Buy Alert: 3 Undervalued 10% Yields For August 2024

Summary

- While long-term interest rates are falling in anticipation of Fed rate cuts, there are still some very attractive high-yield opportunities in the market.

- We discuss 3 that yield 10%+ right now.

- We compare them and share our take on which is the most attractive right now.

MarsBars

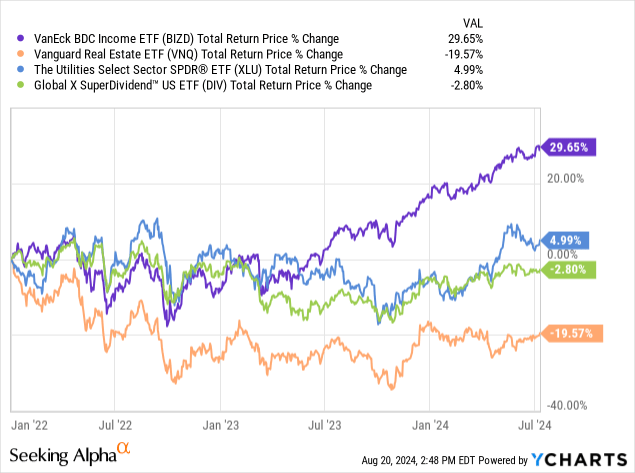

The business development company (BIZD) sector has been one of the few high-yield sectors that generated strong performance during the recent rate-hiking period by the Federal Reserve. Since the beginning of 2022 through early July, the BDC sector had massively outperformed utilities, REITs, and the broader high-yield space, as its exposure to short-term interest rates provided a major tailwind to BDC earnings and dividends. Meanwhile, rising interest rates were a major headwind to bond proxy companies like REITs and regulated utilities.

Data by YCharts

Data by YCharts

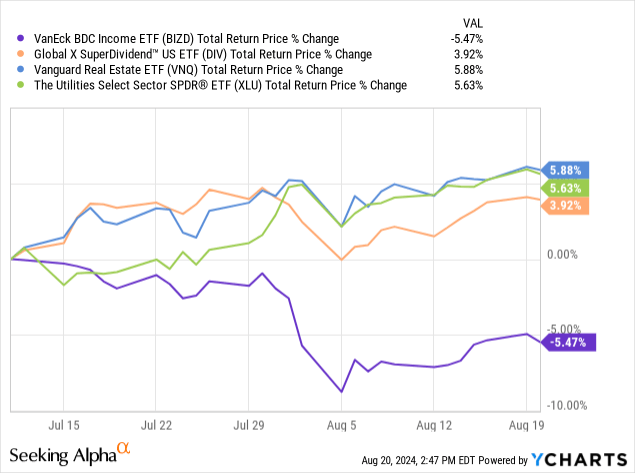

However, over the past month and a half, REITs, utilities, and the broader high-yield space have rebounded, while BDCs have pulled back. This is due to growing expectations for the Federal Reserve to implement meaningful rate cuts in the near future.

Data by YCharts

Data by YCharts

That being said, "price is what you pay, value is what you get," and this pullback in the BDC space has created some opportunities that offer attractive dividend yields that should be sustainable through a potential rate-cutting period, especially if the Fed can navigate a soft landing for the economy. The recent pullback in valuations means that these BDCs also offer meaningful value right now. In this article, we will discuss three of them that yield 10% or even more.

10% Yield #1

The first BDC we will discuss today is Morgan Stanley Direct Lending (MSDL). It stands out in particular due to the fact that 95% of its portfolio is invested in first-lien loans, and it has an attractive 0.75% base management fee, which is quite a bit lower than many of its peers. It also has considerable insider alignment, with 10.9% of the company's stock owned by insiders, and its leverage ratio is on the low side at 0.9 times. The net asset value per share has also been growing on a sequential basis, and the dividend is covered 1.26 times by net investment income, which is quite conservative for the BDC space. MSDL's exposure to first-lien loans is only increasing, with 99.1% of new investment commitments during the past quarter being in first-lien senior secured loans. They also recently declared a $0.10 per share special dividend, and their balance sheet was recently reaffirmed at investment grade. In fact, its leverage ratio is even lower than 0.9 times on a net-of-cash basis, sitting at just 0.85 times.

Its investments are also performing at a high level, with 98.1% of investments performing generally in line with their initial underwriting expectations and only 1.9% underperforming, earning the worst risk rating of four. The company also has no debt coming due this year and has a relatively small amount coming due next year, which was already taken on at a high 7.55% interest rate, so refinancing that amount may actually provide an interest rate tailwind for the company. Beyond that, they have no debt due until 2027 at the earliest, with the large bulk of it due in 2029. Overall, the non-accruals sit at a mere 30 basis points of the total portfolio at cost.

The biggest risk to MSDL is that it has nearly all of its loans invested in floating-rate loans, so it will experience an earnings headwind if interest rates are cut. However, the dividend is very well covered by net investment income, providing a cushion that should make the dividend sustainable through this period. The other major headwind is that two-thirds of the lockups for insiders prior to the BDC going public remain unlocked, so when that does happen, there could be significant selling that will unleash downward pressure on the stock price. For long-term investors who are focused purely on income, this is not a big concern, but it is something to keep in mind before buying this stock. Still, with a roughly 10% dividend yield without even including the special dividends, MSDL looks like an attractive income opportunity.

10% Yield #2

A second 10% yielding BDC that I like right now is Golub Capital BDC (GBDC). Like MSDL, it recently cut its advancement fee, making it one of the more attractive ones in the sector. Meanwhile, its dividend is covered 1.23 times by net investment income, providing plenty of cushion against any headwinds from rate cuts by the Fed. Its net asset value per share has been growing recently, which also shows that it is not overpaying its dividend and gives it flexibility to pay out special dividends on top of its regular dividend. The company prides itself on investing almost entirely in senior-secured debt, with 93% of the portfolio invested in senior-secured loans. Management claims that both are first-lien, although 86% of them are one-stop loans, which are below traditional first-lien loans, making them almost seem like second-lien loans. So, it would appear that management is overstating the security of its portfolio. Nonetheless, 93% exposure to senior secured loans is still quite conservative relative to some BDCs, and the company's track record speaks for itself. Its non-accruals sit at a mere 1% of total investments at fair value and 1.6% at amortized cost, indicating that its underwriting performance has been quite strong. Additionally, only 0.7% of the portfolio is meaningfully underperforming expectations, and 89.2% of the portfolio is either performing in line with or outperforming expectations.

The leverage ratio net of cash sits at 1.05 times, which is prudent and reasonable. Meanwhile, the company offers an attractive 10.6% dividend yield and trades at a 3.6% discount to net asset value, which is even more attractive than MSDL's 2.74% discount to net asset value. Additionally, GBDC does not have lockup expirations in the near term, removing one more risk from the equation. While MSDL is probably a bit more well-positioned to weather an economic downturn due to its greater exposure to traditional first-lien loans, GBDC's overall position remains strong.

10% Yield #3

A third 10% yielding BDC that I like right now that offers around a 10% yield is Blue Owl Capital Corporation (OBDC)(OBDE). They have two publicly traded tickers, OBDC and OBDE, which have announced their intent to merge. Both offer yields of around 10% and have discounts to net asset value of between 5.3% and 7.8%. Their portfolios are also quite similar, with first-lien and second-lien exposure of a little over 90% for OBDC and about 82% for ORCC. They have investment-grade credit ratings, and their non-accruals are at 1.4% at fair value and 3.1% at cost, which is reasonable, though not outstanding. While net asset value per share declined in the most recent quarter, net investment income did increase and cover the regular dividend by 1.3 times, making it well-positioned to weather potential Federal Reserve rate cuts.

Investor Takeaway

Between these three BDCs, if I could only buy one at the moment, it would be GBDC due to its attractive fee structure. While its discount is not as high as OBDE's or OBDC's, its portfolio is roughly similarly defensively positioned, has lower management fees, a well-covered dividend, and slightly better underwriting performance at the moment. However, I think all three deserve buy ratings at the moment, especially for investors who are buying for income and want to diversify their portfolio just in case the Fed can navigate a soft landing without having to cut interest rates too much and believe that inflation will likely remain somewhat sticky, thereby keeping the Fed from being able to cut rates too much.

By combining BDCs like these with high-quality utilities, infrastructure businesses, midstream companies, and REITs, investors can position themselves with very attractive income and strong risk-adjusted total return potential in the current environment.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.