR outlook, citing "continued leisure transient softness."

iREIT®+HOYA Capital

- FFO Guidance: 4 Raise, 1 Maintain, 4 Lower (-10bps Average)

- RevPAR Guidance: 10 Lower (-60bps Average)

- Positives: Favorable expense/margin trends, Accretive external growth

- Negatives: Clear signs of moderating leisure demand and softer pricing

- Notable Winners: Ryman Hospitality (RHP), Sotherly Hotels (SOHO)

- Notable Losers: Ashford Hotels (AHT), Xenia Hotels (XHR)

iREIT®+HOYA Capital

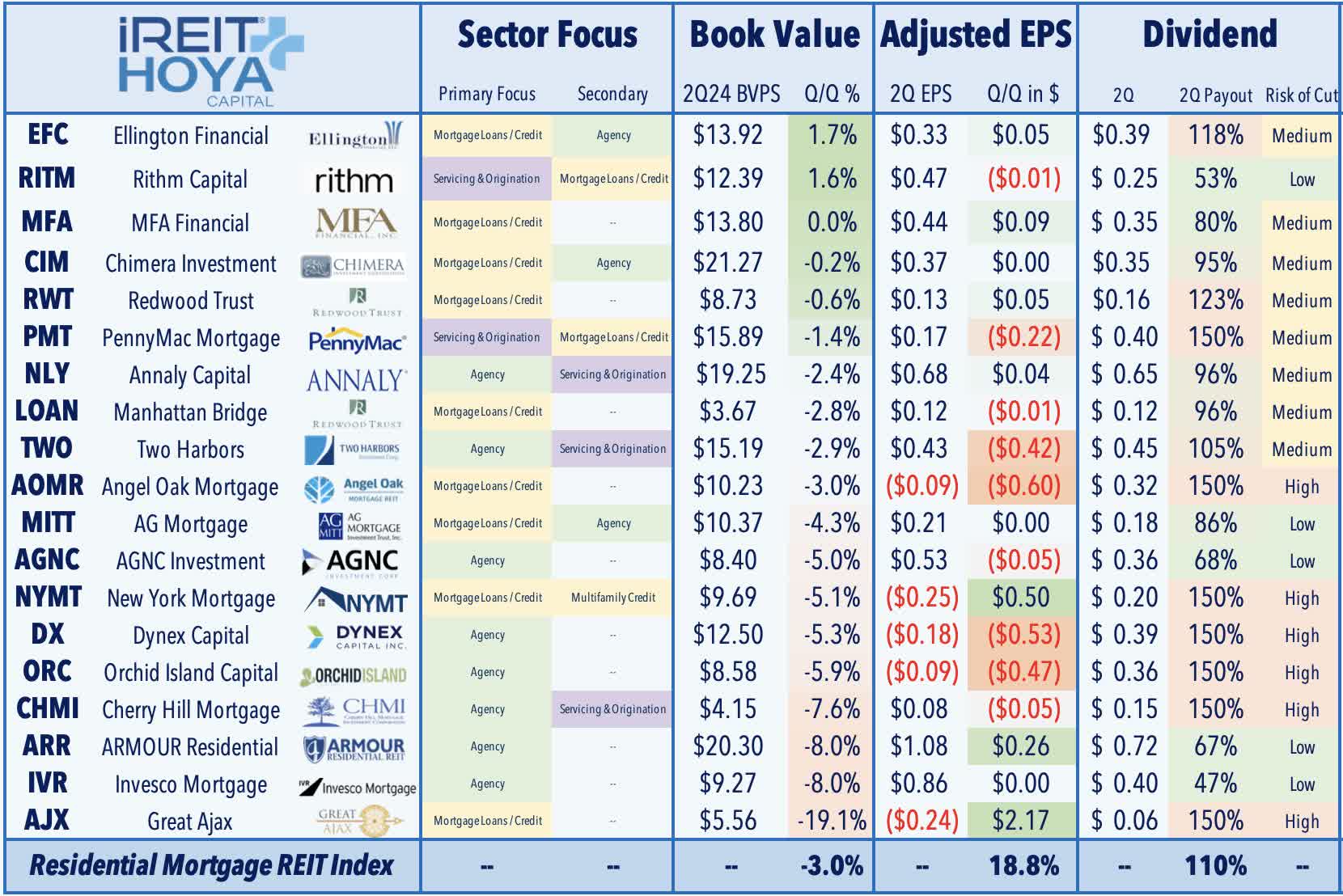

Loser #3: Mortgage REITs

Commercial mREITs: (Final Grade: C+) After posting relatively solid results throughout 2023 showing surprisingly limited loan distress, results from commercial mREITs showed a marginal acceleration in office loan delinquencies and indicated that - while widespread distress remains isolated to office assets - no property sector is necessarily "safe" if rate-driven downward pressure on property values continues. Weighed down by the most office-exposed mREITs, commercial mREITs reported an average 2.6% decline in Book Value Per Share ("BVPS") in Q2 - the steepest decline since late 2020. Four commercial mREITs announced dividend reductions this quarter. Blackstone Mortgage (BXMT) - the second-largest commercial mREIT - announced a 24% reduction in its quarterly dividend, citing a desire to "strategically deploy more capital and generate incremental earnings." BXMT noted that its portfolio was 90% performing in Q2, down from 92% in Q1. Claros Mortgage (CMTG) also reported particularly downbeat results and reduced its dividend by 60%. Granite Point (GPMT) and Brightspire (BRSP) - among the most office-exposed mREITs - also dipped after reporting a sharp dip in its BVPS due to the downgrade of additional office loans. On the upside, KKR Real Estate (KREF) - which had been among the weaker performers this year - surged after reporting that its BVPS actually increased 0.4% during the quarter to $15.24, as its CECL reserves covered the realized losses.

iREIT®+HOYA Capital

Residential mREITs: (Final Grade: C+) Results from residential mREITs were mildly disappointing in light of a rather benign interest rate environment during the second quarter, in which valuations of Mortgage-Backed Securities ("MBS") were remarkably steady. Annaly Capital (NLY) - the largest residential mREIT - reported in-line results, noting that its BVPS declined by 2.4% in Q2, as rate volatility and modestly higher Treasury rates weighed on its agency MBS portfolio, which offset strength in its MSR portfolio. We saw similar themes from other agency-focused mREITs, with the combination of hedging costs and the impact of equity issuance dragging on Book Values. Credit-focused mREITs reported stronger results, however, highlighted by modest book value increases reported by MFA Financial (MFA) and Ellington Financial (EFC). Mortgage Services Rights ("MSR") was also a source of strength in the first quarter, driving a solid BVPS increase from Rithm Capital (RITM), which was the best-performing mREIT during the rate-hiking cycle.

iREIT®+HOYA Capital

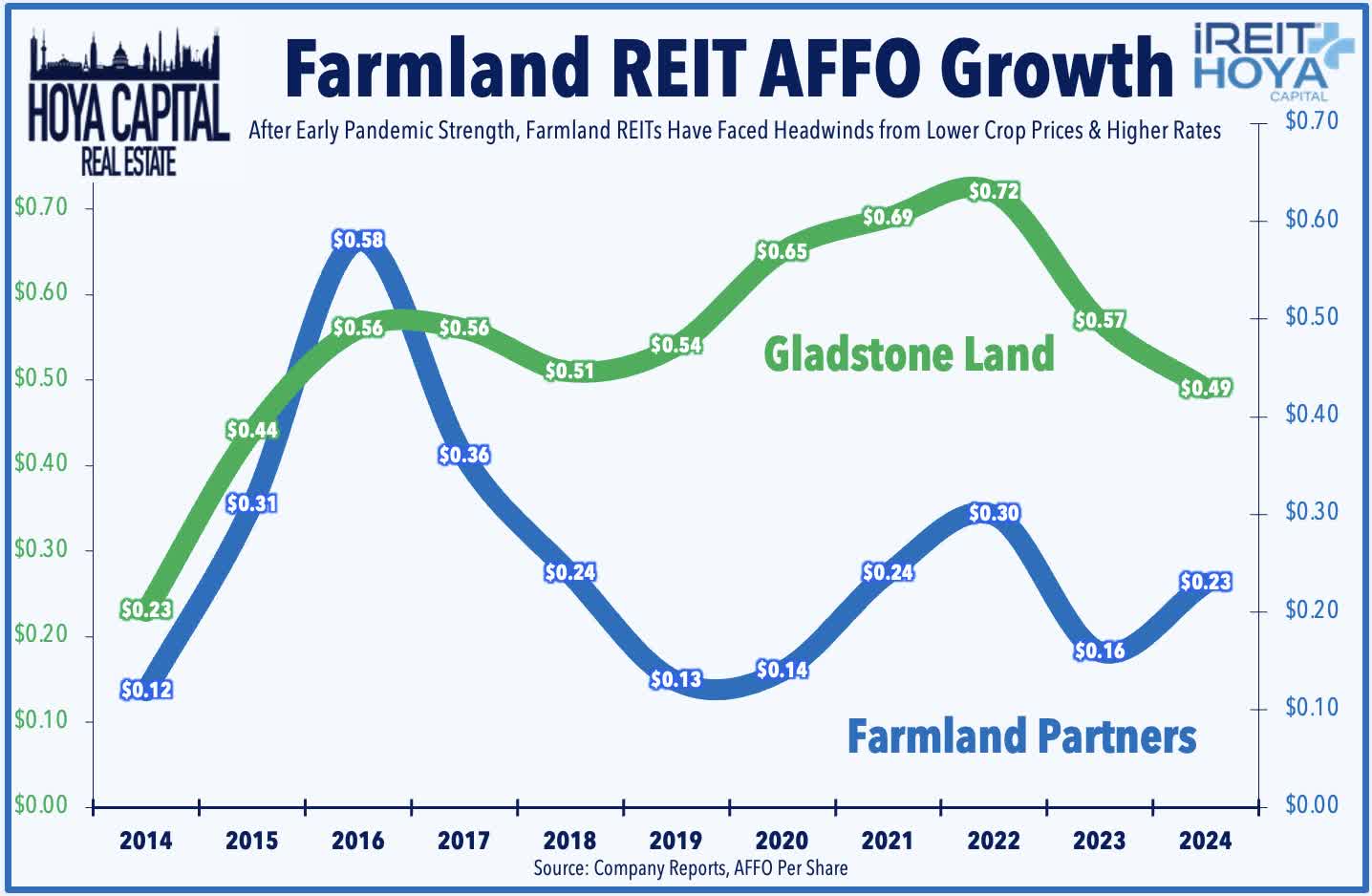

Loser #4: Farmland REITs

Farmland: (Final Grade: C+) Sluggish trends on the "goods" side of the economy were apparent in the soft results from farmland REITs, which have been pressured by a "triple whammy" of lower crop prices, lower crop yields, and higher interest rates. Farmland Partners (FPI) dipped more than 12% this earnings season despite marginally raising its full-year FFO outlook, as commentary indicated further concerns over tenant distress. FPI noted, "certain challenges for farmers in terms of their cash flow and the strength of their balance sheets... [but] by no means a crisis. There are a few farmers facing gradual levels of distress" due to lower row crop prices. Gladstone Land (LAND) reported similar tenant challenges, noting that it currently has one farm that is vacant and an additional 12 farms that are now "directly operated" following tenant defaults - consistent with the vacancy rate in the prior quarter. Positively, the once-dire water constraints in California have eased after a multi-year drought, but this improvement comes after LAND invested heavily in water resources in the region in recent years. LAND commented, "The current problem facing our farms is not water. [The problem is] lower prices for the permanent crops, and the farmers are making some money, but they're not making enough to make it worthwhile."

iREIT®+HOYA Capital

Takeaway: REITs Rebound As Rates Retreat

Two years of persistent rate-driven pressure on residential and commercial real estate markets appears to finally be abating as the worst of pandemic-era inflationary pressures subside. This 'light-at-the-end-of-the-tunnel' comes as commercial property values were approaching the critical 20% drawdown level, a level that can result in cascading distress that extends beyond the weakest players. While not out of the woods yet - especially given the ever-present recession concerns - real estate earnings results were notably better than expected, providing an added uplift to a broader REIT rebound fueled by a long-awaited retreat in benchmark interest rates. Upside surprises at the property-sector level included Strip Center Retail, Sunbelt Apartment, NYC/Sunbelt Office, Senior Housing, and Industrial REITs. Favorable expense trends (disinflation) and moderating supply growth drove much of the incremental upside. There were few major "bombshells" this earnings season, but we did observe ongoing pockets of distress among some of the most highly levered small-cap REITs which had entered the rising-rate environment with significant variable rate debt exposure. Losers included Self-Storage, Hotel, Farmland, and Mortgage REITs. The West Coast - particularly California - was a region of notable weakness. External growth remained limited, but there are signs that animal spirits are beginning to come alive.

iREIT®+HOYA Capital

For an in-depth analysis of all real estate sectors, check out all of our quarterly reports: Apartments, Homebuilders, Manufactured Housing, Student Housing, Single-Family Rentals, Cell Towers, Casinos, Industrial, Data Center, Malls, Healthcare, Net Lease, Shopping Centers, Hotels, Billboards, Office, Farmland, Storage, Timber, Mortgage, and Cannabis.

Disclosure: Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index. Index definitions and a complete list of holdings are available on our website.

iREIT®+HOYA Capital

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.